Stocks Crash 70% And 76% Will Underperform – Can You Handle That?

Stocks crash and stock markets too

Before investing, you must know that stocks can crash 70% anytime and 50% of individual stocks will likely deliver negative returns or below 2% while 75% will underperform the market. If you are not ready for that, better don’t invest in stocks! It is that simple!

It is not about whether there is going to be a crash next, it is about what are you going to do when a crash comes and are you ready if stocks don’t crash.

I have looked at research that shows how investors underperform the market by trying to time a stock market crash and about how difficult it is to time it. The key is that you see how does the possibility and magnitude of a crash fit your tolerance. Stocks can crash 70% anytime and stay down for decades – are you ready for that?

When it comes to individual stocks, the situation gets uglier. 30% of individual stocks will crash and actually deliver negative returns. Only 4% of stocks will do really great and compound! Can you handle the pain of investing in stocks?

If you can’t, I don’t know, buy a house!

Whenever the stock market is crashing, I am reading many emotional comments. That is normal and naturally human. Whenever a stock crashes that I discussed, I read many comments of what an idiot I am. Both things are natural, but we have to stay rational. In this article I’ll explain what investing is by discussing:

- How stocks markets can crash anytime, stay down for long and how it is up to you!

- How most stocks deliver poor returns and even if you get only 4 out of 10 right, you are a genius!

- How to approach investing from a probabilistic rational perspective.

- I’ll add just a bit of good news to end it all.

Stock market crashes, rationality and investing outcomes

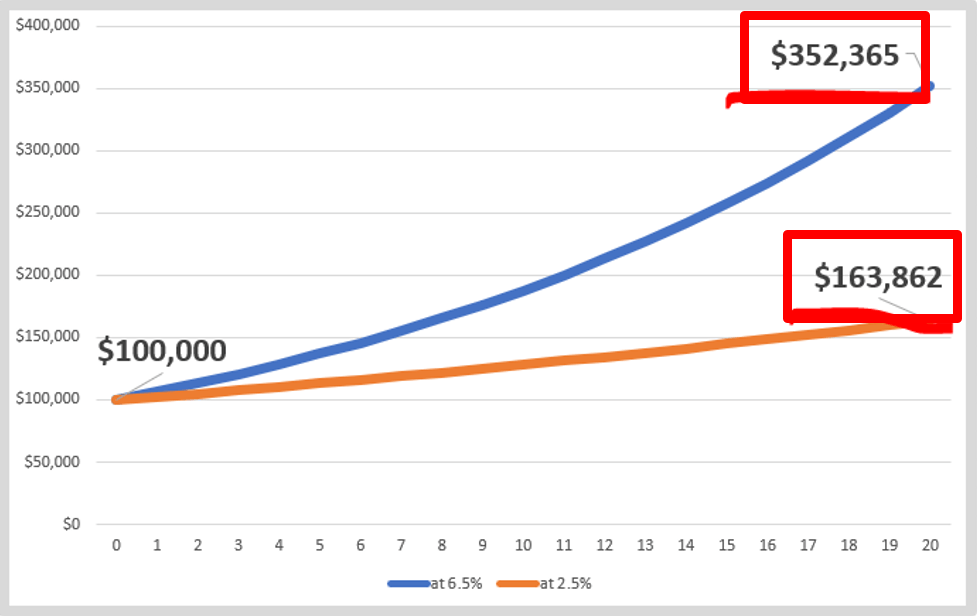

Emotions don’t keep you rational and can therefore lead to many mistakes that don’t have to happen. I wish to share 3 investing principles that will help you avoid the mistakes the average investor made over the last 20 years. Mistakes that got him a return of just 2.5% per year while the S&P 500 achieved 6.6%.

Average yearly investing returns per asset class – Source: J.P.Morgan

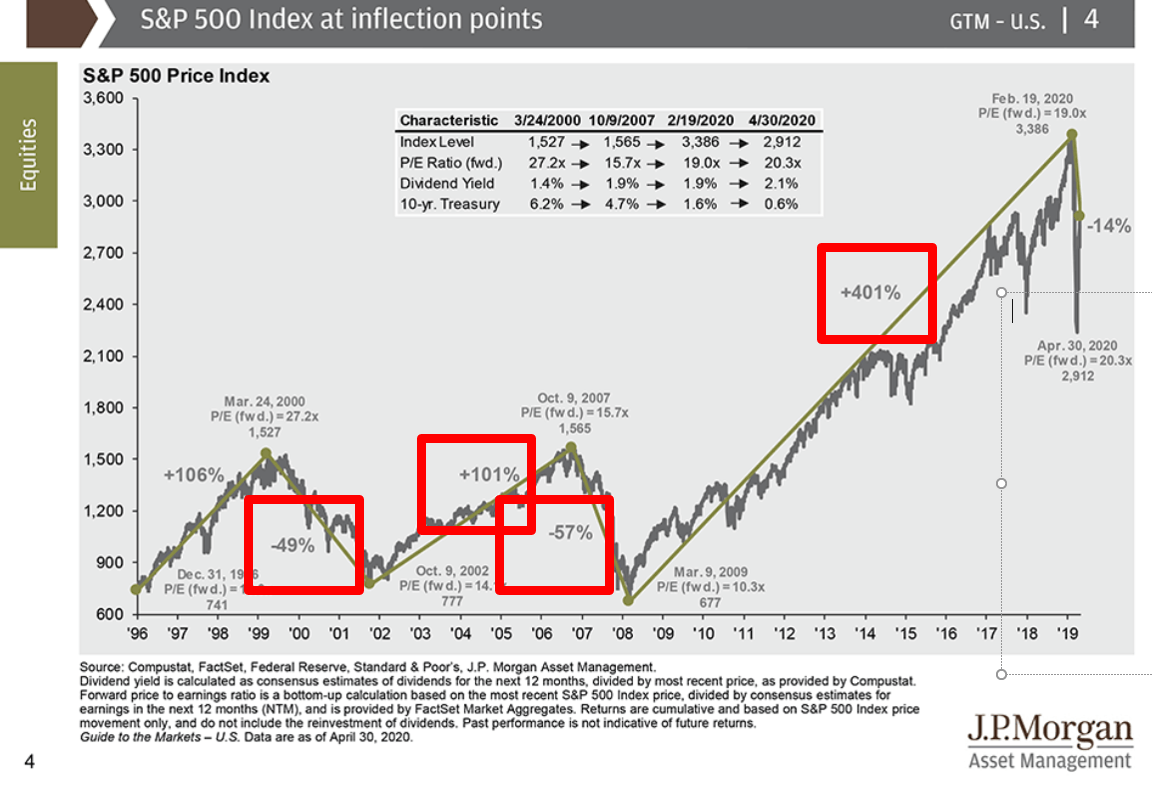

Over the last 20 years, the market had two bear markets and two bull markets. The two bear markets were approximately 50% down and the latest bull market was one of the best in history.

All in all, the market went up 6.6% per year. How come the average investor got only 2.5% per year?

Let’s say you have a $100k portfolio, at 6.5% over 20 years it becomes $352k while at 2.5% it reaches just $163k. The difference is staggering and extremely significant.

The reason behind the underperformance is because most do the wrong thing at the wrong moment in time! This means buying too much in exuberance when stocks are high and selling in panic when it seems like the world is about to end. On a side note, it is funny how it seems the world is about to end every few years. The decision making is usually related to emotions and therefore we have to know what might happen and more importantly, know what will we do about it.

To paraphrase Ray Dalio: Every asset class will likely go down 70% once or twice in our life time!

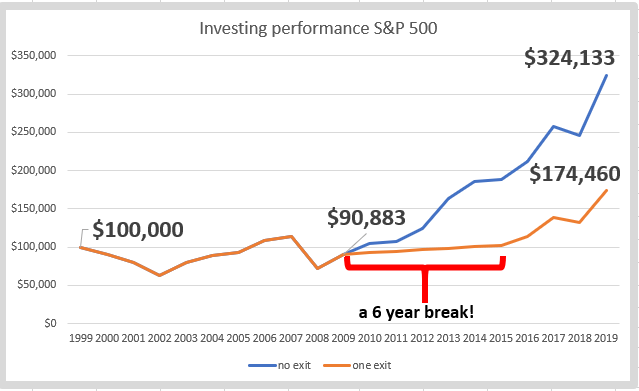

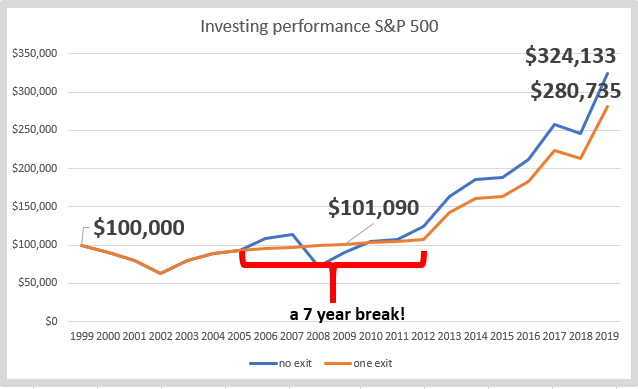

This is such an important principle to understand before investing. From 2000 to 2002 and from 2007 to 2009, the market fell 50%. Many couldn’t handle the volatility and sold in October 2008 or March 2009. When the situation stabilized, the double dip recession was off the table, they probably got back in around 2014. Unfortunately, the market timing experiment maybe saved their nerves, but it cost them more than 50% of the cumulative portfolio returns as shown in the chart below!

Even if somebody sold in 2005 and got back in in 2012, thus avoided the 2009 crash, the returns would still be below the market’s return. This shows how difficult it is to time the market in a profitable way.

Now, why would you time the market? Well, people time the market if their investment goals aren’t aligned with what investing in stocks can deliver.

If you are afraid your portfolio will go down more because the news is terrible, because you don’t want to see your wealth evaporate, then you will likely sell at the wrong moment in time like many did.

So, the key principle here is that you have to be able to tolerate a 70% decline in the markets! If you can’t, you better not be invested in stocks. This is the likely process:

- Stocks down 10% – it is a correction, it will likely pass

- Stocks down 20% – ok, a recession, stocks will recover

- Stocks down 30% – hm, this is getting dangerous, what should I do, I can’t risk my retirement

- Stocks down 40% – bad news, this will get worse, I better sell and protect what I have

- Stocks down 41% – market bottom and bull market ahead!

By being ready to see your portfolio go down 70%, you can keep adding when stocks are cheaper instead of selling in panic. This would actually allow you to have a return that is higher than the market’s return from an absolute wealth making perspective.

When can a crash happen and how long it might take for the recovery? Nobody knows! Stocks can recover in a few years or it might take decades!

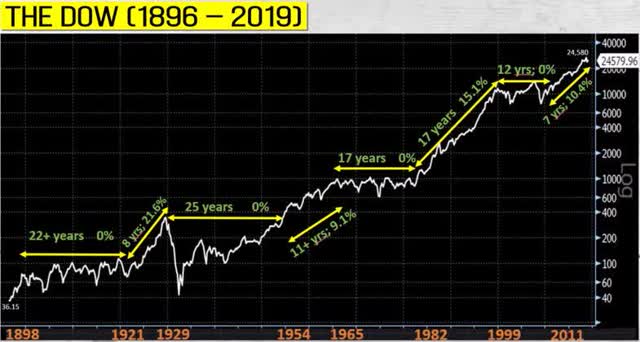

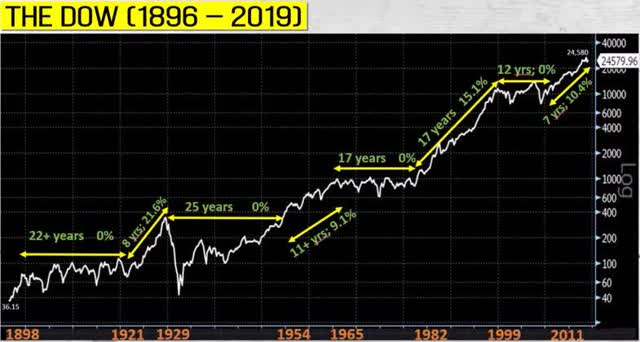

The Dow – Courtesy of Mohnish Pabrai

It is also possible for stocks to deliver 0 returns over periods of 12 years or even 25 years! Keep that in mind when investing and based on how much you invest in stock!

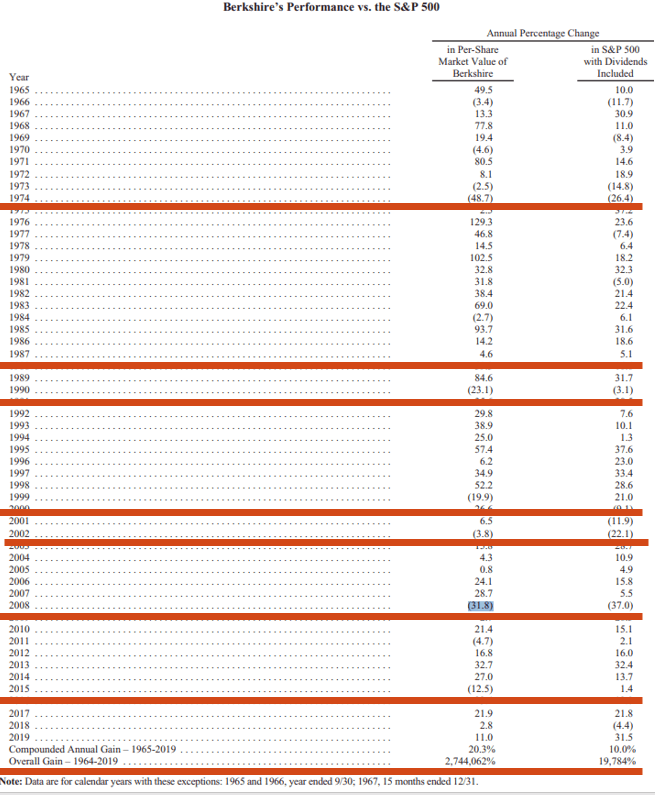

I know that my portfolio can crash 50% or more at any given time. Even Warren Buffett’s BRK stock crashed more than 40% on average ever 12 years since 1968.

Yearly changes in BRK’s market value – top tick to bottom tick changes were much bigger – Source: Berkshire letter to shareholders

Predicting crashes is too risky, therefore the only thing we can do is accept it as a possibility, or even better, a certainty, and when it happens make the correct decision. It also gives you a good perspective on how much money to invest in stocks. With all the money I have invested in stocks, I can easily tolerate a 50 to 70% decline. I know it will happen sometimes and I know that hedging against it is usually too expensive for me to do on a constant basis. So, I accept it and adjust my strategy to that.

If you invest in individual stocks, the situation is even worse!

Individual stocks crash even more – investing outcomes

When you own the market, you own a bit of everything, but when you own individual stocks, there is where the fun begins.

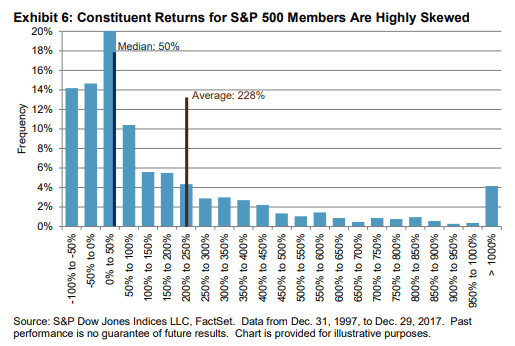

If we take a look at the distribution of returns from 1997 to 2017 for all the constituents of the S&P 500, the actual median return was just 50%, that is just 2% annualized. The average total return was 228% and that is just because a few companies delivered staggering returns.

Many losers, few winners – Source: Spindices

14% of stocks delivered negative returns between 50% and 100%, 15% between negative 50% and 0% while 20% delivered returns between 0% and positive 50%. Thus, 50% of S&P 500 stocks delivered returns below 2% per year.

On top of the 50% that delivered very poor returns, another 26% didn’t beat the market over 20 years, thus a total of 76% of stocks don’t beat the market.

If you invest in individual stocks, 7.6 out of 10 investments are likely to be losers. That is something crucial to comprehend when investing in stocks!

The thing is that the 24% likely winners will cover for all the losers. So, if you are an investor, you have to be happy if your have less than 7.6 losers out of 10 investments!

If you get 4 right and have 6 losers, you are a great investor, if you get 5 right, you are at Warren Buffett levels and if you get 6 right, you will go down in history as the best investor that ever lived.

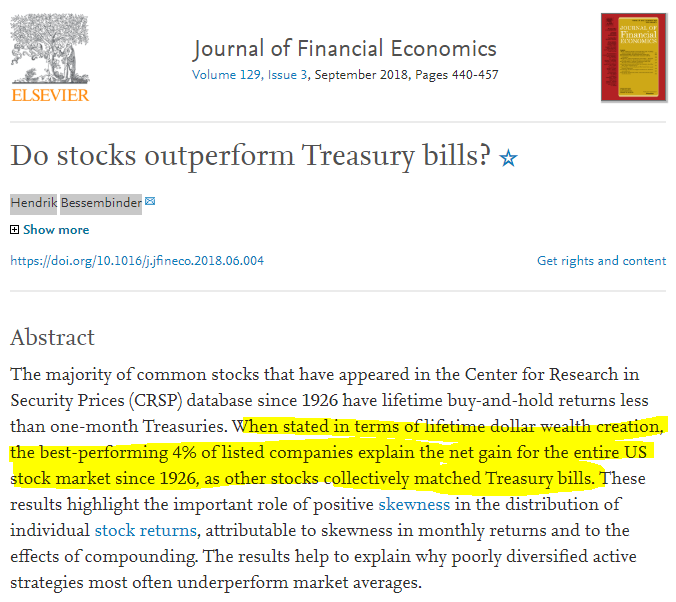

According to research by Hendrik Bessembinder with his Journal of Financial Economics aritle on stocks and Treasuries performance, only 4% of the stocks since 1926 explain all the positive returns the stock market delivered since then. The other 96% of stocks performed as Treasury bills.

Source: Science direct

The difference is again staggering! $1 dollar invested in the market would now be measured in thousands for owning stocks, while it would be just $21 dollars for owning Treasury bills or the 96% of stocks that didn’t do well.

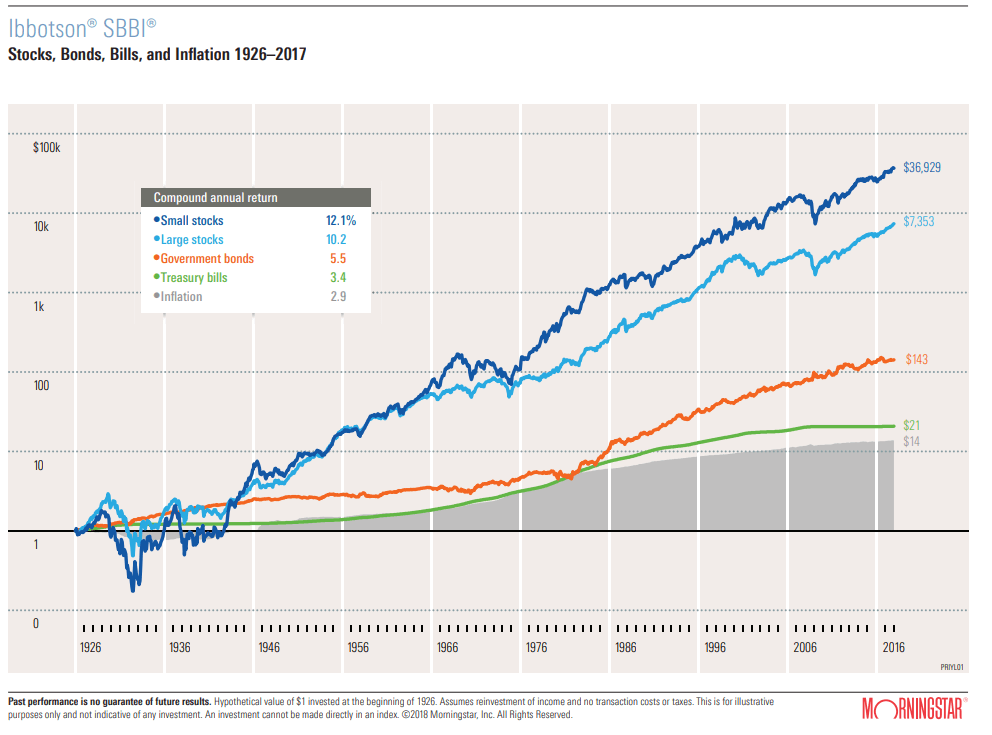

Comparative returns – stocks, bonds and inflation – Source: Morningstar

Morale of the story – when investing, you’ll make many mistakes, the trick is to water the flowers and not the weeds. So, don’t feel bad if 6 out of 10 stocks in your portfolio are losers, stick to the winners, that is where you will get your returns.

Accepting mistakes is a must – simply put it into a statistical framework. That is also what I do that allows me to survive all the comments of how big an idiot I am when a stock that I discuss or own goes down significantly. I can guarantee you I’ll make many mistakes, if I can get 5 out of 10 right, that will deliver an amazing return!

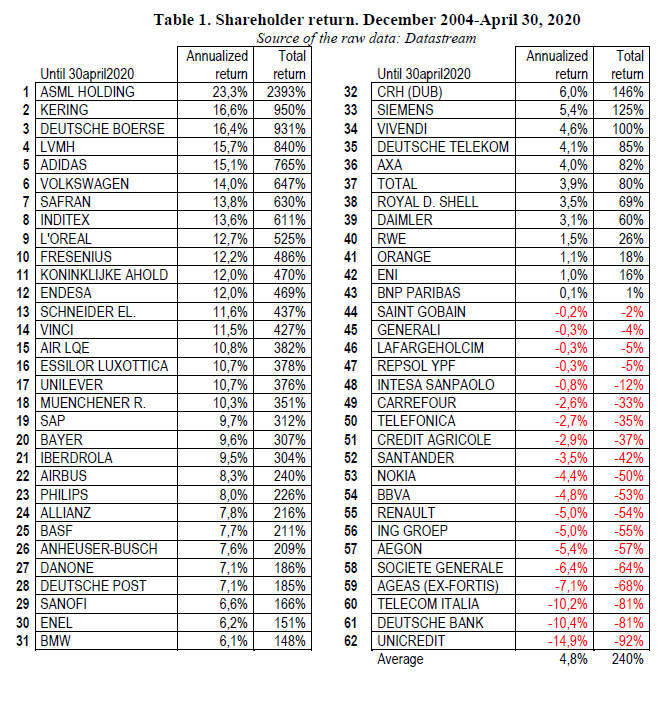

I have another example from Europe using Eurostoxx 50 index between 2004 and 2020. The average annual return was 4.8% and, in this case on a smaller sample and shorter period with only one crash, 50% of stocks underperformed. Still, with 5 out of 10 mistakes, you would still do good! Keep in mind this is a 15-year period, the longer the period, the larger the discrepancy between winners and losers.

Shareholder returns of Euro Stoxx 50 companies: 2004 – 2020 Source: Fernandez

If you are investing in individual stocks, you must know that 5 out of 10 will likely be ugly, some, probably 2 out of 10 will lead to losses higher than 50% and only a few will give you returns higher than 15% per year, likely less than 5% of the stocks you own over 20 years, and less than 10% of the stocks that you own over 10 years. It is simple maths, the good thing is that the losses are limited to 100% and unlimited on the upside.

However, also keep in mind that behaviourally we hate losing 2.5 times as much as we love winning – so investing will not be a pleasure walk on your nerves and this is also where all the hate comments on my loser picks come from.

Quality and size don’t really make a difference

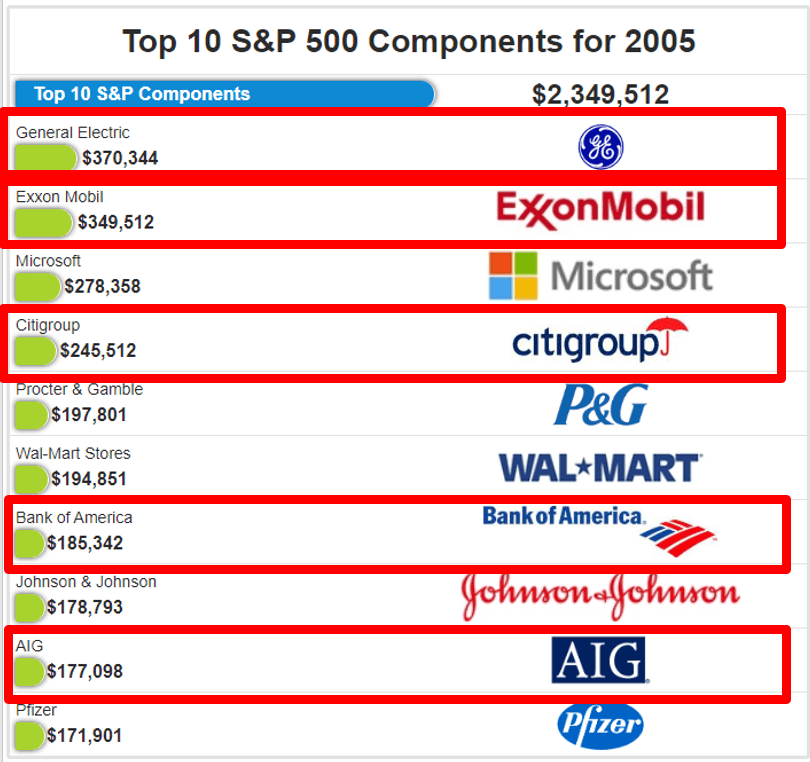

Now, you might think that by investing in only the best companies in the world might lead to better outcomes. If you invest in emerging markets it is logical things can get bad very often, but if you focus on quality, like then top 10 positions of the S&P 500, then the odds should be in your favour, right?

Well, not so fast, if we take a look at the S&P 500 top 10 positions from 2005, just 15 years ago, we can see how the outcome numbers we discussed above apply to all sorts of stocks, even those of highest quality.

Out of the top 10 S&P 500 position at the end of 2005, 5 positions performed extremely bad.

Visual S&P 500 top positions – Source: ETFDB

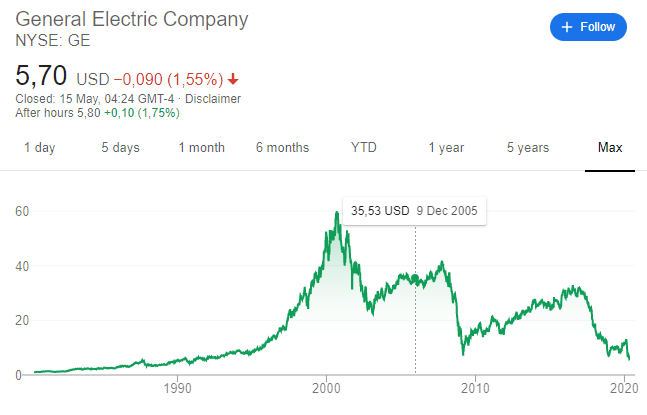

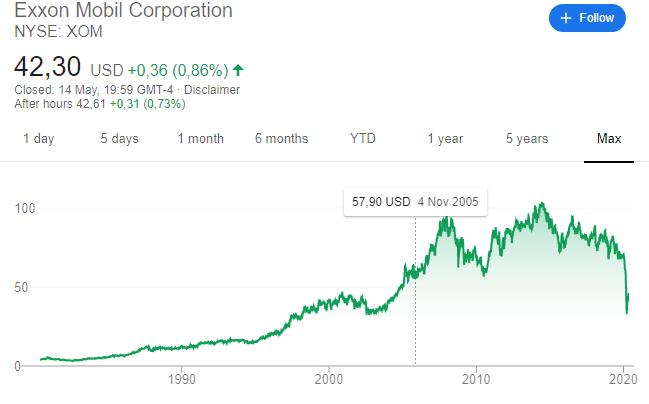

GE is down almost 85%.

Exxon is down much less and the dividends cover up for most of the losses, but still it heavily underperformed the index.

The banks were the worst performers, but the unpredictable happened with the financial crisis. However, we have to keep in mind that the unpredictable can happen anytime.

Therefore, when investing, one has to always keep in mind that stocks can crash 70% at any given moment and that 20% of individual stock positions will likely decline between 50% and 100% over the long-term.

How to invest – the Buffett model!

I firmly believe investing is personal, and each decision has to be made in relation to what you can handle. Investing is actually about finding asymmetric risk and reward opportunities in order to eliminate the potential losses and maximize the potential winners. At the 1989 shareholders meeting Warren Buffett said it like this:

“Take the probability of loss times the amount of possible loss from the probability of gain times the amount of possible gain. That is what we’re trying to do. It’s imperfect, but that’s what it’s all about.”

This means that we have to look at the probability of the outcome, the impact of it and then compare it with the probability of the positive outcome and the impact of it.

Also, given that investing is personal, I would also assess how the worst-case scenario affects you personally and what would your forced actions be in that scenario?

I’ve created a little table to explain what Buffett is saying, also discussing my guesses for where the S&P 500 could be in 10 years based on my current gut feelings, nothing more.

My target for the S&P 500 is 4,950 points in 10 years. That would give you a return of 6.2% per year which is in line with the current valuations, inflation and business growth rates.

However, you have to keep in mind there is a possibility the index or any other investment goes down 50% and stays down for a while, like it was the case for long periods in the past. In that case, the only thing one can do is patiently accumulate.

I am just reading Ray Dalio’s principles again and within his personal story he discusses how everybody was talking stocks in the 1960s because everybody was making money. Unfortunately, it took stocks 17 years to break even. Keep in mind that might happen again and it will likely happen sometime in your investing life cycle.

Warren Buffett accumulated during those times and the result is Berkshire as we now it now where huge wealth was created! Be ready to do that same if that scenario materializes!

To sum up:

- Stocks, or anything else for that matter, can crash 70% at any point in time – expect that is possible and adjust your strategies.

- If you get 4 out of 10 individual stocks right, you are a genius!

- It is all about probabilities and about how the worst-case scenario affects you!

I hope this helps you in determining how much to invest and how to invest. Investing for the long-term is the key here and watering the flowers, not the weeds will allow you to get to good return.

Keep in mind the volatility of it all, that will allow you to make rational decisions and actually take advantage of the market. Make the market your servant!

Crucial to understand before putting any money into investments:

- At any time, stocks can crash 70%

- 7.6 out of 10 investments held for the long-term will do badly

Thus, there will be lots of mistakes, there will be ugly situations. The key is to keep accumulating what has good chances to become something good and lead to positive eternal cash flows that will create new cash flows.

If you prefer a video/podcast, here it is:

If you enjoyed the content, understand the implications investing not done well can have, but want to learn about what can investing done well do, please check my Stock Market Research Platform.