Rosenbauer International AG stock analysis

Rosenbauer International AG stock analysis is part of my full, stock by stock analysis, of the Austrian Stock Market that offers interesting investing opportunities. Check my Austrian Stocks List for more Austrian stocks.

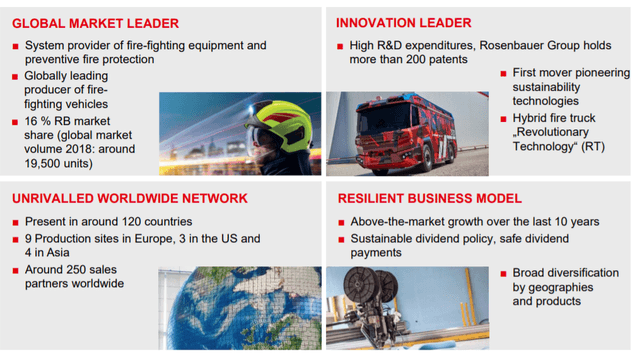

Rosenbauer International AG is the world’s leading manufacturer of firefighting and disaster protection technology situated in Austria. The company employees 3,828 people and has sales, production, and service locations in 19 countries.

Rosenbauer stock price analysis – VIE: ROS

The company was founded in 1866 and had its IPO on the Vienna Stock Exchange in 1994. Rosenbauer’s stock price had a great run up till 2015 when the all-time-high was reached at above 80 EUR per share. Since then, it could hasn’t recovered and is now trading 58 % below the peak.

If you would have invested during the COVID-19 crash in March 2020 you would have done excellently. The low was around 21 EUR which led to an increase of around 70% – but that has been the case for almost all stocks since March 2020 lows. Long-term investors have not performed well as the dividend is also just around 2 % and the stock is down over the last years. Let’s see whether the stock was high due to exuberance in 2015 or it is now down due to real structural issues with the business.

Before we can define the classification of the Peter Lynch stock category, we need to look at the business in detail as it is not clear by just looking at the chart. Let us look at the business fundamentals first, a free cash flow estimation, and then get to a conclusion.

Rosenbauer business fundamentals

Rosenbauer develops and produces vehicles, fire extinguishing systems, equipment, telematics solutions, and systems for preventive firefighting. Their customers are located around the world in over 100 countries. Their export quota is over 90%. Their mission is to be a quality leader and “we are offering the best value for money”.

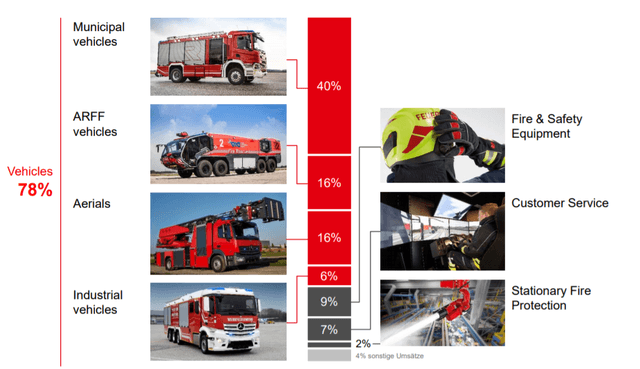

78 % of their revenue is generated with vehicles and just 9 % with fire & safety equipment, 7 % with customer service, and 2 % with stationary fire protection. Also, 78 % of their customers are municipals. Having municipalities as customers is always a risk due to their high debt levels and in many countries we can expect to see crises in the sector.

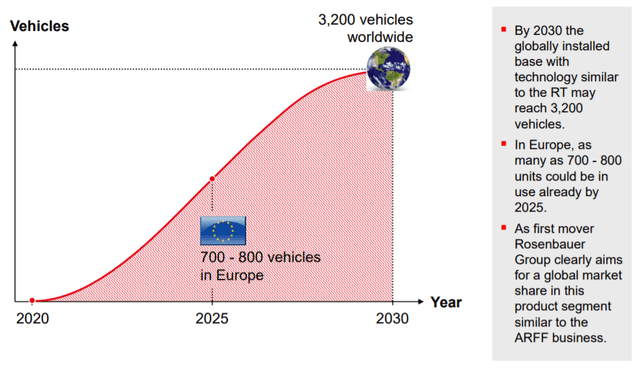

However, Rosenbauer is developing a hybrid fire truck where the goal is to be in production of 200 vehicles per year by 2031 but there is a long way to go for Rosenbauer.

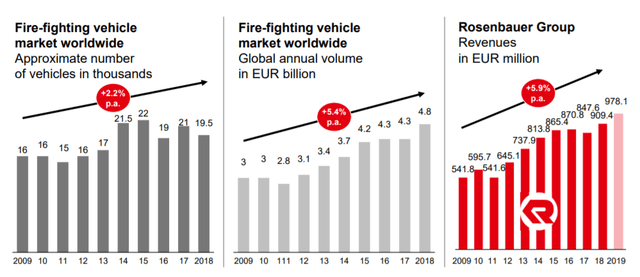

As Rosenbauer is operating in a very specific market it is good to look at the general market and how Rosenbauer has performed in comparison to that.

As you can see above the general market has just grown by 2.2% p.a. but revenue is growing by 5.4% p.a. which is indicating that the companies have quite a strong pricing power – definitely a positive. Rosenbauer has about the same growth rate as the fire-fighting vehicle market. Thus, the company is not the top performer but can keep up with the growth and profit from it. It holds about 16 % market share (in value) and 11% (in units).

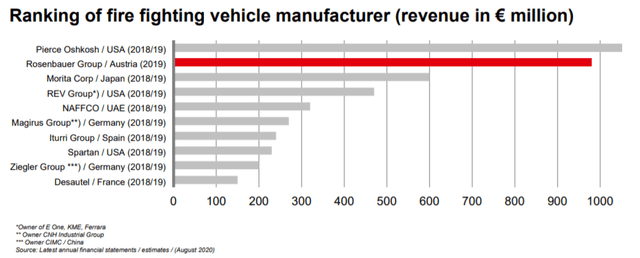

The other competition is mostly from the USA and Japan. The buyers are mainly public institutions. The Top-10-companies account for 70% of the whole market. As the world develops there might be more need for fire trucks due to urbanization etc.

RT stands for ‘revolutionary technology’ for Hybrid fire truck offering. With their claim to be a first mover in pioneering sustainable technologies, there could be further demand but as discussed above they plan to be able to produce significant numbers by 2031. Therefore, it is not a catalyst for the next few years and I don’t know whether fire trucks should be hybrid – it is not that they make many miles in a day.

The world fire service market follows the economic cycle with a delay of several months according to Rosenbauer. The demand has stabilized in Q3 2020. Full-year revenues are expected to exceed the previous year’s figure and for 2020 the sector is assumed to move sideways with a stable revenue of Rosenbauer.

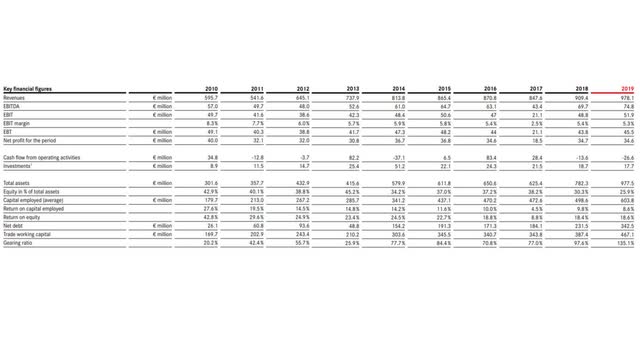

The revenue nearly doubled in the last 10 years which is a great but that is about it when it comes to good fundamental numbers. The EBIT-Margin decreased from a high of 8.3% to 5.3% which indicated high competition levels as most of the vehicles are always sold via tenders.

Investments per year doubled as well, which would be in line with the revenue growth, but other costs rose more which is the reason for the net income staying flat. What is really worrying, is the net debt. It increased from 26 million in 2010 to 342.5 million by 2019 which is a staggering twelve-fold increase.

This leads to a high interest rate risk. It is true can be borrowed cheaply these days as interests are low but for 2019 the company had to pay 6.7 million EUR in interest, about a fifth of net income. If we take a closer look the balance sheet, we can see that the company has 291 million in non-current liabilities and 140 in current interest-bearing liabilities and about 50 million in cash. That equals to around 7 EUR cash per share plus a dividend of about 2 % per year. The dividend was raised only in 2015 and afterwards decreased.

In 2019, the free cashflow was negative as well as in 2018. Potentially there are profits of about 34 million minus the interest payment (7 million) and the CAPEX (17 million) equals 10 million. Currently the company is paying 8.5 million in dividends. Hence, there is not much room to estimate a growing dividend.

Rosenberger stock investment outlook

The company has an interesting market as not many people will look at fire extinguishers vehicles. Rosenberger is the second largest company in this sector (revenue). The growth is estimated with around 5 % per year. The dividend is around 2 %. That is about it. Debt is growing like crazy; cash flows are negative and net income has been flat over the last 10 years.

For the Peter Lynch stock category, I would say Rosenberg is a slow grower and therefore avoid it. This company is a pass for me, and I am not going to follow it.

You have to see how it fits your portfolio and investment style.

If you enjoyed this analysis and would like to get notified when I write more such analyses, please subscribe to my newsletter.