Vinci Stock Dividend – Too Risky Due To High Debt and Expiring Concessions by 2032

This Vinci stock analysis is part of my global airports stocks list with detailed stock by stock analyses.

Vinci Stock Overview – EPA: DG

Vinci stock is not a pure airport stock but more of an infrastructure holding and building business. However, the business compounded over the years and those investing 25 years ago made more than 20 times their money. If the business model is sound and can continue to compound at similar rates, investors might be looking at similar returns.

This Vinci stock analysis, we will give an answer to whether Vinci might repeat the past success with the following content:

- Vinci’s business overview,

- Vinci stock fundamental analysis,

- Vinci dividend risk analysis,

- Vinci’s investment conclusion.

Vinci stock analysis – business overview

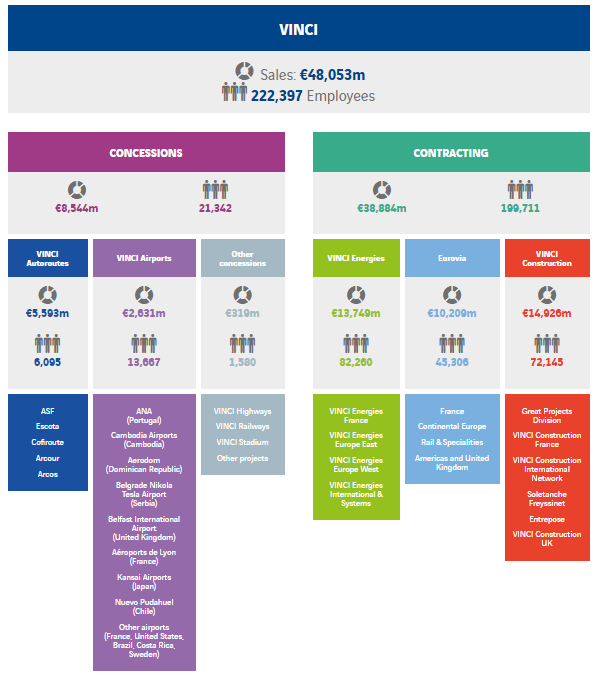

As said, Vinci stock is not really an airport stock, but it is much more diversified offering various concessions and infrastructure contracting. The company designs, finances, builds and operates infrastructure and facilities across the globe.

However, if we divide the above on EBIT, Vinci Autoroutes made 3 billion EUR in 2019, Vinci Airports 1 billion EUR, Vinci Energies 0.8 billion EUR, Eurovia 0.4 billion EUR and Vinci Construction 0.4 billion EUR. So, the main business are concessions where the roads and airports make 71% of profits but just 17% of revenues. This is due to different business models and margins.

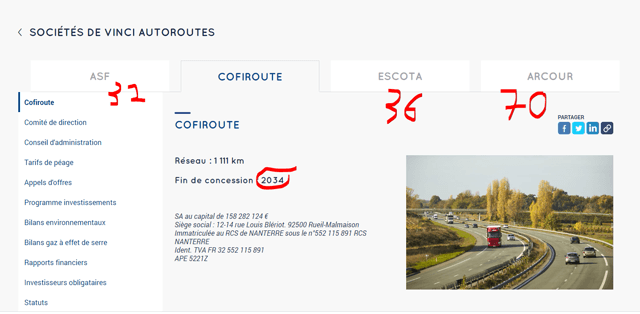

The key to Vinci’s concession business are its French Autoroutes and global airports. The problem with road concessions is that those usually end where most of Vinci’s concessions end between 2032 and 2036. Only the smallest road of just 111km, Arcour, ends in 2070.

The main airports contributing to most of the traffic for Vinci are 10 airports Portugal (59 million) including Lisbon, Gatwick (50.1%) and Belfast in the UK (52 million), Kansai (40%), Kobe and Osaka in Japan (51 million) and Santiago de Chile airport with 26 million passengers per year. The concession in Portugal lasts till 2062, Gatwick is unlimited, Kansai is up to 2060 while Santiago is up to 2035.

The construction business part is coming off a period of high growth, but with still small margins. Given the current economic situation, higher government debt levels due to COVID-19, it is likely there will be a slowdown there and it is also possible to see zero profitability in that segment for a while.

Vinci stock fundamental analysis

Vinci can be categorized as a slow growth stock. They have acquired most of their French autoroute concessions in 2006 from the government, at a good price. The good price paid has been an issue and there were many complaints so it is unlikely that, especially in this low interest rate environment, they’ll manage to get similar terms in the future. Plus, there are only 15 years left on those concessions.

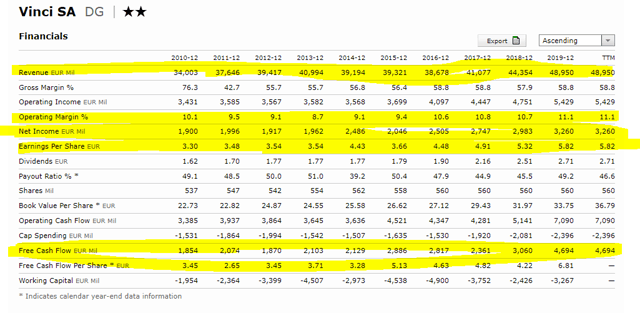

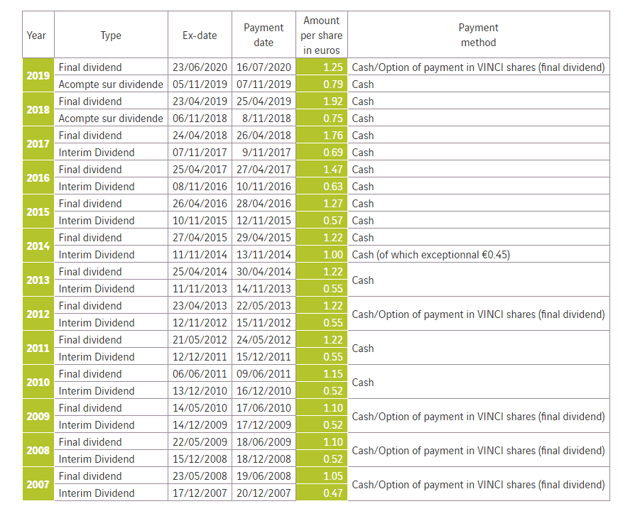

Earnings, dividends and cash flows grew alongside revenues and as the company made more acquisitions; 2013 Portugal, 2019 51% of Gatwick etc.

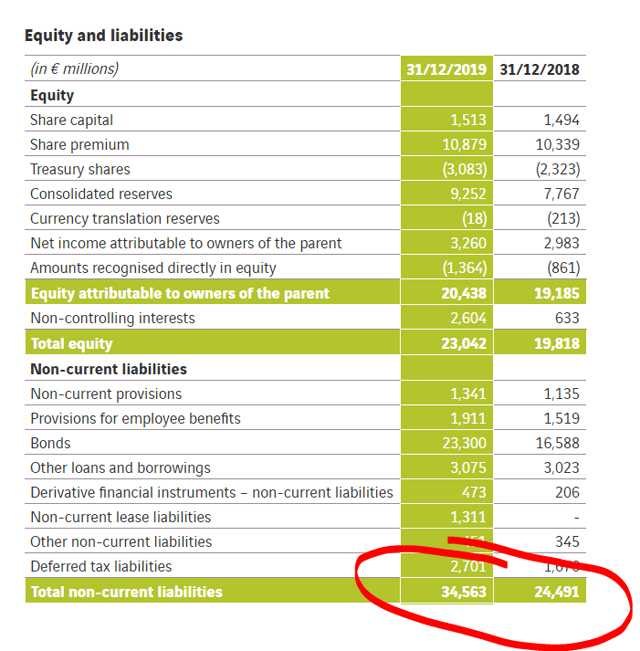

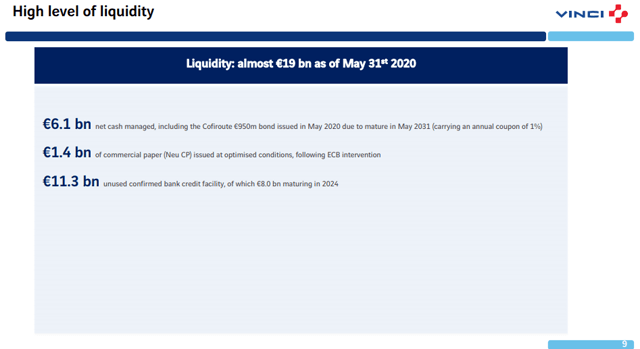

The company has good liquidity and a good credit rating, but the business model is based on taking debt to make these acquisitions. I don’t like the fact that their liabilities keep growing while their concessions have time limits. It all looks like a story that will not end well.

I would say that the great stock market return Vinci stock offered over the past 25 years is mostly thanks to declining interest rates in a growth environment. This allowed for better and better margins, higher valuations and higher dividends, that led to higher stock prices.

Vinci currently has a significant amount of liquidity thanks to all the money printing that is going on, but so have others and therefore, new investments that might come along given the high debt levels government are about to encounter post-COVID, will likely be extremely competitive to get and not highly profitable, especially if interest rates change.

Vinci dividend discussion

Vinci has been paying a constantly growing dividend thanks to lower interest rates that allow for better and better margins in the concession business.

However, as the concession are coming to an end, while the debt keeps on piling, plus interest rates can’t go much lower, I wonder whether this success story might repeat itself. This makes Vinci stock as an investment too risky for me.

Vinci stock investment analysis

When you have something that can provide unlimited value, then the investment risks are small because it is likely people will keep flying and driving. However, when there is a time stamp on an investment, it isn’t an investment anymore but more of a bet on interest rates, debt levels, growth numbers, number of recessions in the period remaining etc.

Plus, the market is often focused on the past, and thus projects completely wrong forecasts on Vinci. I don’t think investors will be pleased when all the analyses out there will start to account for the impact of the lost concessions by 2032. This will likely start in 2022 as when the concessions are shorter than 10 years, the discounted impact gets bigger and bigger.

Vinci stock is one that I am going to avoid but I am going to continue to look for other, hopefully better risk and reward investments within my airport stocks list. For example, Ferrovial stock is similarly priced, but their road concessions expire in 2061 or 2098, which makes a great difference.

The Vinci Stock Analysis is part of my Airport stocks analysis made by Sven Carlin for the Sven Carlin Stock Market Research Platform.

I love to research businesses and the respective stocks. My goal is to research a few hundred of them each year and then hopefully find a few good investments. The only way to do that is to turn as many stones as possible and follow the interesting businesses closely. I am happy to share the research process here and I hope you enjoyed this and the other stock analyses published here.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: