Alcoa AA Stock Analysis – Amazing Leveraged Play on Aluminum Prices

Summary: Alcoa is an amazing leveraged play on aluminum prices. A great play on volatility but be careful because the underlying fundamentals are not that sound. Quick returns of 50% possible every 3 years.

This Alcoa stock analysis is part of my full aluminum sector analysis. Here is a video discussing Alcoa and comparing it to KALU, CENX, ACH & NYH.

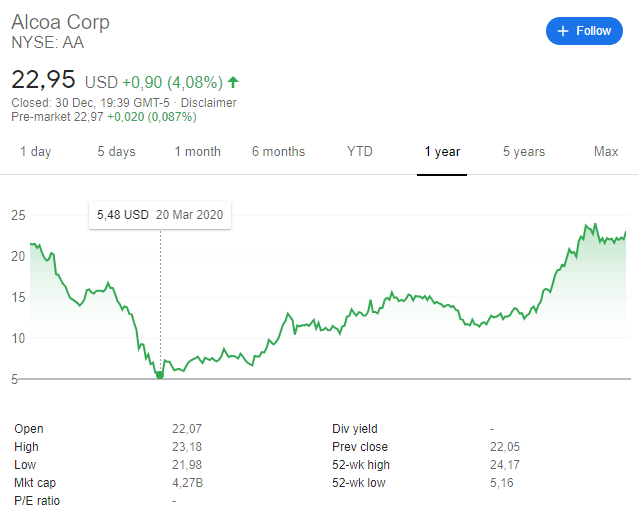

Alcoa stock price overview – NYSE: AA

Alcoa stock did greatly since the March 2020 lows and is one of the nicest recovery stories on the market.

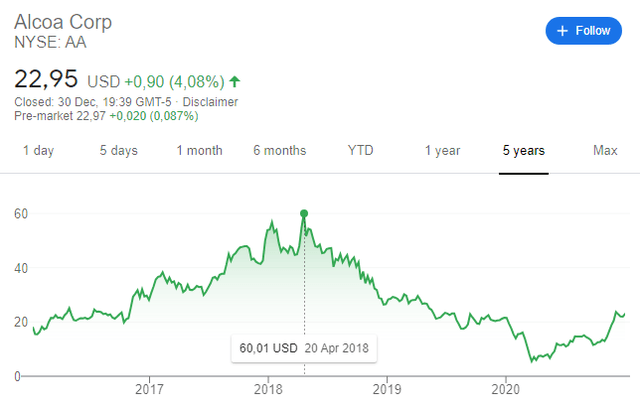

However, we are still 60% down from the 2018 peak at $60. Just to put things into perspective, Alcoa stock wend from $60 to $5.5 in less than two years, only to rebound to $23. Then there are people saying how the market is efficient…

The point of the above is to show how difficult the aluminum investing environment is. The extreme volatility is due to the fact that on average, aluminum producers haven’t made any money over the last decade. A highly competitive industry with no barriers to entry, can often make things look very ugly, especially for companies like Alcoa that don’t have competitive advantages and are a price taker with legacy burdens in the form of pension obligations and higher input costs in for of energy prices.

When things are bad like those were in March of 2020, the market, given its myopic attitude, thinks the bad will last forever. On the other hand, when things start to improve, the market becomes exuberant and thinks good times will last forever. That is typical behavior in a cyclical industry but I can guarantee you that the only thing that will last forever in the aluminum industry is volatility.

Volatility doesn’t mean one can’t find good investments. A savvy investor can make money with well placed, low fundamental risk, high potential reward trades. The underlying fundamentals for aluminum demand are positive, which means that there is a long-term tailwind telling us that good companies will not go bankrupt.

We as investors, or in this case fundamental speculators, have to keep in mind that the company will not make any money in bad to average times, but make a lot of money compared to the market capitalization in good times. As Peter Lynch puts it within his 6 stock categorizations; you have to buy a cyclical stock when things start improving. To do that you have to follow it and then be greedy when others are fearful. My goal and the reason I am analyzing the complete aluminum industry, is to find a stock that I can follow and then take advantage of that low risk 50%, 100% or even higher cyclical upside.

Plus, given the place aluminum has in the global economy, I feel it is crucial to follow as an amazing representation of economic activity, market sentiment and expectations. I will certainly cover a few aluminum stocks.

Alcoa’s stock investing situation

Given Alcoa’s stock chart, I would say we are looking at a medium risk, good potential reward situation where the stock can still easily double on more good news like it was the case during 2016 and 2018.

I am going to make a fundamental analysis of Alcoa in order to assess the risks of investing now and compare those to the potential upside.

Alcoa stock analysis – business overview

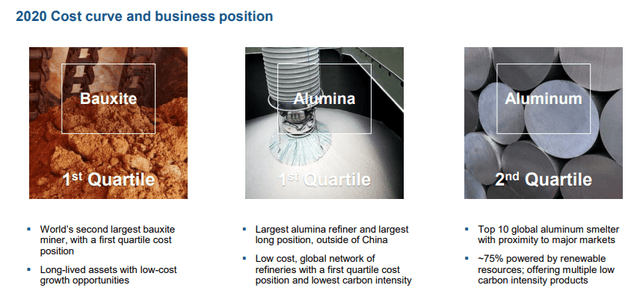

Alcoa is an aluminum producer with significant integration.

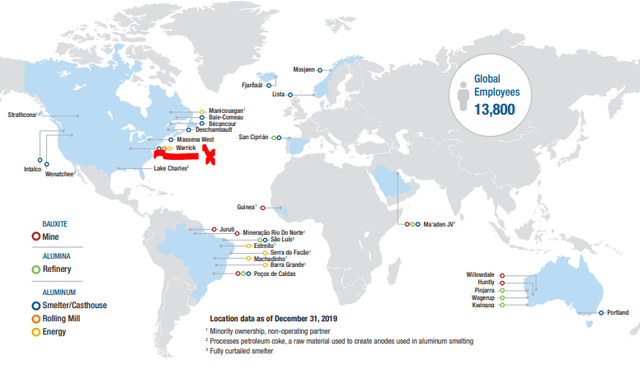

Business is mostly focused on the Americas.

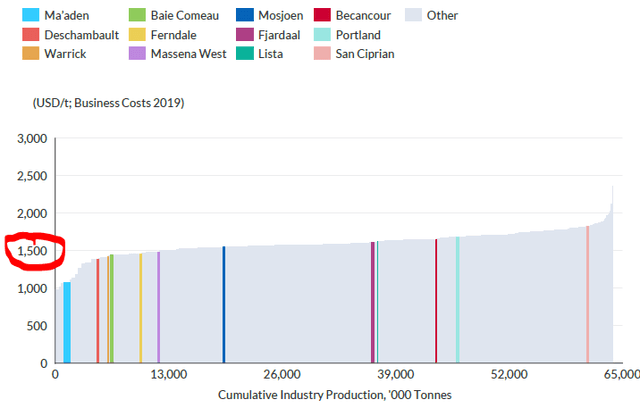

The problem is that the cost curve in the business is pretty flat and with prices being where they are and oversupply expected up to 2024, not many chances of high profitability for a while.

With aluminum prices below $2,000/t, and just business cash costs being around $1,500, you don’t make much.

If there is higher than expected demand for aluminum globally, Alcoa will continue to do good but that is something the future will tell us.

Let’s make a fundamental analysis to see what are the average cash flows one can expect in order to determine investing risks.

Alcoa stock fundamental analysis

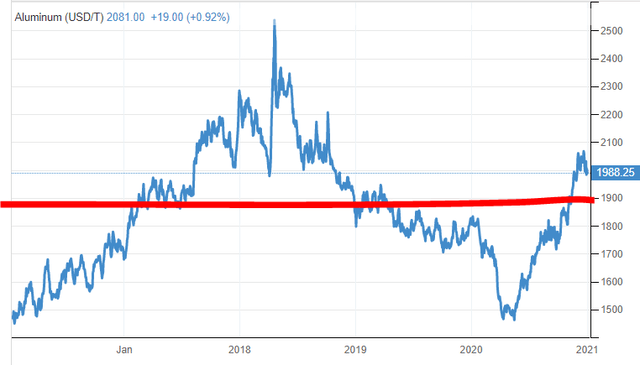

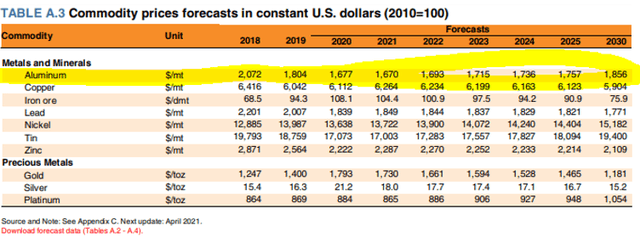

The last 3 years are good years to take as averages for aluminum given that the prices fluctuated but we around the midterm current expectations of around $1,900 per ton.

Not surprising, Alcoa’s stock price practically followed the above chart, confirming that the market doesn’t know how to adjust for cyclicality with a stock price. This is one of the great advantages retail investors with a long-term fundamental investing mindset have over the market.

If I take a look at Alcoa’s fundamentals over the period, from a cash flow perspective, the company doesn’t even make money in such an environment. Thus, like other aluminum producers that I have analyzed, for the industry to be profitable they need higher prices. The problem is that with low interest rates, Chinese companies like Chinalco investing no matter what, there will always be a fool (or genius) ready to invest a few billions into a new facility thinking how prices will be higher when the oversupply subdues in 2024. Why genius? Well, if you can gamble with other people’s money, for me you are a genius because that is the essence of value investing: no risk, high potential reward.

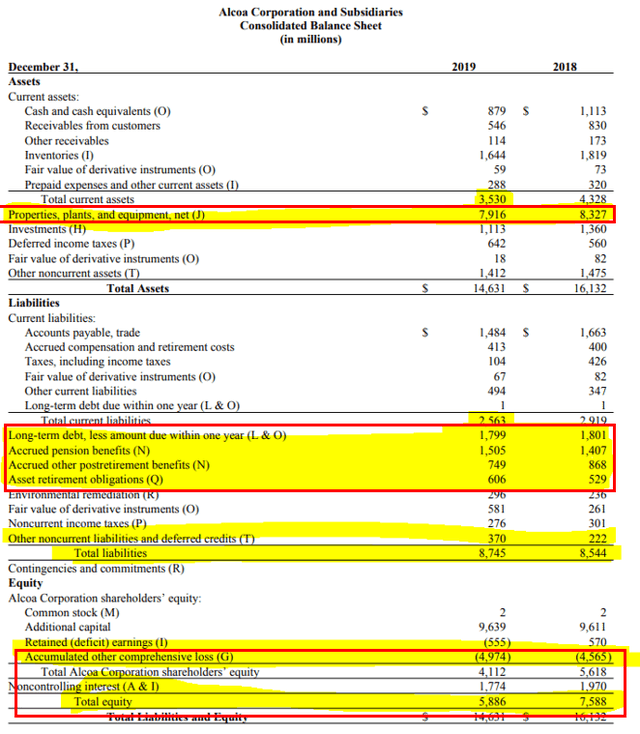

Now, one would think how Alcoa is a good buy to sit and wait for better times. However, a look at the balance sheets shows how there are a few skeletons in the closet. If you read Fisher’s book Common Stocks For Uncommon Profits written in 1956, you have read about how a great stock Alcoa was over the decades prior to 1956. Unfortunately, this also means there are humongous US pension liabilities.

The equity for shareholders is equal to the market capitalization which means there is no margin of safety if buying Alcoa now. Keep in mind the stock was at a quarter of the current market capitalization just 9 months ago because with markets declining, the pension liabilities increase because the value of the assets in the pension funds goes down.

I don’t know what is the mumbo jumbo behind the hedges and how big could the risk be for the pension liabilities but I know I am not going to look at that either because I am already convinced to look for better pastures than Alcoa is at the moment. I am a long-term investor looking for low fundamental risk offering high potential returns. With Alcoa, there is always the risk of real bankruptcy. Thus, even at very low stock prices, it isn’t possible to bet heavily and with a high conviction level but it might be good for small swing trades. Norsk Hydro seems a better fundamental bet to follow. Norsk Hydro stock will rebound much less, but will allow me to sleep better.

With forecasts seeing aluminum prices below $1,900 for the longer term, the fundamental reasoning for buying Alcoa now is lacking, given prices are above $2,000.

But, if aluminum prices go down and the stock price goes down the drain again, then you might consider buying it for another rebound. If that continues to happen every 3 years, you can get quick 50% returns every few years. That could make Alcoa the biggest contributor to your investment returns, even if you never have the intention to hold it.

Alcoa just sold its Warrick Rolling Mill for a purchase price of $670 million at an implied multiple of approximately seven times adjusted EBITDA to Kaiser Aluminum (NYSE: KALU). This shows how the management is doing whatever it can to create shareholders value, but also that they lost $100 million in EBITDA and I am sure Kaiser picked one of the most valuable assets. The Kaiser acquisition is more of a confirmation how the old powerhouse needs to sell the jewelry to survive which is a sad and ugly situation.

If you are interested in better aluminum stocks than Alcoa, check my full aluminum sector analysis.