KSU Stock Offers Multiple Upside Opportunities (Takeover Candidate)

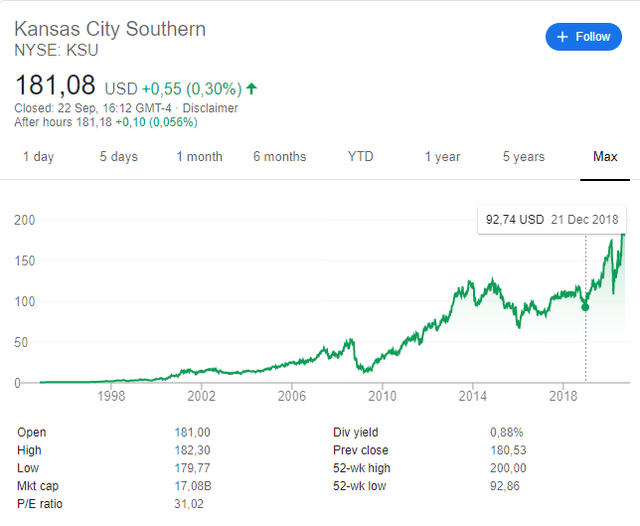

KSU stock price analysis

Kansas City Southern stock (NYSE: KSU) is in a very interesting situation. Reportedly, the management has rejected a $20 billion, $208 stock price, takeover bid from Blackstone Group and Global Infrastructure Partners. KSU stock is currently trading at $181 and the offer would represent a significant premium, especially on historical prices.

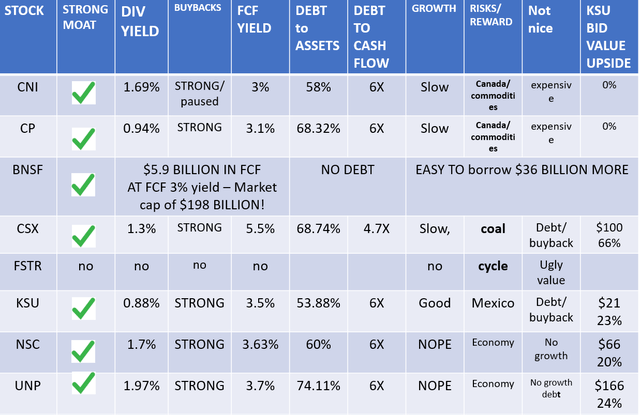

The takeover bid is an excellent example of how to value railroads. Price earnings ratios of 31 and dividend yields of 0.88% might seem expensive, but in a financial environment where investment firms can get money almost for free, borrowing at 1% and investing in something that makes 3% while offering growth opportunities ahead, is still an amazing deal. At the end of the article there is a railroad stocks comparative table giving valuation estimates based on the KSU takeover bid.

The KSU situation also indicates what could be a valuation for other good railroads. But we must not forget about the risks. If the current liquidity in the market dries up valuations might quickly change and KSU stock could quickly fall below $100 where it was trading prior to 2019. This is unlikely as all central banks will do ‘whatever it takes’ to help the economy, consumption and employment by flushing the markets with liquidity, but it is good to keep in mind and consider when comparing to other investment options.

KSU stock analysis content:

- Business overview

- KSU stock fundamentals

- KSU dividend and buybacks

- KSU stock investment thesis and comparison

This KSU stock analysis is part of my full railroad stocks sector analysis. Here is the:

If you prefer enjoying a coffee and listening to the content, here is the video on rail stocks, article continues below.

Kansas City Southern business overview

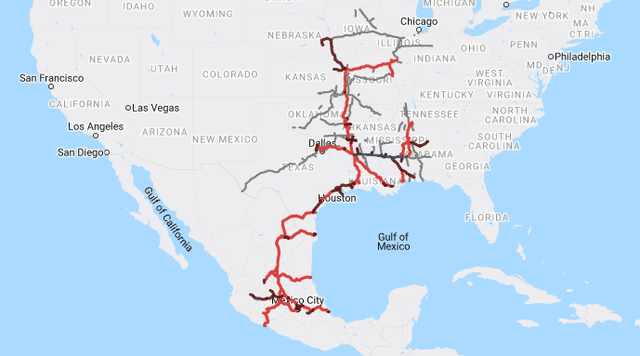

Kansas City Southern, as the name says, connects the U.S. with Mexico.

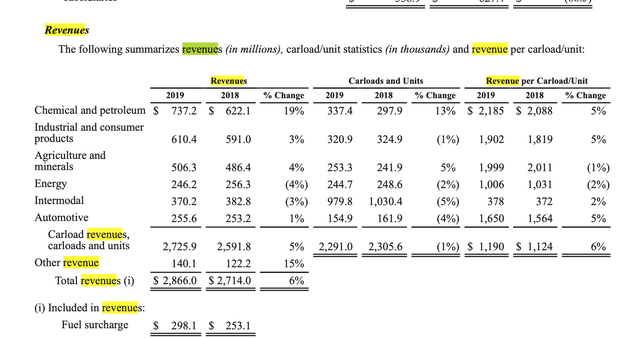

KSU’s revenue is diversified but still mostly depending on chemical products and petroleum. Given its geographical position, that is logical.

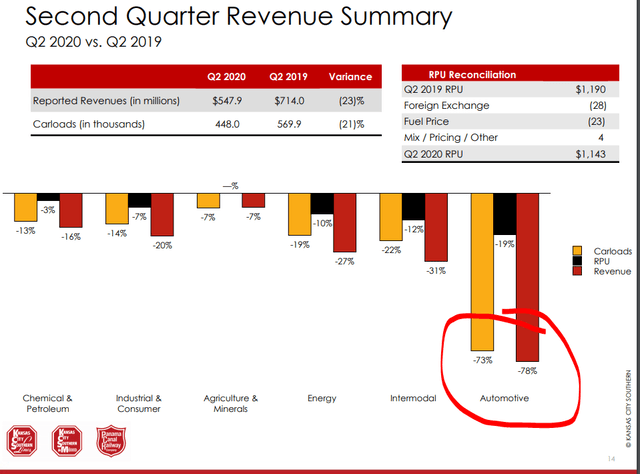

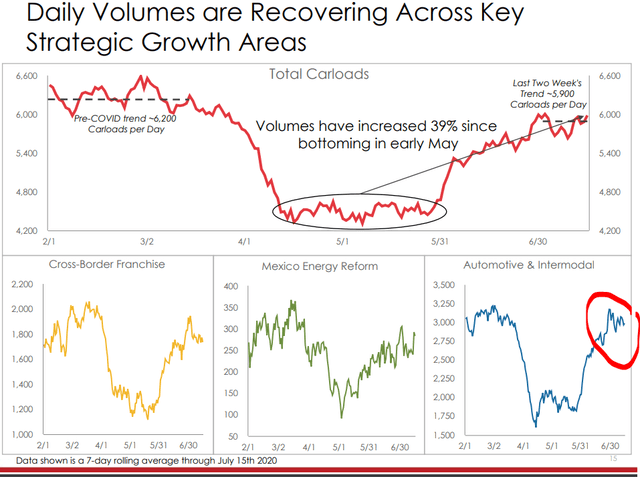

Surprisingly, the automotive sector was the biggest detractor to Q2 2020 revenues and not oil, despite the lower prices.

Given the outlook for oil in the U.S., it is a sector to watch carefully over the coming years while I would argue that automotive will rebound as it is already the case.

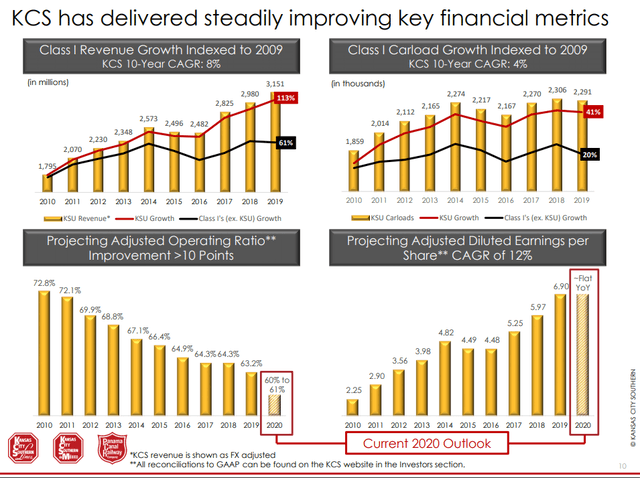

Despite the oil risk, it is likely KSU will keep growing based on emerging market growth as it might even benefit from the China related trade wars. Over the past years, KSU has seen twice the revenue growth compared to the average class 1 railroad. Therefore, I don’t think growth will stop, it might just be a little slower for a while.

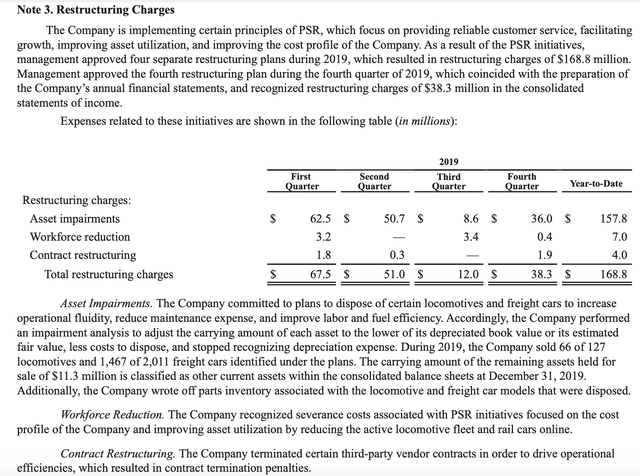

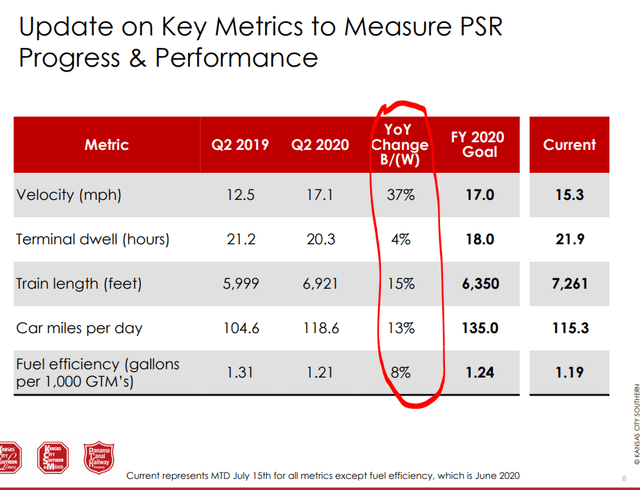

Operating metrics have been continuously improving and will continue to improve as the company decided to implement precision scheduled railroading. This required $168 million in upfront restructuring costs but is already showing positive effects.

Improvements on all key operating metrics:

From a business perspective, KSU depends on trade activity with Mexico and the oil sector. Given the likely economic growth and development in Mexico, we could assume KSU offers the highest growth potential among the railroads but also possibly the highest volatility given that emerging market economies suffer more during downturns.

KSU stock analysis – fundamentals

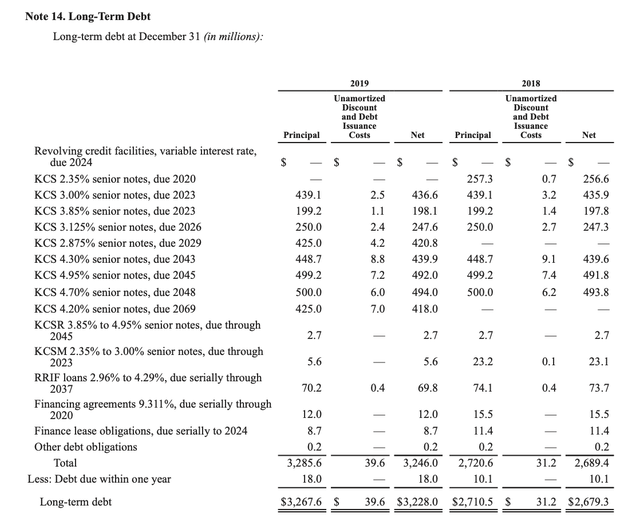

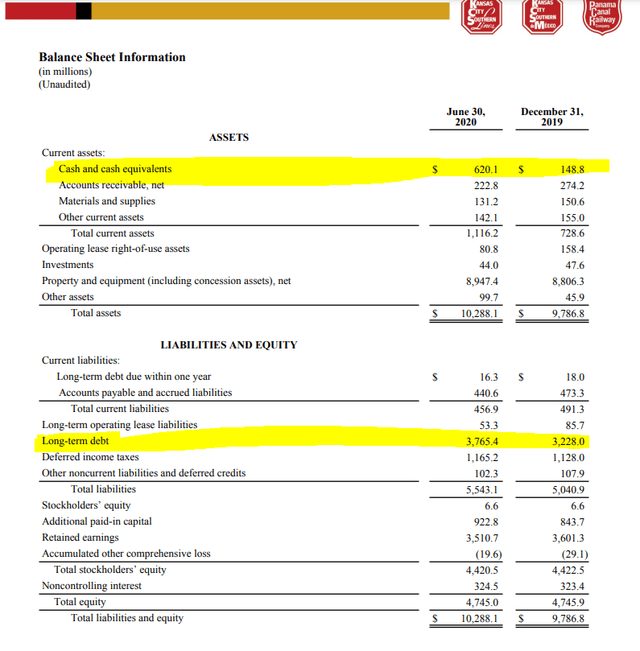

KSU’s debt level was at $3.26 billion at the end of 2019 with interest rates between 3% for the shorter notes up to 4.2% for the notes due in 2069. There is one financial agreement with a 9.31% rate, they used to buy rail cars with, that fortunately expires in 2020.

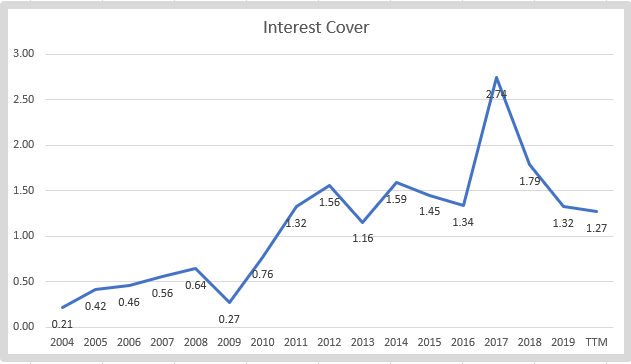

Interest cover is on the lower end when compared to other railroads.

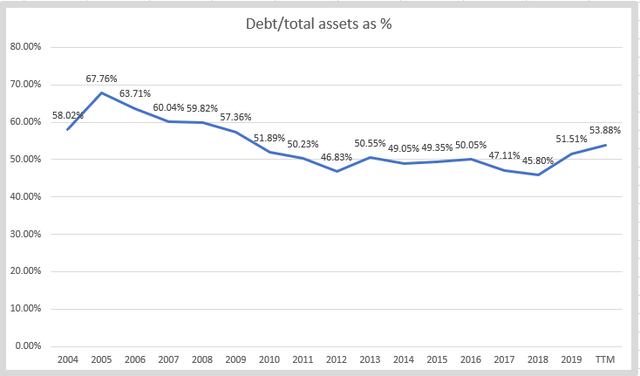

But the debt to assets ratio is on the better side. It had been decreasing up to 2018 when the latest surge in investing and capital spending started.

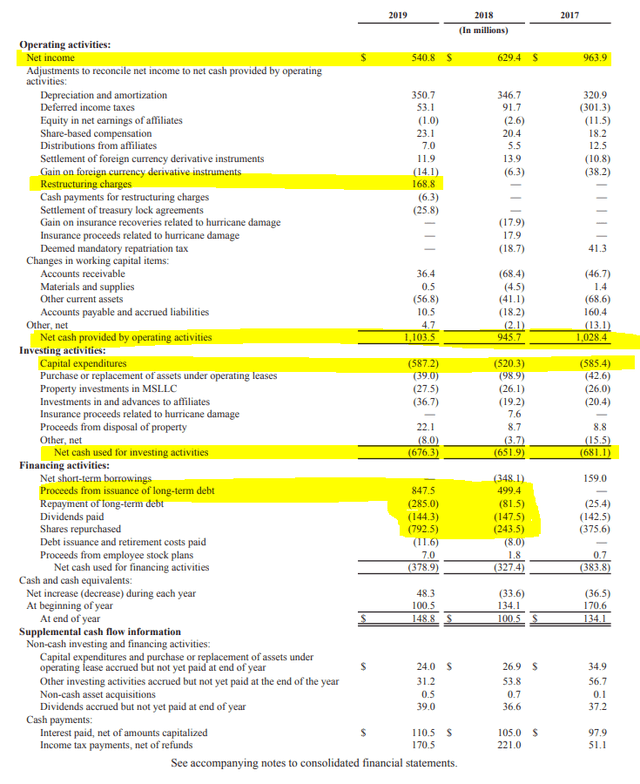

The best way to value a railroad is to look at cash flows. KSU’s operating cash flows have been around $1 billion over the last 3 years while the capital investments were constantly at around $600 million which leaves $400 million in free cash flow.

However, as they won’t spend on new locomotives anymore and the restructuring program is already showing its benefits, we could assume capex to be close to $400 million going forward. This will allow for stable dividends and more buybacks.

Looking forward, with PSR improvements and business as usual, KSU should be able to achieve free cash flows of around $600 million. That would give it a 3.5% cash flow yield.

KSU dividend and buybacks

KSU’s dividend is stable with the company spending approximately $140 million per year for it. It is likely the dividend will grow as the company focuses on buybacks and lowers the number of shares outstanding.

As we have seen above in the cash flow statement, the company spent $792 million on buybacks in 2019 and took on debt to do it. In the first months of 2020 they spent $294 million on buybacks while further increasing their total debt by $500 million to $5.5 billion.

They have also increased their cash position to take advantage of the low interest rates out there and it is likely they will use that cash to push the stock price even higher with more buybacks.

All of this creates a very interesting investment thesis that reminds a bit of Restoration Hardware where the focus of the management was to push the stock as higher as possible – it worked perfectly.

KSU stock investment thesis

Compared to other railroads KSU is nothing special except for the possible higher growth outlook.

But we know there is a takeover bid which the management rejected while they are pushing hard on buybacks and taking more debt to do more buybacks. I think they are trying to make as much money as possible for themselves as for a buyer the stock price isn’t relevant, but the stock price is extremely relevant for the owner of the stock, i.e. the management and other stock owners. Let me explain.

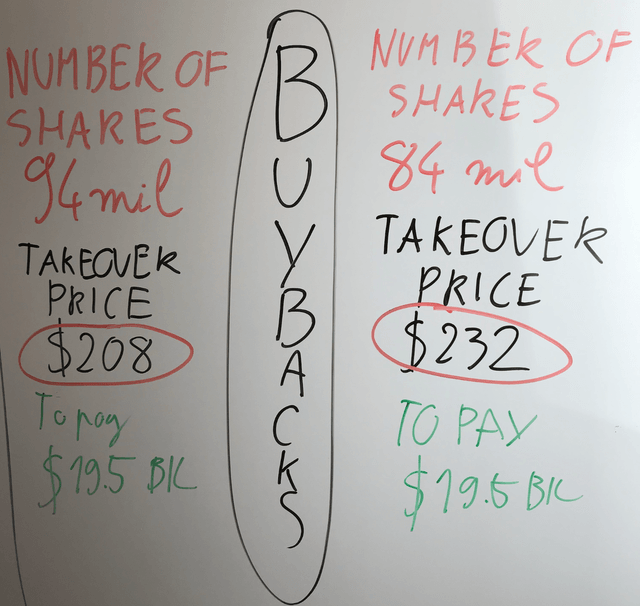

If they manage to lower the number of outstanding shares by another 10 million for what they would need $1.8 billion at current stock prices which can be done with just 3 years of cash flows, the stock price could be $232 and not $208 at the same price for the acquiring company. Actually, with a bit more debt, they could do it in an even shorter time span.

Therefore, the management’s intention is to push the stock higher no matter what because it is in their interest to get as much money as possible as a shareholder. That could be why they rejected the bid, they might not be able to get more in general terms, but they might be able to get more in the form of a higher stock price for them and also for other shareholders. Nothing wrong with such a strategy.

Thus, it is likely the stock price will continue to go up as they keep on pushing it higher through buybacks. When the takeover happens, shareholders and management will be rewarded. In the mean-time, we have a floor for the company value of $20 billion, possibly negotiable a bit higher even if then we are at really low free cash flow yields.

KSU stock compared to other railroad stocks

What differentiates KSU from others is the attractiveness for a takeover. It is unlikely anybody could find $100 billion to take over a company like CSX but $21 billion to take over KSU is manageable.

Other metrics are in line with the sector average plus they have the Mexico growth card. I would say that KSU stock will follow the market in a downward trend but outperform the market in an upward trend due to the buybacks and the takeover bid situation.

With a bit more of buybacks and a better takeover bid, they could engineer a takeover price of $250 over the next 12 to 24 months. That would represent a 38% upside which is not bad.

For more information on other railways stocks, please check my comparative railway stocks article with links to other detailed railroad stock analyses such as this one.

If you like this comprehensive approach to investing, please subscribe to my newsletter to be notified when I analyse a new sector. To check my past analyses, covered stocks and portfolios, feel free to check my Stock Market Research Platform.