STOCK VALUATION

Stock valuation – do you need complex math?

The valuation of a stock

The valuation of a stock can be extremely complex or simple. The fight is between two worlds: the academic world and the stock market investing practitioners. 99% of people who invest are academics because that is what you learned at school. Only the 1% are practitioners who have constantly beaten the market over the last 5 decades.

We are going to discuss today:

- Stock Valuation and input parameters – complex or common sense?

- Stock Valuation Formulas

- Methods of Stock Valuation

- Equity risk premium

How to do stock valuation properly to get good investing returns not academic titles or grades!

To quote Warren Buffett:

“There is so much that’s false and nutty in modern investing practice and modern investment banking, that if you just reduced the nonsense, that’s a goal you should reasonably hope for.”

What is stock valuation?

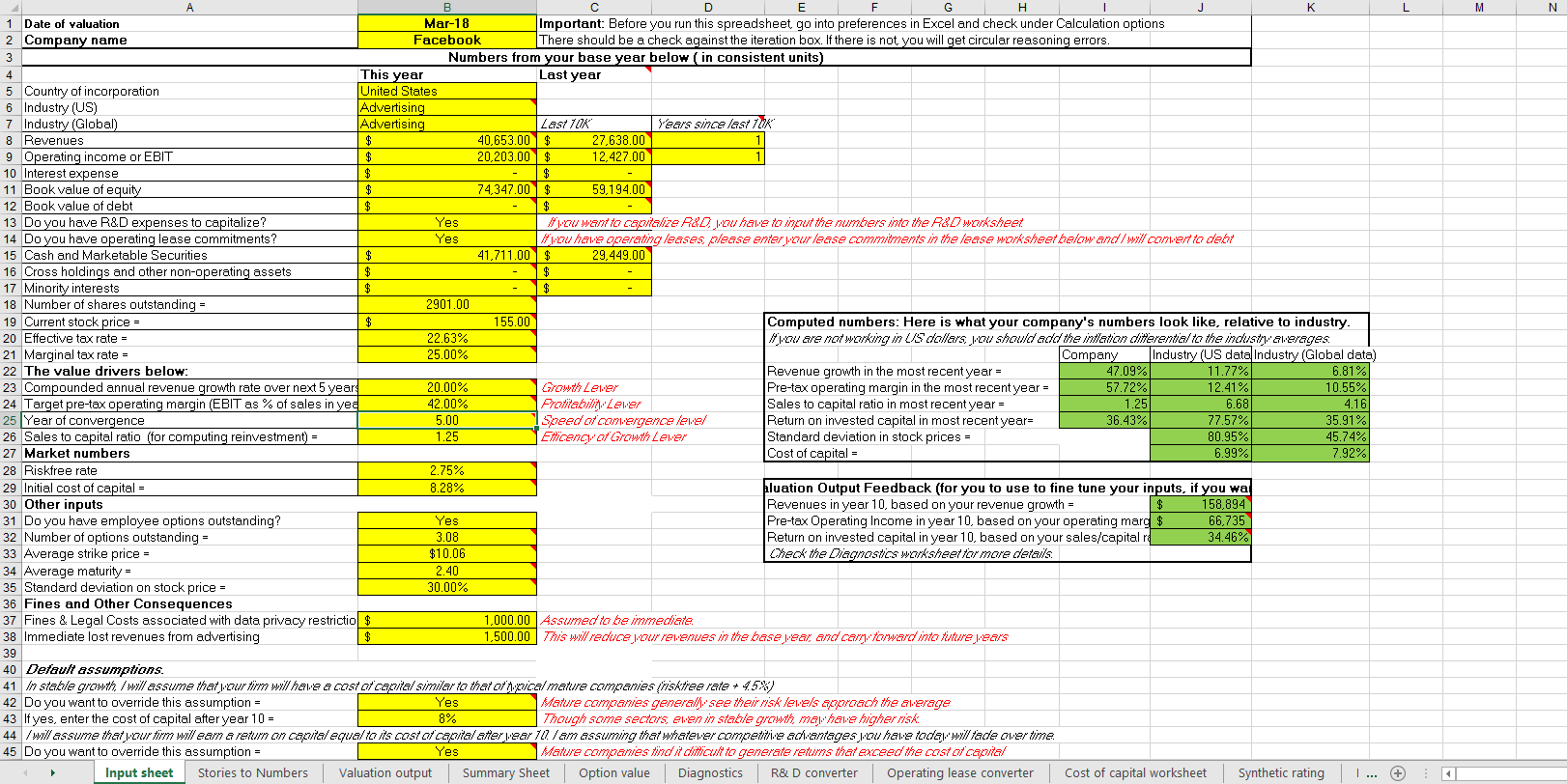

For example, I recently analyzed Facebook ’stock and my earnings model looks like this:

The parameters used are the growth rate and the discount rate that is my required return, a price earnings ratio of 10 for the terminal value which all lead to a present value. All other factors are qualitative and not quantitative, and I don’t believe anyone can put those into numbers. It is funny to compare my model with professor Damodaran’s model from the Stern School of Business at New York University. You can download his model here.

This is 50% of the first sheet of the excel file with 8 similar sheets. But let’s just focus on the first steps, the input page.

All normal things like revenue and margins, growth but then we come to the risk free rate and the initial cost of capital.

Munger:

“Some of the worst business decisions I’ve seen came with detailed analysis. The higher math was false precision. They do that in business schools, because they’ve got to do something.”

Stock valuation formulas

Stock valuation formulas can be simple or complex. The initial cost of capital – if you don’t know what is your firms cost of capital, you can compute it in a sheet like the following.

This shows more in detail what is required.

So, you are basing your investment decision on the risk free rate, ok, but then also on the beta coefficient, past equity premiums and here is where academics and practitioners strongly disagree.

To quote Munger:

“Using [a stock’s] volatility as a measure of risk is nuts.”

Methods of stock valuation

I always use this example, let’s say you are Luigi and you own a restaurant in Venice. Do you care about the risk free rate, equity premium and the beta coefficient of your business?

Luigi is a smart guy, and he only cares about the number of customers, the price of the ingredients used in the pizza etc. in order to get to the money he will be able to get out of the business in that year. He might reinvest that money somewhere, but then he will again compare what he has to put in, whether it is a good business and what he can get out. Does he care what is the price of his restaurant now or what it was 6 months ago, no, he will never sell it, he is a business owner investor and not a speculator.

Similarly, to quote Munger again:

“In the real world, you uncover an opportunity, and then you compare other opportunities with that. And you only invest in the most attractive opportunities. That’s your opportunity cost. That’s what you learn in freshman economics. The game hasn’t changed at all. That’s why Modern Portfolio Theory is so asinine.”

Buffett, looks at the business he invest in, not about what the market things about the business. That is the difference my friends. If you are studying business valuation and you have paid a lot for your studies, you degree will get you a high paying job and a good return on investment. As for your own investments, they will not benefit from what you are learning in school. All of those things that you learn in school change – the risk free rate, the equity premium, the beta, everything constantly changes, you have to have a portfolio that embraces those changes.

Yes, academics will be right in their explanations, after the thing has already happened, common sense investing is about investing before the thing gets known to all.

And that is the biggest difference between academics and practitioners. Academics can only look back and estimate what will happen, practitioners can use common sense and street smarts. That is the advantage we independent investors have, 98% of the market is all about academics because you look smart. Those who made constant market beating returns, year after year, decade after decade, don’t use those mumbo jumbo, lollapalooza formulas.

The lollapalooza effect is often discussed by Munger that explains how most people do thing because of social pressure. If you pay $250k for an Ivy League education and all you learn about is the WACC and all of your superiors use the formulas or expect you to use them in you analyses, who are you to do things differently.

Munger: I’ve never heard an intelligent discussion on cost of capital.

BTW, in my Ph.D. all that I did is to compare what Buffett has been saying all his life and what academics. The explanation of stock market price changes from the Beta coefficient came to 5% max, while what Buffett says explained 36% of long term stock price movements.

Equity risk premium

According to academics risk is the standard deviation of a security’s price over a number of periods.

However, others say different things:

Risk is not knowing what you are doing – according to Buffett

Risk is looking for what you don’t know – according to Dalio

Risk is calculating what is the max permanent capital loss – according to Klarman

Risk is not short term volatility – according to Munger

Stock market valuation

Investing is yes about valuation, but not about what the market tells you the value is, it is about what you think the value of the business is and the advantage we have is to buy when the markets backward looking says one thing, but value screams the opposite.

“We don’t give a damn about lumpy results. Everyone else is trying to please Wall Street. This is not a small advantage.” Munger

For example, the recent drop in Facebook’s stock price would have made the stock riskier to academics due to the higher volatility and higher beta, but a real investor would see the stock as cheaper. The more you know about what you are doing, the lower is your risk.

How to do stock valuation

The key things to watch are:

- Price earnings ratios,

- Earnings growth

- Fundamentals – book value

- Have your own discount rate if you must as it is simply easier to compare

- Compare investments and invest in the best handful

- Think what can go wrong

- KEEP IT SIMPLE

The point is to know the difference between investing success and academic success – academics cannot beat the market when using their formulas and complex analyses, and that is why the continue to discuss the efficient market theory etc. Investment practitioners, those who apply common sense to what is going on, they beat the market over the long term. I have both a Ph.D and I have beaten the market, better to say destroyed the market in the last 16 years just because I applied common investing sense to what I did in the stock market, not academics. So, I can talk about this.

I’ll finish with Munger who is amazing as always:

“I have a name for people who went to the extreme efficient market theory—which is ‘bonkers.’ It was an intellectually consistent theory that enabled them to do pretty mathematics. So I understand its seductiveness to people with large mathematical gifts. It just had a difficulty in that the fundamental assumption did not tie properly to reality.”

If you want to save time by having me do full time stock market research and valuation for you for just $0.96 per day, check my Stock Market Research Platform.

If you enjoyed reading this or watching my videos on YouTube please subscribe to the weekly letter where I summarize what I’ve been doing through the week and the videos that were posted.