BERY Stock Analysis – Interesting Small Cap Offering 10% Returns

I’ve been researching the MSCI Worls Small Cap Index, stock by stock, (you can see more about that here) and one of the interesting ones found is Berry Global Group (BERY). I’ll first discuss the stock price, business, fundamentals and then conclude with a valuation. Here is a small cap video discussing what I look for and why I am researching BERY, BERY stock analysis below.

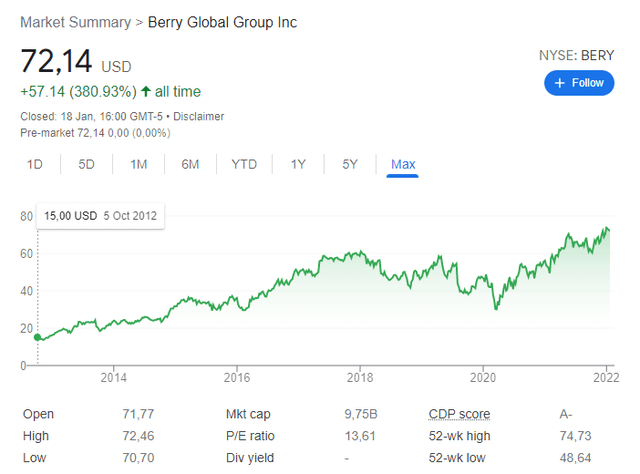

BERY Stock Price Overview

Over the last decade BERY stock did really well which is already an indication that the business is a good one and can compound across cycles.

The current market capitalization is $9.75 billion which is what I will use to compare to my valuation.

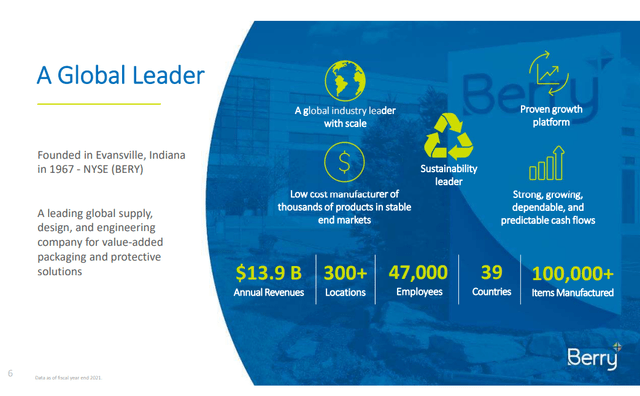

BERY Stock Analysis – Business Overview

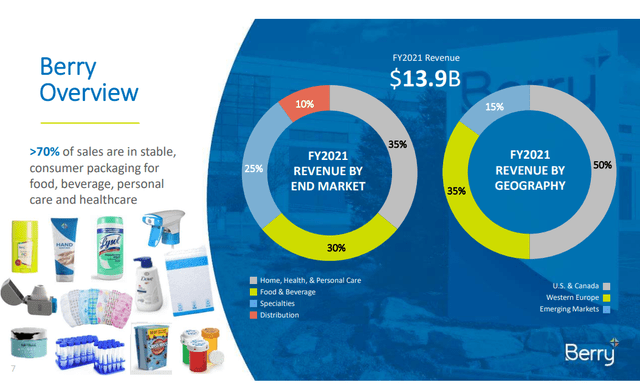

BERY operates in the currently booming packaging industry but I consider it a cyclical industry because there are no real barriers to entry. When it comes to cyclicals, the best time to invest is when things look ugly, not when things are booming, but as we have seen above with the stock price chart, BERY can compound across cycles.

Plus, once the business connections are made and if you have the scale to be a low cost manufacturer, you can reach a decent return on capital over time despite cycles.

Berry is the global leader in a sector that will likely continue to expand over the long-term.

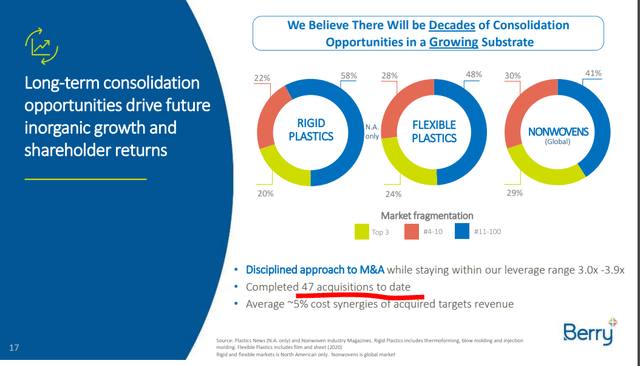

The business will have its ups and downs as the cycles evolve, but it is likely Berry will continue expanding over those cycles thanks to its leadership position and scale. The strategy is to continue growing by making acquisition and integrating the smaller players into the Berry ecosystem.

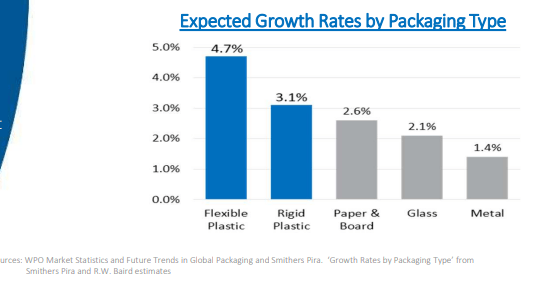

The market is expected to grow and this is a key when it comes to investing because with a positive tailwind investing is less risky and brings to higher rewards. In a growing sector, investing mistakes can be softened by general sector growth while business returns compound faster.

For more information about Berry’s strategy, sustainability and strategic focus, please check the Berry Investor Relations Presentation.

BERY Stock Analysis – Financials

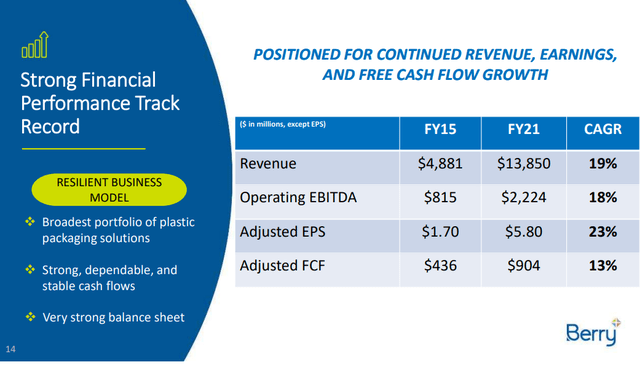

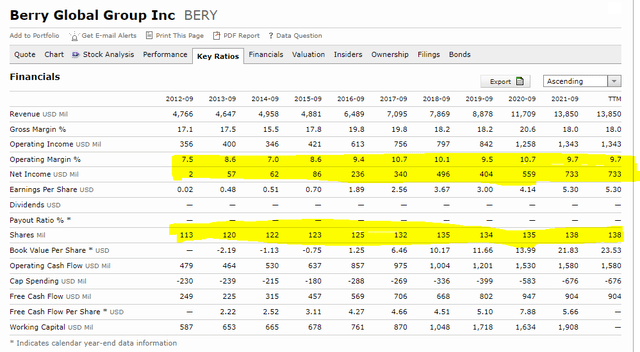

Up till now, Berry’s growth strategy has been working really well.

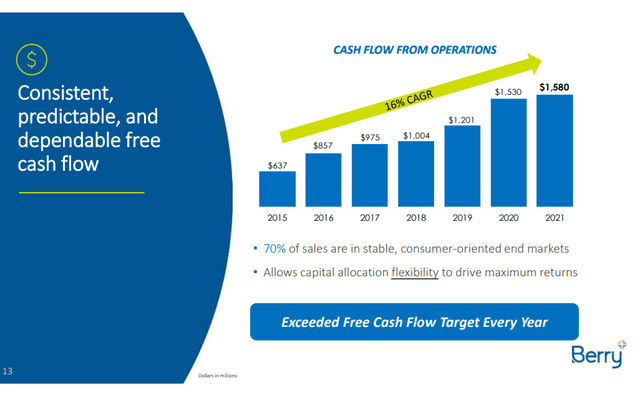

Current cash flows have boomed thanks to the situation with increased online ordering and home consumption in addition to inflation and supply issues, so I would expect a contraction there as things normalize, but $1 to $1.2 billion in operating cash flows as it was the case prior to 2020 is still good from an investing perspective.

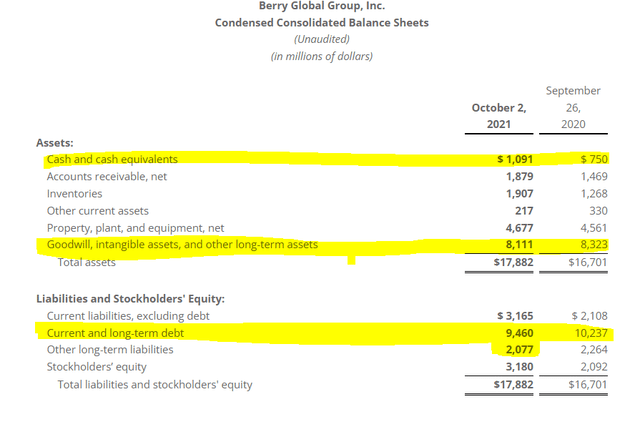

And now we come to the most significant risk when it comes to Berry. The above all sounds great, but it comes at a cost; leverage.

The company is working on lowering debt, but $9.4 billion is a significant number or $3.1 billion in equity and $8.1 billion in goodwill as a consequence of all the acquisitions.

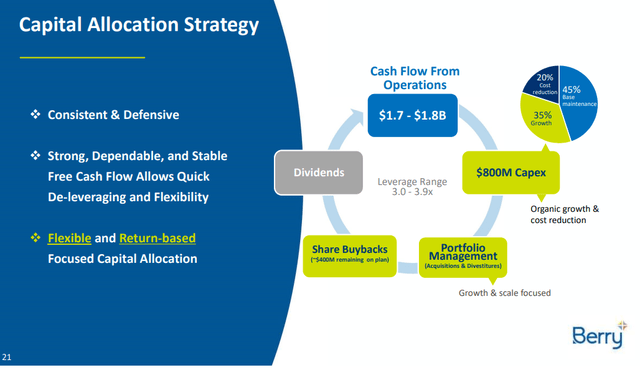

The capital allocation strategy is focused on investing to keep up with the competition and grow, share buybacks and also dividends while holding a leverage range between 3.0 and 3.9 on EBITDA.

If you have one or two bad years, where EBITDA goes to $1 billion, you suddenly find yourself with and leverage ratio of 9, which usually breaks covenants and leads to hell from an investing point of view. This is the main risk but if it doesn’t materialize, BERY stock will likely do really well.

The company is doing some buybacks but the actual number of shares outstanding has been increasing so I wouldn’t give much significance to those.

BERY Stock Valuation

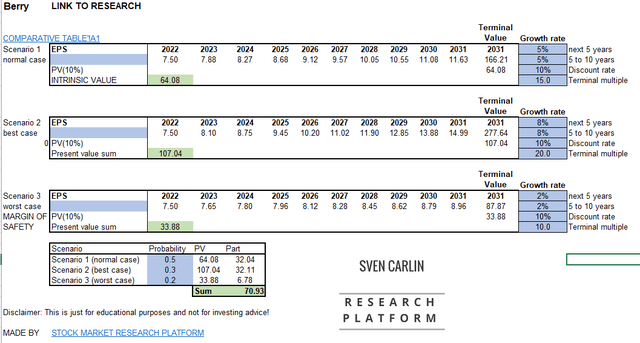

Apart for the leverage risk, with the company expecting adjusted earnings per share to be $7.20 – $7.70 for fiscal year 2022 Berry, we are looking at a company trading at a PE ratio of around 10.

With interest rates at historical lows, it even isn’t smart to lower your debt, but it is a risk to consider and possibly also the reason for the low valuation.

Anyway, if I take the earnings forecast and assume 5% industry growth ahead for Berry in a normal scenario, with a 8% growth rate in the best case scenario and a 2% in the worst case scenario, I get a stock valuation of $70.93 while expecting a 10% return on investment (with 50% weight for a normal, 30% best case scenario and 20% for a worst case).

BERY stock valuation – Source: Sven Carlin Research Platform (free downloadable template with list of 100 stocks analyzed)

BERY Stock Analysis – Investment Risk And Reward

In the current market, a business offering a likely 10% long-term return isn’t bad. However, the packaging industry looked ugly around 2015 while now it looks great and I would categorize it as a cyclical industry. According to Peter Lynch and his stock categorization, cyclicals are best bought when things look ugly but are starting to improve. At the moment, BERY looks really good, which means the risk of investing is higher and the likely returns ahead will be lower. Those that dared and bought in the early 2010s did really well, but those did buy into high uncertainty.

For me personally BERY stock doesn’t cut it as there is too much leverage risk and it might be the wrong moment in the cycle to invest. However, I think it is a good business, in a good industry and trading at a relatively cheap valuation so see how it compares to your other investing options.

If you enjoyed this analysis, don’t forget to download the free template above with many other stocks analyzed and also consider my newsletter: