Andritz Stock Analysis – Good But Not Good Enough

This Andritz stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian Stock Exchange. Austria is one of the cheapest stock markets globally at the moment so please check the Austria Stock List for interesting investments.

Andritz stock Overview

Andrits Stock Vienna: ANDR

Andritz Stock OTCPK: ADRZF

Andritz stock represents Andritz AG which is an international technology group providing plants, systems, equipment, and services for various industries. The company is one of the technology and global market leaders in the hydropower business, the pulp and paper industry, the metal working and steel industries, and in solid/liquid separation in the municipal and industrial segments.

Andritz stock analysis – Business overview

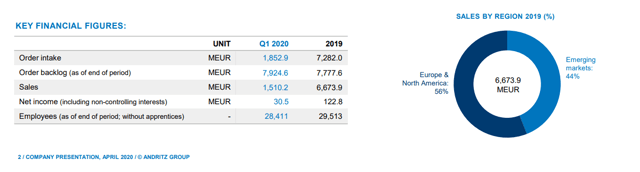

Andritz stock represents a globally diversified business but it also has a low net margin of just 1.6% in 2019.

However, the business offers very interesting products for very interesting sectors, sectors that are expected to grow as the global economy grows and develops.

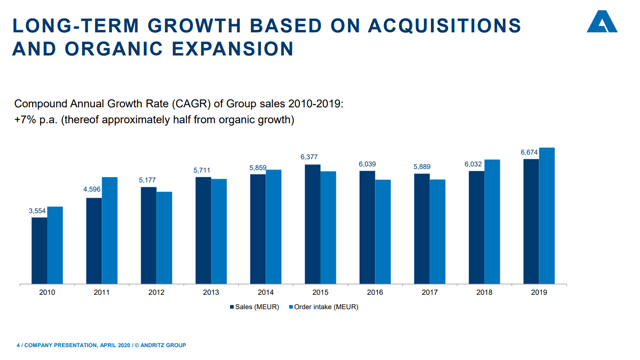

What is also interesting is that the business has been growing steadily over time organically and through acquisitions. Growth, if done smartly and profitably, is usually an investing positive.

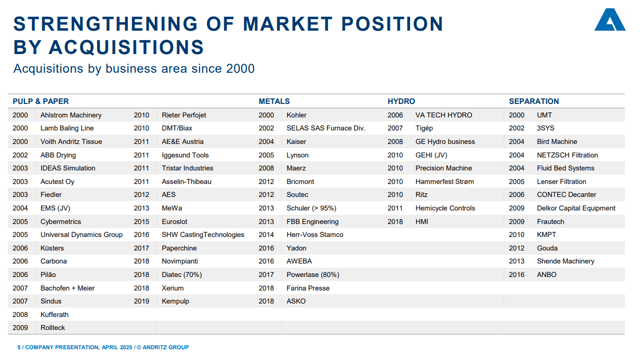

Additionally, when a big company acquires many small companies, it can scale their technology and products globally, which is a good thing. Andritz has made many acquisitions over the last two decades.

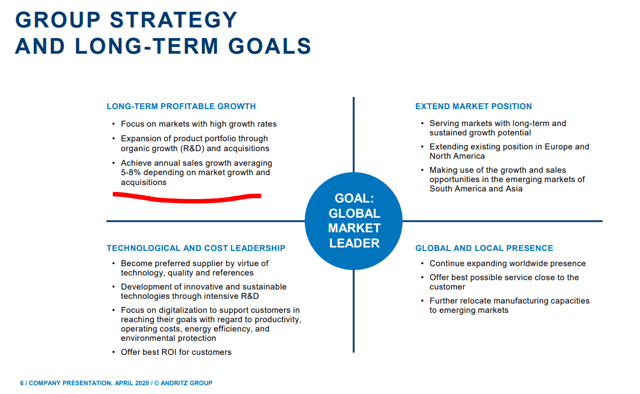

The managements’ target is to grow between 5 and 8% per year. They will strive to offer the best products to their customers and continue to expand into growth sectors. This explains the company perfectly: “The ANDRITZ GROUP does business in highly competitive markets in which only a few large suppliers bid for only a few large orders”.

Let’s now see how the above business model is reflected in the stock’s fundamentals.

Andritz stock analysis – fundamentals

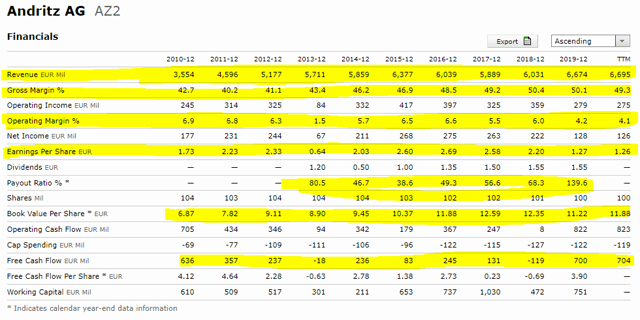

Revenue has been growing steadily, gross margins are very high and have also been improving over time, going from 40% to 50%. But operating margins are in the low single digits that leads to low earnings. The dividend pay-out is high and consequently the book value doesn’t increase fast. Cash flows are volatile but can reach high levels in good years. The key to check is whether the operating margins can be increased to high single digits, something that would completely transform the company. Information about possible margin improvements can be sometimes found in the annual reports and management discussions.

Andritz Stock Analysis – A look into the annual report and management discussions

The first page in the management discussion for 2019 is about the slower economic growth which leads to the conclusion that the business is cyclical and dependent on economic growth. More growth, more sales and likely higher margins and vice versa.

All in all, Andritz’s business depends on activity in:

- the paper markets,

- the automotive industry for the metal segment,

- demand for hydro.

The issue is the fierce competition in all of the above segments and all their products are created to increase return on investment for the customers, which means cost is key. This leads to low margins. In good times, when business in the sectors is good, customers are incentivized to invest more, which allows for higher sales and higher margins for Andritz.

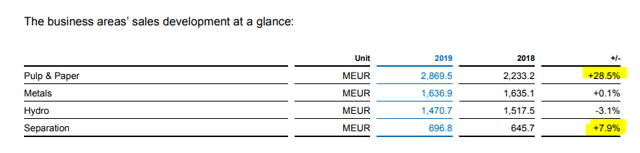

Despite the negative environment, sales in the paper and separation business segments grew.

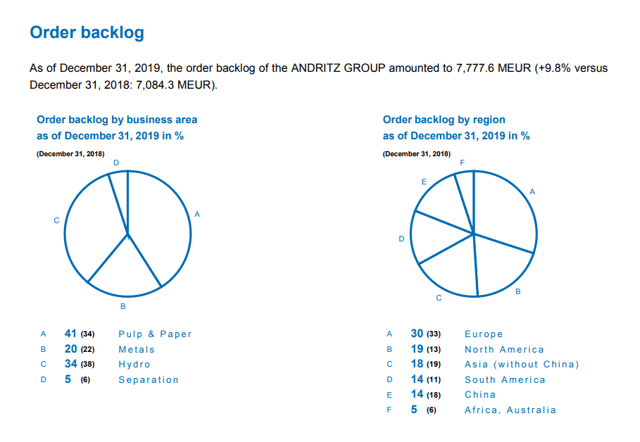

The order intake is high for paper thanks to new mills being built in South America (probably Klabin in Brazil and UPM-Kymmene in Uruguay.

The backlog could be lower due to covid, but the 2019 situation indicates how stable the company is, which is a good thing.

Andritz stock analysis – earnings

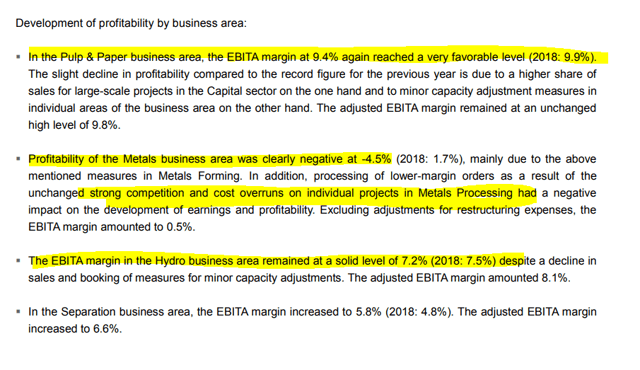

In 2019, earnings were impacted by processing lower margin business in the metal area (fierce competition) and due to measures for capacity adjustments totalling 113 million EUR (MEUR).

When it comes to margins, the detractor is the metal business.

Given the current environment in the automotive industry, not so much oriented to increasing production, the number of cars, but switching to electrification, I don’t know if there will be many new factories being build that require their machines, or perhaps it will take some time for the oversupply in the sector to even out.

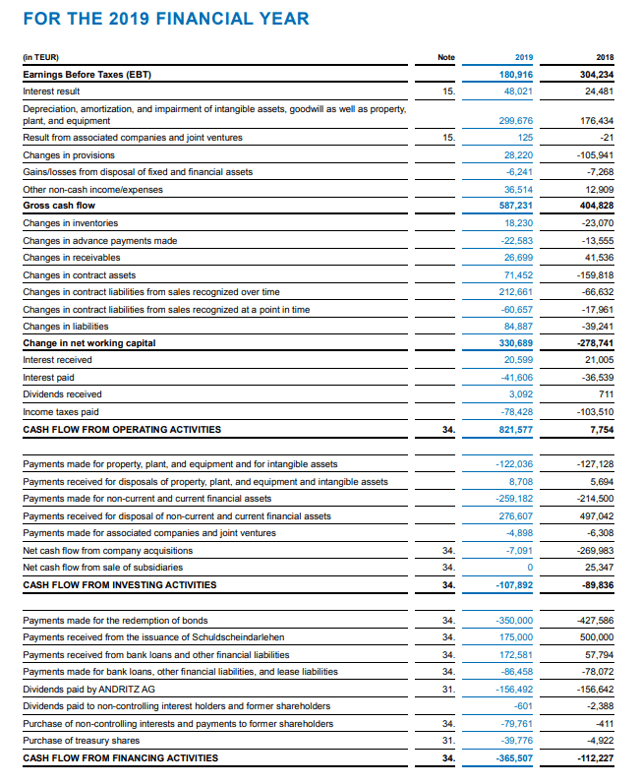

When it comes to investing, it all boils down to cash flows and cash flow is good with Andritz. Cash flow from operating activities is at 821.6 MEUR.

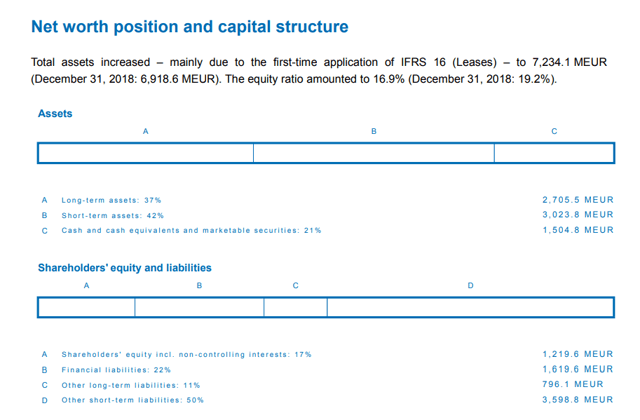

Andritz stock analysis – fundamentals

At first look, Andritz looks like a highly leveraged business, but most of the leverage comes from contract liabilities from sales recognized over time in the amount of 1,230.3 MEUR, provisions (489.8 MEUR), and trade accounts payable (668.9 MEUR). The most important items in other liabilities (935.0 MEUR) are accruals and outstanding order related costs (428.2 MEUR), as well as unused vacation and other personnel-related accruals (255.7 MEUR). Non-current liabilities, at 796.1 MEUR, largely contain provisions (593.3 MEUR), Lease liabilities (213.7 MEUR), and deferred tax liabilities (159.7 MEUR).

So, it is not that they have huge debt in the form of loans that they can go bust on. The financial liabilities are 22% of the balance sheet.

The gross cash flow per year is approximately 500 million EUR per year, the working capital if volatile, but it should even out over time, or grow as the business grows. They have actually used 365 million of their cash flow in 2019 to repay debt. On a market cap of 3.3 billion EUR, that is a 10% yield. Repaying debt is a way to increase value for shareholders.

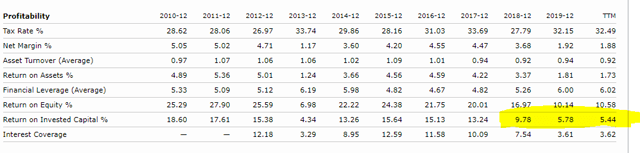

The company is cash rich, and the cash position is at 1.2 billion, which is high compared to the market capitalization. The main question is whether the focus will ever be on really rewarding shareholders or whether they will continue doing acquisitions for their slow growth. At the end it boils down to return on invested capital, is it better to give the capital to investors or reinvest it?

As their earnings haven’t really been growing, but they keep investing and buying companies, my conclusion is that the return on invested capital isn’t enough to invest in this company except in cases where it would be extremely cheap. Let’s look at the investing situation.

Andritz stock analysis – investment situation

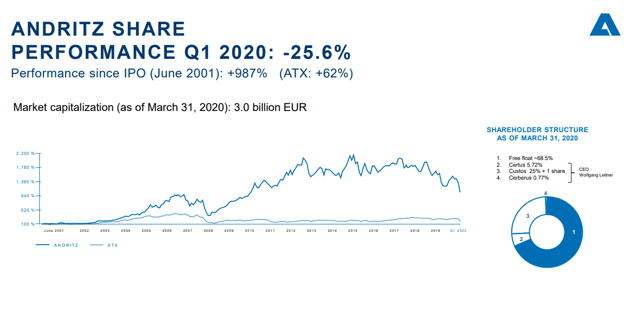

Andritz stock has been an amazing investment since the early 2000s, up even 20 times at a point in time. But the stock didn’t do much since 2013.

The current market cap is 3.3. billion which is interesting on 500 million in operating cash flows. However, we need to deduct 100 million in capex, the constant acquisitions they need to make just to keep up, where they likely overpay as we don’t see improvements in margins.

I would say that investors should expect the dividend yield to be between 2 and 5% depending on the situation in the economy which is ok, but we can’t expect the boom from the early 2000s to happen again as the competition is much more intensive now than it was the case when China was just starting to boom and required many machines made by Andritz.

All in all, it looks like an ok business, well managed but in a tough industry with thin margins and high competition. Investment returns will likely be positive but in the single digits long time, in line with the return on invested capital. Unfortunately, the focus is not on making money for shareholders but mostly to maintain the current business.

Perhaps in a new upward cycle, the ROIC might turn higher, but the competition is high, probably attracted by the high ROIC measures the company delivered in the past. The situation can remain ugly for very long, as it has been the case since 2013, so it is not something I will spend much time on.

The Andritz Stock Analysis is part of the full Austrian Stock Market Analysis make by Sven Carlin for the Sven Carlin Stock Market Research Platform.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: