Aeroports de Paris Stock – Groupe ADP Stock Offers Global Growth With 400% Return Potential

This Aeroports de Paris stock analysis is part of my global airports stocks list with detailed stock by stock analyses.

Aeroports de Paris Stock Overview – EPA: ADP

Aeroports de Paris Stock or Groupe ADP stock has been severely hit due to COVID-19 and is currently down 50%. When compared to other airport stocks, ADP group stock price decline is among the worst declines.

Groupe ADP’s dividend is in line with other airport stocks dividends, even if a bit on the lower end. For example, Aena stock has a 2019 dividend yield close to 6%. The market cap is 9 billion EUR while the price to earnings ratio of 17 is also relatively high. The stock went public in 2006 when the French government did a partial IPO.

In this Groupe ADP stock analysis, we will give:

- A business overview,

- Fundamental analysis,

- Dividend discussion and

- Aeroports de Paris Stock Price Forecast and Investment thesis.

Aeroports de Paris Stock Analysis – Business overview

Aeroports de Paris stocks gives you exposure to the following airports and markets:

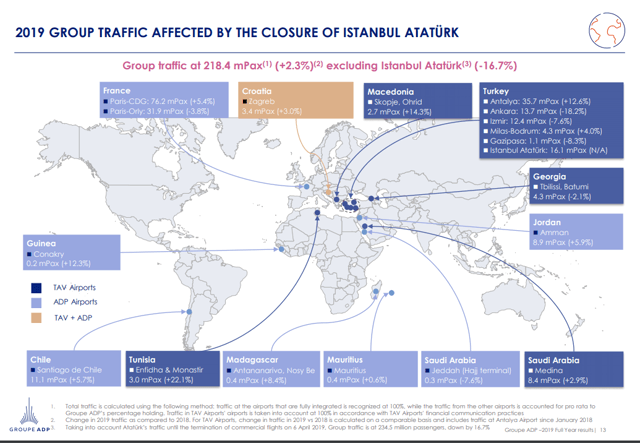

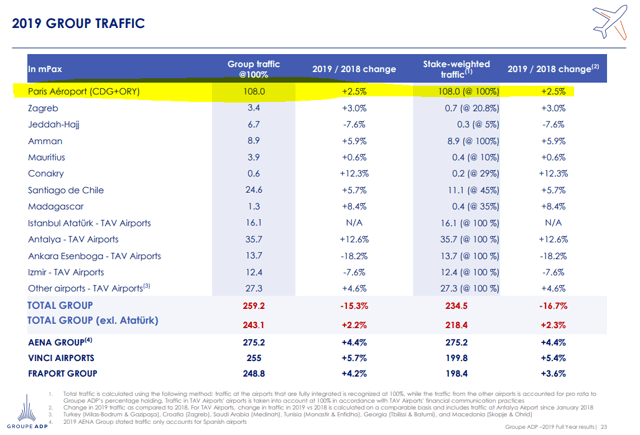

The principal airports are Paris CDG and Paris-Orly. Then the airports in Turkey (46% stake) and various airports around the globe. The largest chunk of traffic and revenue comes from the two Parisian airports.

Stakes and acquisitions over the years:

They also own 8% of Royal Shiphol Group which owns the main airports in holland and also Terminal 4 at JFK.

Further, Groupe ADP is currently in the process of acquiring 49% of the Indian group GMR Airports that includes Delhi International Airport and Hyderabad International Airport in India, airports in development: Mactan-Cebu Airport in the Philippines, Goa and Heraklion, and yet to come airports Nagpur and Bhogapuram.

The new acquisitions had traffic of 102 million people in 2019, EBITDA of 205 million EUR. The paid price 1.360 billion EUR which gives an EBITDA ratio of 13, in line other historical airport acquisitions made since 2012. They don’t expect it to be accretive to earnings before 2025, but expect significant improvements afterwards as it will be accounted through the equity method given the 49% stake.

If you can borrow money in Europe at ridiculously low rates and then invest in India where the IRR is above 10%, you should be stupid not to do it. The same game is played by most European airports that have access to practically free capital. Could be a big contributor to earnings over the coming decades.

All in all, a global airport operator that is playing the card all other airports are playing on – global traffic growth. The acquisition adds significant potential for growth as air traffic in India is expected to grow a 6.7% per year over the coming two decades. If that happens, the acquisition is a no brainer at any price.

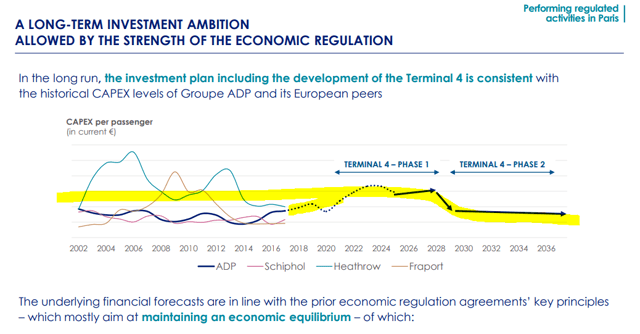

Other plans are the development of Terminal 4 at Paris CDG, expanding/improving Paris-Orly. Apart from these bigger projects and the Indian acquisition, there is a plethora of other typical airport projects like improving shops, real estate projects etc. To note is the earlier closure of the operated Istanbul Ataturk Airport where they received compensation for. This is due to the opening of the new airport in Istanbul.

Groupe ADP’s actual strategy is to have a mix of airports with different risk profiles, from Paris to Turkey and India. They will also continue with acquisitions when possible.

Groupe ADP Stock Analysis – Fundamentals

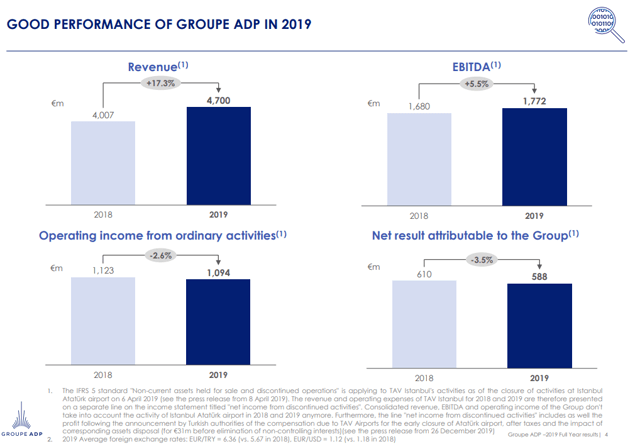

If we would value Groupe ADP at the same valuation they paid for the recent Indian airports acquisition, the value should be 22 billion EUR as EBITDA for 2019 was 1.7 billion. The current market capitalization is 9.3 billion EUR so we have to see whether the difference is justified or a value investing opportunity thanks to the market’s currently negative sentiment towards airports.

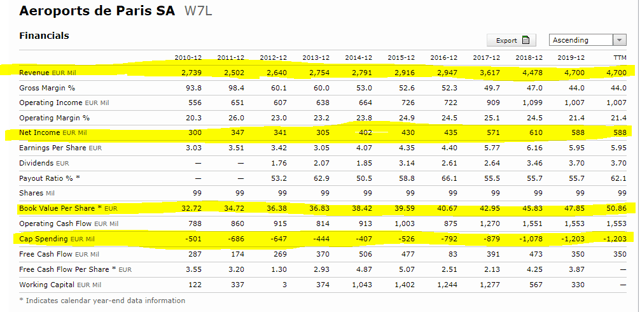

Revenues have been growing steadily as the Parisian airports grew and acquisitions were made. Net income followed and, alongside generous dividend payments, book value grew too, from 32 EUR per share to 59.86 EUR per share. Increased book value alongside a growing dividend means the management has been able to create value for shareholders.

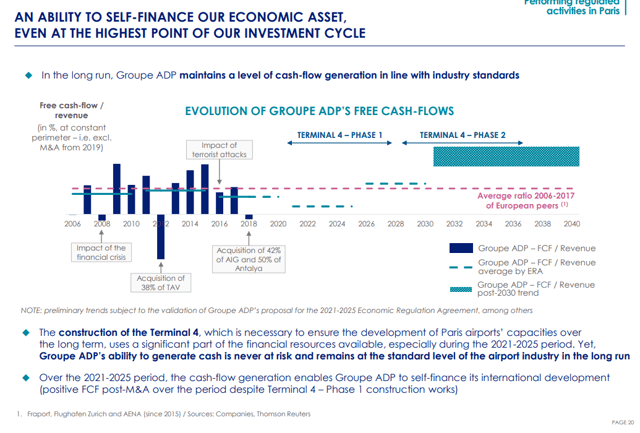

Cash flows are good with operating cash flows at 1.5 billion EUR while the free cash flows are ‘just’ 350 million but that is because of the extremely high investment numbers.

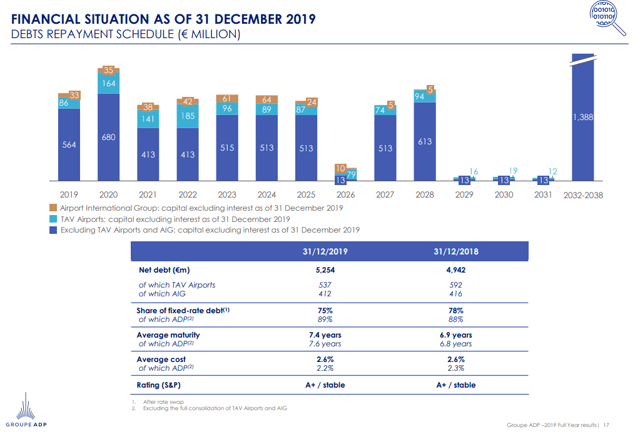

The debt structure will probably be altered after we get the second quarter results for this year including the COVID-19 impact, but from what we are seeing, interest rates have never been so low and liquidity never so high. Therefore, debt doesn’t seem like an issue nowadays. It actually might be a hedge against possible inflation coming due to all the money printing.

The average cost of debt at the end of 2019 was 2.6%, a very low interest rate if you ask me. The average maturity is 7.4 years that gives some kind of protection against inflationary moves in the future.

Also, they plan to finance their growth by themselves which means they already have strong cash flows and don’t need to partner up or take too much debt.

Of course, the key in the short-term is the COVID-19 impact where the stock and the business will be very bad. However, as investors, we are looking at the long-term and perhaps the current situation will be one of the best times to add airport stocks to your portfolio. The dividends will certainly be cut.

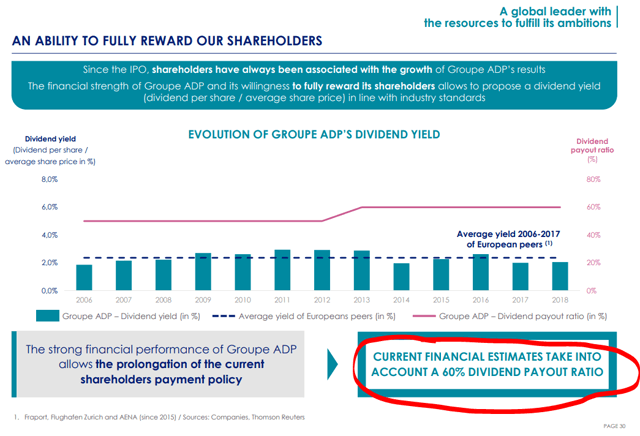

Groupe ADP Dividend

The Aeroports de Paris dividend makes it a dividend growth stock as the dividend went from 2.07 in 2013 to 3.7 EUR per share in 2019 for a yield of 4%. That is not as high as other airport dividends but we much calculate the potential future growth into the dividend assessment. It is unlikely the dividends will grow much before 2029, even if the COVID-19 situation returns to normality because the company is entering a high capital investment cycle.

However, after 2029, we could see extreme growth in dividend as the capital expenditures stabilizes and traffic growth leads to higher profits. If the current dividend pay-out ratio of 60% increases, the benefits could be even higher.

If they can grow EBITDA to 3 billion over the next 10 years and from that, pay 2 billion in dividends, the dividend yield on the current stock price would be close to 20%. That would likely lead also to a quadrupling in stock price which is not a bad thing over 10 years.

Of course, the positive scenario will not happen overnight, but this is the reason one might invest in airports.

Aeroports de Paris Stock Price Outlook

The short-term stock price outlook mainly depends on COVID-19. But, as investors, we are partial owners of the business so given the short to medium term uncertainties, you have to think as an owner. Based on the 1.5 billion in EBITDA, the valuation should be close to 30 billion which gives you a 3x at the start. If I add the potential growth coming from global economic development, especially with the Indian exposure, plus the high capital investment that should lead to higher future dividends, the 3x might only be the start of the story over the coming decade.

I have been looking at European airport stocks over the last week and the more I look the more I am intrigued by the potential these businesses offer. Of course, it all depends on future traffic growth, but I don’t see people not flying in the future and not visiting Paris or other cities. Plus, Indian economic growth adds huge potential. They also plan to make more acquisitions, if they keep doing it with free European money, not a bad thing.

The Aeroports de Paris Stock Analysis is part of my Airport stocks analysis made by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundred of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: