Don’t Fear A Market Crash, Fear An Investing Tragedy (4 Strategies to Avoid it)

One of the biggest fears investors have is a stock market crash (SPY). Nobody likes to see the value of his portfolio go down along other likely negative thoughts related to such a situation. This might be losing your job, economic uncertainty or who know what else can come, seeing how COVID-19 surprised us. However, fearing a crash is an irrational activity, you should welcome any stock market crash.

Here is the video discussion, article continues below:

Welcome a stock market crash

However, a crash is not what we should fear, fearing a crash is irrational because it increases your long-term investing returns. Actually, a crash is something that should be welcomed.

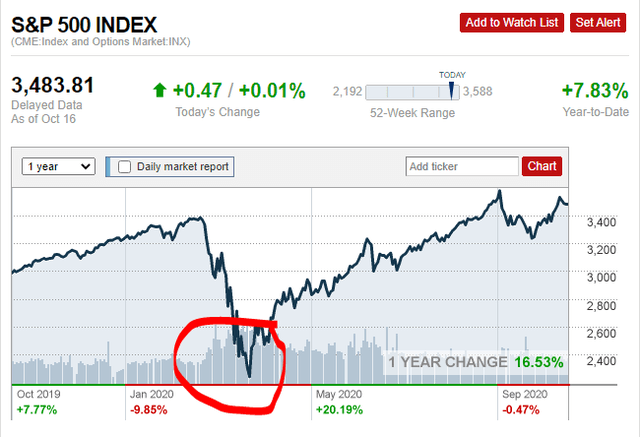

We have all witnessed the 2020 stock market crash. The stock market crashed more than 30% in a very short period of time, less than a month actually, and the outlook was extremely negative.

Within a month of COVID-19 lockdowns, the FED and other global central banks intervened, injected huge amounts of liquidity in the financial system and now, incredibly, investors are actually better off than in February 2020 as the market is higher.

Similarly, if we look at past crashes, the stock market sooner or later recovers which means that stock market crashes represent opportunities to buy what you already like at a cheaper price and thus increase your long-term returns.

Over 40 years, all those that bought after a crash, achieved better returns than those buying before the crash as sooner or later stocks always surpassed their previous highs.

So, next time there is a crash, simply sit back, relax and enjoy the buying opportunity as it will likely increase your long-term returns, be it if you just reinvest your dividends or put more money into your portfolio. Don’t do what most do, sell and never look back at stocks again!

If there is one guarantee I can give you when it comes to investing, it is that there will be many more crashes. Be ready and take advantage when that happens.

So, if you don’t have to fear crashes, what is it that you have to fear when it comes to investing?

Fear your possible investment tragedy

I believe investors have to fear an investment tragedy, let me explain. For me an investment tragedy is when an investor doesn’t reach his financial goals at the point when those were supposed to be reached. The sad thing is that while investors exuberantly cheer stock markets that go up, they are falling deeper and deeper into the investment tragedy trap that is being created.

I’ll further elaborate by discussing retirement goals, market valuations and the outlook on investment returns.

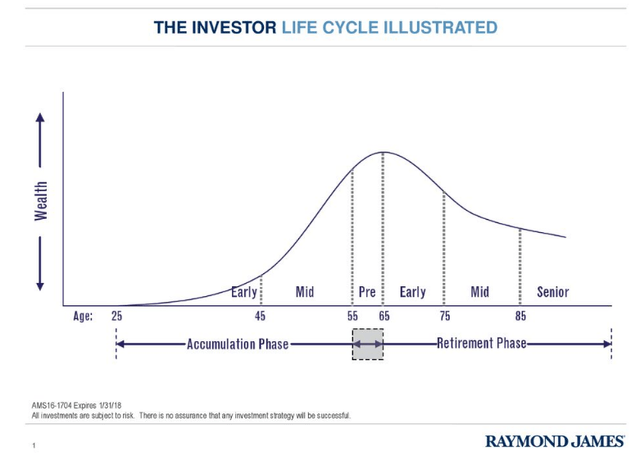

Most investors have a long-term investing goal that is likely related to retirement. This also means that we all have an investment life cycle which usually starts when we get our first job and lasts till the day we retire.

This means that we are net contributors to our investment plans for around 40 years. From such a long-term perspective, stocks going up might not seem that great of a deal. In your accumulation phase, you want stocks to be as cheap as possible and to go down all the time.

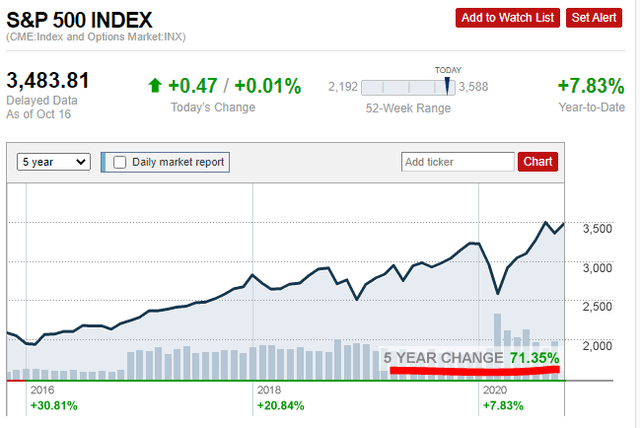

Stock markets up 71% in 5-years – Tragedy 1

By now you must think I am crazy because I am saying a crash is good and the fact that the S&P 500 is up 71% in the last 5 years is bad.

The fact that stocks are up 71.3% over the past 5 years means that your retirement, the vehicle that should bring you to your long-term financial goal, just got 71.3% more expensive than it was 5 years ago.

Also, the dividend yield, the earnings yield is much lower compared to the price of 5 years ago and your expected returns are consequently much lower. Lower returns lead to slower compounding and a longer road towards reaching your goals. These lower expected returns come from higher prices that increase valuations.

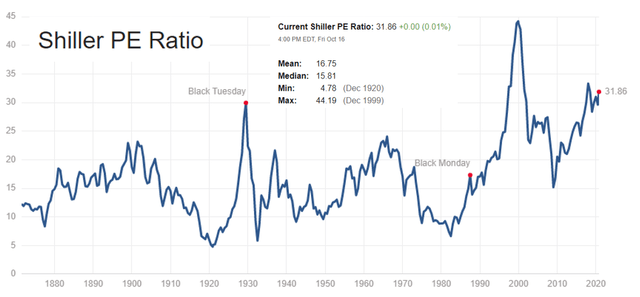

Stock market valuation at historical highs – Tragedy 2

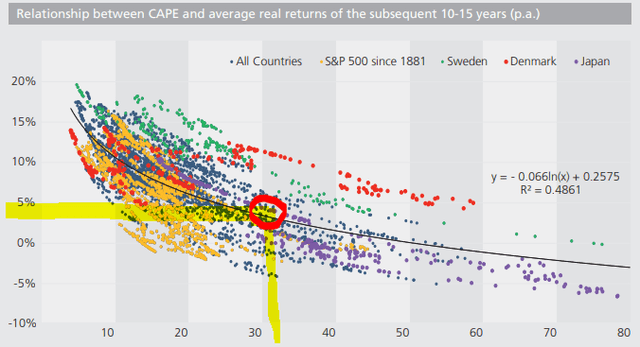

The S&P 500 cyclically adjusted price to earnings ratio (CAPE) that takes into account 10 years of earnings when calculating valuations, is at 31.86. This level has been higher only during the peak of the dot-com bubble in 1999.

If the CAPE is at 31.89, we can expect earnings returns from S&P 500 businesses to be 3.13% per year. If there is business growth and some inflation, then the return you should expect should be around 4 or 5% as we can add a percentage point or two for inflation and growth.

Unfortunately, history isn’t on our side when it comes to high valuations. With a CAPE ratio above 30, the likely real 15-year returns are going to be between -1% per year and 4% in a good scenario. CAPE and stock market returns – Source: Starcapital

CAPE and stock market returns – Source: Starcapital

Low returns don’t help you when it comes to compounding to reach your goal.

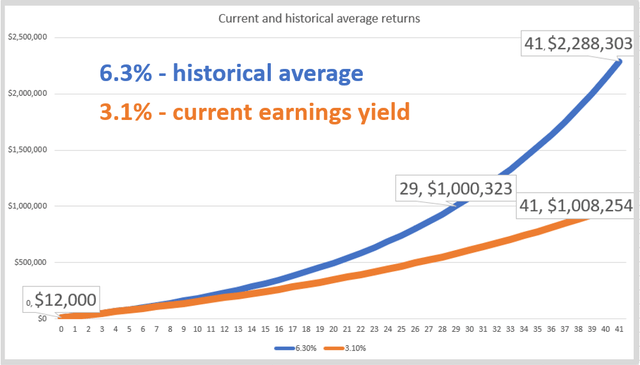

A 3.13% return is much lower than the average return delivered from the stock market over the last 140 years which was around 6.3% (add growth and inflation and you get to the average between 7% and 9%).

Over your investing life span, a 3 percentage points yearly difference in returns is enormous and significantly increases the money you have to add to your investment account to reach your goal.

If you invest $1k per month or $12k per year, it takes you 29 years to reach $1 million with a return of 6.3%. With a return of 3%, it takes you 41 years to reach a million. That is not just 12 years longer that you have to wait, but also $144 more that you have to invest to reach the same goal. This is the investment tragedy that might hit many of today’s retirement savers.

If you wish to have a portfolio of $1 million within 29 years with a 3.1% average return, then you need to invest $21k per year, compared to the $12k with a 6.3% yearly return. Investing almost double to reach the same goal is one of the life tragedies I think most people oversee because of the exuberance related to stocks going up.

Stock Market Investing Outlook – Tragedy 3

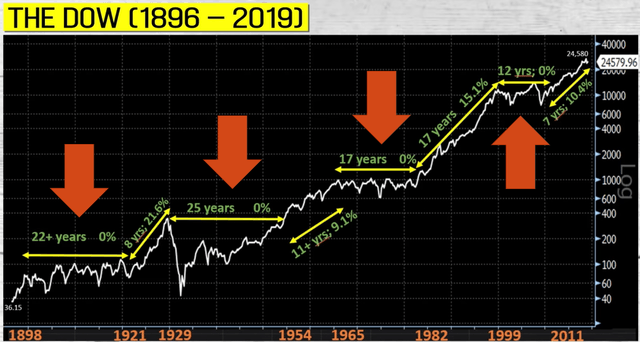

Given the high valuations, bad economic situation, demographics and low interest rates, long-term returns in general are not going to be much. Actually, over the last 150 years, it has been completely normal for the stock market to deliver zero returns for very long periods.

This leads us to tragedy number 3, many are expecting returns of 5 to 10% from stocks because the predominant idea is that 10% what stocks do. However, few shout how it is also possible that after 20 years of investing, you can look at your portfolio and it could be at the same level as at the beginning. It wouldn’t be the first time that happens and given the situation with high valuations and low dividend yields, we might be going into such a period in the stock market cycle.

However, to end on a bright note, this also represents an opportunity for long-term investors. If stocks don’t deliver anymore, if the exuberance subdues, there will be many opportunities for patient investors to pick up what capitulating investors sell. In the late 1970, early 1950 or 1930, nobody wanted to hear about stocks, but exactly those were the best time to invest. Keep that in mind when the next crash comes or people complain about low returns.

Stock Market Investing Risk – Tragedy 4

But perhaps the biggest tragedy of all will hit those that just entered the market and don’t understand fully what they are doing. I recently received the following comment where the self-called ‘investor’ has put all his money in stocks for 4 months now but with no real gains!

For me this is likely to become another investing tragedy. Given the boom in investing applications, more and more people that don’t understand what investing is, put their money into vehicles they don’t understand because those that went before them made money. We that have been investing for more than a decade now, know very well the party will not last forever.

Businesses are cyclical, at some point all looks bright, the outlook is good and it seems like the companies in the right sector, like it seems the case is for the FAANGS now, will simply make more and more money over time.

However, money always attracts competition which means you always need to be a step ahead and you need to invest to do that. Consequently, there are no dividends and given the environment we live in, I wonder when will those dividends arrive because of the cut throat business environment. If profitability doesn’t arrive, while the competition increases, we might head into a 2000 dot-com bubble situation.

Actually, I am sure of that, I just don’t know whether the Nasdaq index will first double and then fall or not. Nobody knows how long will the party last, but when the music stops, it will be tragic for many so called ‘investors’.

What can we do to reach our financial goals in a saferway?

As a value investor, I will tell you to look at value, safety and certainty and not to go by market fads. Boring companies like Berkshire offer returns of approximately 7% while if you look globally, you can find returns above 10% or even 15% because the assets are in Russia, Asia or Africa.

Get rich slowly is the key.

Secondly – Avoid unsustainable situations! I know it hurts, when everybody that invested in Tesla made huge amounts of money over the last year, but it hurts only if you don’t know the risks involved and how to invest for the long-term.

Thirdly, another thing we as investors might always keep in mind is that things constantly change. A year from now, there will be something else that is cheap and low risk with good returns as two years ago one could had said gold stocks were relatively cheap, or solar stocks after China cut stimulus in June 2018, look at those now.

Thus, give it time and diversify across time, your investing life cycle is probably 40 years if not more, so there is no rush in nailing everything right now. All you need to do is make a few wise financial decisions a few times in your life, and you will do great, that’s it.

To be wise just a few times in your life boils down to what kind of investor you are. If you are the one that follows the herd, I can’t help you. But, if you are one of those investors that wants to get rich slowly and safely, then my message is to look at vehicles that will most likely deliver the required return, see what is cheap at the moment, and build the vehicle that will lead you to your financial goals over time.

Knowing what stock will go up 100% over the next 12 months is very difficult for me, but knowing what business will likely pay higher dividends 5 or 10 years from now is much easier. Thus, I am not the one to follow if you wish to double your money every 12 months, but if you wish to get rich slowly, please click that subscribe button.

This is part of my free stock market investing course, feel free to check it out.