Frequentis stock is an interesting small cap niche growth player (Air Traffic Growth)

Frequentis Stock Overview – ETR: FQT, VIE: FQT

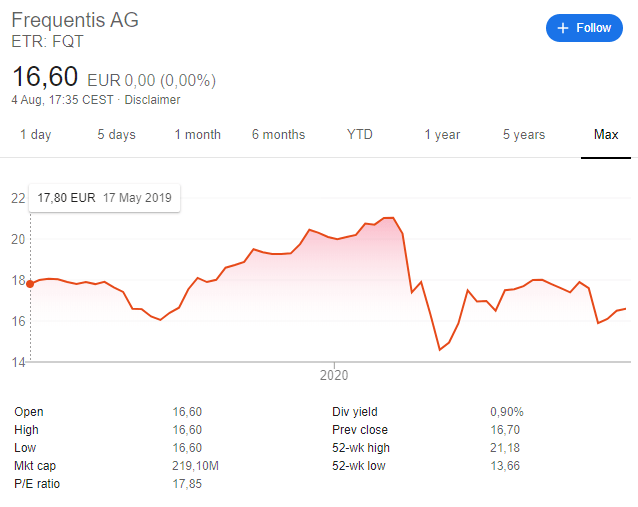

Frequentis stock has recently gone public with an IPO in 2019. The stock didn’t do much since but the low market capitalization of just 219 million EUR and interesting business in the communication sector make it an intriguing stock to watch.

The stock is owned by the Bardach family. In the IPO they cashed out as of the 3.1 million shares sold, 1.2 million were new shares and the rest was provided by Mr. Johannes Bardach (the “Selling Shareholder”).

I was recently discussing Austrian stocks in a video, the Vienna and Fraport airport stocks to be more specific, and a viewer commented how in the 1990s, the Vienna International Exchange was called the VIP – Vienna Insider Platform as it was mostly a place where insiders took advantage of clueless investors. A funny note, but something to be very careful of when it comes to investing in small cap stocks owned by one shareholder.

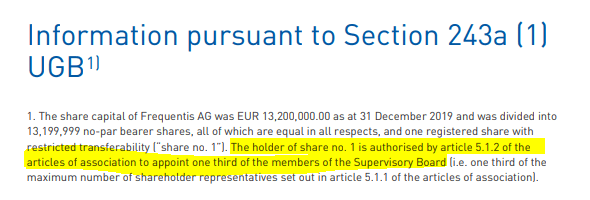

For example, the owner of the share no.1, out of 13.28 million shares outstanding, can appoint a third of the supervisory board.

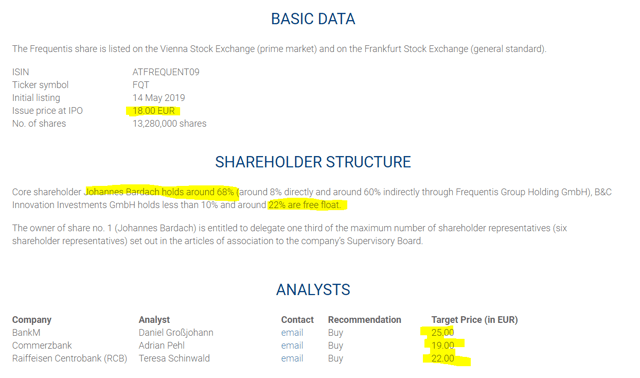

The following is the ownership structure and stock basic data:

The fact that Bardach owns 68% of the company and share no.1 doesn’t mean much but it is a thing to carefully watch over time. Analysts estimations for the stock are all positive with target prices up to 25 EUR that give a 50% upside.

Frequentis stock analysis content:

- Frequentis stock basic data

- Frequentis business overview

- Frequentis fundamental analysis

- Frequentis dividend

- Frequentis investment conclusion

This Frequentis stock analysis is part of my full analysis of the Austrian stock market, stock by stock, that you can find here:

I do a similar analysis for each company, following Buffett’s advice to start with the As when looking for investment opportunities. So, check all the analyses if you like such an approach.

Frequentis business overview

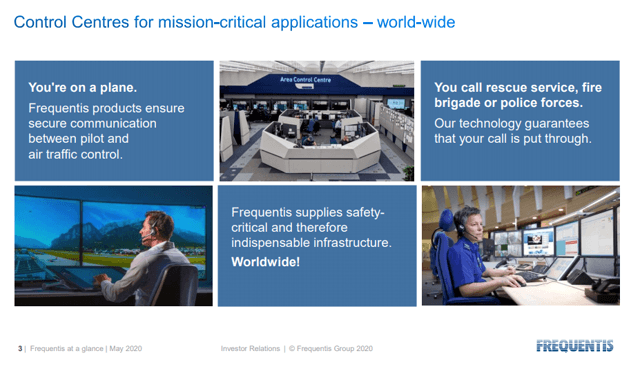

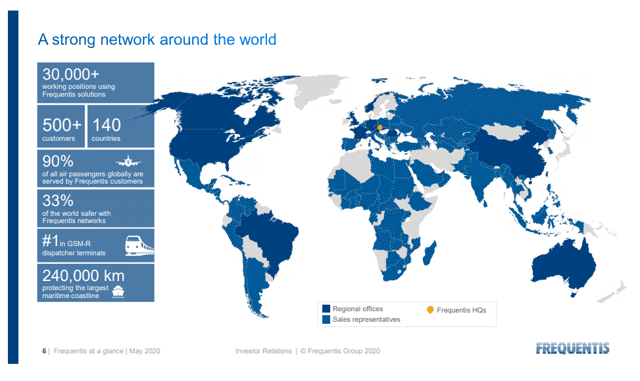

Frequentis has a very interesting business model focused on communication that requires a high degree of safety. Air Traffic Management (civil and military air traffic control, air defence) and Public Safety & Transport (the police, fire brigade, ambulance services, shipping, railways) are the main customers.

They have a very strong global network which is very important because they like to do small acquisitions and then scale the product globally. This is a very smart way of growing a business.

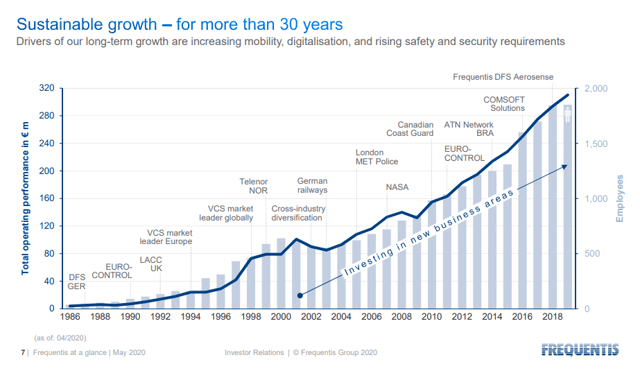

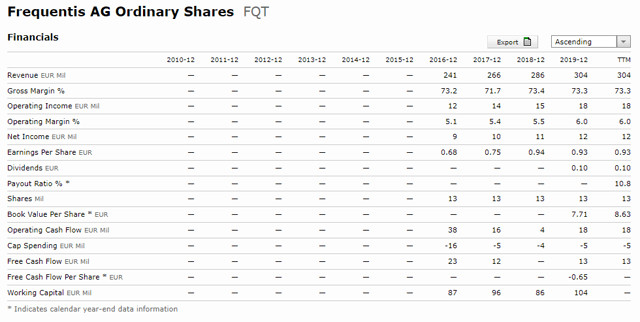

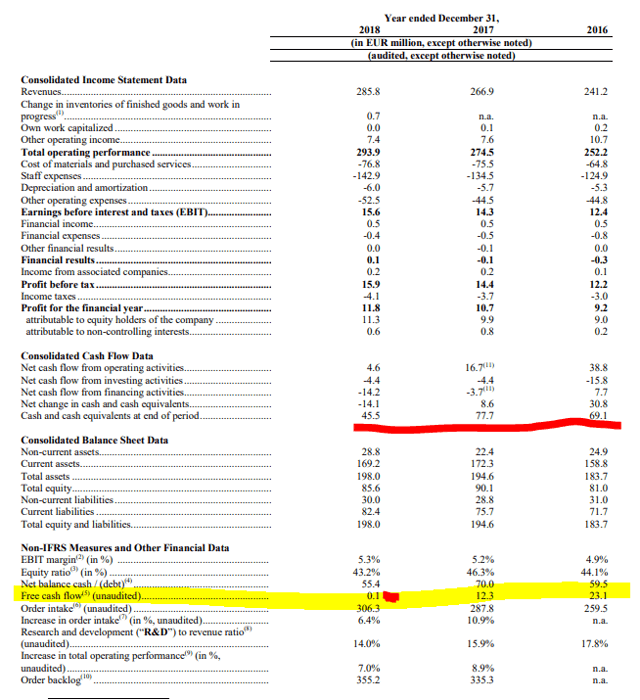

Through various investments in new business areas, the company managed to grow revenue from 80 million EUR in 2000 to the current 300 million. That is a stable growth rate of 7% per year.

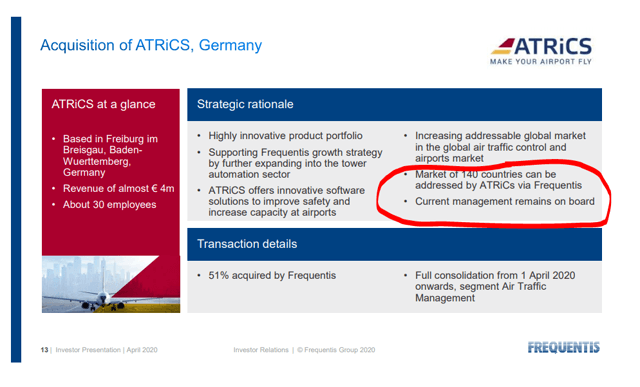

For example, Frequentis has recently acquired ATRiCS, which is a very small company with only 4 million in revenue, but if they can scale its product by selling it to their customers in 140 countries, it might be a very good acquisition. Plus, the fact that ATRiCS owners retained 49% of the company could indicate there is more value to be created there.

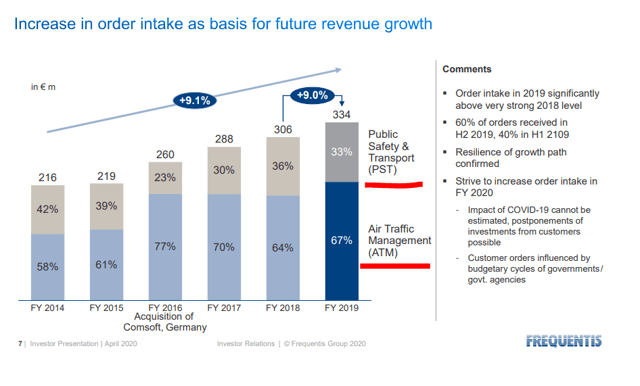

Two thirds of revenue come from air traffic management and the rest from public safety and transport.

The current situation is not that positive as there is little air traffic but they still expect to reach 210 million in revenue over 2020, secured revenue, and hopefully even more

Frequentis stock fundamental analysis

Frequentis is focused on slow and stable growth. Gross margins are high at 73% while operating margins are average at 6%. The biggest cost are personnel expenses that make 50% of revenue. This leads to net income of 12 million in 2019 giving a relatively high price to earnings ratio of 20. Not that bad for a business growing 7% per year, but also not that cheap.

Earnings per share amount to 0.93 EUR in 2019, likely to be a bit lower in 2020 but if the company can keep growing and servicing the air traffic and safety sectors; revenues, earnings and dividends might keep growing.

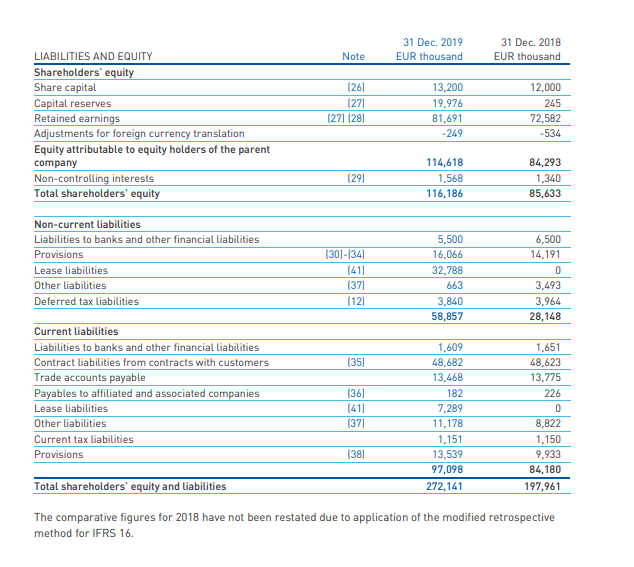

The company has 66 million of cash on the balance sheet, or 4.96 EUR per share while liabilities aren’t high. Frequentis has practically no long-term debt and most of the liabilities are lease liabilities and contract liabilities.

The absence of long-term debt and the retained earnings of 81.6 million EUR, plus the high cash position show how Frequentis is a good business where, with this first look, I would say this is a well run family business. Let’s look at the cash flows and dividends for more insight.

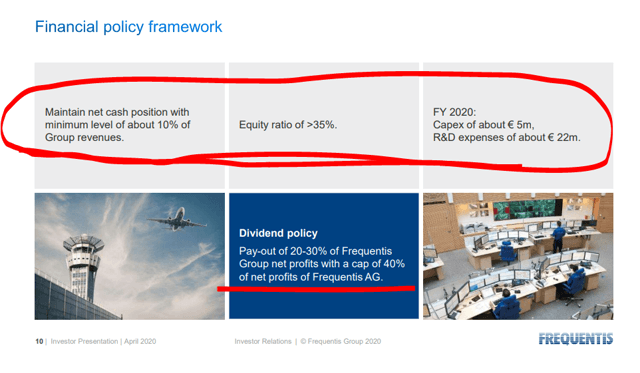

Frequentis dividend

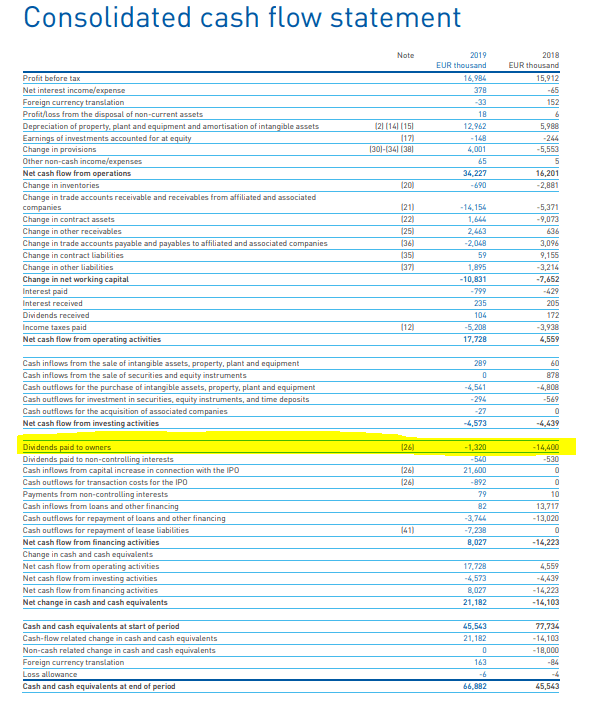

Before the IPO, the owners paid themselves a nice dividend of 14.4 million EUR which was more than 1 EUR per share. In 2019, the dividend was lowered to 0.1 EUR per share.

The 2019 positive net change in cash of 21 million EUR shows how the company has a much higher potential for dividend payments.

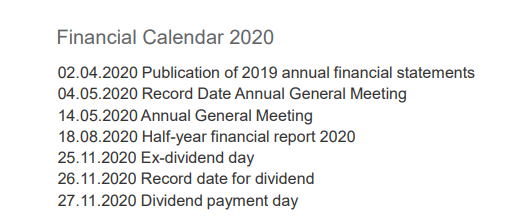

The dividend proposal for 2019 in of 0.15 EUR and will be paid in November of 2020.

In the past, free cash flows have constantly been high too.However, dividends have been more in line with the current dividend and not with the pre-IPO dividend of more than 1 EUR per share.

The dividend policy is pretty clear and gives room for higher dividends. Perhaps when this COVID situation and air traffic improve again.

If they pay out 30% of net profits, the dividend should already be closer to 0.3 EUR per share. So, there is further room for dividend growth alongside special dividends when the cash position allows it.

Frequentis stock investment conclusion

Frequentis stock is a small cap, which means there is a lot of potential for growth. Plus, the company is a good cash producer which means the dividend might be higher alongside growth ahead.

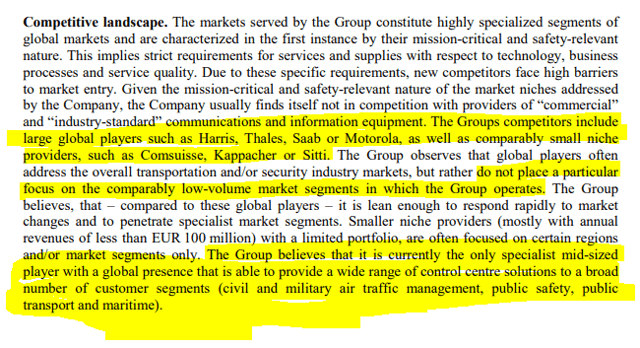

The company operates in a niche environment as I don’t know many that specialize in security communication. The main competitors are big companies that will not really bother with these small kinds of projects distributed across many customers globally. This represents a niche that also has high barriers to entry as once you installed your communication system, it is difficult that you will change it and all the upgrades will also be delivered from the same supplier.

The niche business above could also make it a take over target and also a reason why the company went public, to set it up for a better sale and full family cash out.

In case of a takeover, that would likely be at 12 to 15 EBITDA in this environment. With 2019 EBITDA at 30 million EUR, the value could be higher than 450 million giving more than 100% upside.

From a fundamental, cash focused investing perspective. Free cash flow is close to 15 million per year on average. This would give a cash flow yield of around 7% on a 1.12 EUR per share cash creation. If I add 7% future long-term growth, returns could be in the double digits from this small cap niche business stock.

I am personally very intrigued to put this business on my stocks to watch list within my Research Platform in order to take advantage of possible future opportunities. The stock is followed only by 3 analysts, the air industry is a growth industry despite the COVID outbreak and the company operates within a niche alongside some competitive advantages. I’ll likely first finish the Austrian stock market analysis and then make a decision.

I might even go to Vienna in September as they have often have a conference there but first, let’s see the half year results that come out on the 18th of August 2020.

For those interested in more air industry related stocks, here is my airport stocks list with detailed analyses.

Don’t forget to subscribe to my newsletter to get more such analyses directly in your inbox.