RH Stock Analysis – Berkshire Owned Upscale Furniture With Luxury Financial Engineering

If you prefer watching, here is the RH STOCK ANALYSIS video, full article continues below:

RH STOCK ANALYSIS SUMMARY

- Over the past years the business was managed really well. Inventories declined while business expanded.

- Lower inventories and higher traffic and margins increased cash flows. Consequently, those were used to do buybacks. However, convertible debt was issued to triple down on buybacks.

- If you invest in RH, you must move fast, as fast as the CEO that recently sold $115 million worth of shares.

- The financial engineering makes RH more of a trade play based on buybacks rather than a long-term stable investment. It is an extremely cyclical business, a combination that often doesn’t do well with aggressive financial engineering.

RH, formerly Restoration Hardware, (NYSE: RH) is a stock in the Berkshire (BRK.A, BRK.B) portfolio which makes it an interesting research prospect. Further, the stock was hit hard due to the current situation as shops are closed.

Let’s investigate what is the investing risk and reward so that RH’s investment proposition can be compared to other options in the current relatively favorable investment environment for value investors.

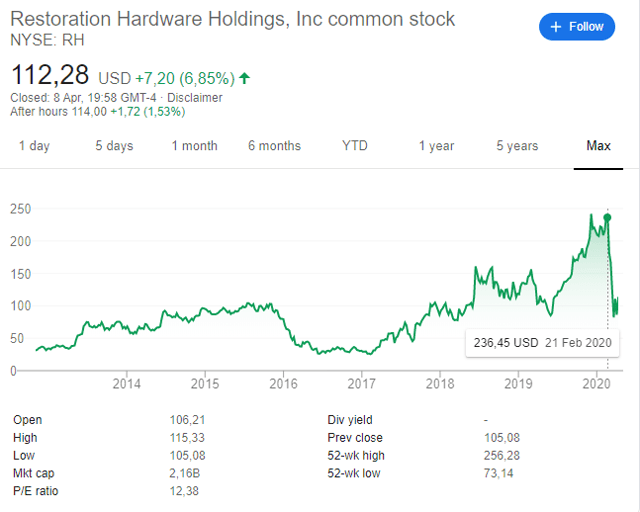

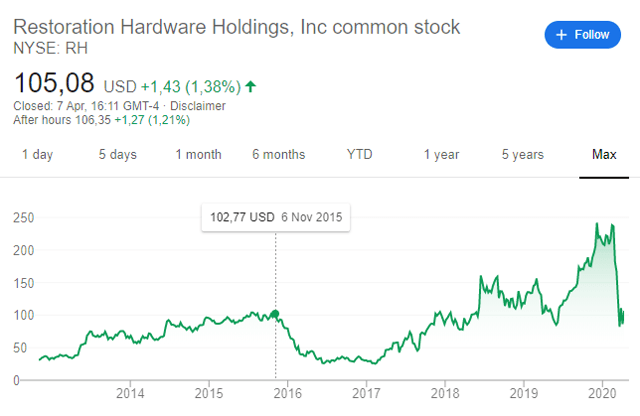

RH STOCK PRICE

RH stock analysis – the business model

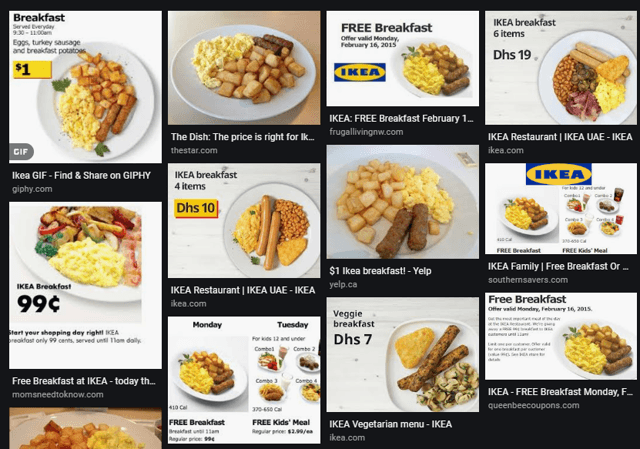

A business model that I really admire is IKEA. You are probably familiar with the Swedish, relatively cheap furniture brand, that has managed to scale globally and also get more than 15% of its revenue by selling food, even with $1 or free breakfasts.

The house we sold in the Netherlands was partly furnished through IKEA and a Dutch IKEA restaurant on a Saturday morning is a scene you better avoid seeing with large families, elderly couples all rushing towards the cheap breakfast. Mea culpa.

However, what if a similar concept can be created where the food is luxurious and the furniture too? You are not competing with IKEA, you have a scalable business model and people love to hang around great furniture. Well, that is the idea RH started developing a few years ago.

You can see the idea behind the business model in this video presenting the Chicago store:

IMPORTANT NOTE: don’t make the same mistake I did and discuss this business idea with your spouse as you won’t be buying any stock but most likely a $3,000 chair or sideboard. Then, when you buy the first item, you’ll likely become an RH member and redo your complete house. If that happens, you can say goodbye to your retirement savings, will have to work forever and forget about investing. Therefore, keep quiet about this investment idea at home and don’t go about testing the product thinking you bring your spouse out and do investing research.

RH is an American upscale (read: overpriced) furnishing business. Demand for furnishing products depends on discretionary purchasing power, real estate activity and thus the general situation in the economy. The general situation in the economy is currently not a great one, plus the shops are closed and therefore the stock got hit severely. However, investing is about the long-term outlook.

To create an outlook for RH’s business we have to estimate when will economic activity return to previous levels which is practically impossible to do. Therefore, it is better to look at fundamentals and see how long might RH be able to survive in different environments, can it take advantage of the situation by gaining market share and consequently what would be a fair price depending on various scenarios.

Restoration Hardware – The business – Source: RH

Restoration Hardware – The business – Source: RH

Restoration Hardware fundamental stock analysis

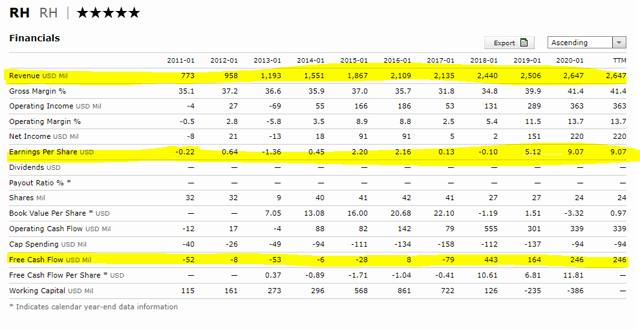

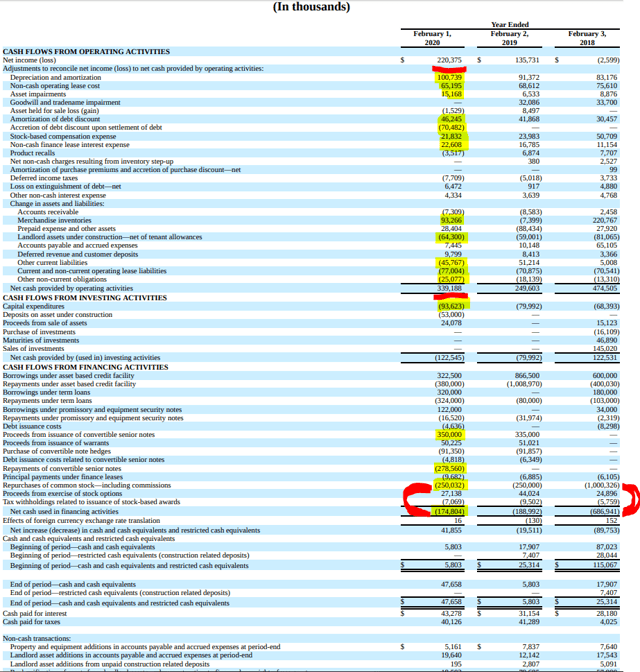

A look at fundamentals shows interesting things. Revenue has been growing fast over the last decade with earnings and free cash flows following. With a growth company it is important that earnings grow too because earnings and cash flow growth indicate the quality of the business model and its scalability. Margins are high, which is logical on upscale or ‘overpriced’ furniture. On a market cap of $1.66 billion and $2,6 billion in revenue, there is more room to scale.

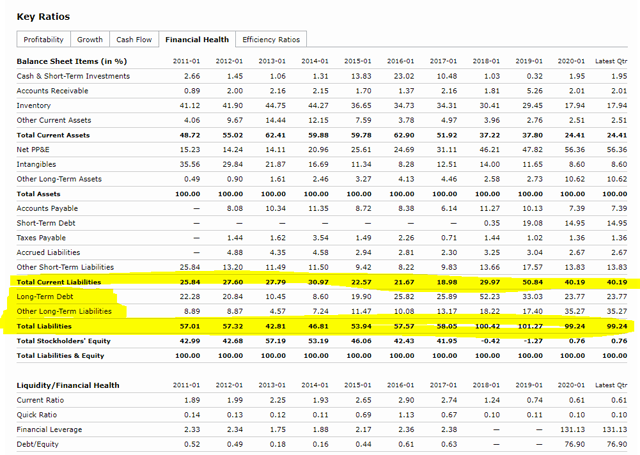

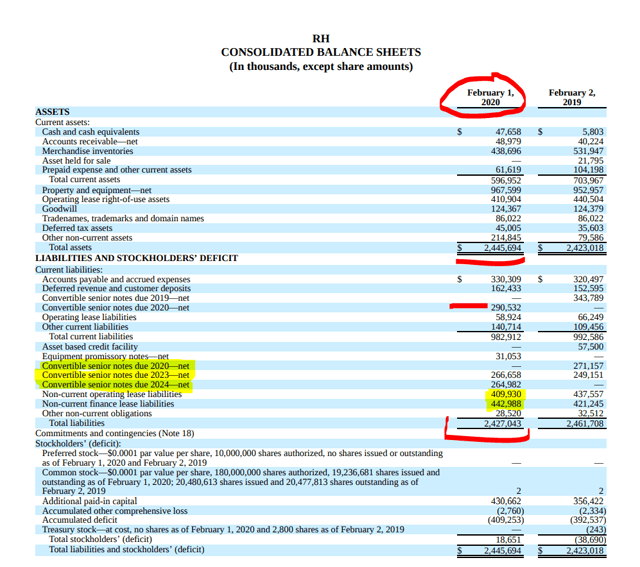

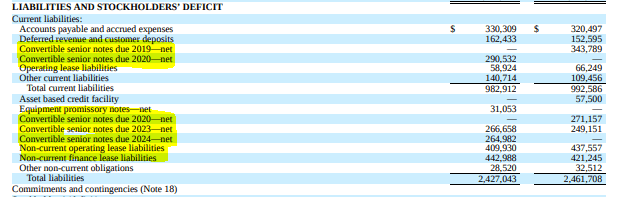

However, one part of the fundamental story is intriguing and has to be researched deeper. Liabilities are huge compared to the equity. This means that, no matter how wonderful the business might be, if there is a dry spell like the current situation definitely is, creditors might quickly want to take advantage and ownership.

There is practically no stockholder equity or, it is $18 million on 19 million shares outstanding. If we include the convertible notes and possible dilution, the number of stocks goes up to 24 million. On the other hand, there is more interesting information about sold warrants that are antidilutive etc. However, at current stock prices, nobody will convert, they will all want their money back or more even more dilutive shares. Even the 2020 bonds issued in 2015 have a strike price of $118 which is above the current level.

Source: RH investor relations

The book value simply isn’t there but the value of a business is the “discounted present value of all the cash flows the business is going to deliver from today till judgement day” to quote Buffett on this holding of his.

RH Stock Buybacks – Cash flows and remarkable financial engineering

The current market capitalization is $1.66 billion. In the last 3 years they have spent $1.5 billion in buybacks. In 2017, operating cash flows were $474 million, even if mostly thanks to depreciation and merchandise inventory. On top of that, they managed to spend one billion on buybacks in 2017 and lower the number of shares outstanding from 41 million to 27 million in just one year, a remarkable feat.

What they did over the last few years is the monetization of inventory that has brought $327 million, they have issued $685 million of convertible notes and made profits of $355 million. Sum that up and you come to $1.36 billion which is close to the $1.5 billion spent. For a company with cumulative earnings of $353 million over the last 3 years, to spend $1.5 billion on buybacks is a remarkable feat of financial engineering in my book.

Now are these guys smarter than the street or will the buybacks come back to haunt them in the future as it is usually the case with those that try to be smarter than the street? Think of Valiant (BHC), Boeing (BA) etc.

Improving inventory days and making the business leaner is what every manager should do and they really did a great job over the years. However, issuing convertible notes, buying expensive bond hedges and selling antidilutive warrants to buyback shares is something interesting. The good thing about the convertible bonds is that those are usually issued with a 0% coupon. So, the current cash flows are not burdened by the debt.

We have to see whether it is profitable to issue convertible stocks, buy bond hedges and issue antidilutive warrants and then buyback stocks. In what kind of scenario, it works and in what it doesn’t.

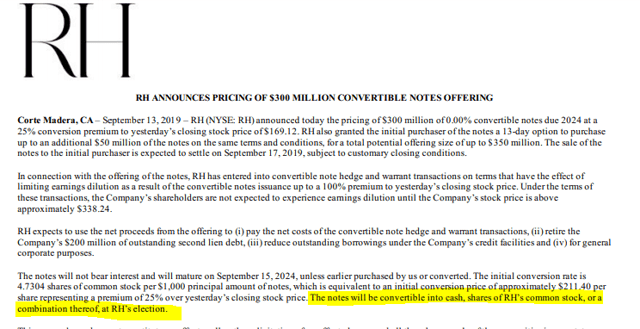

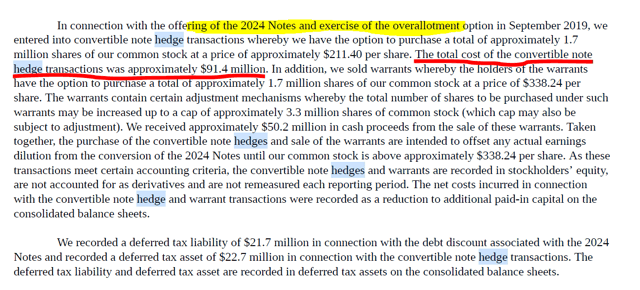

There is $290 million of convertible notes due this summer, another $266 and $266 million due in 2023 and 2024 respectively. It is important to note that the biggest risk from the bond is dilution as the bonds are convertible into cash, shares or a combination thereof, at RH’s election. This means creditors can’t come knocking on the door for cash – a good point. However, if RH doesn’t have the cash to repay, it might be highly dilutive as the company would have to issue shares at prices that would probably be lower than the buyback prices (even if most of the 2017 buybacks were made at a stock price of around $50).

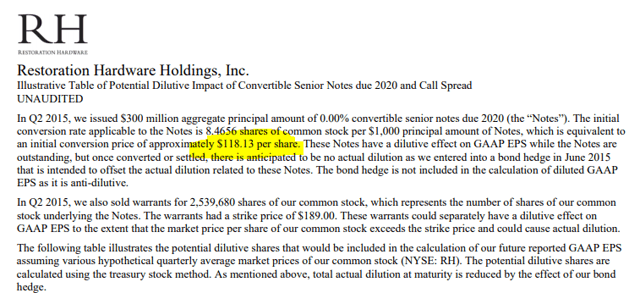

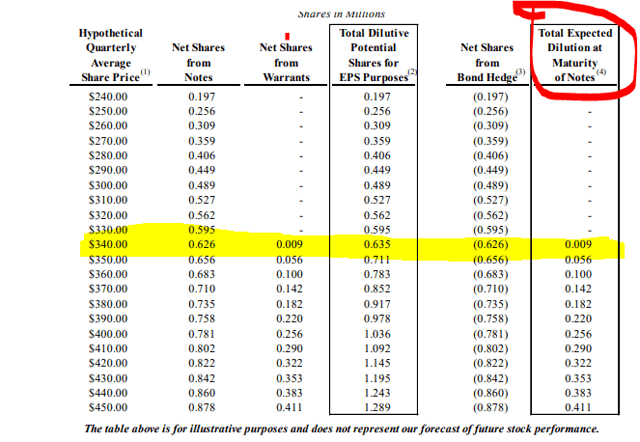

The 2024 notes have a conversion price of $211,4 with an expected dilution of 1,655,640 common stock shares at a conversion rate of 4.73 shares per $1,000.

To mitigate the effect of dilution, they have sold warrants for the above number of shares with a strike price of $338.4. A stock warrant gives the holder the right to buy shares at a certain price before the expiration. When a warrant is exercised, the company issues new shares, increasing the total number of shares outstanding.

However, to cover for the potential dilution between the strike price of the warrant $338.4 and the strike price of the bond of $211.4, the company entered into a bond hedge where it paid $91 million just to have that difference hedged.

Source: 10-K

It might be called a zero-coupon convertible bond, but paying $91 million to borrow $264 million as it is the case for the 2024 convertible bond, is a pretty high interest rate.

The company also paid $73 million to hedge the 2019 convertible bond, another $68 million for the 2020 note and probably a similar amount to hedge the 2023 bond. So, the company is happy to pay $91.4 million, to hedge for a potential dilution of 1.7 million shares as it is the case with the 2024 bond. On 19 million shares, the dilution would be 9%, or at current stock levels approximately $170 million. Thus, they are happy to pay half of that to prevent 9% dilution. Thus, actually paying 5% of the market cap to prevent a 9% dilution. Why would they go through such a hustle and why aren’t other companies doing the same? Well, there is a person whose incentive is just to push the stock price up, nothing else. Nothing wrong with that, but make sure you as the shareholders are on the same boat.

The CEO’s mega retirement package – reason for all the financial engineering

There must be something behind the above insane financial engineering. Even if the company lowered its share count from 41 million in 2017 to 19 million, the market capitalization, the actual value of the business, didn’t go up much, actually it declined.

In 2015, there were 41 million shares outstanding and the stock price was $100. The market capitalization was $4.1 billion.

Currently the market capitalization is $1.9 billion. Even a month ago, when the stock price was at $236, the market capitalization was still below the levels from 2015. If we compare the 2017 lows of $25 per share – the market capitalization was actually lower at $1 billion compared to the current one. However, free cash flows went from constantly negative numbers to about $250 million per year.

Given the above, one can argue whether there has been actual shareholder value creation. If you bought in 2015 and didn’t sell, you didn’t make much.

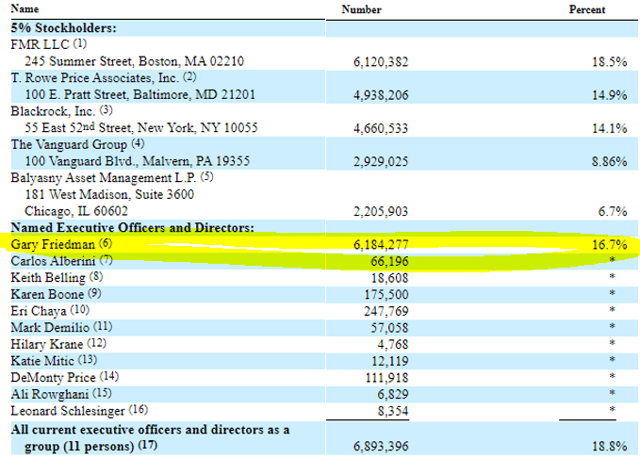

However, let’s take a look at why the CEO would do whatever it takes, do crazy financial engineering just to push the price higher. In 2017 the number of outstanding shares was 33 million and he owned 16.7% of the company. Mind that the number of shares outstanding in Q1 2016 was 40.6 million.

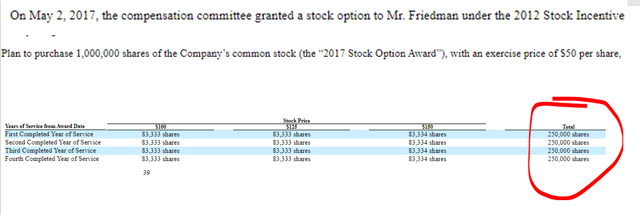

16.7% of a company worth $1 billion was $160 million but in 2017 the CEO was granted a stock option plan where he could get up to a million additional shares at an exercise price of $50.

RH stock CEO Source: RH proxy

If you get such an option plan, your only goal is to increase the stock price, at whatever cost. The option plan was granted on the 2nd of May 2017 and the company announced a $700 million buyback plan just 2 days later.

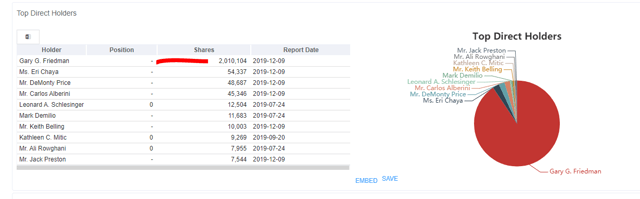

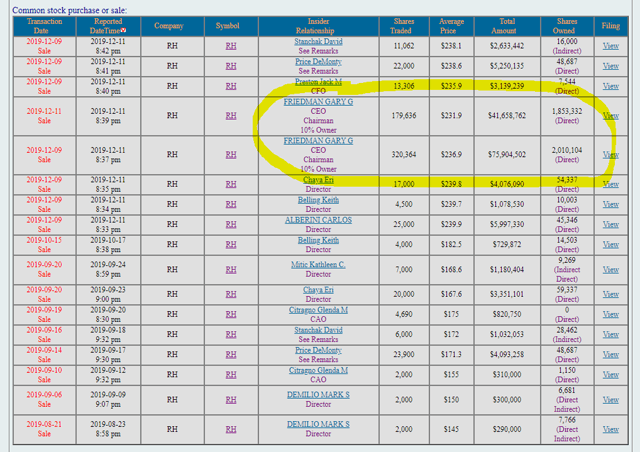

From the last reporting, the CEO has 2,010,104 shares – source: Gurufocus

So, over the period of just 3 years, the CEO went from 6 million shares to two million shares and actually sold shares worth $115 million dollars in December of 2019. It has probably been his plan to simply push the stock price as high as possible, cash out and retire. Few shareholders would complain when the stock price goes up. It is just that this crisis might have postponed the party a bit.

RH insider transactions – SEC form 4

Also, there were no reported purchases by the management over the above period.

Now, the CEO recently wrote a nice letter to shareholders explaining the current situation and how the company will deal with it.

Source: front page RH

My first thought was about finding the time to make such a nice picture in these times but I hope he took the picture prior to the crisis. The second thought was about his confident look, laser focused image with a blessed smile telling us everything is going to be great. Well, if you just sold 500,000 shares on the market at a price of above $230 per share and got $117.5 million from the sale, it is logical you feel blessed, happy, confident and secure about the future. I wonder whether other shareholders that have been holding the bag since 2015 feel the same?

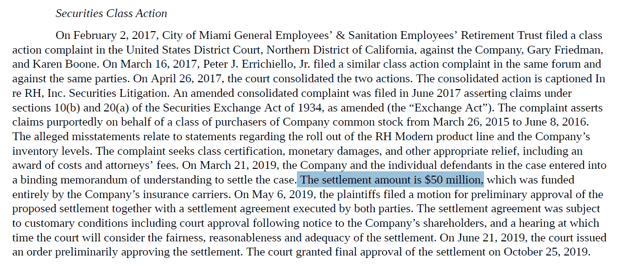

To remain on the topic of management integrity, something usually very important to Berkshire, if you read the annual report, you find other interesting things like the below class action complaint that was settled for $50 million.

RH stock investment proposition

RH is a business where the management’s priority is to push the stock up, even if just temporarily so that the management and probably other shareholders can cash out. If you want to invest, you have to be in that group.

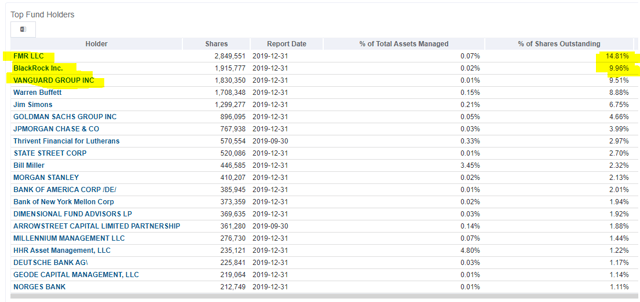

Index funds and small shareholders that like the buy and hold method are the bag holders. Fidelity, Blackrock and Vanguard are not investors that are going to sell when the stock goes up.

RH stock top fund holders – source: Gurufocus

Therefore, if you invest in RH, you have to move as fast as the CEO.

The business is of a cyclical nature, leaning towards the luxury side of things. This means that when there is plenty of money in the system, sales will be good and the investments in new stores will look smart. However, at any economic contraction, sales will suffer, stores will be empty and fundamentals will look terrible. At the moment, the only thing holding the business up are cash flows. In a bad year, or two bad years, that will always come as demand depends on the strength of the economy but also on consumer preferences, cash flows might turn negative. When cash flows turn negative, and eventually they will, perhaps already in 2020, the company will have to pay the full price of the financial engineering transactions from the past. A normal company, without this much financial engineering would have a buffer for bad times. RH doesn’t have it.

So, for an investment strategy, you have to watch the willingness Americans have to buy overpriced furniture, sorry, upscale furniture, and then try to estimate when will the company be able to borrow more and do more buybacks. The thing is that due to the small float and high short interest, they can push the stock up significantly without much money. Therefore, I would consider RH to be a speculative stock where you can make good money thanks to the company’s financial engineering. But, don’t forget, when you make you money you have to sell, RH doesn’t have a safety buffer for bad times. And, trust me, bad times always come.

From a business perspective, this company will make $200 million in legit profits and cash flows per year, perhaps $300 over the next decade alongside growth and thus at the current market cap, it gives a return of around 20%.

However, given the shop closures, and the fact that current liabilities amount to $982 million against $438 million of inventories they can’t sell at the moment, alongside $47.6 million in cash, tells me the only question here is whether RH will survive this crisis and if it survives how costly will it be for current shareholders. Dilution would revoke all the good that has been done with financial engineering over the past years. Well, except for those that sold.

If you enjoyed this kind of analysis, please consider checking my Stock Market Research Platform with more stock analyses.

If you with to learn how to do these kind of analyses, please join my FREE Stock Market Investing Course