Mayr-Melnhof Stock Analysis – A Strong Business

Mayr-Melnhof Stock Analysis content

- Mayr-Melnhof stock price analysis

- Business overview and risks

- Fundamental analysis

- Q2 results

- Dividend

- Valuation

- Investment thesis

- Mayr-Melnhof Stock Analysis

This Mayr-Melnhof Stock Analysis is part of my stock by stock analysis of the Austrian Stock Market. Check the list out the Austrian stock market is one of the cheapest stock markets on the globe.

Mayr-Melnhof stock price analysis

Knowing that Mayr-Melnhof is in the paper and packaging industry you immediately know it is a cyclical. This is also showing in the stock price that has constant ups and downs. However, over the very long-term, since 2002 the stock has constantly been in an upward trend despite the 2009 global and 2012 European crises. A stock that keeps going up means the management is creating long-term value for shareholders which is a key indication of business quality and investability.

The stock is traded on the Vienna Stock Exchange with ticker MMK. There is also the Mayr-Melnhof Karton AG ADR traded in North America on OTC with ticker MNHFY.

The market capitalization is EUR 2.92 billion.

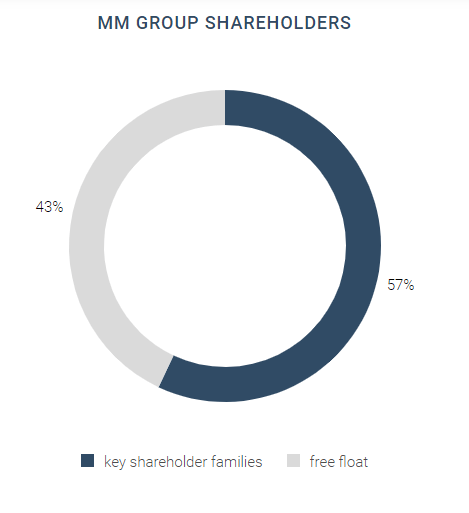

Mayr-Melhnhof Karton is mostly family owned (57%) which emphasizes its long-term value creating orientation.

Let’s discuss the business, fundamentals and then make an investing valuation.

Mayr-Melhnhof Karton AG business overview

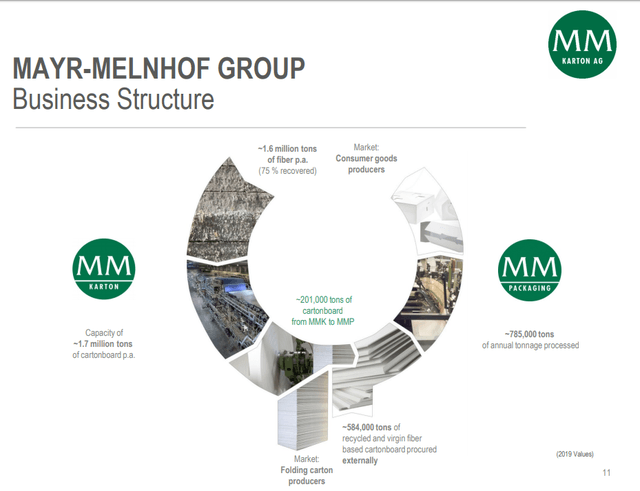

The paper and packaging sector is a highly competitive sector but a growth one for sure. Mayr-Melnhof is global leading producer of coated recycled fiber-based carton board and Europe largest folding carton producer.

It owns 52 production sites in 20 countries but its main market is Europe.

Europe isn’t really a growth market due to no population growth but thanks to scaling abilities leading to cost efficient production and technological improvements, Mayr-Melnhof manages to grow even in Europe. A company that sells the paper machines is Andritz, another Austrian company I have analysed here: Andritz stock analysis.

Where Mayr-Melnhof excelled is in packaging segment growth.

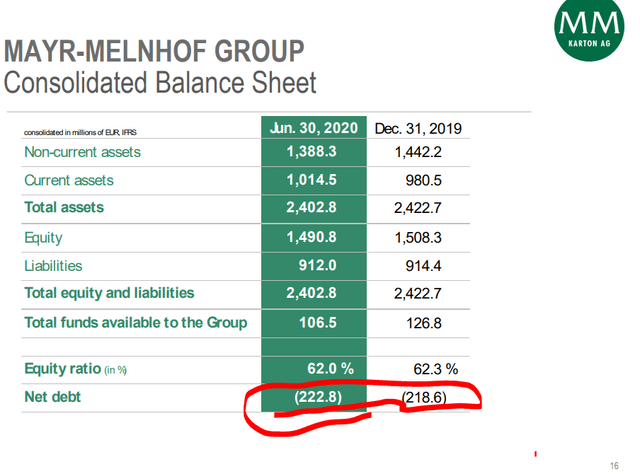

Given that the company is a financial fortress with no net debt, the main risks come from the business perspective.

Mayr-Melnhof key business risks

As the products are mainly used for the production of packages for consumer staples, that is also the main risk when it comes to investing in Mayr-Melnhof. I keep hearing how we should use other things to package products to be more sustainable but I see little actual change. Perhaps it is in us since we were kids that we love to open packages, even if there is no rationale behind it.

A package in a package, just for marketing purposes but that is how the world works

Another risk is that you can’t really have a moat in the business and the whole focus is on cutting costs. UPM, the Finland based competitor, is investing in Uruguay to grow production at the lowest cost possible given the close proximity of fibre. They are not direct competitors but there is actually no limit to supply growth which leads to cycles that can be ugly.

Given MMK’s stock price cycles, the competition didn’t really affect them for now but it is always a good thing to keep in mind.

They already expect lower earnings over 2020 as it is clear Europe is in a recession and there will be lower demand alongside lower carton prices. But, this will pass too so I’ll make a valuation based on a normal situation.

Let’s take a look at the fundamentals and try to identify the moat worthiness of MMK.

Mayr-Melnhof stock analysis – fundamentals

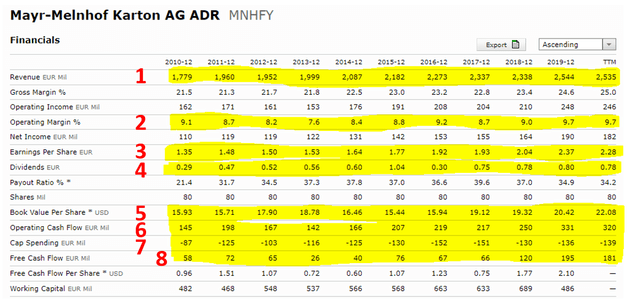

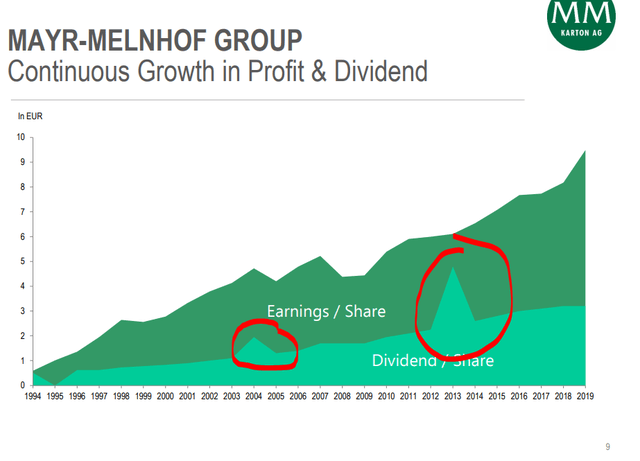

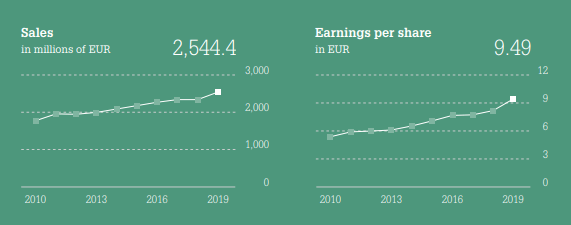

Revenues (1 in the below table) over the last 10 years have been growing slowly and steadily. The growth is nothing spectacular at just 3.6% per year, but sufficient for the significant stock price increase we have seen in the historical chart at the beginning of this article. Margins (2) have been surprisingly stable over the years which lead to slow and stable earnings (3) growth that allowed for a significant increase in dividends (4) from 0.29 cents to 0.80 cents per share. As the dividend increased almost 3 times over the past 10 years, that is exactly what the stock did from 2010 as it went from a level above 50 to the current 146.

Book value per share (5) has also been growing slowly, operating cash flows too and capital expenditures (7) that are an extremely significant factor in the industry, grew very slowly. The slow growth in capital expenditures allowed for a significant increase in free cash flows which consequently allowed also for the significant dividend growth.

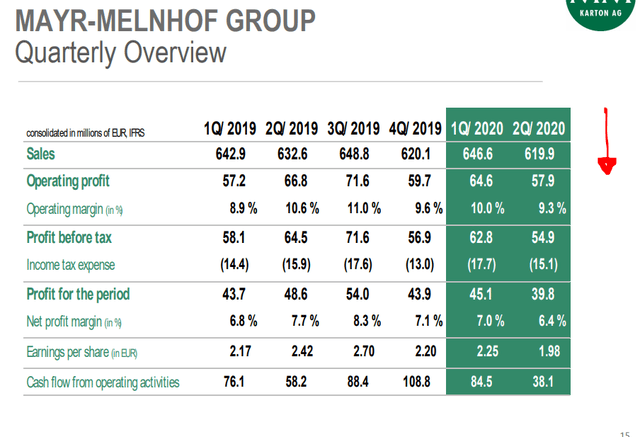

Mayr-Melnhof 1H 2020 results

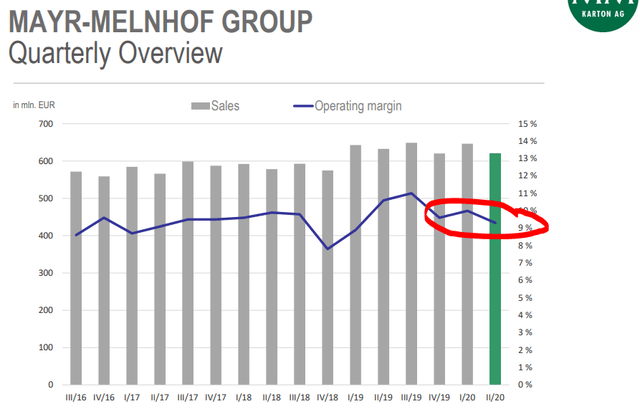

Results for the COVID-19 battered 1H of 2020 have been good as demands for carton didn’t fall that much but still lower prices and lower margins impacted results in Q2 2020.

They expect a recession going forward but that should pass too so I would expect stable results for a while and then a return to slow growth. I have heard already that activity is picking up in Europe so customers we’ll have to renew their inventories soon. It is likely that margins decline a bit which might impact earnings, but 2019 earnings were really record.

A common characteristic of greatly managed businesses is no debt. Mayr-Melnhof has negative net debt which shows that no risks are taken that could jeopardize the business position. Some companies pay out big dividends and take on too much debt but that fires back when the cycle turns which is something that happens often in the paper business.

Let’s take a look at the dividend and stock valuation.

Mayr-Melnhof Dividend

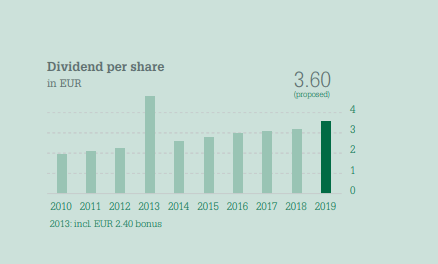

Given the relatively low dividend pay-out rate, we shouldn’t be worried about a dividend cut. What is also significant and shown below, are the bonus dividends paid in 2013 and 2004. That is always a good indicator on how the company, when with excess capital, is focused on rewarding shareholders. Plus, the dividend has been steadily increased over the past two decades which is another positive.

But, when it comes to investing, it always depends on the price you are paying. The dividend per share was 3.6 EUR in 2019 that gives a dividend of just 2.4%. it is likely the dividend will be increased in the future when things improve, but it is likely to be a long-wait before you see significant dividend income.

When it comes to valuing a business like this, at the end it mostly depends on what are the other investing opportunities you have. Mayr-Melnhof is and will most likely remain a great business with a great position in the industry that will keep paying dividends for a long time.

Mayr-Melnhof stock valuation

As we already said, the dividend yield is just 2.4%. The price to earnings ratio when using 2019 is 15.44 implying 6.47% earnings, or owner’s yield.

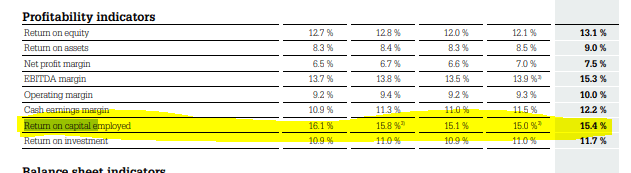

Alongside growth of a few percentage points per year, the expected return from investing in MMK now should be around 10% if they manage to keep growing and retain the high return on capital employed.

I would conclude by saying that there is nothing wrong with MMK stock, it is a really strong business offering good returns to investors. Given that it has no debt, it is a business you can own and sleep well at night but don’t expect miracles as the yield is low. But still, a return of 8% over the years quickly compounds to wealth over time. So, nothing wrong with MMK, see how it fits your portfolio.

For me personally it is a bit too expensive because I can find higher dividends alongside higher possible growth for similar or even lower risks.