Fugro Stock Analysis – Promises, too risky at any price

This Fugro stock analysis (AMS: FUR) is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential with a margin of safety, so as would Buffett say; I start with the As. At the end I need to find only a handful and I’ll do great over my investing life.

Fugro Stock Price Overview

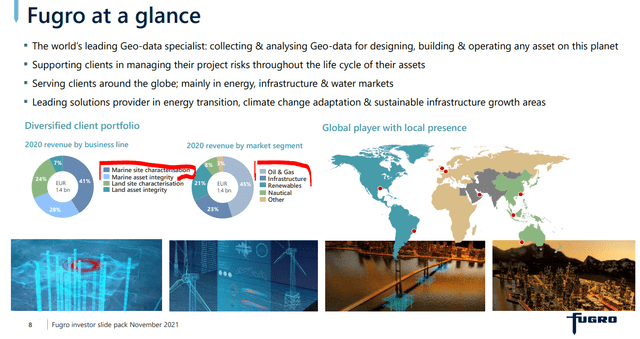

Fugro collects and analyses geo data from the earths surface and subsurface. Unfortunately, the one certain thing that went deep is the stock price that hasn’t recovered from the early 2010s commodity boom.

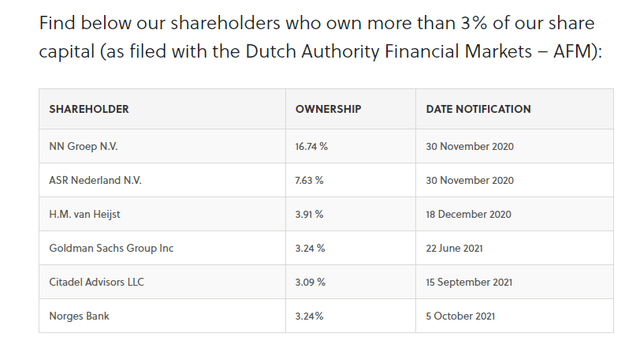

The ownership is with mostly institutions.

Fugro stock analysis – business overview

The business model is focused on marine work and since 2014 it doesn’t pay much to drill much offshore for oil, so Furgo’s business suffered.

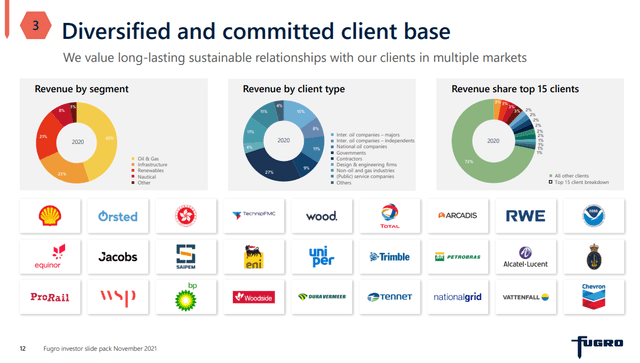

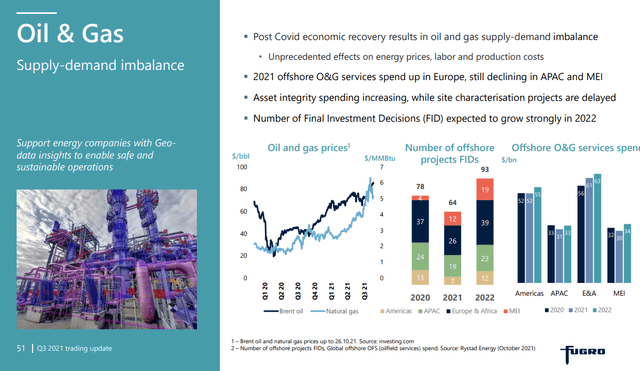

The majority of revenues is oil and gas related.

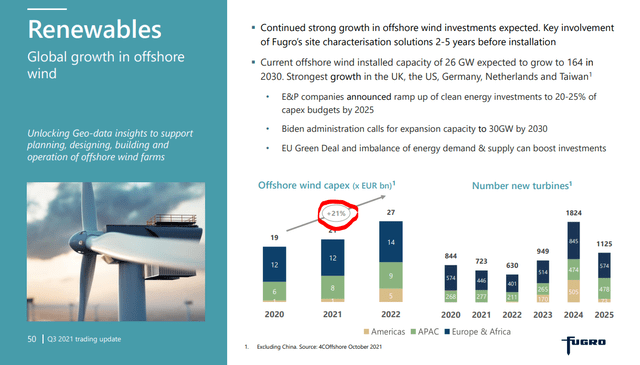

Their strategy is to shift to the renewables and infrastructure markets, but there you don’t need as much data.

But, the renewables market is expected to grow, so that should be positive for them as they have the means to do the work.

Given that oil prices are relatively high, investment in oil might pick up too.

3

3

Fugro stock analysis – Finances

This is a company that has been reinventing itself for half a decade now and is losing money in the process.

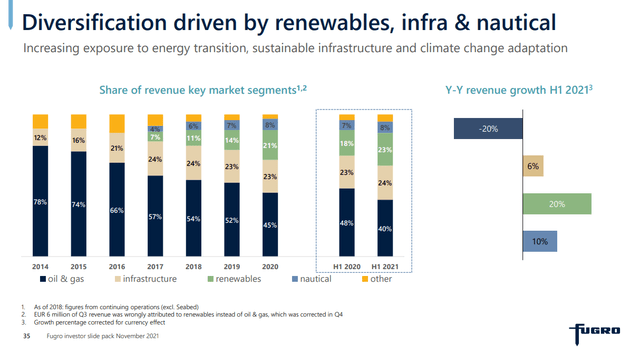

The diversification to renewables sounds nice, but it is not that they are growing much there, it is just that other segments are declining as revenues have halved since 2015.

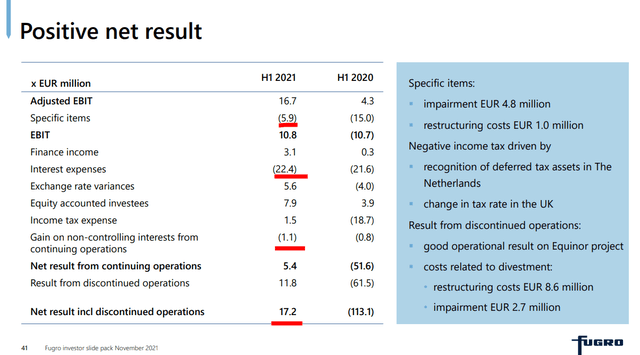

With 22 million EUR in interest payments for half a year, I think they have a lot of debt.

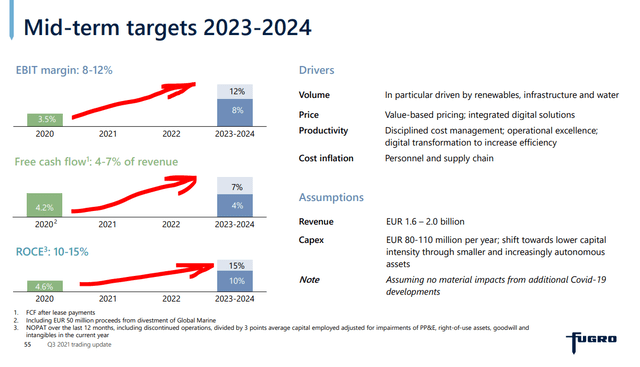

The targets are in line with what every analyst wants to hear. I don’t see anything beyond that those just look nice there.

But even with free cash flows at 100 million, thus 5% of 2 billion revenue.

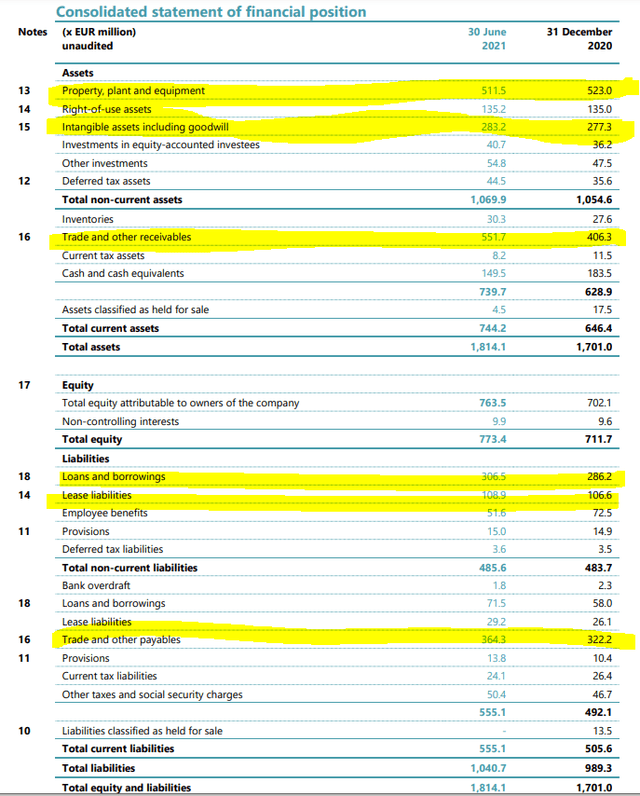

Debt levels are not that much, they have a lot of cash, likely thanks to capital issuing in the recent past.

Fugro stock analysis – conclusion

Fugro looks like another Dutch business involved in those businesses that are surely not easy, where costs are always higher than expected and customers go bankrupt even more often. So, this is too risky in general for me, especially as the company doesn’t make any money, has high debt and high goodwill.

Maybe they will do something good, but that is mostly promises, plus things might be good for a year or two and then bad again with more dilution etc.