The Risk And Reward Of Investing In FCX Stock Explained (When to Buy)

The goal of this Freeport-McMoRan stock analysis (NYSE: FCX STOCK) is to explain the risk and reward of investing in FCX so that you can see how it fits your portfolio. FCX is teasing you with a possible major rally for copper and 100% possible upside for the stock. Is it a real possibility or just a corporate trick?

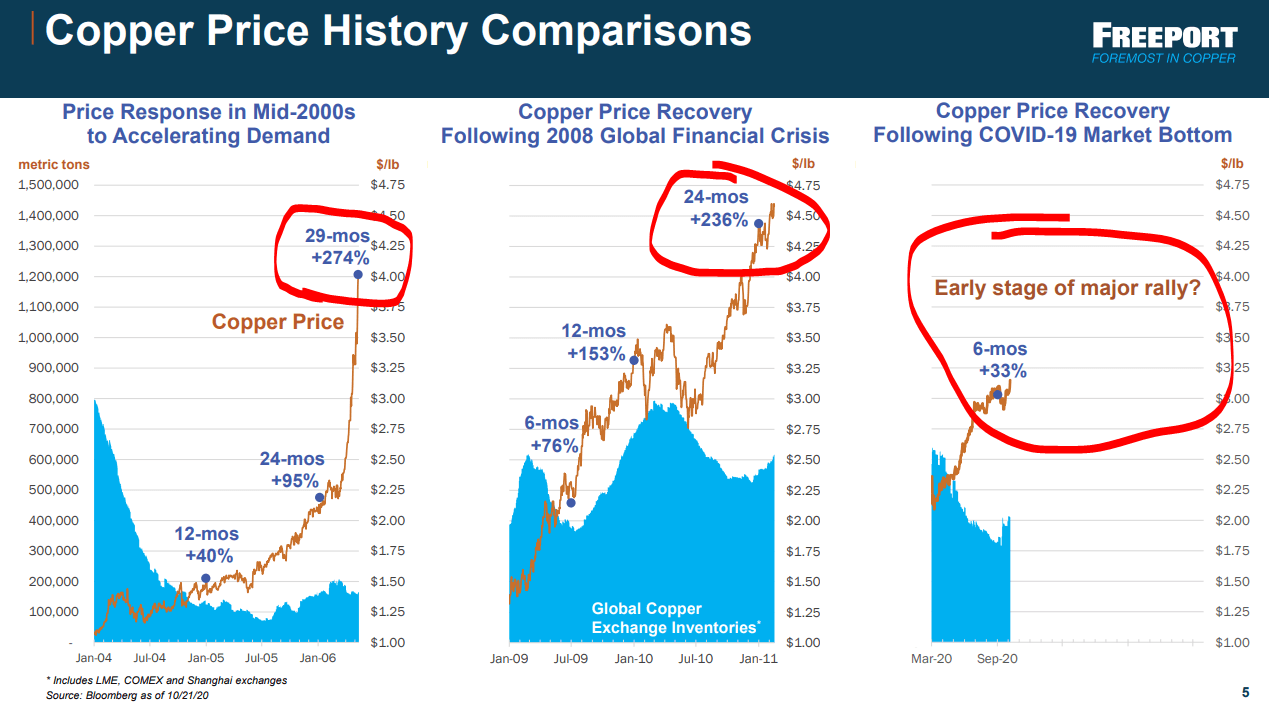

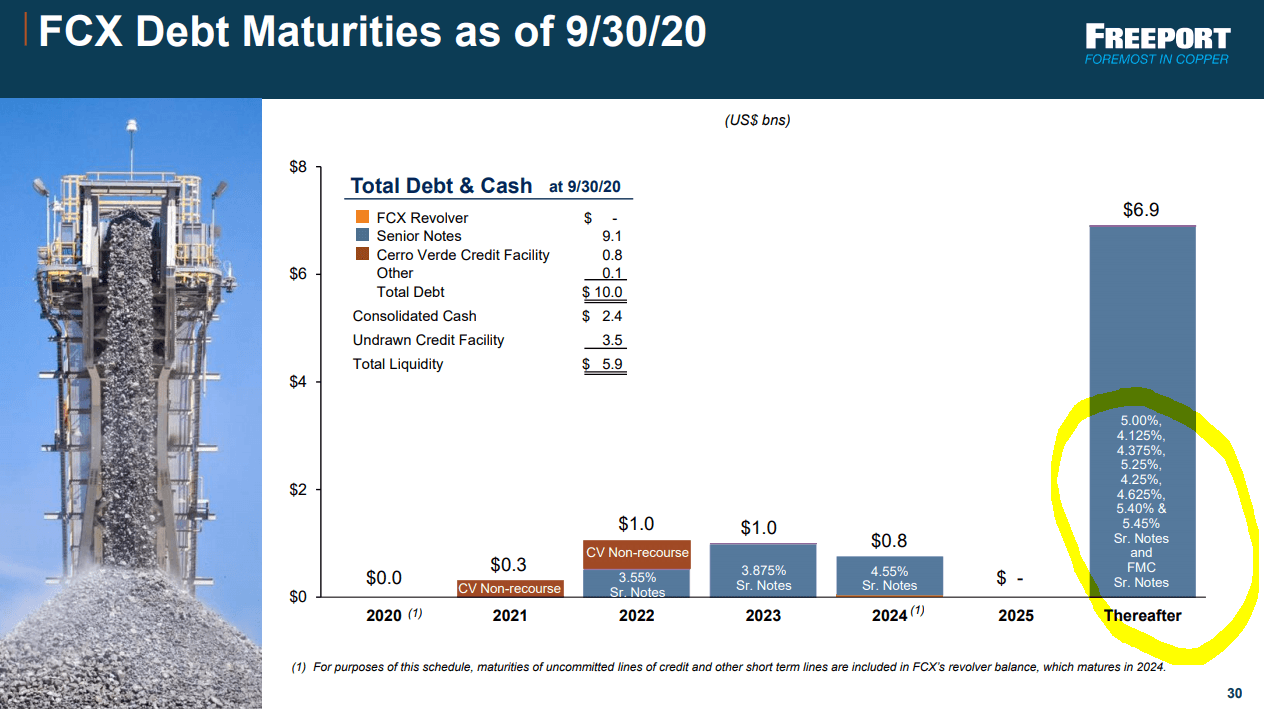

Copper price major rally – Source: Source: FCX Q3 2020 presentation

A major copper rally will likely happen one day, but it has to be preceded by a very bad copper situation for longer. Something that I’ll carefully watch for over time. To better understand the key driver behind investing in copper stocks like FCX, please enjoy this video discussing the situation with copper, demand and supply, the outlook and the current risk and reward.

Here is the copper thesis investing article.

Freeport-McMoRan FCX stock analysis

Freeport-McMoRan stock or FCX stock is on top of the copper ETF. I’ll start this FCX stock analysis with a stock price overview that will give us the market capitalization which will be the basis for the valuation part later and show how the stock moves in relation to copper price movements.

The stock price analysis will be followed by a business overview, stock valuation and investment discussion at the end. The key to understand is the likely free cash flow over the next decade, the quality of the assets and the specific issues for FCX. That should give enough info to understand the long and short investing implications for FCX stock.

Excerpt from copper stocks table with key factors – FCX stock – Source: Sven Carlin Research Platform

Compared to a few other copper miners, FCX is fairly priced given the quality of the assets. The volatility of the stock is similar to others but the assets might be on the better side given the long mine life and low cost production.

FCX stock price analysis

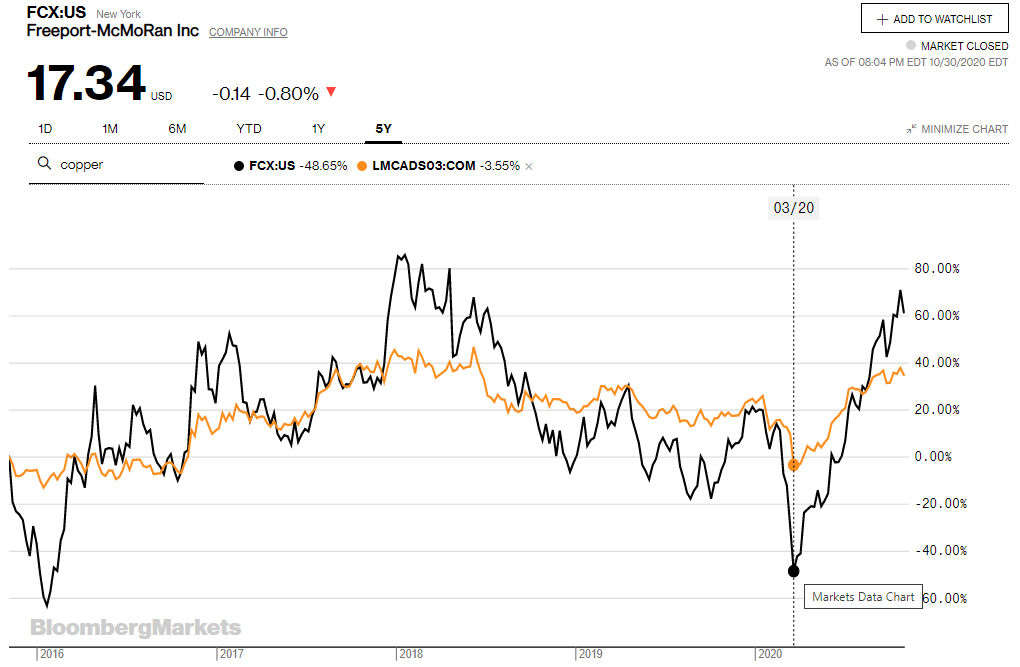

FCX stock price gives us one certainty; things with copper stocks are and will always be volatile. As miners, margins and profits depend on copper prices where a small change in the price of copper has a big impact on the company’s profits and consequently on the stock price. But few really understand this and therefore the volatility also represents a huge opportunity for those who are willing to wait and buy at the right time with a margin of safety and a good strategy.

The current FCX stock price is at a low level from a historical perspective so there is still opportunity.

In January of 2016, during the commodity crisis, the market thought FCX will go bankrupt due to the high debt levels and relatively high mining costs. That didn’t happen and the stock is now 4 times higher than back then but still much lower than the highs FCX stock reached in 2008 and 2011 of above $60.

Similarly, to 2016, FCX stock fell to a low of $5.31 in March of 2020. The reason is that copper prices went close to $2 and many expected them to stay that low. The fact with FCX is that with copper close to $2, it doesn’t make any money after capital expenditures. Therefore, the market doesn’t know how to value it, the stock enters into a negative spiral and the price can go really low. For those who know what to do, it represents an opportunity and that is the main focus of this analysis.

An investment in FCX will depend on copper prices going forward but by identifying the risk and reward based on the current FCX stock price and copper price fundamentals, we can try to find the best, low risk, high reward times to invest in a copper stock.

FCX stock closely follows copper prices where a 10% change in copper prices usually results in a 20 to 30% change for FCX stock. Only when copper prices go very low and get close to $2, then FCX stock really crashes, even 50%, like it was the case in 2016 and March 2020.

The reason for FCX’s bad stock performance when copper prices are getting close to $2 is that the company isn’t really profitable at those levels which changes the market’s perspective on its debt, refinancing options and the negative sentiment quickly spirals into a tragedy. However, over the last two decades, those were the best times to buy FCX.

FCX business overview

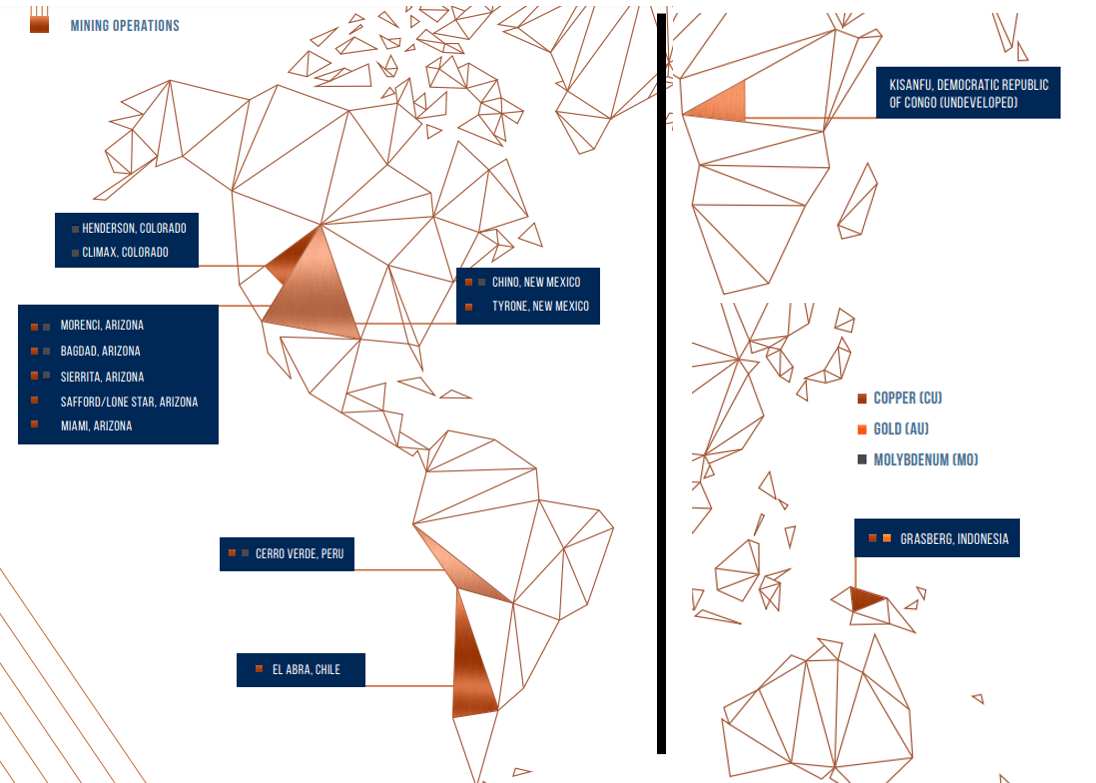

FCX is one of the largest global copper producers, well diversified and essential to the global supply of copper.

FCX copper mine overview – life of mine

Its core operations are in the U.S., Peru, Chile and Indonesia.

All of the above are really good mines with long-life mining ahead.

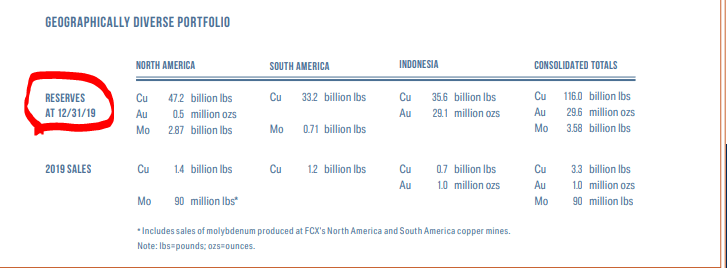

If I take 2019 production levels and compare it to the reserves (Ore reserves are valuable and legally, economically, and technically feasible to extract) there are still 33 years of mining ahead in North America, a bit less than 30 years in South America, more than 30 years in Indonesia for a consolidated total of approximately 33years of mining ahead. That is remarkable and something to really keep in mind when investing in copper miners.

Another key factor for FCX is that it is not just a copper miner, the gold component is also important as the company produced 1 million ounces of gold in 2019.

The above reserves estimations were determined using metals price assumptions of $2.50 per pound for copper, $1,200 per ounce for gold, $10 per pound for molybdenum and $15 per ounce for silver. Prices are currently higher which means it is likely FCX will be a miner for the next 3 decades and much more.

As for resources, FCX identified estimated mineralized material totalling 133 billion pounds of incremental contained copper, which was assessed using $3.00 per pound. Thus, likely another 30 years of mining on top of the 30 years ahead. That is important because usually mines and miners have a finite life, not FCX.

FCX Mine ownership

Indonesia – FCX has a 48.76 percent interest in PT-FI and manages its mining operations. Based on their deal, the economic interest is 88% through 2022, after that 48.76%. Morenci is owned 72% while the rest is 100% owned.

FCX outlook – key for valuation later

In a recent call with investors, when asked about the future necessary capital investments to keep up production, the CEO answered how there is not really a timeline but there are great options. Further, the focus on the company has been on low hanging fruits related to costs and operational improvements.

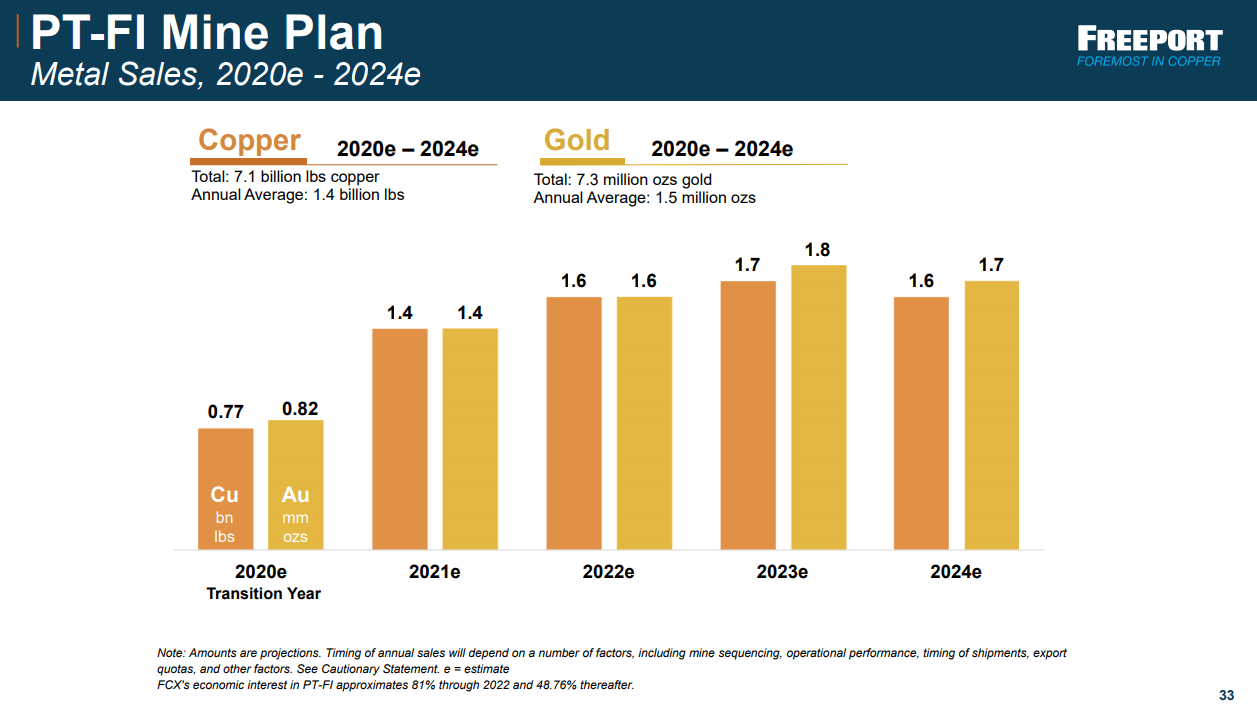

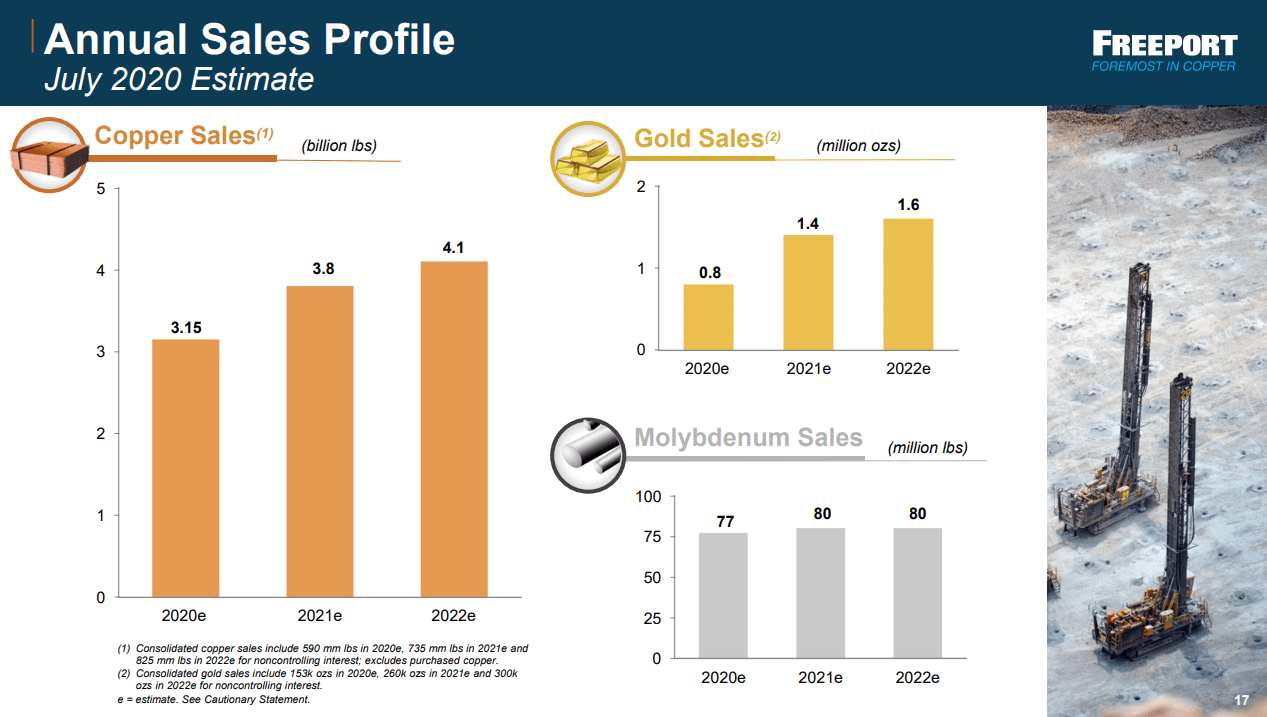

Consolidate production for 2020

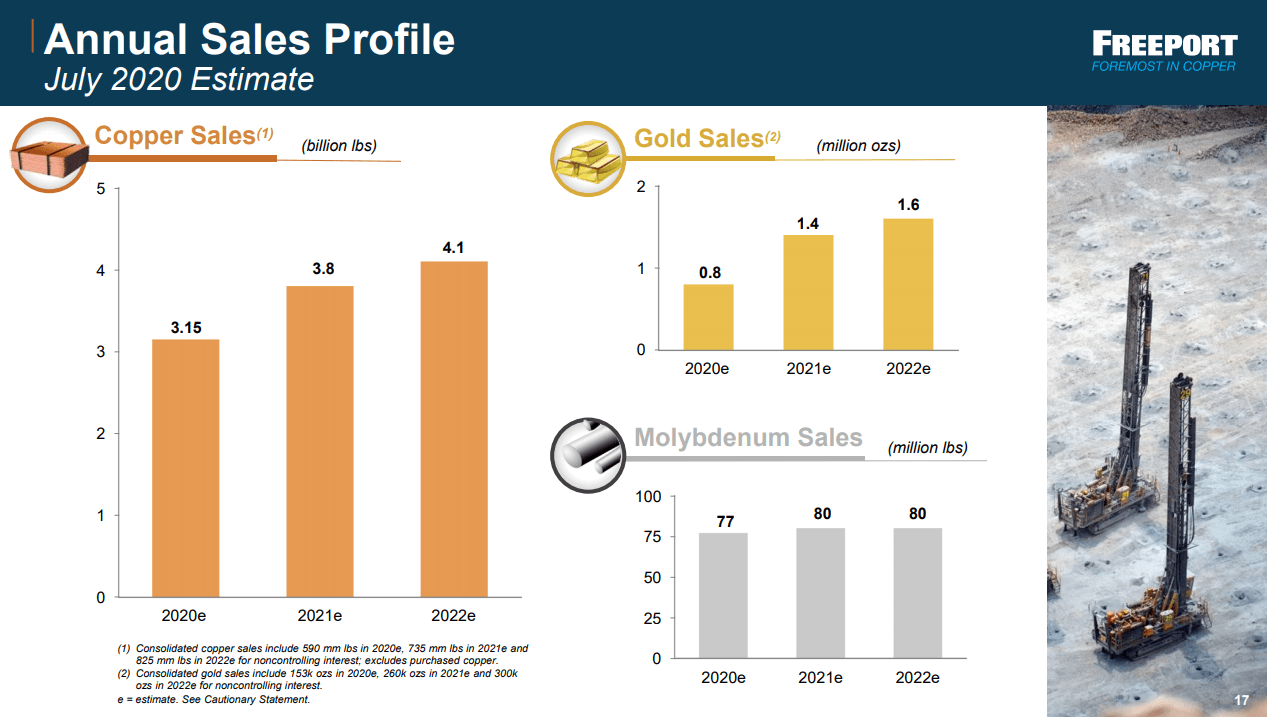

Production is further expected to increase and consolidated sales for 2021 are currently expected to approximate 4.3 billion pounds of copper, 1.4 million ounces of gold and 90 million pounds of molybdenum.

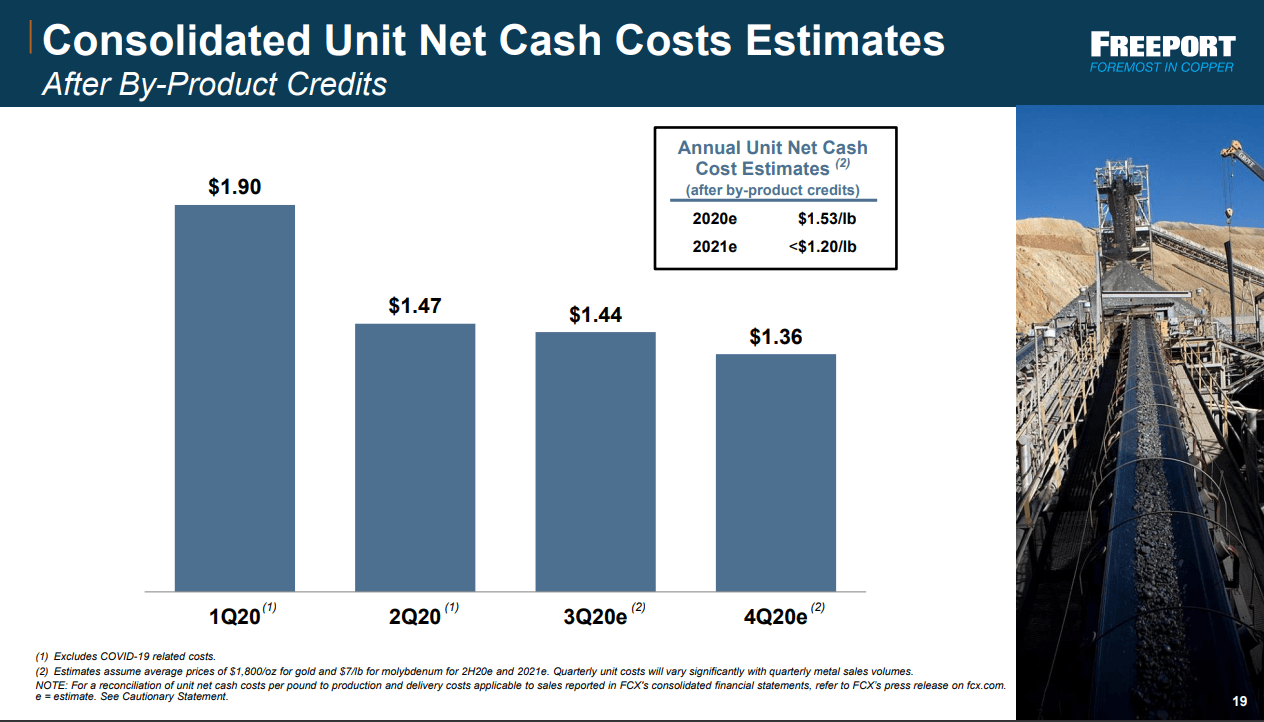

Mining costs are expected to be at $1.75 per pound of copper, these are cash costs and include gold and molybdenum sales.

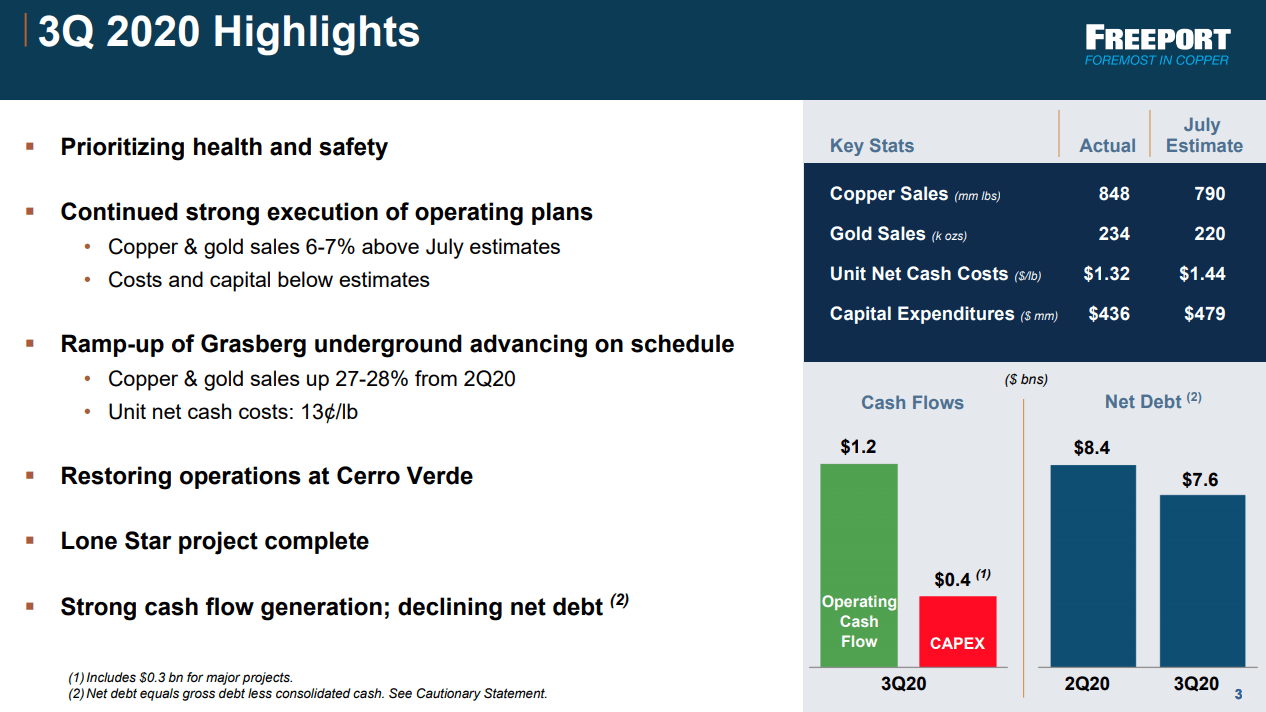

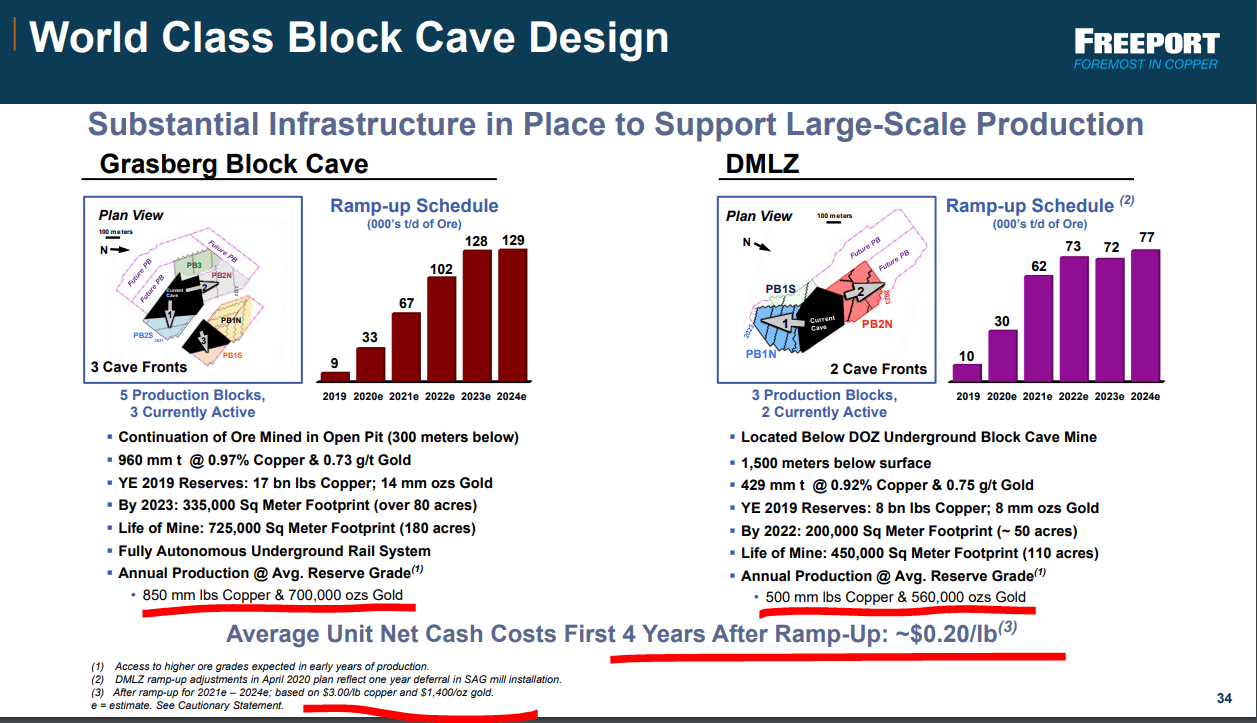

The ramping up of Grasberg in Indonesia is key for FCX because it should lead to positive free cash flows by the end of this year and even improve the situation in 2021. The Lone Star project is also being completed in the US and Cerro Verde is ramping up nicely after the mandated shutdown.

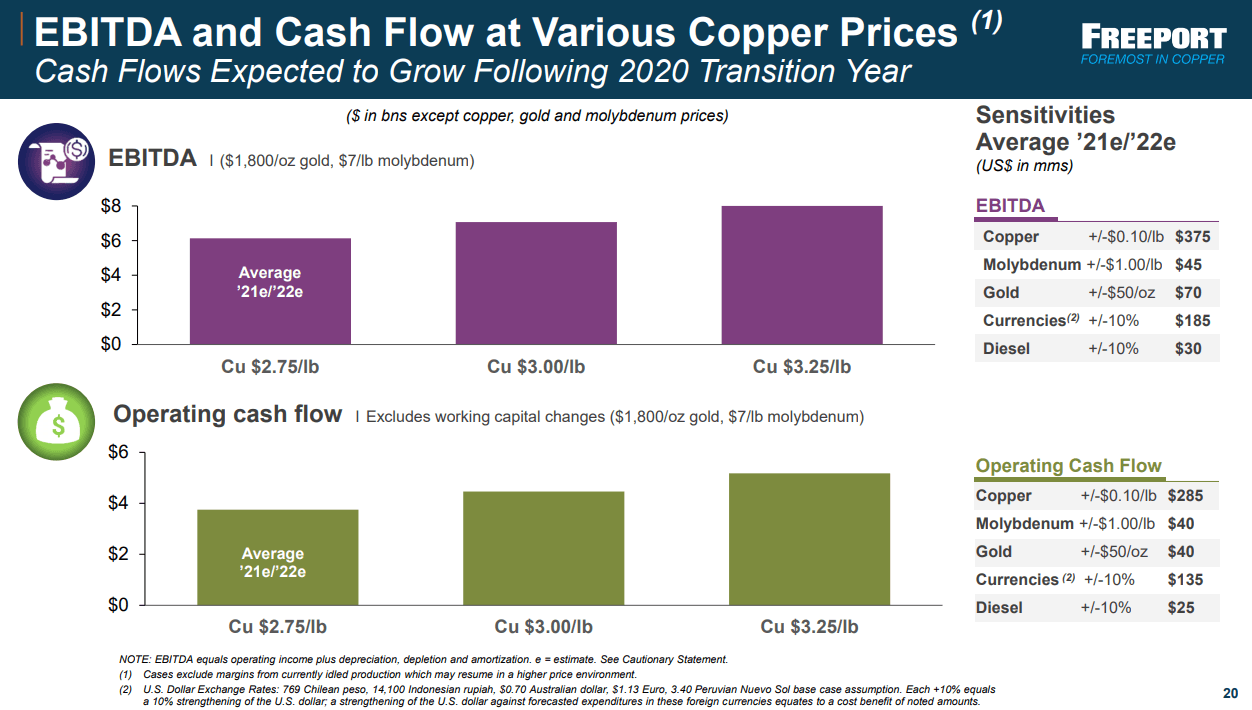

FCX free cash flow valuation

With copper at $2.85 and gold at $1.500, FCX should make operating cash flows of $2.4 billion in 2020.

With capital expenditures at $2.4 billion, FCX should not be free cash flow positive in 2020. However, the management’s expectation is to turn free cash flow positive in 2H 2020 and stay positive and increase free cashflows over 2021 and beyond. They are doing well on that front with Q3 2020 delivering good cash flows.

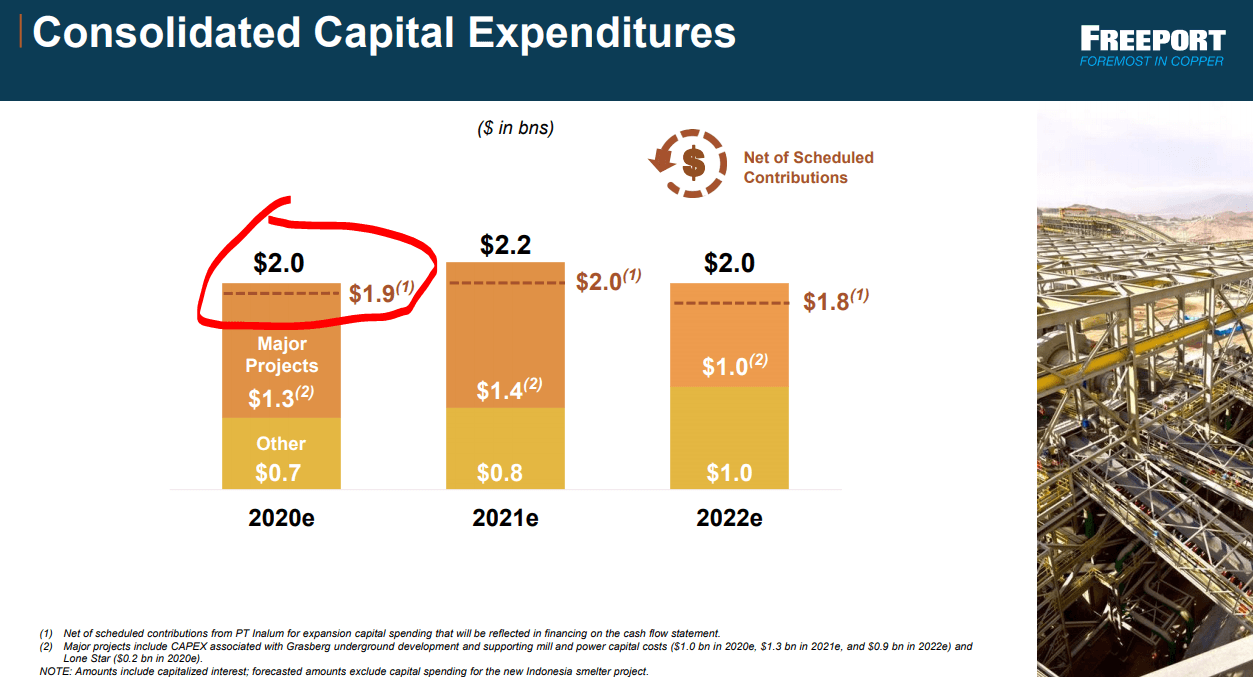

The capex to be deducted from operating cash flows is expected to be around $2 billion per year going forward.

FCX is about what will happen next, beyond 2020.

FCX future cash flow outlook

Production is expected to grow but we have to account for the 50% at Grasberg and 28% Morenci not owned stakes. Grasberg should produce 0.7MT of copper per year at no cost given the gold by product.

From the above, we have to deduct 50% of production for Grasberg, that after the ramp up should be a total production of 1.6 million pounds of copper and 1. 7 million ounces of gold at a very low cost thanks to gold benefits, actually the copper production cost is zero. Grasberg’s benefit to FCX will be 0.7 million pounds of copper at a cost of $0. Full ramp up is expected in 2023 when the economic interest will be 48%. Thus, operating cash flows should be $4.9 billion. $2.5 billion for FCX from Grasberg – before taxes, royalties and who knows what surprises from Indonesia.

All in all, the estimate should be that FCX will produce 3.5 billion pounds of copper over the long-term. The Grasberg benefit up to 2022 will likely be used for building the smelter that is a requirement from the Indonesian government.

FCX full production – Source: FCX investor presentation

As the cash costs are projected to be below $1.2, FCX should see good profitability over the long term.

Let’s say FCX’s attributable production is 3 billion pounds of copper with costs around $1.2 accounting for other interests in Grasberg and Morenci.

That should lead to operating cash flows of $5 billion per year. To be conservative I’ll take $4 billion because with mining, there will always be something going on. Plus, you have taxes, royalties, interest payments etc. to account for. Debt is at $10 billion with approximate interest rates of 5% – thus $500 million to be deducted.

The capital expenses are expected to be at $2 billion which should leat to free cash flows of around $2 billion per year. In line with the projection below and the growth estimations.

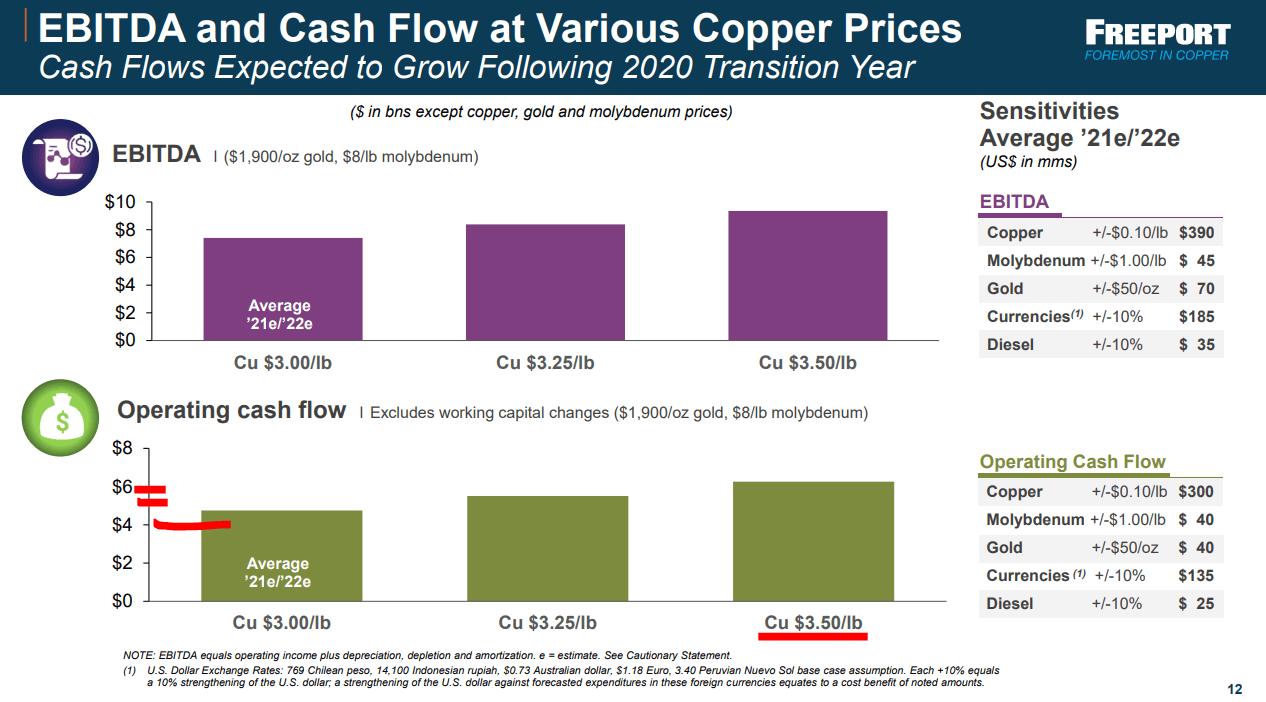

In the last presentation, FCX quickly amended the above slide by adding $1 billion to operating cash flows given the higher copper and gold prices compared to the previous quarter presentation..

FCX Stock Investment conclusion

Given the quality of the assets, the $2 billion in cash flows give a good yield of 8% on the current market cap of $25 billion. Plus, there is all the growth potential but for that you need higher copper prices.

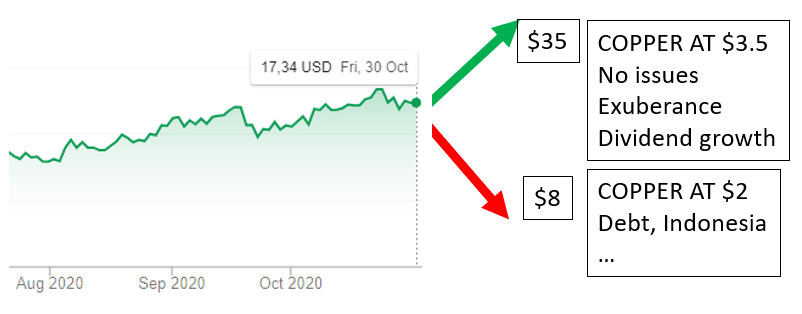

If copper prices go and stay above $3.5 for longer, I think they could double cash flows and bring them to $4 billion. Alongside the likely exuberance in the market, I would assume FCX to reach market cap of $50 billion. So, the upside is 100% from here while if we have another crisis where people start thinking copper will stay at $2 to $2.5, cash flows might be around $1 billion or lower and you can soon see a market cap below $10 billion with the downside being 50%.

The above volatility is something you must take into account when investing in copper mining stocks. There are two ways to approach this:

- Having a portfolio exposure strategy

- Being patient by waiting for the fat pitch

FCX stock as part of portfolio strategy

Given the positive long-term trends for copper, you could set a fixed portfolio exposure to copper that makes you sleep well. As copper stocks will certainly be volatile, every time the portfolio exposure increases by 50%, you can sell the gains and bring down the exposure to the initial level.

If stocks fall 33%, you can buy more and bring the exposure back up again. Given the environment, you will surely be buying low and selling high which is usually a very good tactic when it comes to investing. Also, by focusing on portfolio exposure, you’ll surely avoid the dangerous exuberant situations and force yourself to buy when things look really ugly, which are usually the best time to buy copper stocks.

Waiting for the fat pitch

My personal strategy is to wait for copper mining stocks to reach a level where the long-term downside risk is minimal and the upside maximal. The current downside for FCX is 50% or more and the unlikely upside is 100% in case of a rally in copper prices.

I think that with copper at $2.5, some delays with Grasberg ramping up, FCX could easily fall 50%, which would create a situation where the long-term downside could be practically zero while the long-term upside could be minimally 100%. If you like such a strategy, please consider following.

If you enjoyed this analysis and would like to have me follow the copper environment for you and notify you when the time for the fat pitch will come, please check my Stock Market Research Platform where the focus is exactly on that.

If you wish to learn more about what I do and get an email when I publish a new interesting stock or sector analysis, please subscribe to my newsletter.