Porr AG stock analysis – VIE: POS (Cheap Value Turnaround)

Porr Ag stock analysis is part of my full, stock by stock analysis, of the Austrian Stock Market that offers interesting value opportunities like Porr is too. Check my Austrian Stocks List.

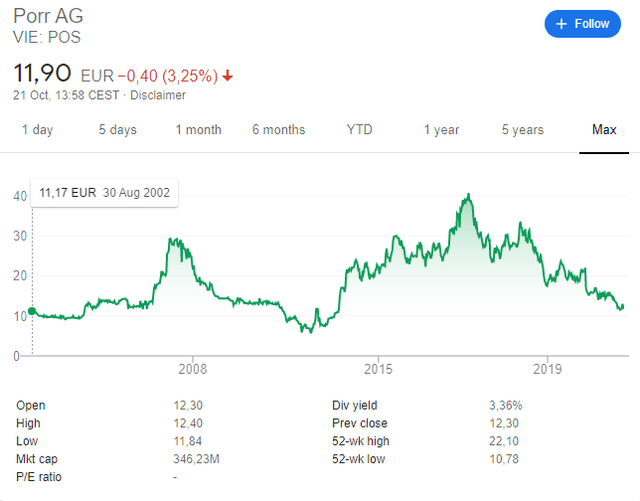

Porr stock overview

Since becoming public, Porr stock hasn’t really created value for shareholders except for the occasional dividends paid. Porr stock is trading at almost the same level it traded in 2002.

Porr stock has been very volatile, which is typical for stocks in a cyclical industry like construction. The construction business is very competitive and with tight margins, but as you can see above, at the right price a construction stock might be a good investment. Porr stocks is definitely not a stock to hold forever, but one to invest into the upturn in the cycle, a typical Peter Lynch cyclical stock.

During the 2007 global real estate boom Porr stock did good, then it had declined in consequence of the 2009 global financial and 2012 European crises, rebounded as low interest rates contributed to building activities in Europe and now it is significantly down again as the outlook on construction is not positive. However, compared to previous upturns, Porr stock can rebound 200% like it did in 2007 or even 300%like it did in 2017. Will Porr stock rebound again is the answer we have to find?

In this Porr stock analysis I’ll describe the business (you will not like it), but also analyze the investment fundamentals (that is likable with price to book at 0.5 and potential price to cash flow of just 3). So, don’t look away because of the ugliness of the business environment (exactly why the stock is cheap), but think of the investment opportunity and then see how it fits your portfolio. Porr stock analysis content:

- Porr business overview

- Porr stock fundamentals

- Porr dividend

- Porr investment conclusion

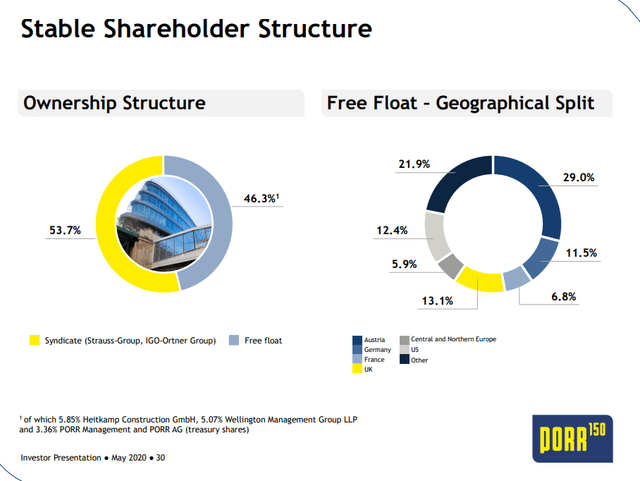

The Strauss Group acquired a controlling stake in 2012 when it increased its position from 6% to the 37%, later lowered due to the capital increases in 2013 and 2014. The capital increases added confidence into the stock, but it didn’t last long as the stock is back to where it was during the 2013 downs.

Let’s start with the analysis.

Porr AG business overview

Porr’s business is related to infrastructure and real estate construction. The current situation isn’t positive because given the COVID-19 impact, there might be a lot of vacant real estate but there could also be high government stimulus investments in infrastructure.

One problem with the above business model is that the project is handed to the lowest bidder which means you don’t have much room for excessive profits. If you want the business, you must take the lowest margin.

Consequently, we’ll see later in the fundamental analysis that cash flows are shaky.

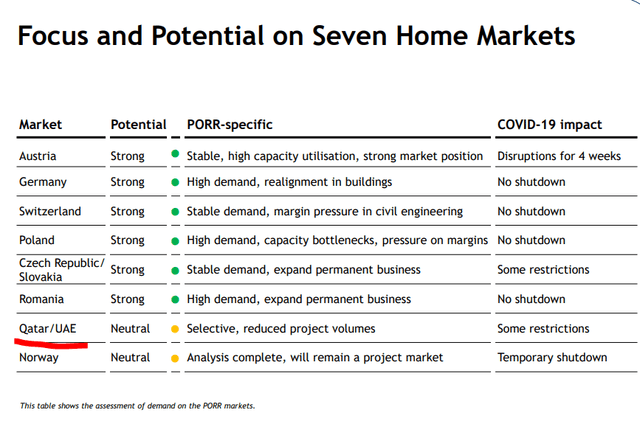

Porr Ag is focused on specific markets but these are highly competitive markets.

I must say that “Why Porr” simply doesn’t convince me. Its 7 focused markets are highly competitive and from what I follow the market (my stepfather works in the industry), it is a cut throat low profitability business. The best option you have is to make some money through M&A.

Further on long-term demand, demographics in Europe are terrible, so long-term isn’t positive. ‘Transformation’ and ‘digital’ are two words that were maybe fancy 20 years ago, when I hear them from a business, I usually prefer to steer away because the management is trying to sell me a story, not a business. But, at some stock price level, Porr stock will be and interesting investing value proposition. As the business is ugly, few will look at it and like it, which is where you might find great opportunities. So, let’s dig into the fundamentals.

Porr stock fundamentals

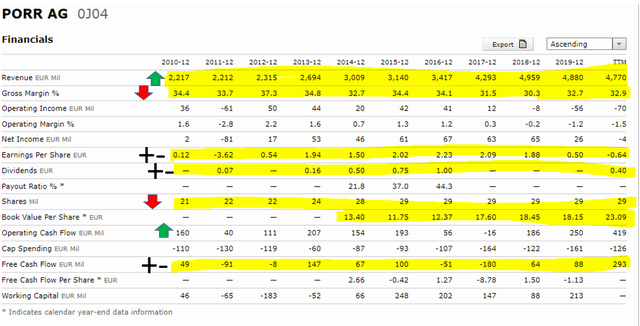

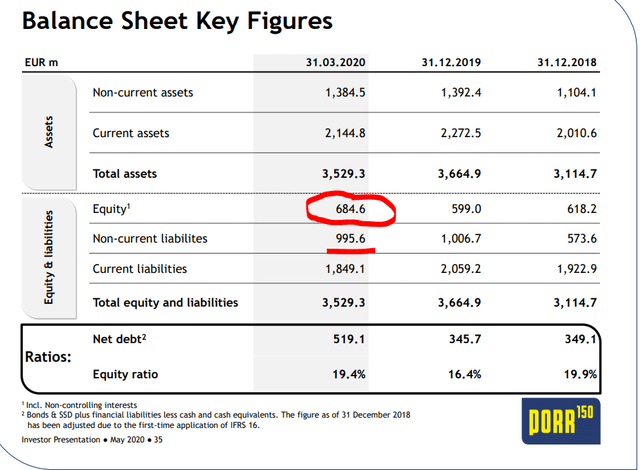

Over the last 10 years the company has doubled revenues, but also seen its margins decline. Thus, a positive and a negative. Earnings, dividends and cash flows have been extremely volatile. Book value has doubled over the last 5 years which is very interesting, but we have to see whether that is from acquisitions or from earnings (book value increases if you buy competitors trading at below book value)

Another issue for Porr is the debt. Debt to equity is just 19.4% which means that negative trends on the market can quickly erode your equity and your borrowing capacity but it is also good to mention an equity ratio between 20% and 25% is the norm in the industry given the business model.

Further, the company has 1.5 billion EUR in trade receivables and 1 billion in trade payables. This means they take on customer payment risk as they give longer payment terms to customers in order to gain more business, a very risky thing to do.

However, on the value side, the price to book value is just 0.5 which means that to replace what Porr owns from an accounting perspective, you would need to pay twice the current value. This could make the stock attractive for an acquisition or at least offer a margin of safety for investors.

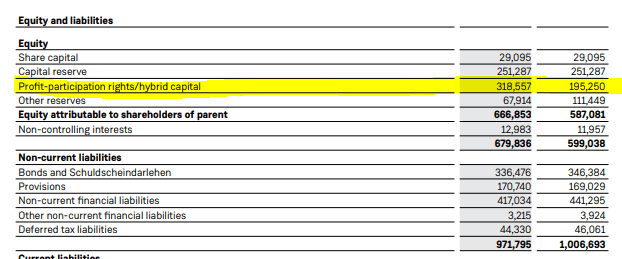

But, the book value has increased while earnings were negative, that is a very peculiar situation. The equity increased because of the profit participation rights or hybrid capital account.

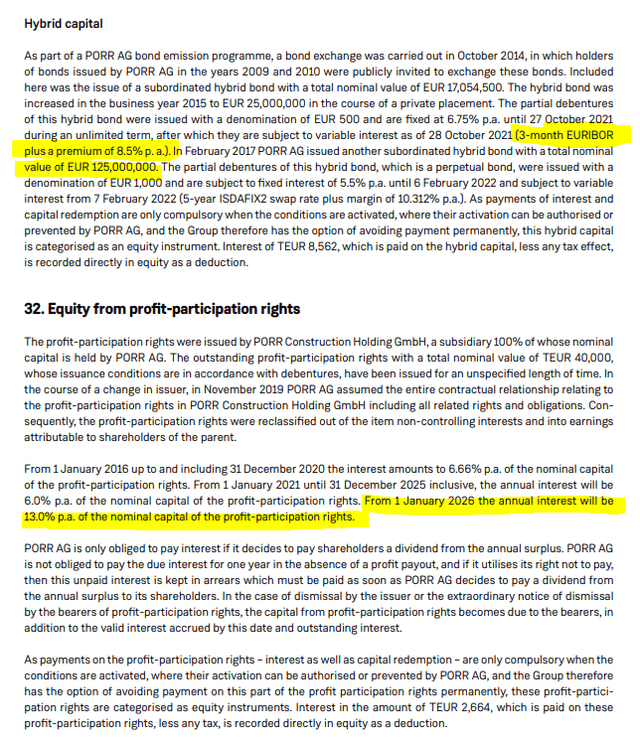

I’ve looked at the annual report, into the notes explaining the issue and what I have found is that it is not equity, yes accounted for as equity but not equity, it is a loan with a big fat interest rate on it of 8.5% and on one part of the hybrid capital even 13.5% from 2026 onward. It is considered as equity because the company doesn’t have to repay it back, but it is a loan and I think they will want to repay it given the interest rates.

So, the equity is actually half of what it is reported and the stock is trading at book value then. What an accounting colonoscopy! That is equal to issuing preferred shares but without there being a number of shares attached to that.

Porr dividend

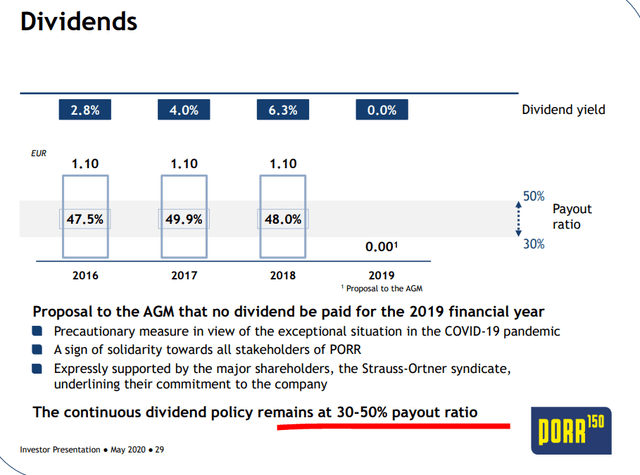

The only positive here, could be that, in a good year like it was the case in 2018, the company can earn 1.88 EUR per share and pay a 1.1 EUR dividend which would give a price to earnings ratio of around 6 and a dividend yield of 10%. If and when that happens again, the stock will minimally double if not even more.

Porr stock investment outlook

Porr stock will double only if the company survives till the next upturn comes. However, the situation is really ugly because if just a few customers default, the equity could be wiped out. And if you are in a situation where you promise 13.5% interest rates into perpetuity to get money that is not loan but is, so that your balance sheet looks better, you are in a pickle my friend.

I personally don’t like this kind of businesses despite the value there and the potential turnaround. You see how it fits your portfolio.

If you enjoyed this analysis and would like to get notified when I write more such analyses, please subscribe to my newsletter.