Kaiser Aluminum Stock Analysis – Dividend & Buybacks Rewarding Shareholders – 10% returns expected – NASDAQ: KALU

This KALU stock analysis is part of my full aluminum sector analysis. Here is a video discussing Kaiser Aluminum and comparing it to AA, CENX, ACH & NYH.

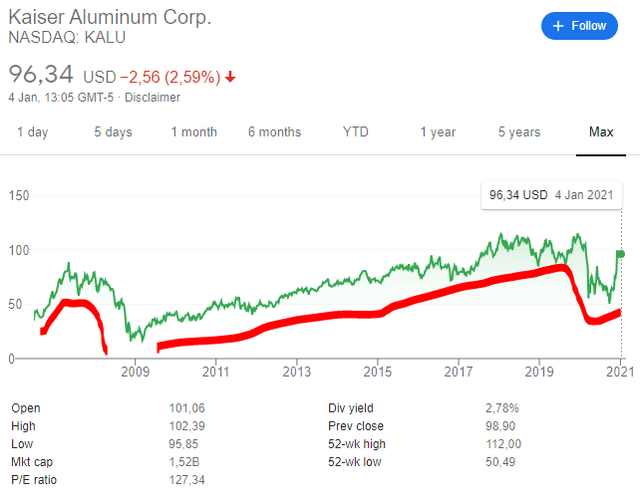

Kaiser Aluminum stock price analysis

Kaiser Aluminum (KALU) stock chart is peculiar as it doesn’t have the typical cycles that other aluminum stocks have. Kaiser’s business model made not to depend on commodity prices, but the stock still shows cyclicality from an industrial perspective.

Real recessions like 2009 and the recent one, have hit KALU stock, but both times the stock recovered and more. Let’s see what is the market pricing in and what is the investing outlook. Kaiser aluminum has rewarded shareholders both with dividends and buybacks in the past and will likely continue in the future.

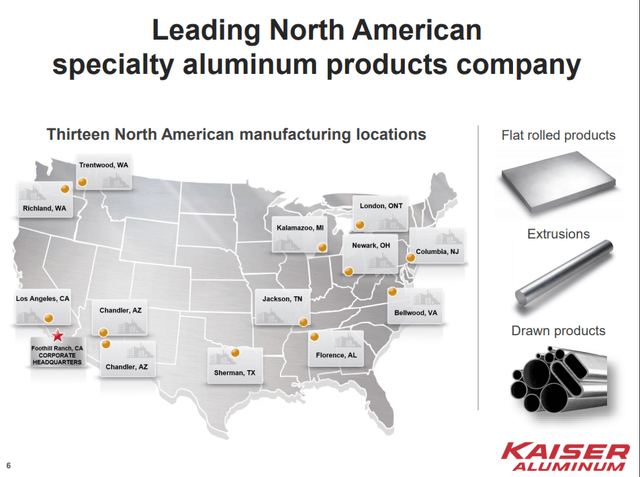

Kaiser Aluminum business overview

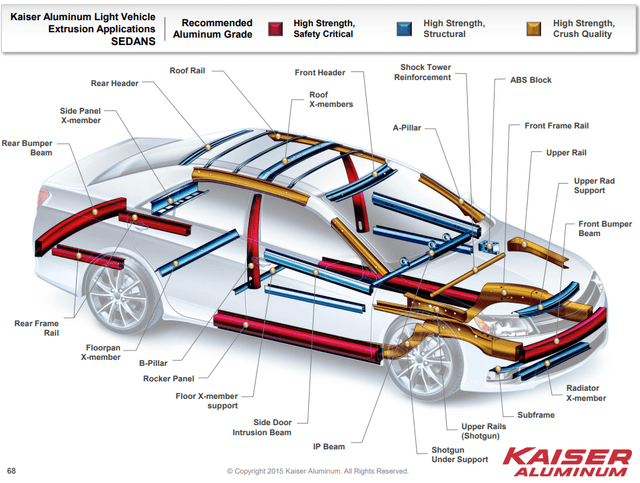

Kaiser Aluminum focuses on specialty aluminum, tailored to the customer’s needs.

The focus is on making things that are not easy to make and build relationships with customers that are difficult to compete with. This is similar to 3M’s 118,000 of patents which makes MMM stock a moat like stock.

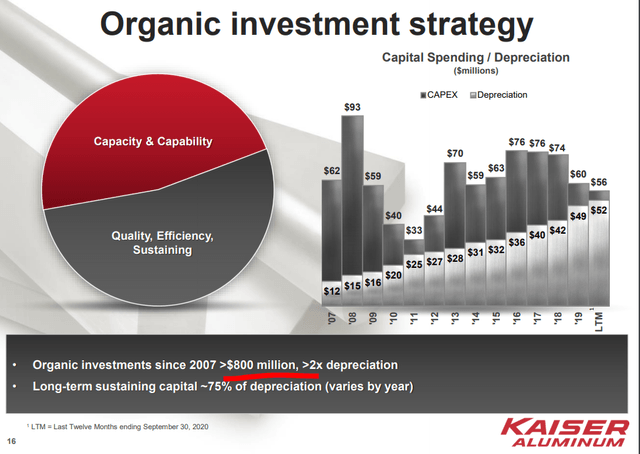

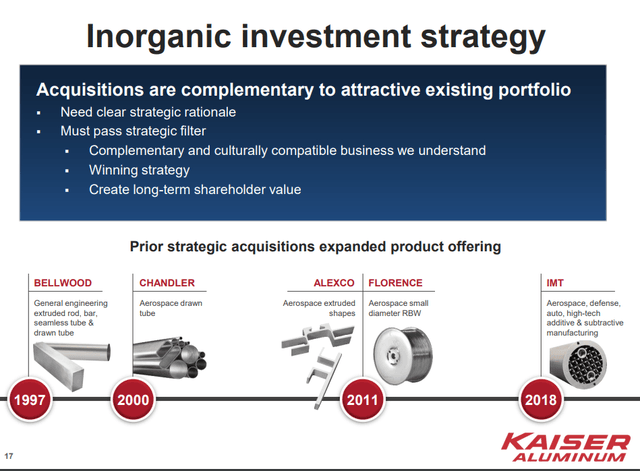

KALU has invested $800 million over the last decade in organic growth but it didn’t shy away from acquisitions either.

Their latest acquisition has been Alcoa’s Warrick LLC Rolling mill (ingot casting facilities, hot and cold rolling and coated finishing capacity) for 7 times EBITDA, paid in cash that they had. This should add $100 million to EBITDA and improve debt ratios.

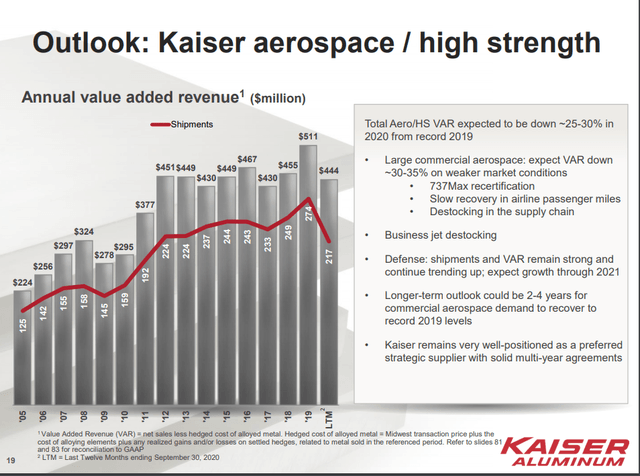

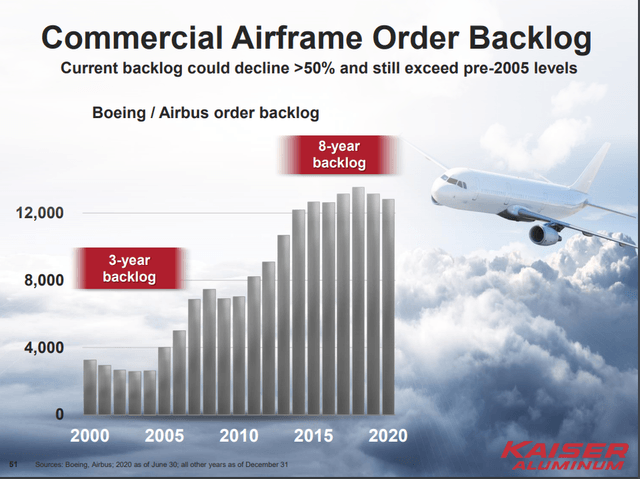

The reason for the recent stock price decline has been the decline in aerospace demand that is not expected to return to normal for a few years.  Kaiser Aluminum Stock Analysis – aerospace – Source: Kaiser investor presentation

Kaiser Aluminum Stock Analysis – aerospace – Source: Kaiser investor presentation

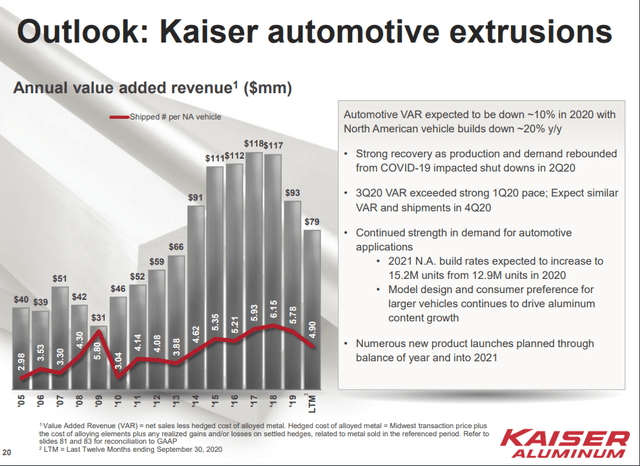

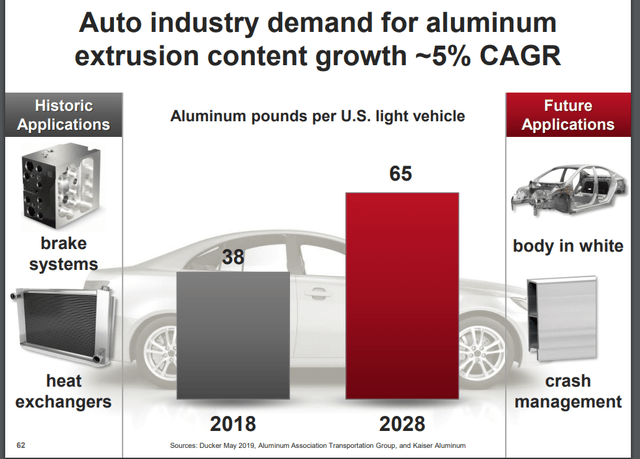

But fortunately, the automotive segment has already rebounded and so did the stock.

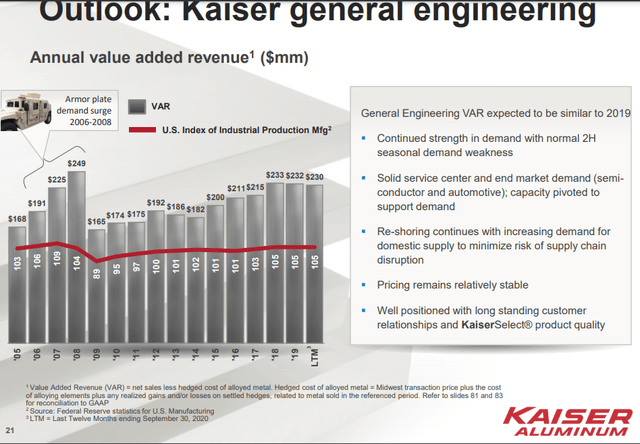

General engineering is stable as stable can be.

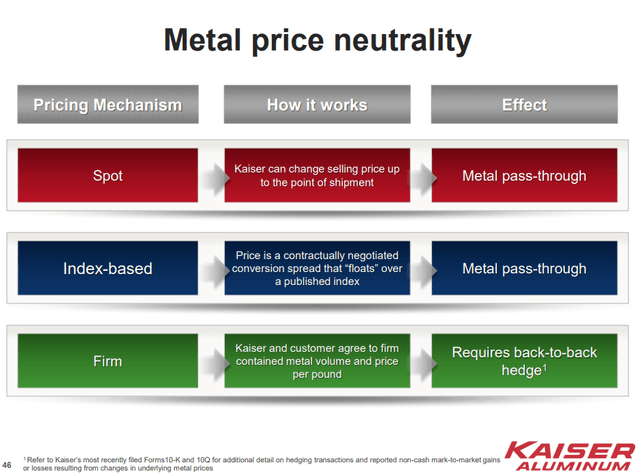

Kaiser Aluminum is not really an aluminum stock because its performance is not dependent on aluminum prices. Kaiser is more of an engineering industrial stock.

Any changes in aluminum prices are transferred to the customer so Kaiser is paid for creating the product and therefore the stock is only influenced by industrial cyclicality and not aluminum price cyclicality.

Kaiser Aluminum stock fundamental analysis

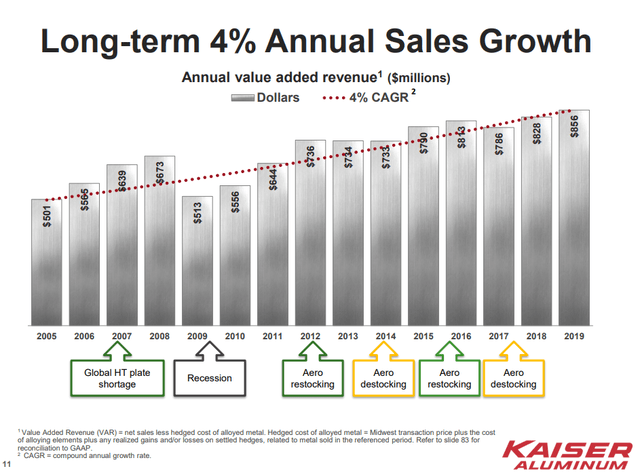

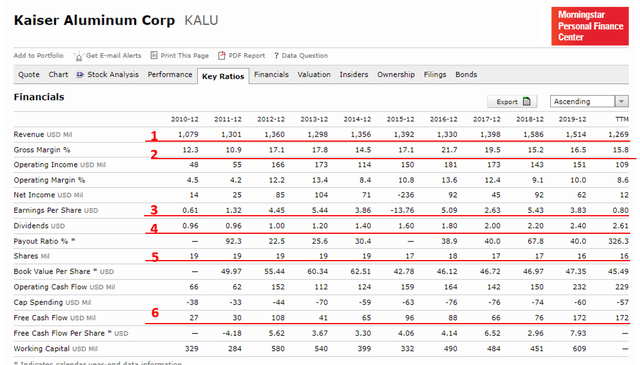

The company has been constantly increasing revenues but those revenues drop significantly when there is a real industrial recession.

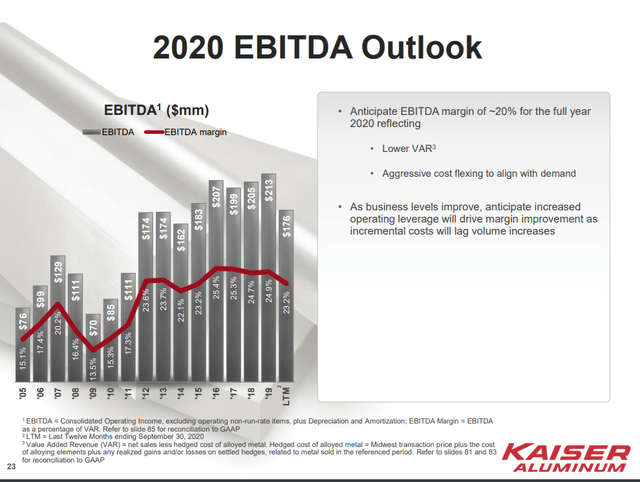

Despite the revenue decline from automotive and aerospace, the company will remain profitable thanks to its high margins.

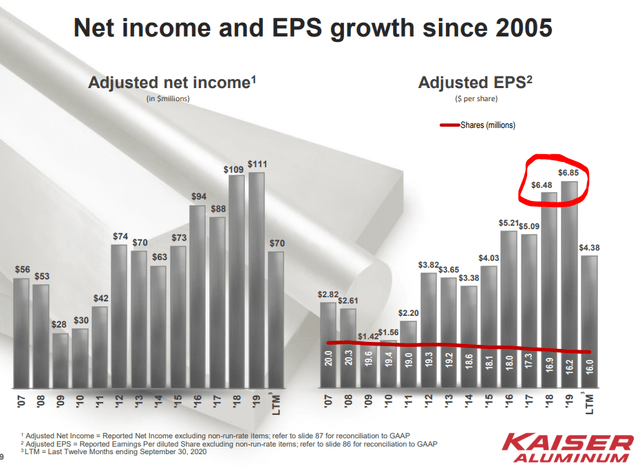

When things return to normal, the company will likely make $7 per share in earnings or even more over time.

Until then it is still expected to make $4.38, but if in the next decade, it triples earnings like it did since 2008, that will be your investment return too. Key to note that it didn’t double earnings thanks to fast revenue growth, but thanks to careful margin improvements and steady buybacks.

Total debt is significant at $850 billion, but given the low interest rates, the high margins, it should not be a concern. With a bit of debt management or more aerospace business, the company should quickly be at a debt to EBITDA level of 2 which is their long-term target with possible spikes for opportunistic acquisition like recent Warrick one.

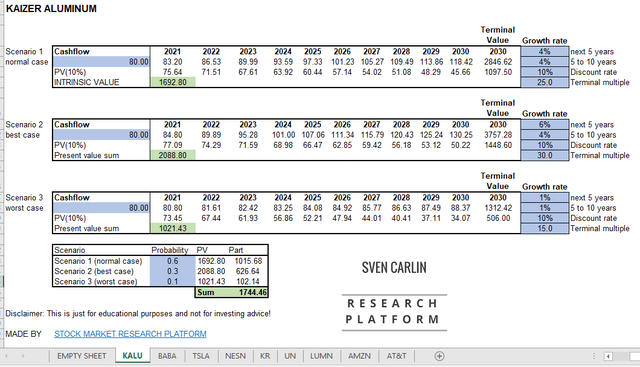

Kaiser Aluminum stock valuation

When it comes to valuations, the key is to put the right assumptions into a model. Aerospace is not expected to recover soon, but it is still expected to do well over time and recover sooner or later. Kaiser will likely remain profitable no matter when the recovery happens.

Regarding the automotive industry, the trends is for more aluminum in a car.

If they grow revenue (1) another 50% from their 2019 levels over the coming decade, increase their margins a bit (2), I would expect free cash flow (6) growth to be similar to historical levels. Thus, free cash flows could go to 150 million on average.

Of those free cash flows, they do constantly increase their dividend and if they continue to do that, they need around 40 to 50 million to do that in the future. They have spent on buybacks and lowered the number of shares outstanding by 15% over a decade. I’ll take $80 million as average FCF over the last years and will put a growth rate of 4% per year for the next decade.

In practice, 70% free cash flows have been returned to shareholders.

Given Kaiser’s quality, I’ll put a 25 multiple on free cash flows distributed to shareholders in 2030 that should give us an indication of the potential stock price in 2030.

Kaiser Aluminum stock valuation – source: Author’s calculations – you can download the template here

At the current market capitalization of $1.5 billion, Kaiser Aluminum stock seems undervalued by 10% for those expecting a 10% long-term investing return. Given the quality of the business, the positive trends it is exposed, Kaiser could be an interesting part of a portfolio.

If you are looking for good businesses where over the long-term the initial purchase price doesn’t even matter because of the quality of the business, Kaiser is one to watch carefully. Plus, 10% expected returns are not that low either. I will consider again whether to make this a covered stock on my stock market research platform or not.