Baidu Stock Analysis – Margin Call Crash Creates Opportunity

Here is my Baidu stock analysis video, the Baidu stock analysis full research report continues below the video.

Baidu stock analysis summary

- 72% stable search market share in China where competitors didn’t really manage to develop a similar business – the longer you have such a position, the stronger your moat is.

- Stock recently crashed due to technical reasons with a $20 billion margin call on a hedge fund. Non fundamental volatility often creates investment opportunities.

- Many unpriced opportunities in the form of autonomous driving, smart transportation, Robotaxies, cloud, iQIYI and the recent acquisition of YY live.

- Many value investing asset managers from Asia have price targets of $350.

- The risks are the too; most businesses are growing but far from profitable, short-sellers like some parts of Baidu and after all it is always China.

Baidu stock analysis – BIDU stock price overview

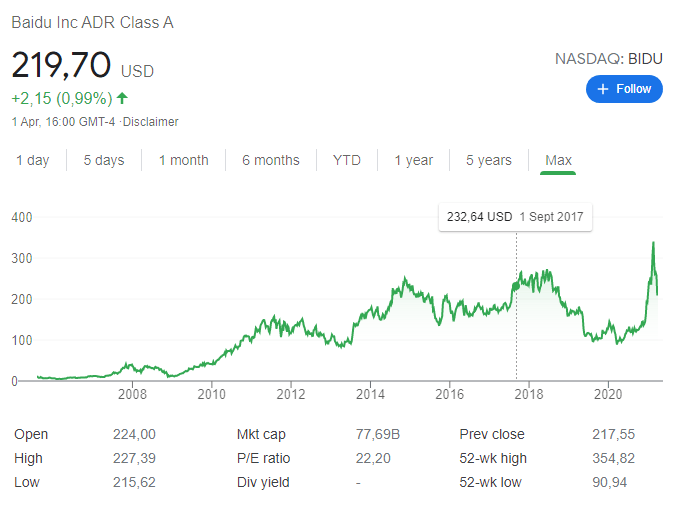

Baidu stock or NASDAQ: BIDU stock did really well since its listing on the NASDAQ in 2005. The stock is almost a 30-bagger in Lynch lingo.

But, as it is usually the case with such growth tech stocks, BIDU stock has also been very volatile. You see the stock peaking in 2007, 2011, 2015, 2020 and recently, February 2021, only to crash after and stay down for a few years.

Baidu is a perfect example of how a stock can be exuberantly pumped up, then forgotten, but where the business actually does well and constantly improves by solving temporary issues. As you will see in the analysis, the current stock price reflects some exuberance about Robotaxies, AI, Cloud and autonomous driving and if the fundamentals don’t reflect the estimations soon, it could reflect in years of bad stock performance ahead. BIDU stock is currently ‘cool’ and it also holds the 3rd position in Cathie Wood’s ARKQ ETF Autonomous Technology & Robotics ETF.

Over the last 5 years, we have seen it crash 66% from 2018 to March of 2020 as the business stagnated, then rebound, only to fall down again 35% from its 2021 February 19 peak of $354.82.

In addition to the crash since February, BIDU stock was severely hit recently with a 25% technical margin call drop due to a $20 billion margin call by several banks on Bill Hwang Achegos Capital Management that led to the liquidation of several blocks of BIDU, Tencent, Vipshop, Farfetch, iQIYI, ViacomCBS, Discovery and GSX Techedu. The margin call led likely to other liquidations which is the reason for the sudden 25% drop.

Apart from creating an opportunity, BIDU’s stock price action also indicates what is often the likely result of momentum trades that are fueled by margin debt as BIDU’s stock price had been propelled up in Q4 2020 and early 2021, before the change in momentum towards tech stocks lately. Nevertheless, it all creates volatility, and volatility is one of a value investor’s best friends.

High volatility is always interesting because if you look at the fundamentals of a business, you can take advantage of the market’s irrationality and stock price swings. Let’s dig deep into Baidu, create an earnings model, make a sum of parts valuation, compare to western investment options and see what is BIDU’s stock investment risk and reward.

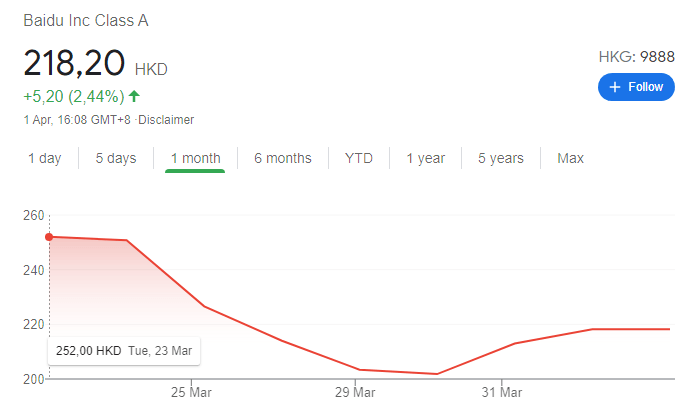

The company has recently listed its stock in HK, likely to hedge any possible issues with what is going on regarding Chinese stocks listed in the US and the negative political environment there. Baidu stock ticker in HK is 9888.

50% of the listing proceeds will be used for further AI R&D while 40% will be used for the development of the Baidu mobile ecosystem. The remaining 10% for corporate purposes.

The stock has been offered at 295 HK and the current stock price is already lower.

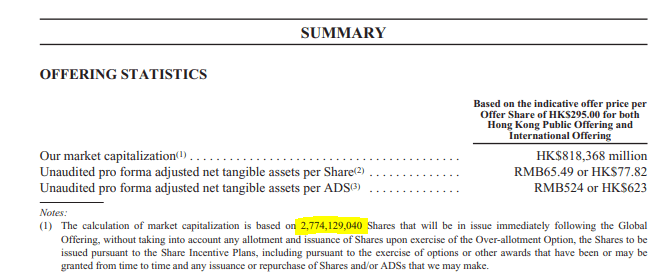

The market capitalization based on the above price and the 2,774,129,040 shares issued is 605 billion HKD or $77.8 billion USD at the time of writing (4th of April 2021).

1 NASDAQ BIDU ADR represents 8 regular stocks.

International investors with access to HK might consider the alternative listing to avoid any US regulatory issues and liquidity constrains. However, lot size is 50 shares for HK, but please recheck investing opportunities with your broker.

It is important to mention that Baidu first repurchased stocks for $4.5 billion at a lower price than the one they issued stocks for the listing in HK. So, they didn’t dilute shareholders and actually created value by buying low and selling high. On the other had share based compensation is significant.

Baidu also has a 56.5% stake in iQIYI (Nasdaq: IQ), a leading Chinese video platform that I will analyse too as the stock price movement looks intriguing.

Baidu stock analysis – Business overview

Most of the content used for this Baidu business overview has been derived from Baidu’s recent HK listing prospectus. A listing prospectus is usually a great document to use to get the best insights into the details of a business.

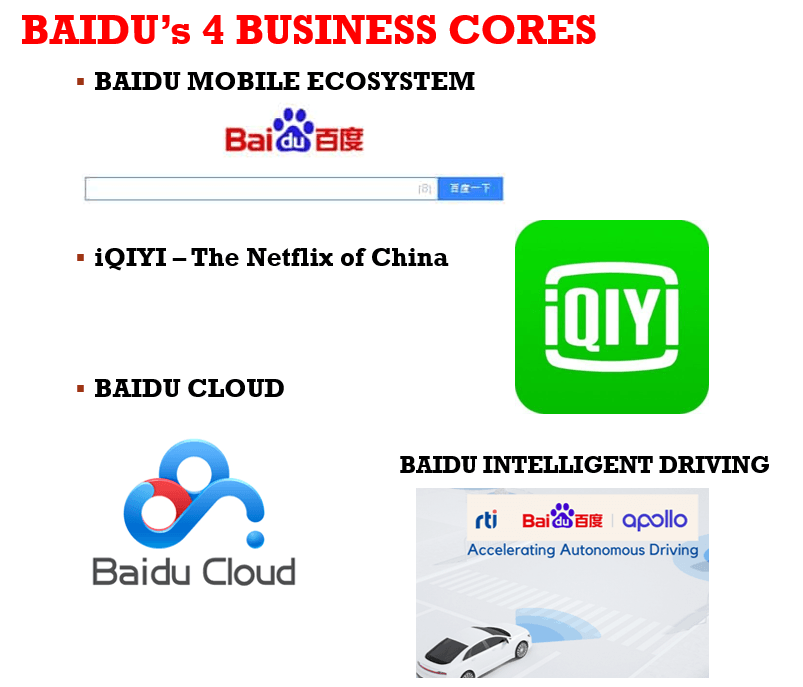

Baidu presents itself as a leading AI company but its core foundation is still the search engine business in China that has been developing into the Baidu App as mobile search traffic sees better monetization with higher average revenues per user due to better targeting. 70% of revenues comes from the Baidu Core business segment and the rest is from iQIYI. Additional businesses are cloud services and intelligent mobility under the Baidu Core segment.

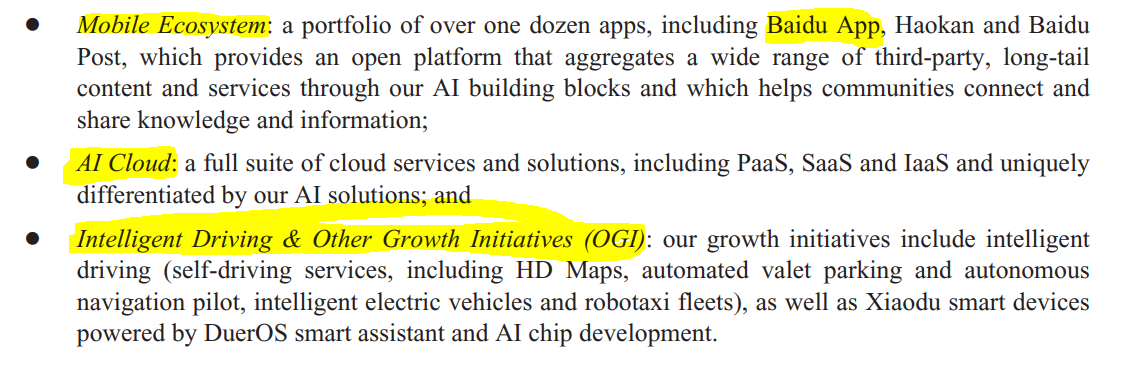

Baidu’s Core search business includes the following segments:

BIDU stock analysis – Baidu Core business segments

In November 2020, Baidu entered into definitive agreements with JOYY Inc. to acquire its domestic live streaming business in China, which includes YY mobile app, YY.com website and PC YY, among others. So, there will be another segment to add to Baidu and it is perhaps following what Google did with YouTube but YY Live is more about scantily clad girls than a real video search engine. However, perhaps they can build on that.

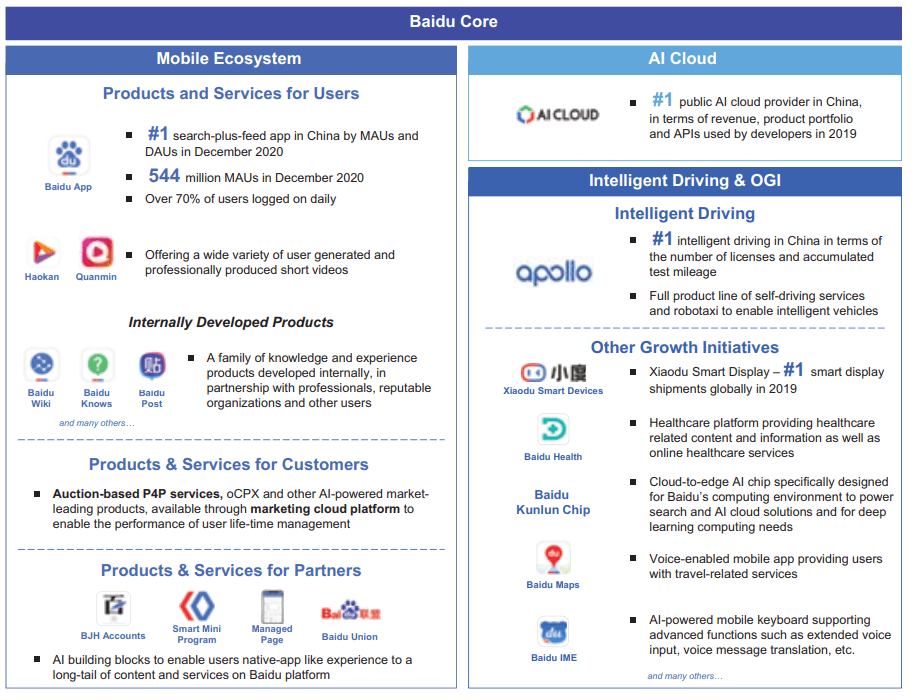

The following chart shows more in detail Baidu’s Core business segment; the mobile ecosystem including the Baidu App, Baidu Cloud and Intelligent Driving.

Baidu Core search business – Mobile Ecosystem

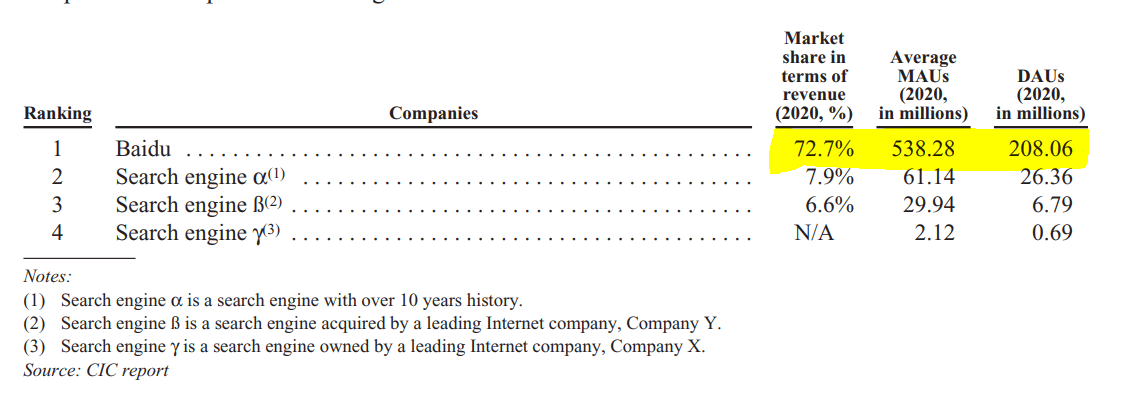

Baidu has a stable search market position of around 72% with 538 million monthly users and 208 million average daily users. Their search market share has been stable as competitors didn’t really manage to develop a similar search business even if they tried – the longer you have such a position, the stronger your moat as simply others can’t easily get all the data Baidu can for search. The main issue for Baidu is to monetize the search traffic and create an ecosystem around the search engine and not having it as an isolated app in the Chinese digital environment.

The key for Baidu is to create an ecosystem around the traffic it gets on search and that is not that easy but the company is investing heavily and it might create interesting things down the road. The ecosystem is supposed to be built around search, AI, autonomous drive and other growth options.

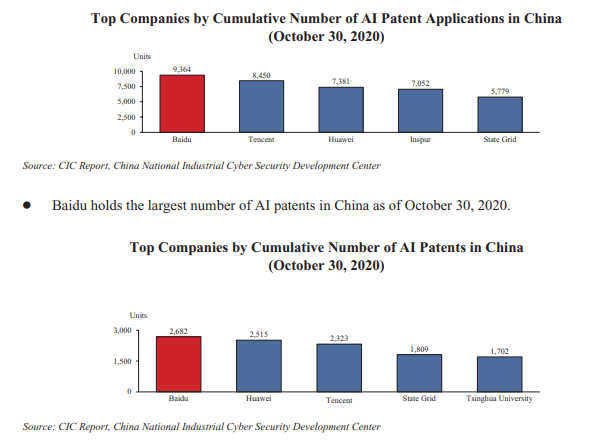

BIDU is also investing heavily into AI and positioning itself among the top, if not the top, AI company in China.

Baidu spends 21% of its revenue on R&D compared to 8.5% for Alibaba and 8.1% for Tencent.

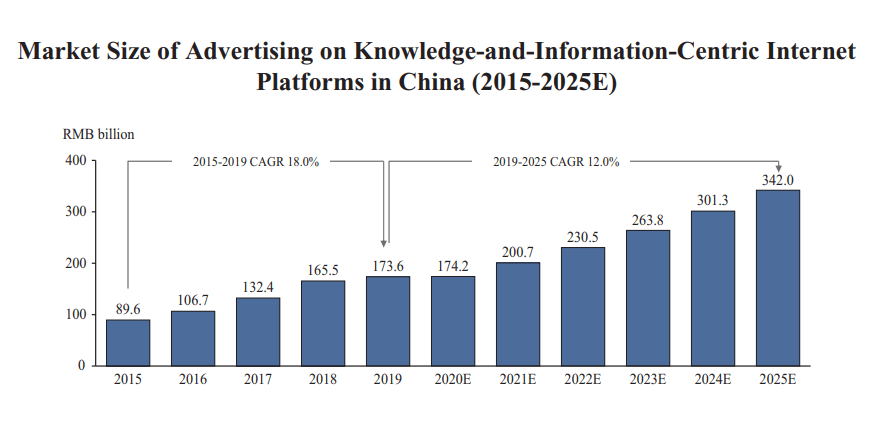

The sector has strong tailwinds as AI and scale enable the key players to create a moat and also as the internal development of the Chinese economy creates much more traffic.

The market related to software sales is expected to increase 7-fold by 2025 in China.

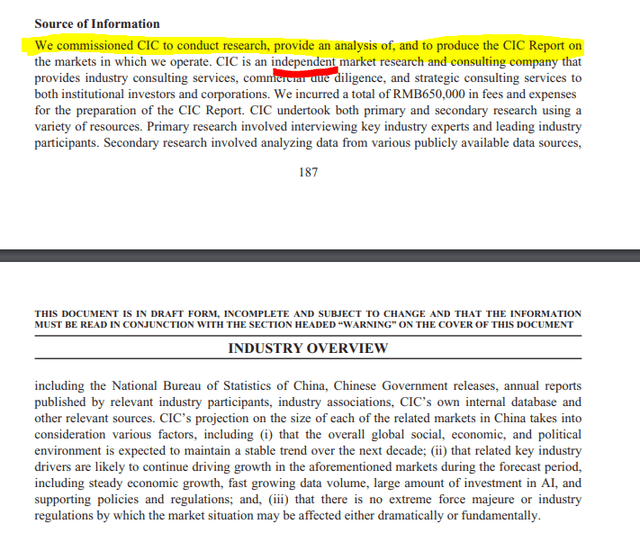

It is important to note that the above CIC report, supposed to be independent market research, which is the source of the data shown by Baidu has actually been commissioned by Baidu itself.

CIC report commissioning – Source: Baidu Listing Prospectus

Thus the CIC data shared in the HK listing prospectus has to be taken with a grain of salt. If you are paid by someone to make research, it is not surprising that the CIC report makes Baidu’s opportunity look good..

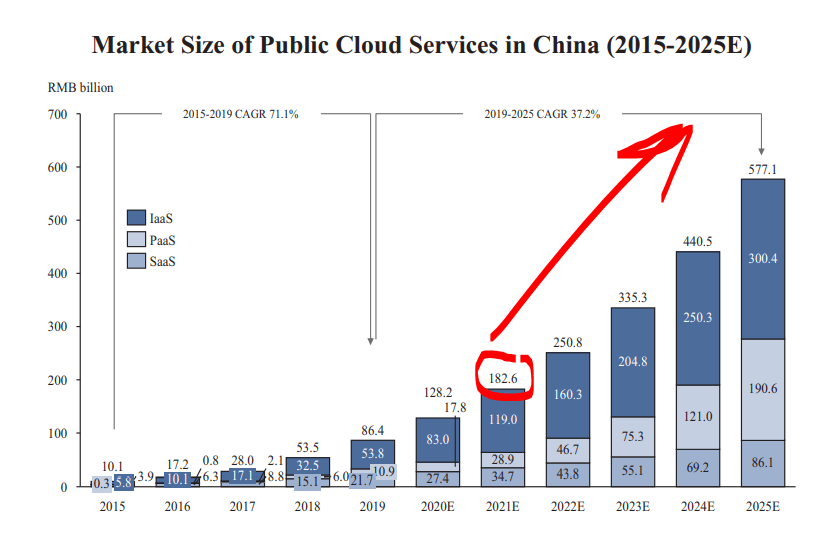

Baidu Cloud Services business

Apart from the search related business, Baidu is developing its Cloud related business too. The cloud services business is expected to grow at 37.2% in China over the next years.

I’ll be discussing the specific segment financials in the financial segment but Baidu’s cloud business has grown 44% in 2020 and if it just continues to match the market’s growth, it certainly deserves a market valuation which is often around 10 times sales.

Baidu Intelligent Driving business

The market for intelligent driving services is also expected to boom in China.

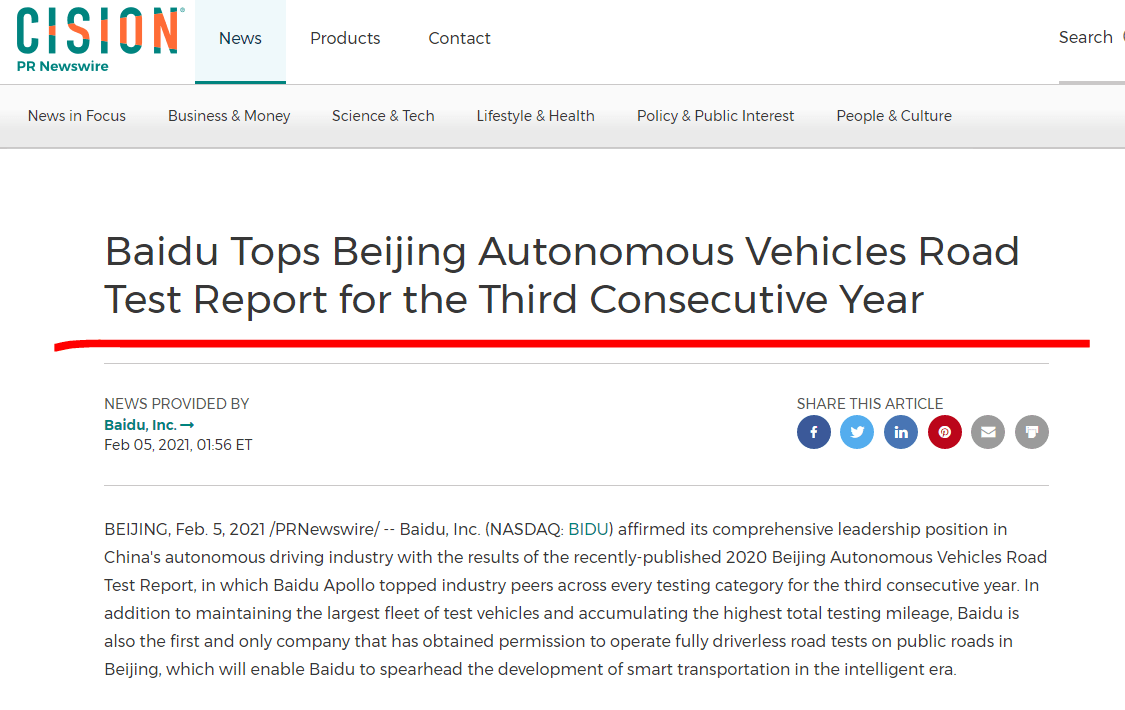

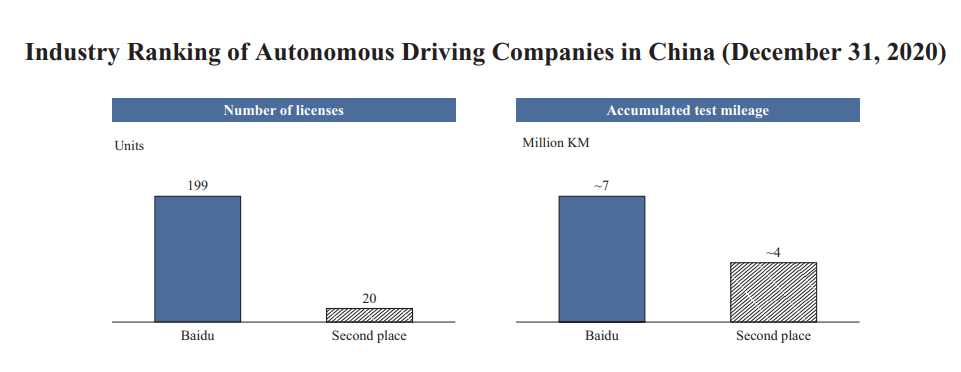

Baidu is the current leader in licences in China and autonomous driving in China. In the 2020 Beijing Autonomous Vehicles Road Test Report, that unfortunately doesn’t include Tesla, Baidu’s Apollo won for the last 3 years.

Baidu has the most licenses and test mileage.

Alongside autonomous driving, the electric vehicle market is also expected to triple over the coming years.

Baidu has entered into a strategic partnership with multinational auto manufacturer Zhejiang Geely Holding Group (Geely) to produce intelligent EVs (owning Volvo too). No plans have been shared but it is expected that it will take approximately 3 years from design to market.

Baidu has the Apollo Robotaxi initiative with 3Apollo Go Robotaxi test pilot programs in operations, in cooperation with Beijing, Changsha and Cangzhou. Apollo is the market leader in China with 4.3 million accumulated test miles and 199 autonomous driving licenses across China. Baidu has spent 11.8 billion RMB on development for Apollo in the first 9 months of 2020 while competitors like NIO (NIO stock analysis) and Li Auto have spent 1.7 billion and 0.7 billion respectively.

Baidu’s plan is to be the first multi modal autonomous driving system.

Autonomous drive, AI related software and Robotaxies alongside other smart transportation might be a big contributor to revenues down the road. When? We can’t know yet, but it is the future and Baidu is positioning itself to be a very significant player in China and likely elsewhere too.

As it is not yet profitable, as a value investor you want to get it for free, something we’ll discuss more in the earnings valuation model and sum of parts valuation. However, as discussed in Peter Lynch’s One Up On Wall Street, perhaps the best way to get exposure to a future trend is to buy a business that has the promising opportunity as a side project and not its core business.

Baidu other growth opportunities

Other business segments that Baidu focuses on are AI chips, healthcare and other growth opportunities. The company constantly invests in stakes in smaller companies and small opportunities. In the tech world, you never know what can come out of that. For now, Baidu’s balance sheet investments amount to a significant 75 billion RMB.

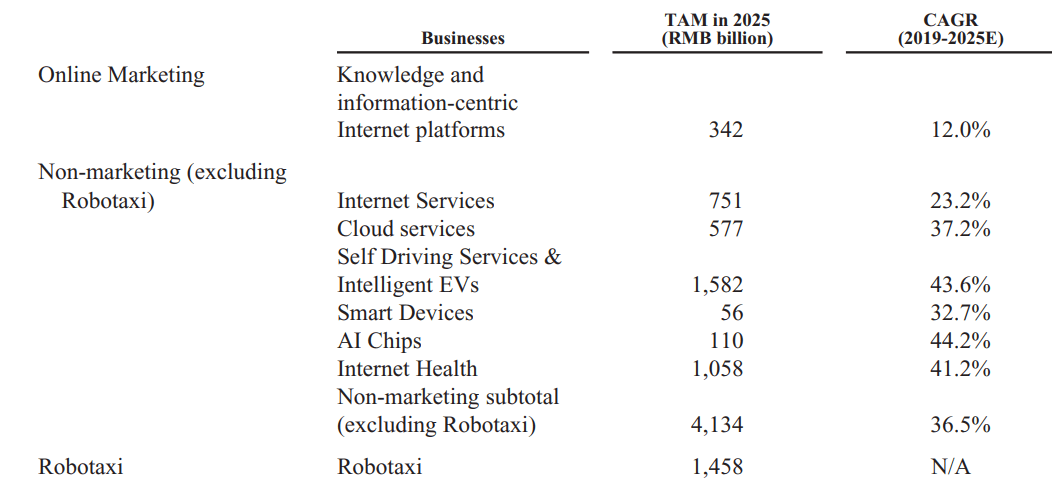

Perhaps the most important table related to Baidu’s other business opportunities in the Chinese market is the total addressable market analysis made by CIC. The search business market will likely grow by 12% which is something already remarkable, but Baidu’s core business is expected to be surpassed both in size and growth rates by internet services, cloud services, autonomous driving & intelligent EVs, internet health and Robotaxis.

With a total addressable market of 5.5 trillion RMB, if they can get just 10% of that by 2025, it would represent 5 times current revenues. If the above actually happens only in 2030, that would still good if they get significant market share and possibly healthy margins as Baidu is positioning itself more as a service or platform rather than manufacturer.

For now, 86% of Baidu’s revenues are still derived from advertising while just 14% from the other segments mentioned above. If Baidu can scale its reach of 1 billion monthly average devices using Baidu services and 584 million Baidu app members on the other business segments, the investment should be an interesting one. Cross-selling opportunities should be significant on the 316 million average monthly Baidu Maps users with autonomous driving etc.

Given the above, and how China is strongly developing its internal business, BIDU might be a great opportunity to diversify into China (as Bridgewater suggests to do now) and the growth in the above markets banking on the growth of the Chinese internal economy.

Baidu’s business is certainly interesting, but let’s see the financial side of it and then make a valuation.

Baidu stock analysis – financials

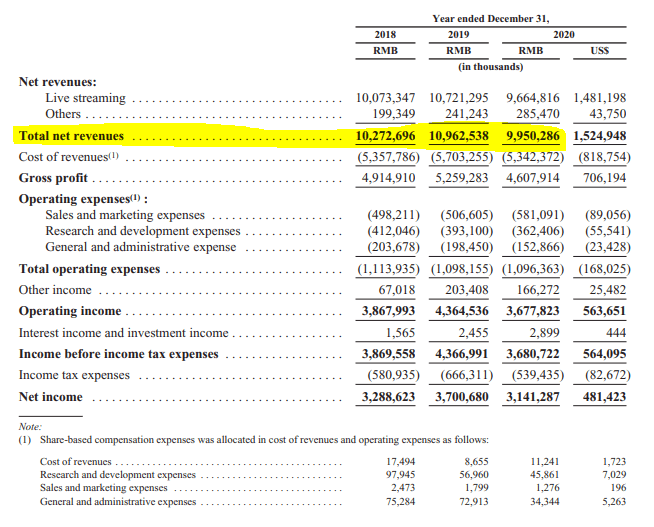

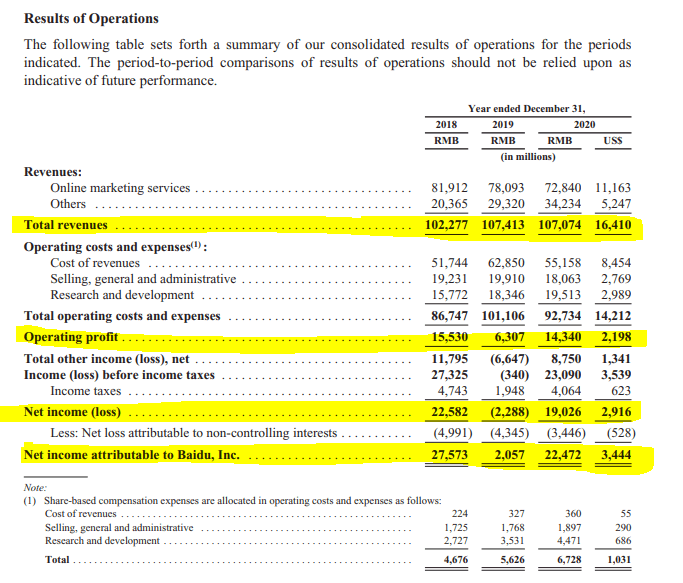

Over the last years, the key thing pressuring BIDU’s stock price was the lack of revenue growth in the Core business segment.

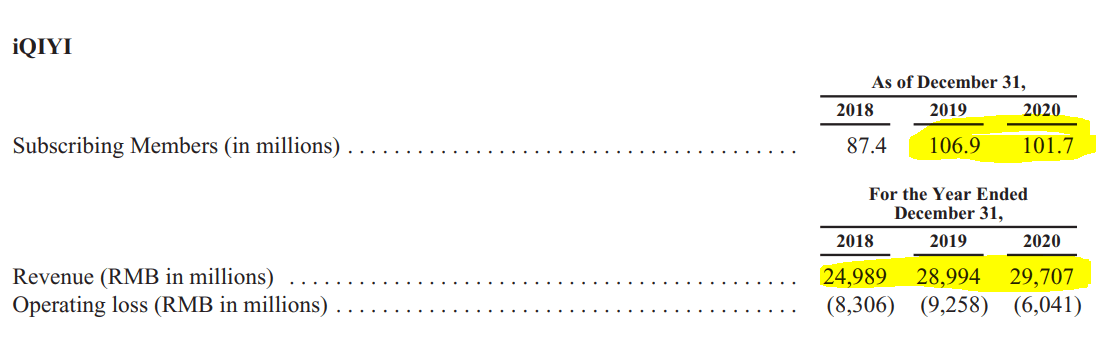

iQIYI has been stagnating too, also seeing a decline in the number of average users while producing losses year over year.

The recent acquisition, YY Live, has not see much growth either.

But, investing is about what will happen in the future compared to the current price.

Despite being hit by COVID-19, Baidu still managed to reach net income of 22.4 billion RMB or $3.4 billion.

From a segment perspective, Cloud has grown 44% year over year and iQIYI membership services 14%. The rest has been stagnating or declining like iQIYI’s advertising revenue. But if you grow membership revenues, it is logical advertising revenues decline.

As Covid restrictions pass, we might see a 10% bounce back for online marketing revenue when travelling and all other sectors strongly related to internet advertising bounce back. If Baidu can grow alongside the expected 12% growth in online advertising, that would be very significant for the company.

Cloud revenues reached 9.1 billion RMB on 44% growth. This is important because we will use it in the sum of parts valuation.

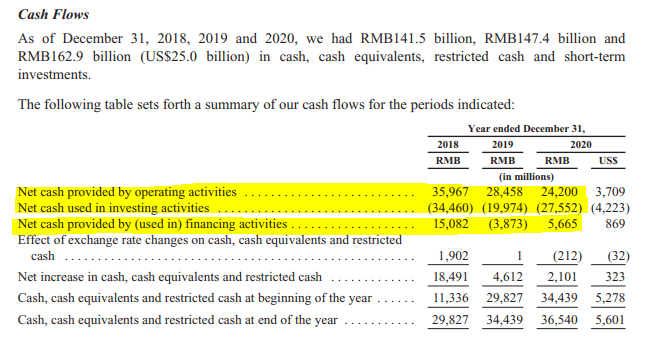

Apart from business cash flows and growth opportunities, Baidu has a strong cash position, extremely significant compared to the $77.8 billion market capitalization.

They have almost a third of the market cap in cash. Net, net cash would be 44 billion RMB or $6.75 billion which is still almost 10% of the market capitalization. If we would just look at available cash compared to long-term liabilities, the net cash position is actually $12 billion.

From a cash flow perspective, the business as is, is operating well. Operating cash flows have been 24 billion RMB or $3.7 billion in 2020.

When looking for free cash flows, we must differentiate between cash flow business expenses and financial investments.

From a balance sheet perspective, it looks like the company could survive also without the cash, so we can only hope the cash gets invested well or fairly distributed to shareholders. Something to watch carefully over time.

Something to watch carefully over time.

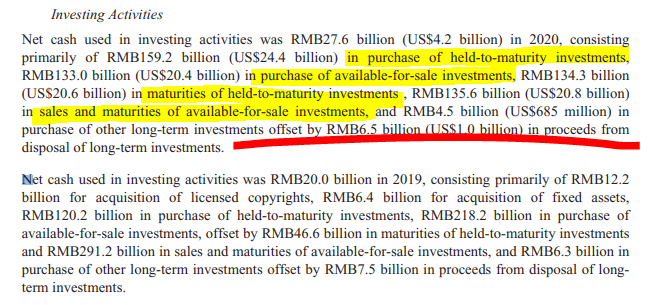

A significant account above is long-term investments of 76 billion RMB. That includes the following:

Of the above 76 billion RMB, 24 billion RMB is not based on fair value measurement, so that is something that we will have to see how it will develop in the future.

Just an example of the investments is the 12% equity interest in Trip worth $2.9 billion given the current market cap of $24 billion for NASDAQ: TCOM. The company is continuing to do many small investments.

From a cash flow perspective, free cash flows for shareholders for 2020 should be 19 billion RMB from net income, plus 5.7 in depreciation, minus 7 billion for investments. So, 17.7 billion RMB from operating activities, minus 7.5 for investments, I get to free cash flows of 10 billion RMB or $1.6 billion.

However, if I eliminate iQIYI, the picture looks much better and we are at 16 billion RMB or approximately $2.5 billion USD for the Baidu core business.

You could say that $2.6 billion is not much for a company that isn’t growing fast, given that the market capitalization is $77 billion and the price to cash flow is than 29.6. However, that is why we have to approach Baidu from a sum of parts valuation too.

Baidu sum of parts valuation

I will start with the market capitalization of $77.8 billion. Deduct $12 billion in cash ($25 billion in cash, minus $3.7 billion for YY and minus long-term liabilities including the short term part of those) and we are at $65.8 billion.

There is 76 billion RMB in long-term investments that includes a 12% stake in CTRIP among other things. If to be conservative, we take 66% of book value of the long-term investments for our valuation, we are at 50 billion RMB or $7.7 billion. Deducting $7.7 billion from the above $65.8 billion we are now at $57.1 billion.

Then we have the unprofitable iQIYI business that Baidu was in some talks to divest. The market capitalization is $13.3 billion where the 56.5% stake is worth $7.5 billion. If Baidu divests its stake, perhaps it can get a premium as it is said Baidu asked $20 billion while buyers think it is worth $10 billion. Anyway, by deducting the current market value of iQIYI from the above valuation, I am down to $49.6.

The cloud business has revenues of 10 billion RMB and is growing at 44%. In the current market, a valuation of 10 times revenues might not be that crazy. In such a case, the cloud business would be valued at $15 billion. Another possible value could be Apollo, the autonomous drive tech, as anything related to electric vehicles and robotaxis is crazily valued today and the autonomous drive leader in China should be worth something. Some say Tesla is worth zero while others think it is worth even more than the current market capitalization.

Nevertheless, I am going to use the above $49.6 billion, compare it to the $2.5 billion in FCF I got above for the search engine business, and I have a search engine with good cash flows in China trading at 20 times free cash flows and huge options for growth coming from Cloud, Autonomous and Robotaxies.

Plus, as the Chinese economy rebounds, we might see 12% growth in advertising revenues.

If I put a $10 billion valuation for Apollo and $15 billion for the cloud business, among other possibly very valuable items, the remaining price for Baidu’s core business would be just $23.6 billion.

| BAIDU SUM OF PARTS (billion USD) | |

| iQIYI | $7.5 |

| INVESTMENTSCTRIP etc. | $7.7 |

| CASH | $12 |

| CLOUD | $15 |

| APOLLO | $10 |

| YY Live | $3.7 |

| Total | $54.2 |

| BAIDU remaining | $23.6 |

If we take into account the above, you get a lot of things and $23 billion for the current Baidu cash flow positive business is ridiculously low. The question is how will the market value the company, the listing prospectus clearly states not to expect dividends soon.

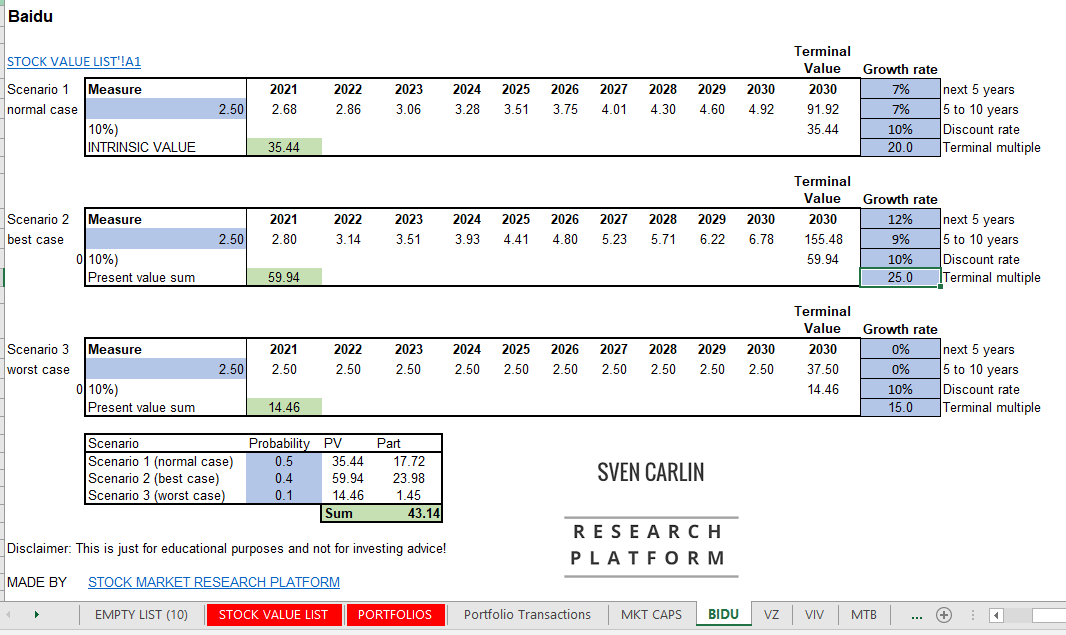

Baidu stock valuation

To make a valuation, I will start by using the $2.5 billion in FCF and attach a 7% growth rate which is pretty conservative given the expected Chinese economic growth rate on internal economy focus and the CIC report 12% market growth rate.

If we assume 7% free cash flow growth onward and a 20 price to FCF ratio in 2030 for the terminal value, the fair valuation for a 10% required return is $35 billion. If they reach 12% growth per year which is possible an in line with the market’s expected growth rate, the fair value would be $60 billion. In the worst-case scenario of no growth with a 15 price to free cash flow ratio, the value would be just $14.46 billion. The $14 billion valuation is not that crazy. If we add the cash and attach some value to other businesses, the low of $30 billion reached in March 2020 was not far.

With a 50% chance for a normal scenario, 40% for the best-case scenario and 10% for the worst-case scenario, my Baidu valuation gives me a fair value of $43.14 billion for an expected return of 10%.

The question is how big is the potential of Cloud, iQIYI, YY Live, Apollo, Chips, Healthcare and Robotaxies worth. If the totally addressable market of 5.5 trillion RMB is even half correct, the value of Baidu’s other businesses could easily be more than $100 billion in 2025, if not more.

We could say that Baidu’s fair value is $43 billion. When we add $12 billion of cash we are at $55 billion and therefore if you invest in Baidu now, you pay $23 billion for Cloud, iQIYI, YY Live, Apollo, Chips, Healthcare and Robotaxies.

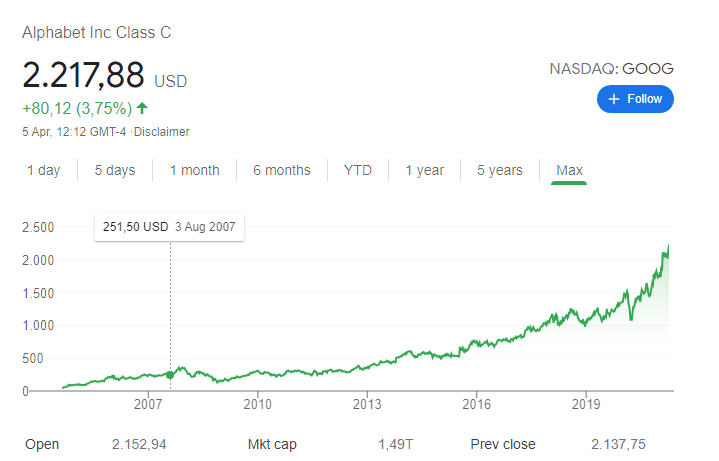

BIDU comparison to GOOG

Baidu’s western counterpart would be Google (NASDAQ: GOOG). However, the comparison is not an easy one as Google’s market capitalization is $1.49 trillion while BIDU’s is $77.8 billion. GOOG’s price to sales ratio is 8.59 while BIDU’s is much lower at 4.47. Of course, GOOG has been growing constantly over the last years, year after year, but if BIDU manages to do the same, we could see a similar valuation especially as the Chinese digital customer becomes more valuable thanks to the focus on internal economy growth.

iQIYI can also be compared to Netflix but that is again a crazy comparison in market capitalization terms but iQIYI has 100 million members while Netflix has 200 million.

Baidu investment thesis & risks

If you think iQIYI is worth its market cap, cloud is worth 10x its current revenues and Apollo can be the dominant player in autonomous driving in China with a strong Robotaxi squad, then BIDU search engine business is maybe even irrelevant from an investing perspective and only there to take advantage of the huge opportunities through cash flows and data.

You can also see it as you are paying a 20 price to FCF ratio for the search engine and you get all the other businesses for free.

The key investment thesis is the portfolio exposure you get to China and to the future tech like cloud, autonomous driving and Robotaxies. If you wish to have such portfolio exposure with a margin of safety coming from a profitable business with a strong position, then BIDU could be your choice.

There are also many risks.

BIDU stock investment risks

We have already mentioned how the stock can be badly looked at the market for many years and deliver negative returns for long periods. If the ‘cool’ business opportunities don’t lead to significant developments relatively fast, many momentum buyers might turn into sellers and put pressure on the stock. Even if ARK ETFs runs into liquidity issues, it might be forced to sell its large position in BIDU and add more pressure on the stock.

From a business perspective, there are several risks and the HK listing prospectus explains the risks for Baidu from page 40 to 112. If you are really interested in investing in BIDU, I strongly suggest you read those. Apart from normal businesses risks like competition from Tencent, Alibaba and others, currency, Chinese government involvements and others, here is a short summary of other interesting risks related to Baidu:

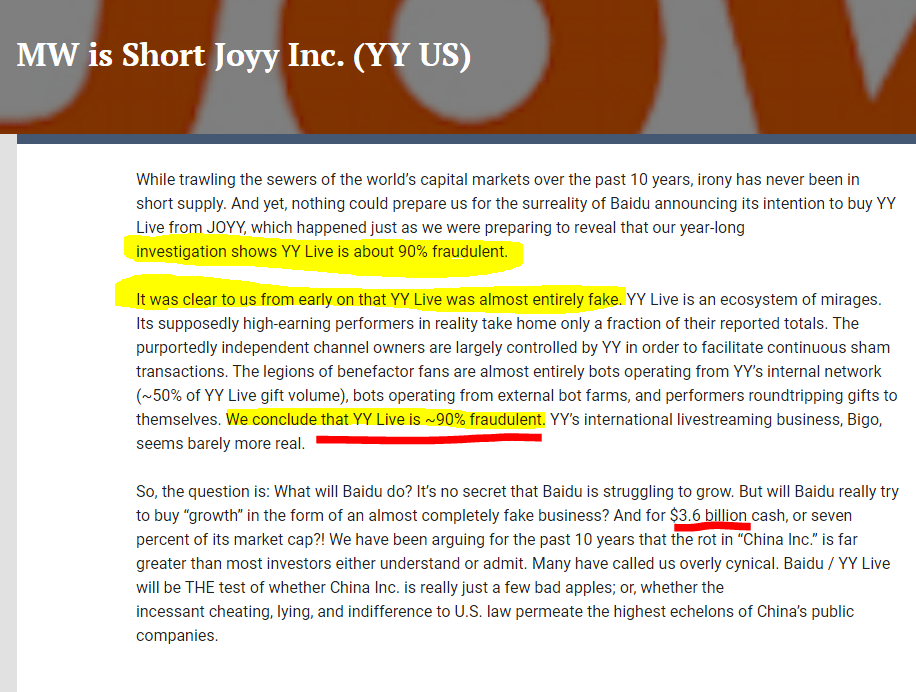

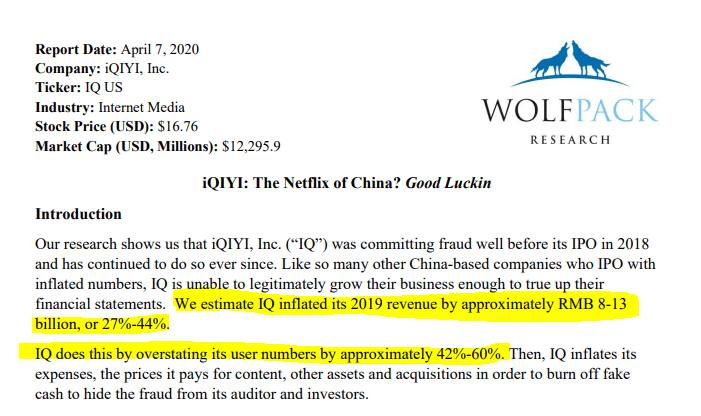

Muddy Waters recently issued a short seller report stating that YY Live is 90% fraudulent and most of the traffic is created by bots.

Similarly to Muddy Waters, Wolfpack issued a report that alleges iQIYI inflated its user numbers

The SEC launched an investigation on the above and there have been other class-action law suits so it is still uncertain what will come out of the above.

A general risk for investing in Chinese companies is also the VIE (variable interest entity) structure through the Cayman Islands. By buying BIDU stock you buy the contractual agreement the Cayman company has with the company on mainland. For now there are no issues with such a structure, but given the environment regarding China and the US, you never know.

On listing issues, for now only Chinese government owned entities have been delisted and then transferred to OTC. We will see how the environment evolves over time.

BIDU stock comparative discussion

From a fundamental perspective BIDU looks fairly priced for a 10% return. However, when compared to Tencent or Alibaba, it is still on the expensive side (Alibaba stock analysis). Of course, many of the growth potential has already been developing for Alibaba and Tencent while with Baidu it is all still in the early stages, so a cash flow comparison might not the proper one.

Nevertheless, if you are looking to diversify into China, Baidu seems an interesting option to be exposed to the internal economic growth ahead in China while also offering currency diversification.

Don’t forget to check the above table for more stock analyses and if you enjoyed this analysis and wish to get notified when a new analysis is made, please subscribe to my newsletter.