Zumtobel AG stock analysis – Potential cyclical upswing or not?

Zumtobel AG stock analysis is part of my full, stock by stock analysis of the Austrian Stock Market that offers interesting investing opportunities. Check my Austrian Stocks List for more Austrian stocks.

Zumtobel AG stock price analysis – VIE:ZAG

Zumtobel stock had a very volatile past with major up and downturns. It is looking like a typical cyclical stock from the Peter Lynch stock category. From the last high in 2017, the stock did not recover. This would imply a potential in the near future but the explanation of the below ups and downs is mostly related to exuberance cycles in the lightning industry that had been promising a lot, but delivered little except for extreme competition and low margins.

Let us look at the business model, the fundamentals, and give an investment outlook.

Zumtobel AG stock analysis – Business fundamentals

Zumtobel is an Austrian company specialized in lighting technology. The company develops, produces, and sells lightning technology and offers lightning solutions, luminaires, lighting management for indoor and outdoor applications.

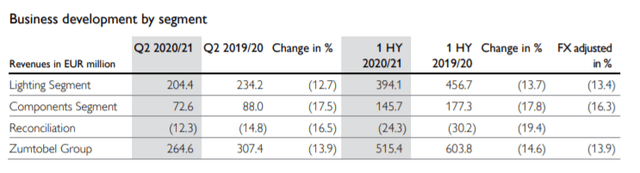

The company operates two main business segments – lightning and components segment:

The key revenue segment is lightning while the components segment makes for the remaining 27% of revenues.

The products from Zumtobel are mostly used in new office buildings and are used for renovations as more and more companies focus on being more sustainable and CO2 neutral.

The products help with achieving their goals, which is the growth catalyst for Zumtobel. Not an extremely big one as the competition is relatively high – seen at the low Operating-Margin of 2 % to 3 % in the last years. This low margin indicates that Zumtobel has not very strong pricing power and consequently no moat.

The revenue distribution is highly concentrated on Europe, with about 75 % of the total revenue. This is a risk, as Europe is not growing that much compared to Asia, for example.

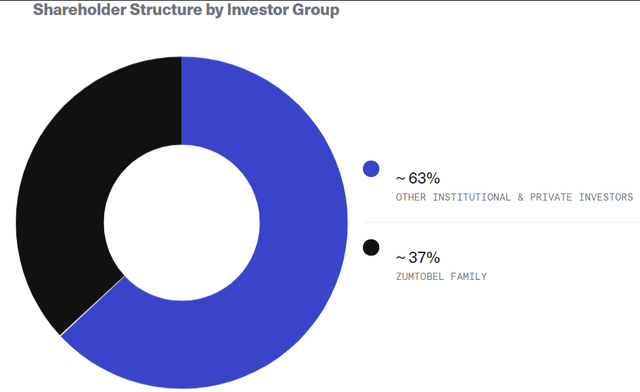

The family of the founder (Walter Zumtobel) holds 37 % and form a strong core shareholder group. A positive aspect, as with their voting power, the family-run businesses tend to focus more on the long-term success other than just focusing on the next quarter. In general, family-run enterprises perform better.

Zumtobel AG stock analysis – Dividend

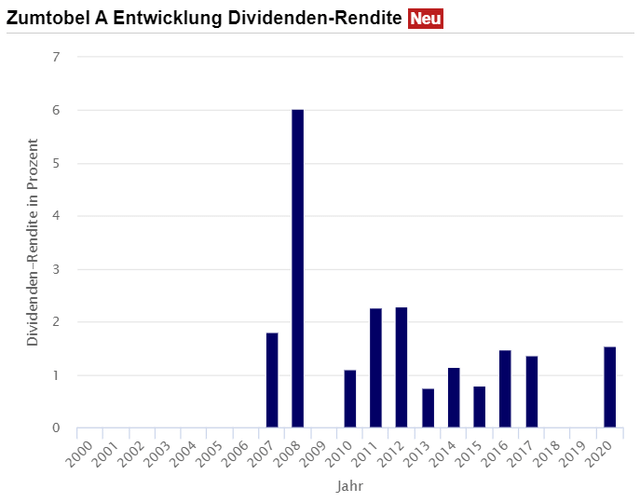

The dividend history of Zumtobel is not looking that great. The yield was since 2010 between 1 % and 2 % and had to be cut in 2018 and 2019.

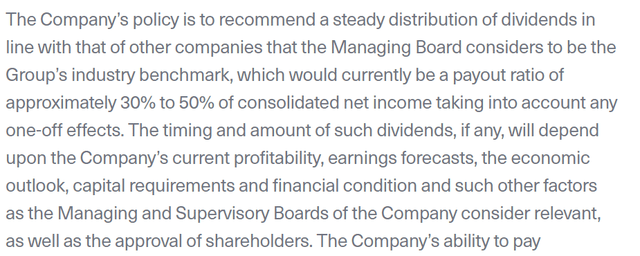

A dividend of 30% to 50% of the net income can be expected in the future. But the net income went from 51 million EUR in 2010 to 2 million EUR in 2019.

The dividend policy is not related to earnings but to cash flows. Earnings are easier to increase/decrease with some accounting tricks like higher/lower depreciation. The free cash flow is the operating cash flow minus the capital expenditures (CAPEX) and, therefore, a bit better to look at it. But more from that in the financial discussion.

Zumtobel AG stock analysis – Financial discussion

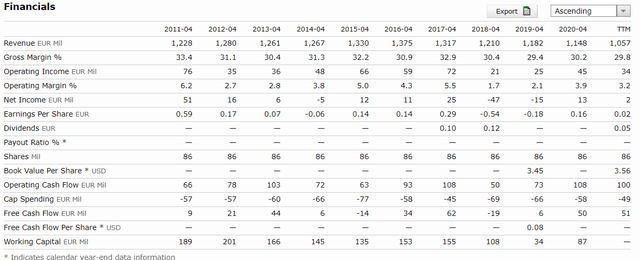

Revenue has been stagnant over the last decade a slow decline since 2016. Unfortunately, profitability went nearly to zero as competition increased and prices likely declined.

A positive aspect of the financials is the operating cash flows but when deducting the capital expenditures, not much is left.

The company has 71 million EUR in cash but 191 million EUR in long-term debt and 25 million in short-term debt. Adding to that are 87 million EUR in pensions obligations, 51 million EUR in severance compensations, and 11 million EUR for employee benefits liabilities, which equals a net debt of 294 million EUR which is a lot for a company not making much money.

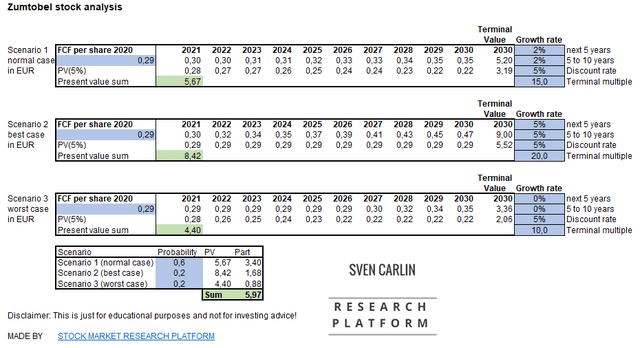

The free cash flow was 53 million in 2019. If we forecast for 2020 a similar free cash flow and taking the lower limit of 30 % for the dividend payout 30, the result is a potential dividend of 0,29 EUR per share. This value will be used in the model.

The valuation model will give a rough stock price valuation. This model’s general assumptions are a discount rate of 5 % and a terminal multiple depending on the growth. The model uses the free cash flow to discount the cash flow available to shareholders.

In the model below are three scenarios:

- Scenario 1 (normal case): 2 % growth for 10 years with a 60 % probability

- Scenario 2 (best case): 5 % growth for 10 years with 20 % probability

- Scenario 3 (worst case): 0 % growth for 10 years with 20 % probability

Based on this model, the investor could expect a return of 5 % annually with the current stock price and the assumption form above.

Zumtobel AG stock analysis – Conclusion and investment outlook

The company offers a potential cyclical investment opportunity. But their growth is dependent on further investments into the construction sector, and even with more robust growth, Zumtobel has weak pricing power.

The debt is relatively high for the company, and the dividend payment is not as frequent as a family business might intend. The best option for the family would be to sell the company but I don’t know if there are interested buyers given the sector is not as hot as it was.

I’ve looked for any kind of differentiators in the investor presentation but found nothing, it all depends on economic and construction activity in Europe. The stock is definitely cheaply priced at 275 million EUR, but apart from some special situations, I don’t see much happening. Plus, given the liabilities, a 5 times EBITDA multiple might be all a company sale could deliver. So, perhaps the owner keep their jobs while it lasts.