S&T AG stock analysis – Profiting from IoT and M&A?

S&T AG stock analysis is part of my full, stock by stock analysis of the Austrian Stock Market that offers interesting investing opportunities. Check my Austrian Stocks List for more Austrian stocks. Global stock analyses list is here.

The S&T System Integration & Technology Distribution is an Austrian company with headquarters in Linz. Before 2008 it was called Gericom, but the company had suffered a drastic decline in revenue, and the stock price plummeted by 96 %. It got taken over by the Taiwanese company Quanmax Inc. In 2015, the company merged with S&T System Integration & Technology Distribution, which led to its name change. Now it trades at the TecDax – a German stock index focusing on technology stocks.

The company has strong revenue growth, cyclical swings in the stock price, and an ambitious acquisitions plan.

S&T stock price analysis – VIE:SANT

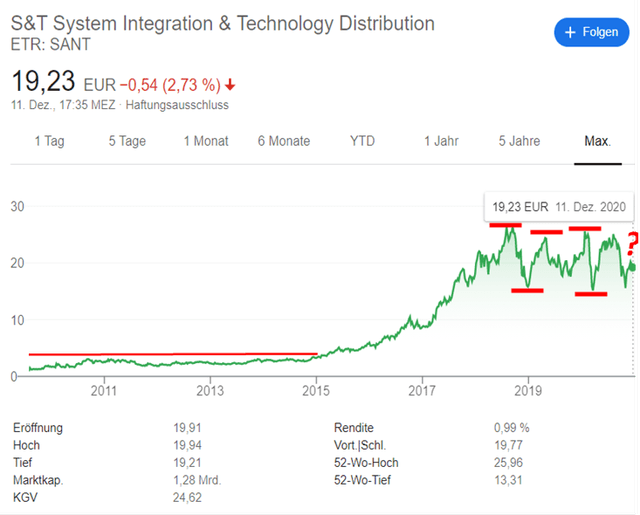

After the dotcom bubble busted, the original stock (Gericom) crashed from over 70 EUR to under 1 EUR. The stock stayed flat for more than ten years, and only since 2015 started to climb again.

S&T stock never climbed over 26 EUR and consequently always quickly fell back to around 16 EUR. By just looking at the stock chart, we could sense a kind of cyclicality. It is not enough to look at the chart for categorizing it for a cyclical Peter Lynch stock. Let us look at the business model, the fundamentals and give an outlook.

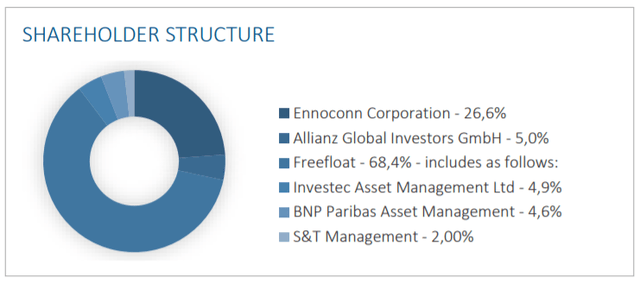

Their shareholder structure shows that the management holds 2% of the company. Not much but better than no management commitment. The Ennoconn Corporation has a controlling stake. Ennoconn is a subsidiary of the Taiwanese company Foxconn.

S&T AG Business Overview

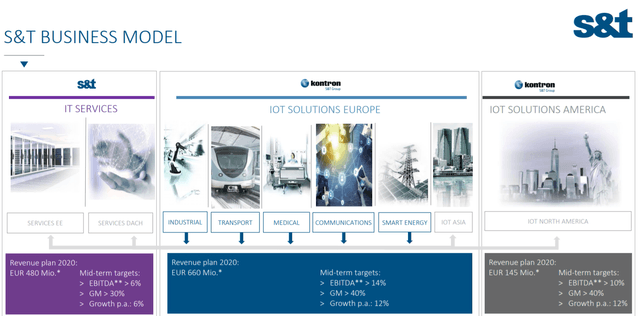

The company has three segments: IT services, IoT solutions Europe and IoT Solutions America.

Their core business segment (IT-Service) expects a growth of 6 % per year – a steady but sure growth. The other two segments expect growth of 12 % per year. S&T built these with Kontron’s acquisition in 2016, which led the company to be one of the leading suppliers in the international markets for Internet 4.0 or Industry 4.0 and IoT (Internet of Things) technologies. IoT is a network of physical objects (things) embedded with sensors and software to connect and exchange data with other devices and systems over the internet. In this context, other buzzwords are smart homes, smart energy, smart factory, and predictive analytics, for example. So basically, everything which should become smart in the future.

The gross margins (GM) are relatively high, with 30 % in the IT-Service segment and 40 % in the IoT segments.

The IT Services is the core competence of S&T and does offer a low single-digit growth. After acquiring Kontron (2017), the IoT segments thrive and are the business’s possible catalysts.

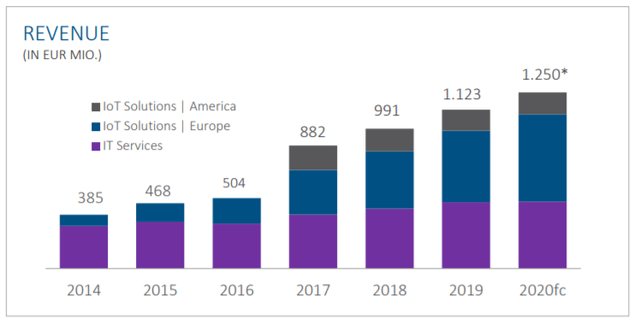

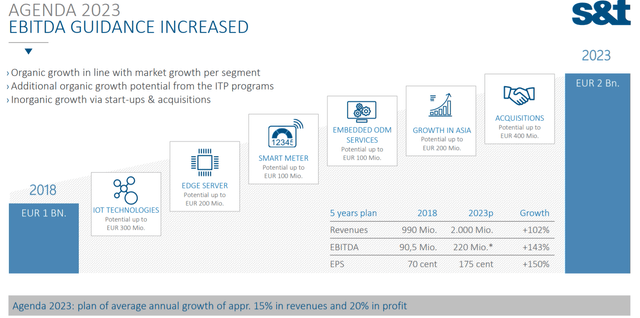

S&T builds the vision 2030 mainly on digitalization. The company expects strong growth in its IoT Solutions segments. Their short-term goal is to hit 2 billion in revenue by 2023.

To achieve its revenue goal, the company needs to grow its business by 15 % per year. This growth should come from six separate areas. S&T focuses on digitalization in four areas (IoT Technology, edge server, smart meter, and embedded ODM services). The other areas are Asia, where S&T expects to grow by 200 million EUR, and acquisitions with an estimated 400 million EUR potential. S&T intends to achieve about half of the growth with acquisitions. Acquisitions are often a dangerous way of growing because prices of other businesses ore often sky high, especially when you announce it to the world that you are going to grow by doing acquisitions and you never know how will those end.

According to the Harward Business Review, Mergers and Acquisitions are abysmal failures in 70 to 90% of cases. As we are in an era of free money, it seems smart to do acquisitions at any price, but that often backfires and I don’t wish to be at the other end of such a situation.

S&T AG Fundamentals

The company has around 253 million EUR in cash and non-current liabilities of 322 million EUR plus current financing liabilities of 52 million EUR. The equity is relatively high in comparison (392 million EUR). The cash is not a precaution in case of a crisis, but the needed liquidity for accomplishing their acquisition goals.

In 2019 S&T earned 83 million EUR in net cash flow from operating activities. If we subtract the CAPEX (27 million EUR), we get to a free cash flow of 56 million. But if we take the acquisitions into account (as it is the central part of their growth story), the free cash flow gets reduced by another 27 million EUR and therefore amounts to 29 million EUR.

With the market capitalization being 1,28 billion EUR, this equals to free cashflow rate of a little bit over zero percent and that in a good year. With the free cash flow, they pay out a dividend of 10 million EUR or 19 cents per share (1 % yield) and have a buyback program worth 14 million EUR. If the economy has a cooldown, the cash flows can go negative fast which explains the cyclicality of the business and volatility of the stock price.

S&T Stock Valuation and Catalyst

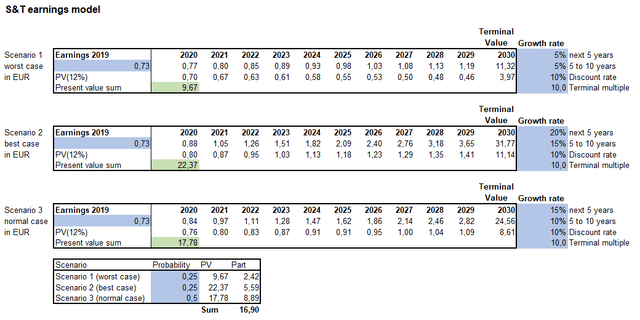

However, the cash flow is not the catalyst in S&T stock. It is the expected growth. As written above, they want to grow profits by 20 %. That will be the best-case scenario. Normal-case is the 12 % growth of their IoT segments + 1 % dividend and 1-2 % share buybacks. Worst-case is just the 5-6 % of their IT-Service segment, the most conservatively business.

This model’s general assumptions are a discount rate of 10% and a terminal multiple of 10. These figures are estimated conservatively as no recession, or economic downturn is considered.

In the earnings model below are three scenarios:

- Scenario 1 (worst case): 5 % growth for 5 years and then 5 % growth with 25 % probability

- Scenario 2 (best case): 20 % growth for 5 years and then 15 % growth with 25 % probability

- Scenario 3 (normal case): 15 % growth for 5 years and then 10 % growth with 50 % probability

These three scenarios equal to a fair value of the S&T stock of about 17 EUR. In the last downturns, the stock reached these price levels and a bit below. With their best-case scenario of 20 % growth in the next year, the stock value at 22 EUR is fair and is below the current stock price.

S&T stock investment outlook

S&T has a healthy balance sheet with about 112 million in net debt (all debt – available cash). It is in an excellent position to profit from digitalization, especially the trend of IoT. In the Peter Lynch stock categories, S&T is a fast grower if they can keep up with their ambitious growth plans. Therefore, S&T will stop growing in the future as 20 % is not sustainable for the long-term. Later, it will be to check in which other categories the stock will fall.

If you believe in the company’s story, it offers a 10% return at 17 EUR; therefore, S&T is a bit overvalued when considering all three scenarios with their probabilities.

In conclusion, the company is not offering the 12-15 % business returns I am looking for; thus, S&T is not a buy for me, and the future growth will come through acquisitions and the trend of IoT. Not a safe bet given the risks of such a strategy.

You have to see how it fits your portfolio and investment style.

Please check the complete list of stock analyses made on this value investing site.