Kapsch TrafficCom AG Stock Analysis – 10% Dividend And 3x Stock Potential

Kapsch TrafficCom stock is a small cap stock and is currently trading close to all-time lows. The reason for the decline is COVID-19 but also the fact that the company completed some highly profitable contracts while others were terminated. This contributed to a 17% revenue decline while the rest is due to COVID-19 for Q1 2020.

Kapsch TrafficCom Stock Details

Kapsch stock ticker: KTCG – traded in Vienna

Number of shares: 13,000,000 pcs

IPO: 2007

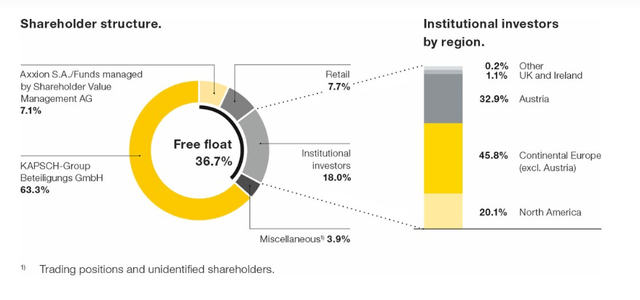

The market cap is 185 million EUR which categorizes Kapsch as a small cap stock. The company is family owned with 36% in free float and 63.3% of the shares are owned by KAPSCH-Group Beteiligungs GmbH.

Analysis content:

- Kapsch TrafficCom business overview

- Kapsch TrafficCom fundamental analysis

- Kapsch TrafficCom dividend

- Kapsch TrafficCom investment thesis

This Kapsch TrafficCom stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian stock market. Check the list out for more Austrian stock analyses:

The author: Sven Carlin, Ph.D. – I am passionate about stock market research because I believe a bottom up approach leads to finding the best long-term investments out there. My rule is to turn as many stones as I can to find the best ones. If you enjoy this analysis and approach, don’t forget to subscribe to my newsletter at the bottom of this article.

Kapsch TrafficCom AG business overview

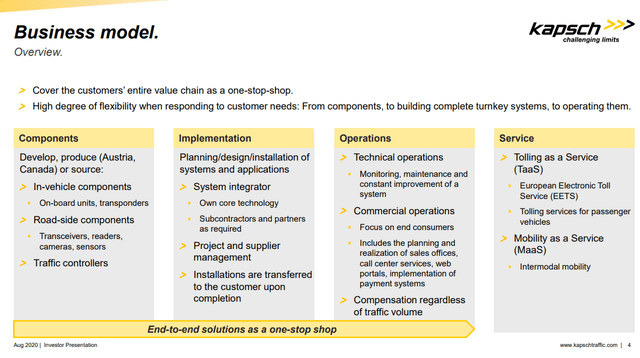

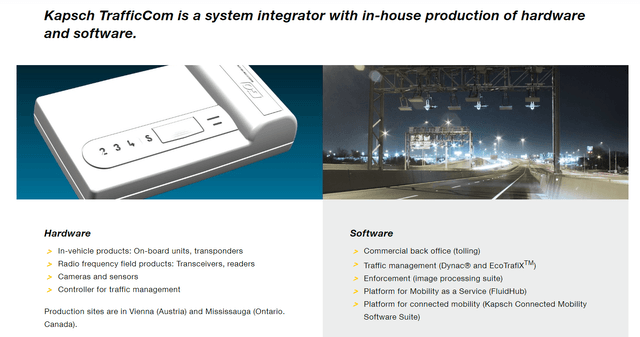

The business is one of offering services to the toll industry with turn key solutions. This is what they do:

This is what you might be familiar with:

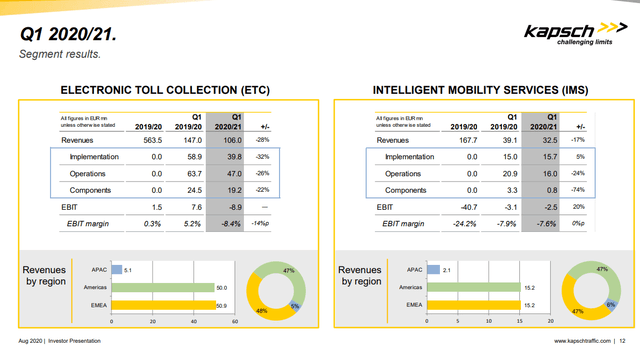

The two main business segments are Electronic toll collection and Intelligent mobility solutions.

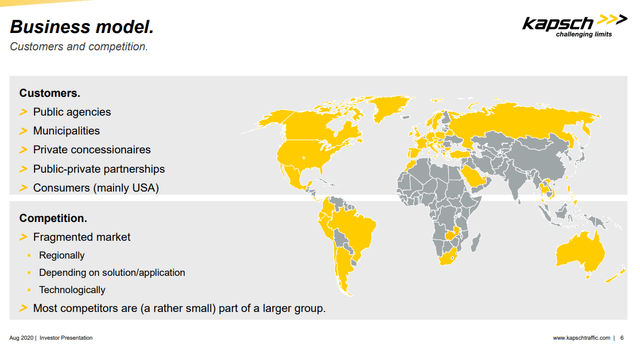

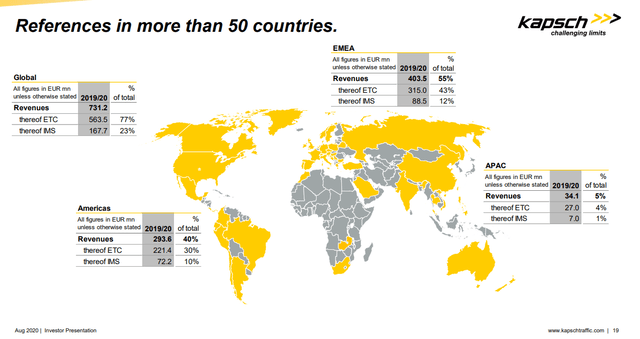

Their strategy is to focus on the growing need in traffic solutions and infrastructure growth due to global growth and development. The company is currently operating in more than 30 countries.

55% of revenues are from EMA, 40% from the Americas and 5% form APAC.

All in all, the business depends on new contracts for growth and on traffic business. In Q1 of the current fiscal year, what would be Q2 2020 for the calendar year, revenues declined 26% as some highly profitable contracts ended. Component sales have been much lower, operations and implementation too.

The company didn’t manage to lower costs and that led towards a loss.

We could expect, given the business, that it will return to normal and growth ahead when the economies return to normal and traffic comes back to pre COVID-19 levels.

This could be an interesting niche business, something similar to another growing Austrian business that operates in air traffic communication systems; Frequentis stock analysis.

Let’s look at the fundamentals for Kapsch TrafficCom in order to see whether the company can easily survive waiting for a return to normalcy.

As the business is often related to governments, it can get ugly. For example, a 400 million EUR contract in South Africa was recently terminated and the company is also suing Germany due to the cancellation of the implementation of the toll system for personal vehicles. The aim to get 230 million EUR but I don’t think they will get that much because that is more than the current market cap. However, there could be some value there too.

Kapsch TrafficCom fundamental analysis

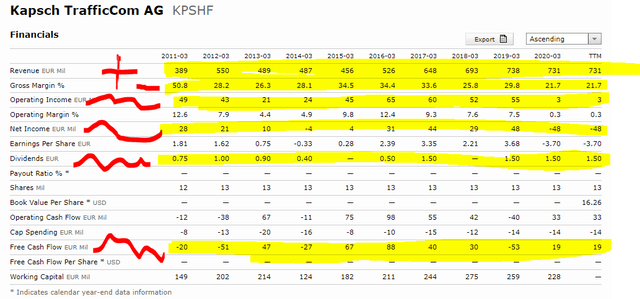

Kapsch TrafficCom managed to almost double revenues over the past 10 years. This shows how there are opportunities for even more growth and that the company operates in a sector with tailwinds.

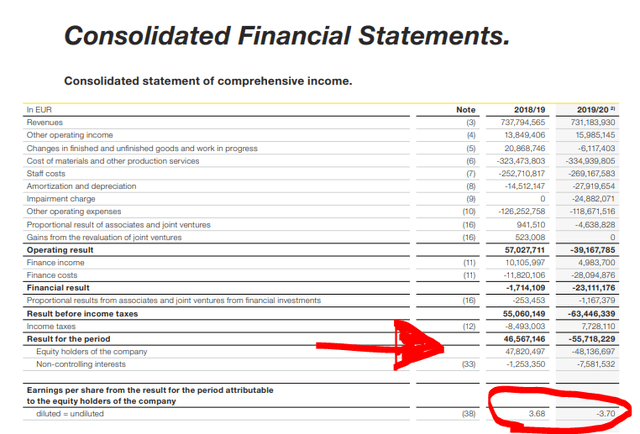

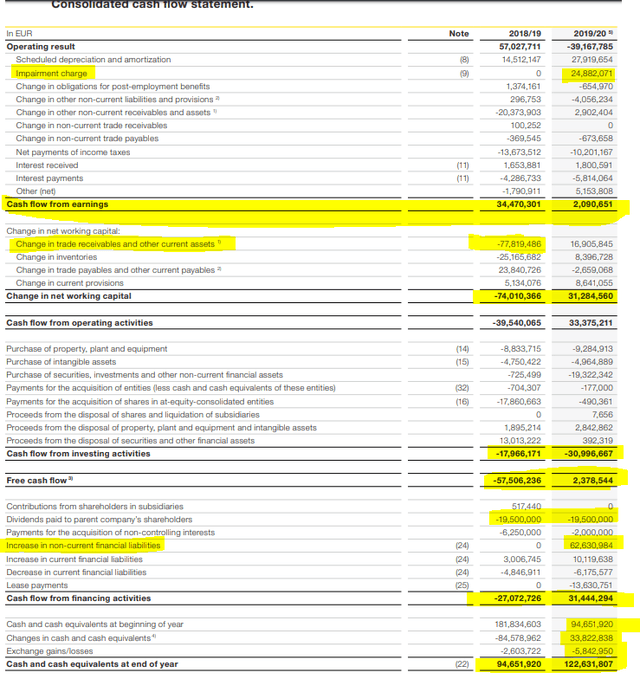

However, apart from revenue growth, everything else has been extremely volatile. Dividends have been on an off, albeit high when paid. Cash flows have also been volatile and often negative. What was earned in 2018, has been quickly lost in 2019.

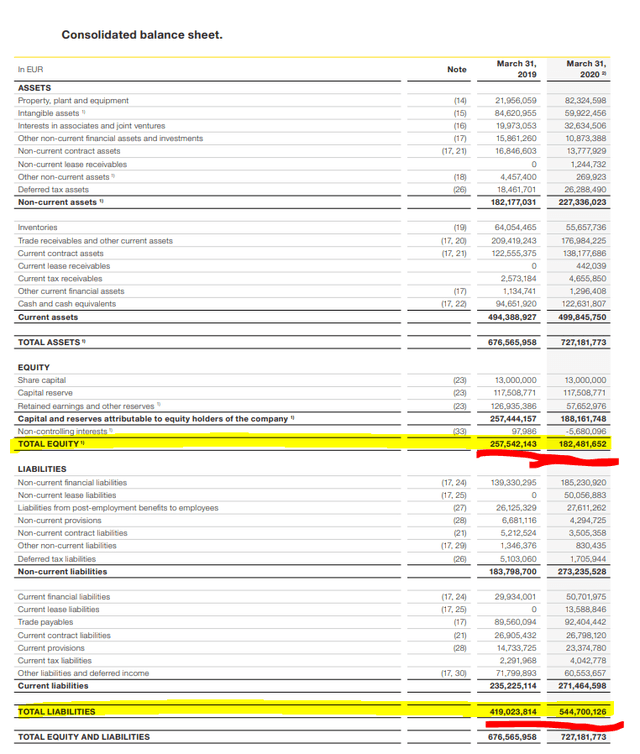

Also, finance costs have skyrocketed and a quarter of equity has been wiped out. In one year, equity went from 257 million EUR in 2018 to 182 million in 2019 while liabilities went from 419 to 544 million.

Most of the increase in liabilities comes from the new accounting rule that requires to account for leases as liabilities.

However, despite all of the above, cash has gone up and is at 122 million EUR. As investing is all about cash, Kapsch remains an interesting investment idea. Also, the price to book value is close to 1 which could give a margin of safety but also at a price to sales ratio of just 0.25, Kapsch could also become a takeover target if the family decides so.

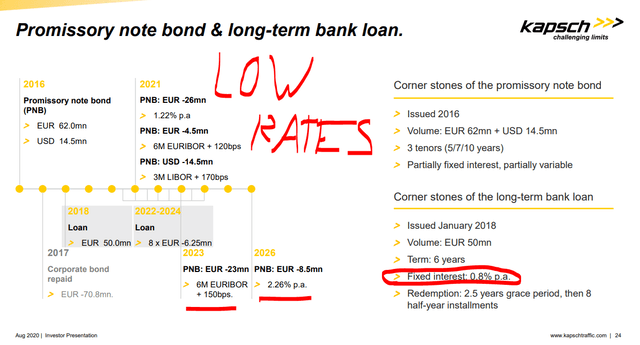

The debt gives it some risk but the interest rates are really low.

The cash on the balance sheet gives the possibility to pay 6 dividends of 19.5 million EUR which means it is likely the 1.5 EUR dividend will be reinstated in the future.

Kapsch TrafficCom dividend and investment thesis

The dividend had been 1.5 EUR per share over the last few years. They initially proposed a dividend of 0.25 EUR for this year but revoked it due to COVID-19. The thing is that on 700 million EUR in revenues, it shouldn’t be that hard to find 19.5 million to pay a 1.5 EUR dividend per share that would give a 10% dividend yield at current prices.

If the situation in the sector returns to normal, the stock price will likely go up too because I don’t see companies in Austria trading at a double-digit yield.

I’ll continue with my analysis of Austrian stocks and when I finish, I’ll pick 3 to follow closely. For now Kapsch TrafficCom stock is one that fits the criteria for me to cover it for long time because when the time comes that things start improving, the stock could easily triple if not more.