DO & Co Stock Analysis – Too Risky Due To Total Airline Exposure

DO & CO AKTIENGESELLSCHAFT Stock Analysis – VIE: DOC

This DO & CO stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian Stock Exchange. Austria is one of the cheapest stock markets globally at the moment so please check the Austria Stock List for interesting investments.

DO & CO Aktiengesellschaft which is an Austrian catering company. It is active in segments such as airline catering, train catering, and international events catering. Businesses that will be hit severely due to the current COVID situation.

DO & CO stock price overview

A look at DO & CO stock price chart shows the severe hit the stock took due to COVID but also that the management delivered value to shareholders over the past decades as the stock quintupled. Given that the market capitalization is just 449 million, there might be more room for growth in case the COVID situation gets resolved and life returns to normal.

However, we can also see that the stock has been very volatile over the years. Consequently, we can expect the same for the business. The airline business is very delicate and extremely cyclical, a thing to keep in mind before investing in DO & CO stock as 72% of revenues are directly exposed to airline travel.

DO & CO stock analysis – business overview

DO & CO’s business is catering which is a very difficult business to be in at the moment.

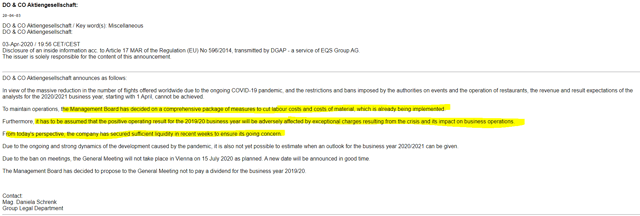

The company announced that their 2020 targets will not be met but that it will remain a going concern. We will take a look at the balance sheet to see the real perspective below.

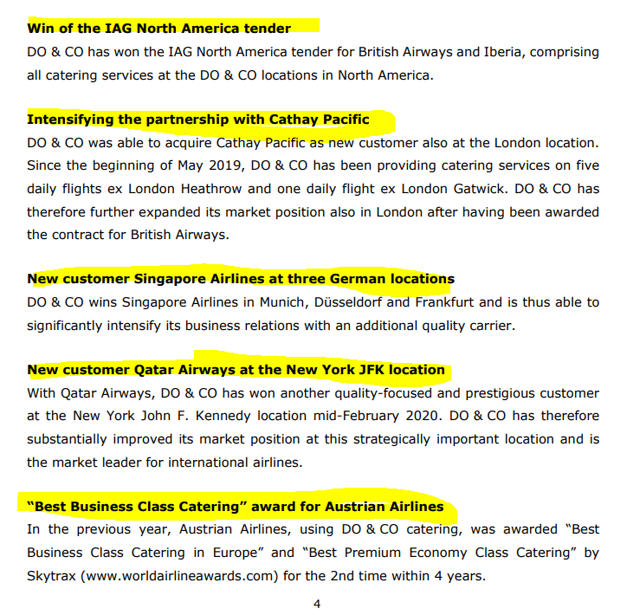

No matter the situation, DO & CO is taking over all the catering services for British Airways at London Heathrow and for that, they are building the largest gourmet kitchen in Europe. They also took over the work for Iberia, which is part of the same group as British Airways, IAG. They also won the IAG North America tender, they will continue to supply Turkish airlines for another 15 years and a many other businesses. This explains the high organic growth rate and one thing is key in such a business – scale. When the operations are set up, there is not a big difference in overhead cost for servicing one or 5 airlines.

The problem is that there is not nuch flying and not even Formula 1 racing where they also cater for 18 races and have been doing so for 28 years.

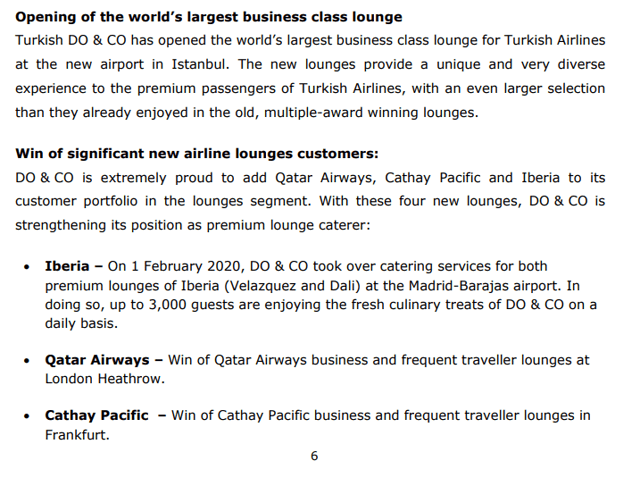

Their restaurant, lounges and hotel business are also closely related to aviation. For example, the largest business lounge at the new Ataturk airport in Turkey is also under DO & CO’s management.

On the outlook, it all depends on COVID and on how long it will last for the situation to return to the previous normal. The business is promising, but risky as aviation and travel are always risky as you have many things that can happen. The management forecasts that the company will emerge from the crisis stronger than before thanks to its flexibility. Nevertheless, we as value investors have to take a look at the financials, the value that is there no matter what and see what are the possible cash flows over the normal, unavoidable cycles in the industry.

DO & CO stock analysis – financial situation

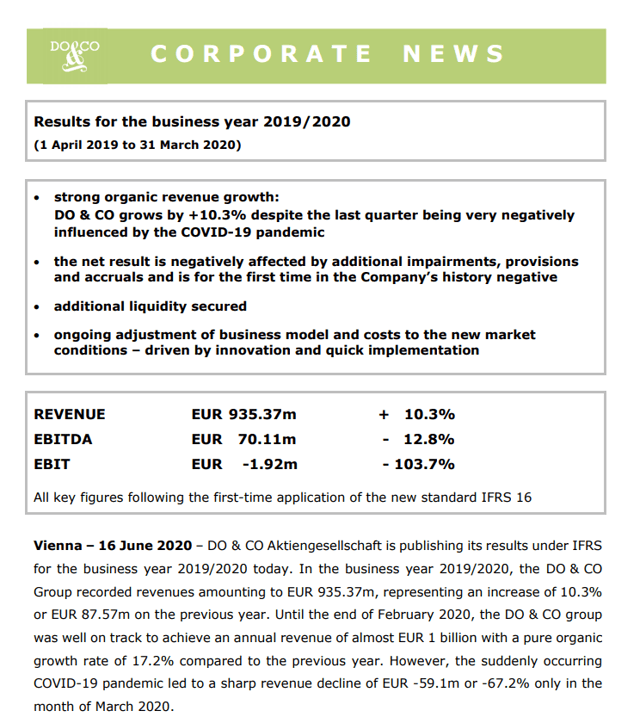

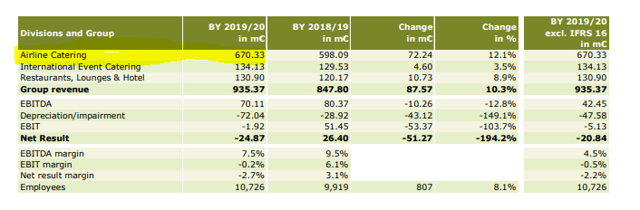

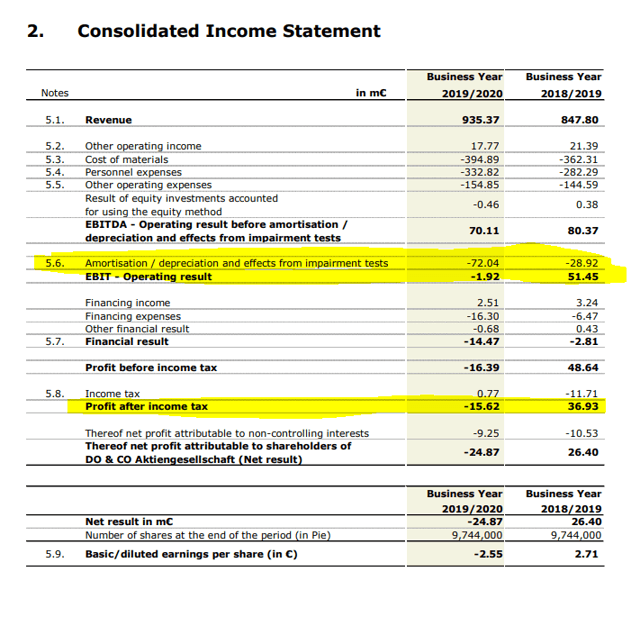

Despite the situation, they still managed to publish revenue growth for the fiscal year that ended on the 31st of March 2020.

Their organic growth rate without the virus impact was expected to be 17.2% which is remarkable. However, given that airline catering, that makes 72% of their business, will be close to zero this year, it is creating an interesting situation.

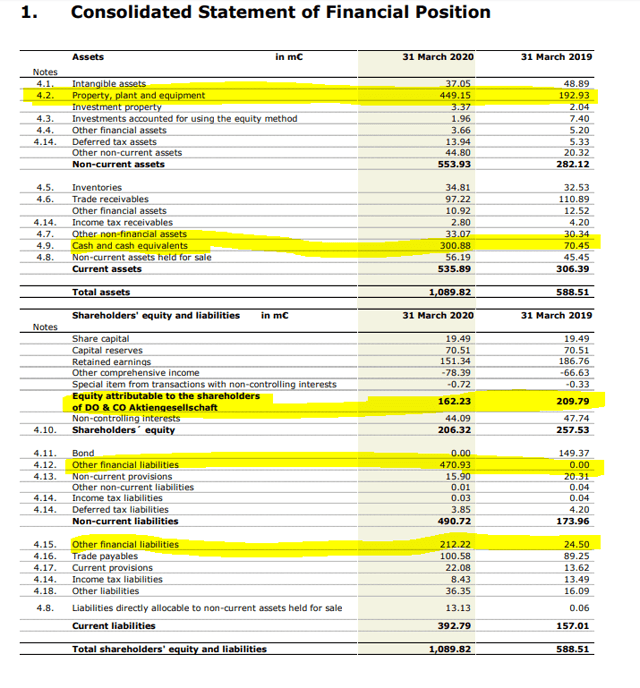

The first thing one notices when looking at DO & CO’s balance sheet is the huge business they were doing based on leases that now have to be shown in the balance sheet due to IFRS 16 ‘leases”. Alongside with the 300 million COVID bank loans taken in the last quarter and the one accounting change, the equity to assets ratio went from 43% to just 18% which makes the company extremely leveraged.

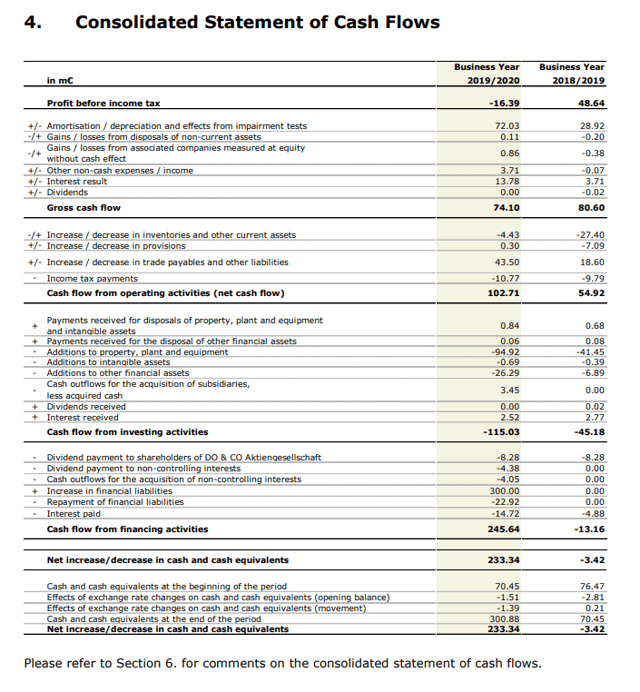

They have increased their cash position by taking bank loans of 300 million EUR to survive the crisis. Just personnel expenses in the last fiscal year were 332 million and other expenses 154 million. This will likely be decreased in the current year, but still the 300 million in cash they have might not last long in case the situation doesn’t return to normal soon.

The number of shares outstanding is 9.744.000 which makes the book value 21 EUR and the price to book ratio 2.18 at a stock price of 45.9 EUR. However, if the losses are measured in the hundreds of millions per year, shareholder value might be erased in a year or two.

The company makes approximately 80 million in cash in a normal year and invests more than that for growth. They even paid a dividend of 8.28 million in 2019 which is just 10% of gross cash flows.

In case this business continues to grow, creates a strong position withing their business niche, they can continue to grow and significantly increase their cash flows once the investments are completed. This could take decades as the industry growth and consolidates, but cash flows of 80 million, growing at 10 to 15%, are very interesting when compared to a market capitalization of 450 million.

The profits are not as high as the cash flows due to high depreciation.

Some things built will create value forever. For example, when you invest in real estate, then the depreciation is just an accounting cost and not a cash cost. However, I have the feeling DO & CO will always have to improve their business as they are not the owners of the real estate. So, they have to constantly change in order to cater to the latest trends, and therefore we can’t just take the cash flows as a measure.

DO & CO stock valuation

For a DO & CO stock valuation, I’ll start with the cash flows of 80 million per year, assuming a normal situation. From that I’ll deduct 50% of depreciation that should be around 50 million on the current 449 million of PP&E (property plant & equipment). So, I am down to 55 million. Deduct another 20 million on the almost half a million in debt they have, we are down to 35 million in cash flows that can create value for shareholders.

When we also add the fact that it will take a few years for the sector to recover, and then you never know from where will the next crisis come (remember the 2010 eruptions of Eyjafjallajökull in Iceland that stopped European flights for some months), the investing situation doesn’t look easy. So, we can’t take the 15% growth rate as a stable estimation.

Investing in DO & CO stock is about balancing the growth in the industry, their investments and the COVID situation alongside other potential crises in the industry. To me personally, it is too risky to pay 450 million for free cash flows of 35 million in a volatile industry like the airline industry is. Investors investing in DO & CO stock have to closely follow the situation and compare the risks and rewards to the other opportunities. I don’t think the investment returns will be as stellar as in the past due to the high valuation for a risky business and a for what is likely to be aslow recovery from COVID.

As we are looking for investments that have a higher margin of safety, are less dependent on such external risks and have similar growth perspective, DO & CO stock will not be a stock to put on our covered stocks list. Perhaps it will be a good investment, but the risks are definitely there, keep that in mind when investing in DO & CO stock.

We will continue with the analysis of other, hopefully less risky stocks traded on the Austrian stock exchange.

The DO & CO Stock Analysis is part of the full Austrian Stock Market Analysis make by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundreds of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: