Prepare For A Currency Collapse

Good day fellow investors,

in the news last Friday, we discussed the earnings of various companies and how a long-term investor should approach those, check the video out if you haven’t. As promised, today we will discuss the economic environment, the FED’s shift in gears and how one should think about long-term investing in relation to what might happen.

I’ll explain how:

- we are most probably going for a global currency collapse, that will happen sooner or later,

- the economy doesn’t have to collapse, and

- how stocks might better than other things.

Just before we start, I wish to thank you all for the great reviews on Amazon, we are in the company of greatness on the Amazon best seller list, with Nobel prize winners like Shiller, legendary investors like Lynch and great trading books like Market Wizards. I thank you all for your support.

The FED’s pause

Let’s start with the news, the last two weeks were filled with crucial news that is important to systematize and put it into context.

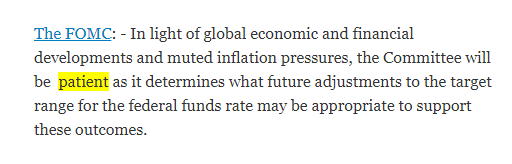

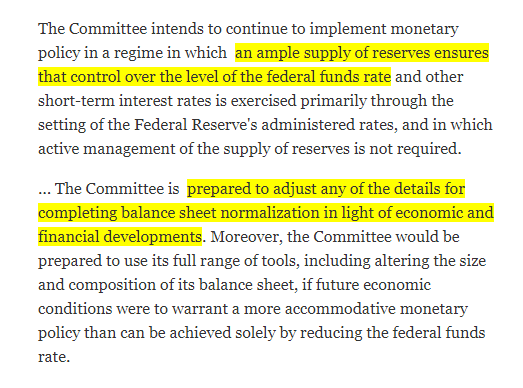

The key piece of information is the FED’s pause and change in rhetoric.

We can say the FED capitulated! The committee will be patient with rate hikes and adjust for whatever might happen.

Source: FOMC

Prior to the FED’s change in heart, there was this expectation that we are in for a global slowdown. After the FED changed its rhetoric, said they will pause to keep the economy up, stocks rallied after the bad end of the previous year.

So, a decline of 15% in the S&P 500 and a 100 basis points increase in the cost of borrowing for the US government, led the FED to stop with raising rates.

Source: FRED

However, the FED capitulating means that the economy isn’t doing good at all because it cannot sustain small hikes!

Source: FRED

It is simple, corporations are too leveraged. US corporate debt has almost doubled over the last 10 years. The situation is similar across the globe.

Source: FRED

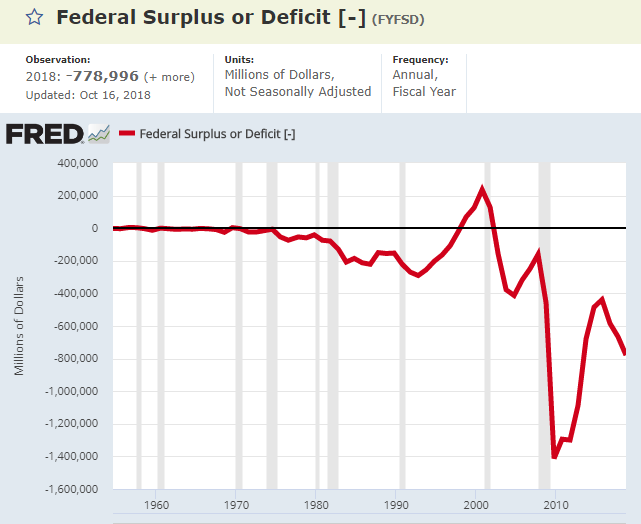

Governments are too leveraged. Budget deficits are piling all over the place.

Source: FRED

Same situation across most of the modern world.

Now, you can tighten interest rates, but that will increase the cost of borrowing for governments, that will consequently force them to borrow more as no politician is going to save money and not spend.

Given the FED, ECB, BOJ and others are ready to do whatever it takes to keep things as those are, the only thing they know how to do is to give more of the same medicine, thus more debt.

NOW, let me make this simple – Q4 2018 – people were selling because of the FED, the economic data was good!

Q1 2019, people are buying because of the FED, the economic data is not that good!

Source: Wolfstreet

Source: Reuters

Germany

Source: The Independent

My conclusion is that there will be no more tightening, no more normalization because, over the last 10 years, politicians and central banks have seen that interest rates can be low and they are now like junkies on low interest rates.

Source: Twitter

How to invest and what to expect

I am looking at the data, I look at the FED’s and the politicians’ behaviour and I am thinking;

1) There will be more money printing, much more

The last recession unveiled a tool that hadn’t been really used before, it unveiled the possibility to use central banks’ balance sheets to help the economy. Before 2009, Central banks’ balance sheets had been mostly flat. After 2009, an explosion of money printing is what followed.

Source: FRED

We have already seen that governments and corporations went on a borrowing spree to take advantage of the low rates. As it is normal with both governments and corporations, there is never the intention to pay back the debt, their only goal is to make money on the spread between what they are earning from the capital used and the interest rate they have to pay. For example, Apple can borrow at an interest rate of 3% on a 10 year bond, if they use that capital and make 5% on it, they make a lot of money. Debt repayment? Don’t joke, you might kill someone with unstoppable laughter.

With governments, it is even worse. US interest expenditures had been stable as interest rates had been declining and stood low. However, as the FED started tightening, US interest expenditures exploded and given the current budged deficit, higher rates would make the payments unbearable. The usual definition of a Ponzi scheme is when one has to borrow just to pay the interest on the debt.

If interest rates increase by just another 100 or 200 basis points (1 or 2%), the interest payments of the US governments would make most of the budget’s deficit and would force the government to borrow to pay interest expenses.

Source: FRED

What does this mean for the long-term? Well, the FED can control rates until a certain moment, at some point it all breaks down like a house of cards. Interest rates go up because who wants to lend money to a government or corporation that is borrowing just to pay the interest, inflation creeps in as people want to spend their money and the FED has to hike to stop the inflation while still printing to save the economy.

2) Be a debt owner, not a debt holder

Debt holders are the suckers, thus all diversified portfolios like my friend’s portfolio with an investment bank is, will see their values erode. Do you know that in the 1970s, bonds were called certificates of confiscation as inflation would eat up most of their yield?

Source: $13 Million Dollar Portfolio Analysis

Or, any other pension fund in the world will be in trouble too. While working in the Netherlands I did have a pension fund, ABP, where the top investments are government bonds, of course.

Source: ABP – Dutch pension fund

3) Stocks might do well

However, the situation gets tricky with stocks as those are businesses and businesses, the good ones can transfer price increases, i.e. inflation to customers. A good example is the Argentinian stock market. From February 2008 the Argentinian stock market increased 17 times.

And you thought the S&P 500 did well?!?

However, the Argentinian Peso did almost the opposite against the dollar.

So, prepare for a currency collapse down the road. It might happen tomorrow, it might happen in 2029. Whenever it happens, if you are not prepared, you are the sucker and you might lose it all.

4) The world will continue spinning

People often forget that the world will go on, the currency environment might be different but emails will still be sent. The cost might be different.

A good illustrative example is a normal postal stamp in Italy. The price in 1958 was 25 lire while in 1998 was 800 lire.

The current price is EUR 0.95, thus 2000 lire. So, over 60 years, the price of sending a letter in Italy increased 100 times.

The problem is that it will not be linear, it will be explosive so that will take many by surprise most. What to do? Well invest in great businesses, we will talk about one tomorrow, Disney, you can invest in commodities, we will talk about that on Monday with zinc, Glencore, Teck, Anglo American and you can make money on inflation, or at least stay protected as we discussed in the video on inflation this week.

My focus now is on businesses we can’t live without. That will give me protection over the long term, looking at margins of safety and healthy business returns.

If you enjoyed this video, please subscribe to my newsletter with a weekly content overview, that will give you the content you seek.