Cheniere LNG Stock Analysis – High Potential Returns (FCF kicking in > lower debt)

LNG Stock Analysis – Key factors:

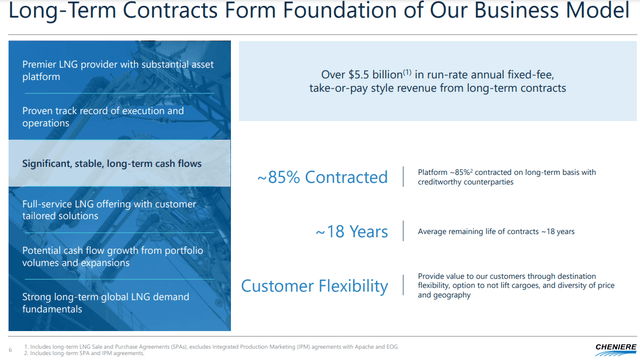

- Contracted business – predictable cash flows for 18 years

- Free cash flows finally kicking in by 2021 – lowering debt & increasing dividend in the mid late 2020s is the focus

- Risk – competition, natural gas prices, environment, trade issues with China (the key for LNG), high on the cost curve

- U.S. oil and natural gas shale outlook

Here is the video version for those that prefer watching or listening:

Cheniere Energy stock (LNG), with its stock ticker NYSE:LNG is all about natural gas and more precisely liquefied natural gas or LNG. A look at LNG’s stock price will immediately tell you the sector is volatile and cyclical.

Seth Klarman, one of the value investors I respect the most, founder of the Baupost Group, had Cheniere Energy make about 25% of his portfolio back in 2014. He sold the position off over the last few years, but now that the stock price is much lower, it is a great time to see whether there is still value within LNG stock. There is always a cycle within the sector, so one has to find the long-term average intrinsic value and then buy low and sell high, or value the likely dividends coming over the next two decades as the investments subdue and free cash flows are finally created.

LNG stock price analysis and ownership structure

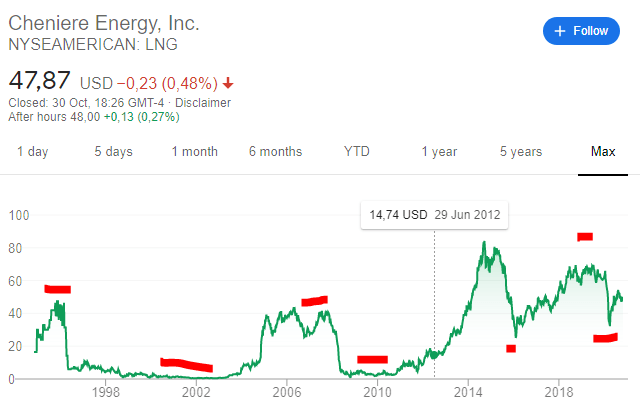

Cheniere’s stock price had some wild rides in the past, going up 40 times from 2010 to 2014, only to drop 70% in 2016, rebound and then drop again during the March 2020 Covid sell off. Important to note here is that Cheniere was an LNG importer prior to 2010, then switched to exporting as shale production turned the table in the sector. Many thought that it will go bankrupt after 2009 which is the reason for the low stock price around 2010. Few believed the export bet Cheniere was making.

However, Cheniere survived, is finishing with its investment cycle and might represent a good investment opportunity. I love highly volatile stocks in sectors with positive tailwinds because the positive long-term demand growth gives me a margin of safety and I can take advantage of the volatility.

The key is to see how strong are the fundamentals and whether it is possible to double down when other investors are selling in panic. Historically for LNG stock, buying low has been a good case and those that were greedy when others were fearful, or better to say, given LNG’s stock price chart above, in panic, have been well rewarded.

My goal with this LNG stock analysis is to better understand the LNG and natural gas markets, plus to get a good grasp of the risk and reward of investing in Cheniere.

LNG stock analysis content:

- LNG stock price overview

- LNG business overview

- LNG fundamentals

- LNG stock valuation

- LNG stock investment outlook – risk and reward

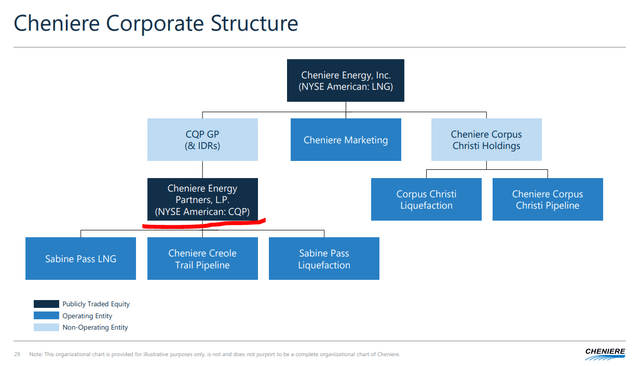

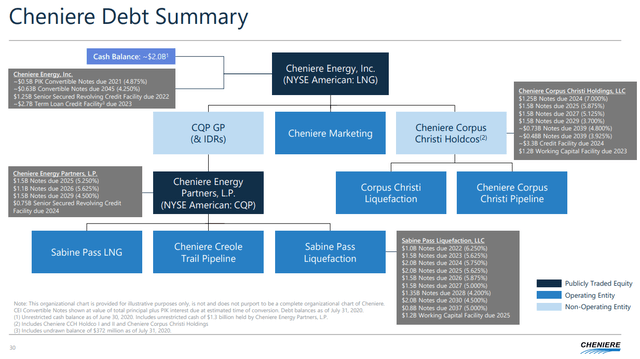

Cheniere ownership structure

The corporate structure regarding Cheniere complicates things a bit as things are not really straightforward.

Cheniere is listed as a corporation and owns 50.6% of Cheniere Energy Partners which is a limited partnership where 49.4% is owned by the Blackstone Group.

Cheniere stock – NYSE: LNG

Cheniere Energy Partners L.P. – NYSE: CQP

The most important thing is that CQP owns 100% of Sabine Pass so that value has to be halved if you own LNG stock or you can own only CQP.

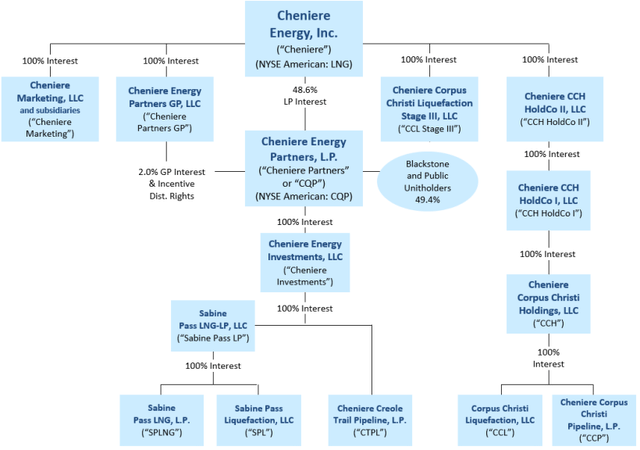

Blackstone has agreed to sell an estimated 42% stake in Cheniere Energy Partners to its own infrastructure affiliate (Blackstone Infrastructure Partners) and Brookfield Infrastructure Partners for $7 billion, in line with the market capitalization as it is just a related party transaction.

Perhaps the easiest way to understand the separation between the above, LNG has a market capitalization of $12 billion which includes 50% of Sabine Pass and 100% of Corpus Christi. Cheniere Energy Partners L.P. has a market capitalization of $17 billion which should be a result of different taxations and due to the distribution, the market loves dividends, no matter how irrational it might be. CQP’s dividend yield is 7.5% while LNG stock doesn’t pay a dividend.

Cheniere Energy business overview

Cheniere is a natural gas liquefier from the US.

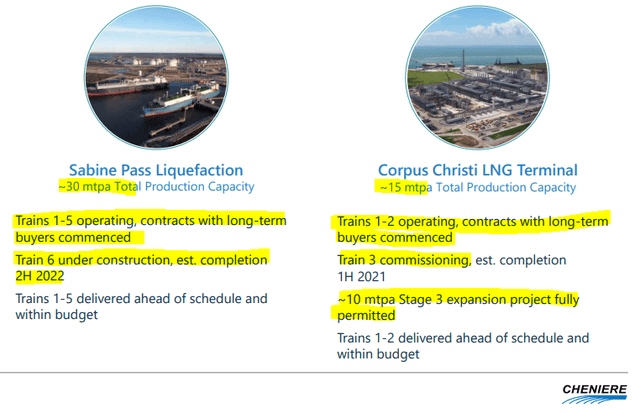

LNG’s two facilities are in Texas; Sabine Pass and Corpus Christi. Current capacity is 45 mtpa while new trains should bring it up to 60 mtpa and then possibly 70 mtpa by 2025.

The foundation of Cheniere’s business model are long-term contracts where the average remaining contract life is 18 years and 85% of capacity is contracted. In 2020, 95% of its capacity has been presold. However, for the recent Train 3 at Corpus, over two-thirds of the contracted liquefaction capacity was sold to unrated off takers (Trafigura, a trading house, and PetroChina, a division of the state owned Chinese National Petroleum Corporation).

Cheniere is a toll business, has little commodity risk and all the contracts say is that it will process the natural gas into liquefied natural gas. However, it has contract risk (no issues till now), procurement risk and operating risks.

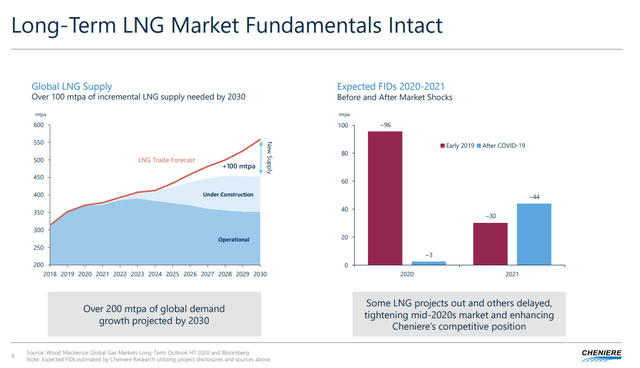

Cheniere’s main investment thesis is twofold; 1) higher LNG demand from mostly Asian countries, as those countries develop globally, 2) in addition to a supply issue for LNG as there are not enough projects being constructed to liquefy natural gas (this can change by 2025 but it is interesting to follow). Cheniere expects demand for liquefied natural gas to grow by 200 mtpa by 2030 which is 25% of current demand.

However, I am always extremely wary of such projections because those are often wrong. With low interest rates and knowing that there is a supply gap coming in 5 years, there will possibly be many thinking about building new LNG projects that might keep supply and demand in balance.

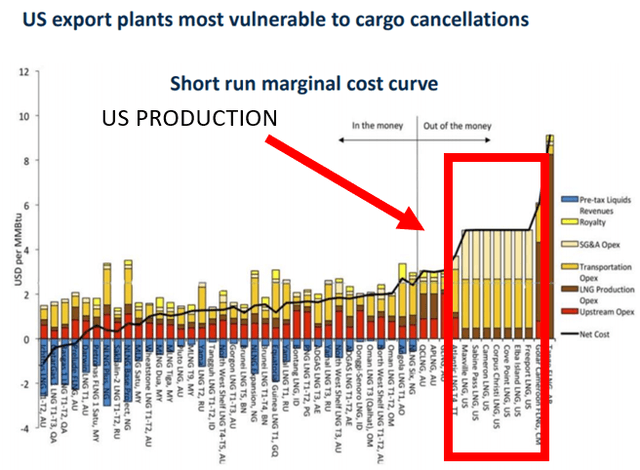

Plus, Cheniere depends on US natural gas production and low prices because US LNG is at a disadvantage from Qatar natural gas from both a cost and geographical perspective as the main demand comes from China and Japan. With the current hit to shale oil, the time of cheap gas in the US might also be over which is another thing to look into.

Further, there are many projects coming online that might eat into Cheniere’s future profitability. (RDS stock analysis)

Not all projects are permitted in the US, but the number is significant and analysts expect a second wave of projects coming from 2022 to 2025 that should double US LNG supply.

One thing that one has to take into account is the high relative costs US LNG supply has.

Any structural changes in the market, cancellations of long-term international contracts or contracts not being renewed, could have an impact on LNG stock valuation. Let’s take first a look at fundamentals and then jump to the valuation and investment thesis.

LNG stock financials and fundamentals

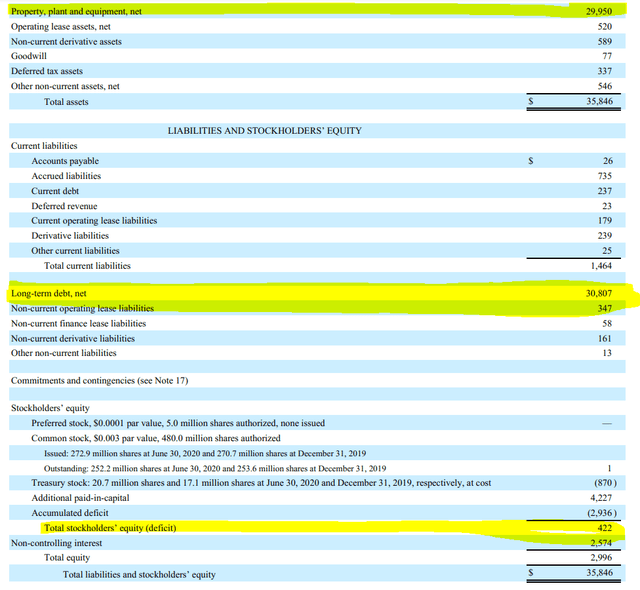

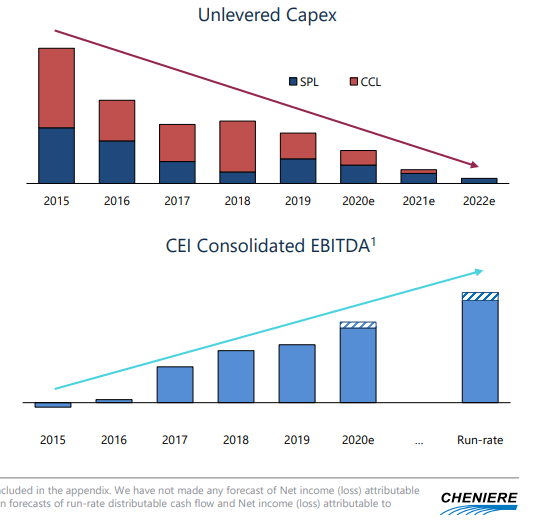

Cheniere has been significantly investing to develop and build all the 9 trains, create the surrounding infrastructure which has been mostly financed with debt. On the balance sheet, there is $31 billion in debt and $30 billion in property plant and equipment. This leads to the equity being just $400 million but you must take into account Cheniere’s business model.

High upfront capital investments lead to negative cash flows in the initial build-up phase that should consequently turn into high free cash flows when the growth cycle is completed. The key to watch are the coming cash flows and how might Cheniere deal with the humongous pile of debt.

Average interest rates on that debt are around 5.5% which leads to yearly interest costs of $1.7 billion per year. We have to deduct those from operating cash flows when making a valuation.

The high interest payments weigh significantly on the income statement and are the reason why when the company passes the free cash flow inflection point, the focus will be on lowering debt.

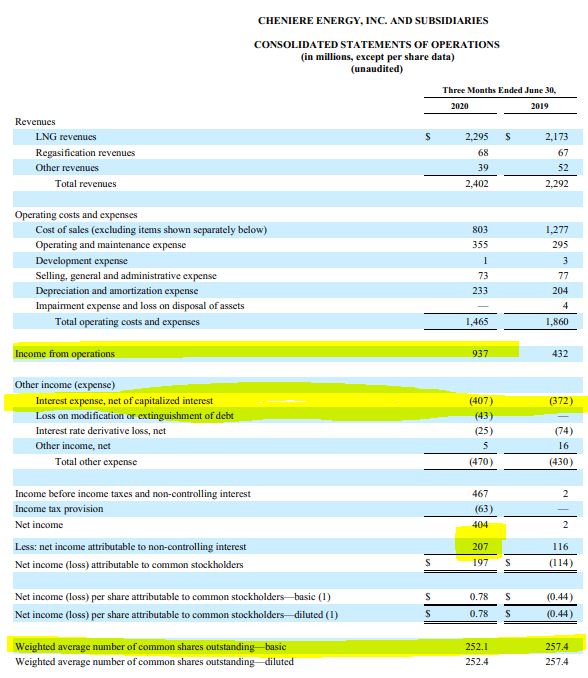

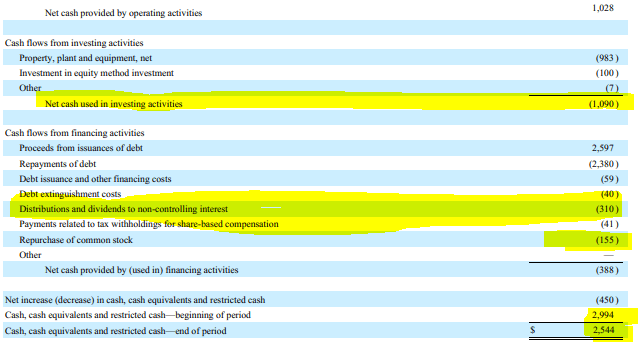

Operating cash flows in the last quarter were around $1 billion, with extreme high capex requirements that have led to a negative cash flow for the quarter but when the $983 million of capital investments subdue, we could see good positive cash flows coming from Cheniere.

Let’s put this, alongside the coming growth, into a valuation perspective.

LNG stock valuation

LNG stock is relatively easy to value given the fixed contracts and capacity. From the above I have current operating cash flows at $1 billion for Q2, when capacity grows to 60 mtpa that should be happening in 2023, I should be at $1.33 billion per quarter or $5.3 in operating cash flows per year.

From the $5.3 billion, now expected to be $5.6 billion as the company achieves operational improvements and growth, we have to deduct $1.7 billion of interest payments, which leaves us with $3.9 billion of free cash flows per year. I see depreciation and amortization at around $250 million per quarter or $1 billion per year so there will also be a 19% tax on the remaining difference of $2.9 billion which should be $550 million (haven’t checked the taxation on the limited partnership). Deduct $0.3 for sustaining capital investments, we are at $3.1 billion of run-rate free cash flows from 2023 onward.

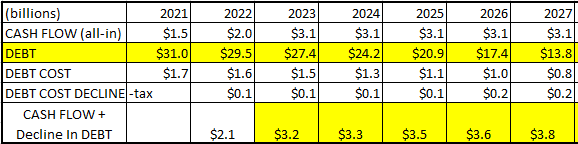

If they use the $3.1 billion in free cash flow to repay all the debt first, they would repay that in 10 years. This would eliminate interest costs, increase taxes a bit on the higher profits, but in total would bring cash flows from the current $3.1 billion expected in 2022 to $4.4 billion by 2028. So, in 2028 we could have a business making $5.1 billion and having no debt.

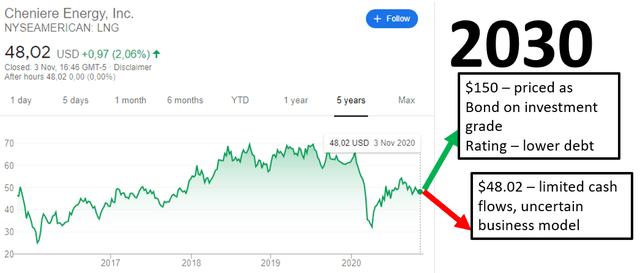

If all else remains equal, US supply of low cost natural gas remains a constant and global demand for LNG remains the same, then we could value LNG in 2030 as a good bond with a 4.4% yield. This would give LNG a market capitalization of $100 billion by 2030 which implies a 233% gain or 12.7% return per year. The 12.7% return per year is actually close to the expected return on capital the whole Cheniere LNG project has which is around 10-11%.

If they lower the debt to ‘just’ $14 billion which should give them investment grade ratings, then by 2027 the company should be able to pay $3.8 billion in free cash flows.

Again, assuming all else remains equal, we should see a valuation of around $70 billion by 2027 in that case, assuming a 5% required yield. This would give a 14.5% yearly return and is what the management’s target is. As the return on capital is higher than the cost of debt, it pays to be leveraged. However, double digit possible returns don’t come easy these days, so there must be more the market is pricing in.

LNG stock investment conclusion – Price forecast

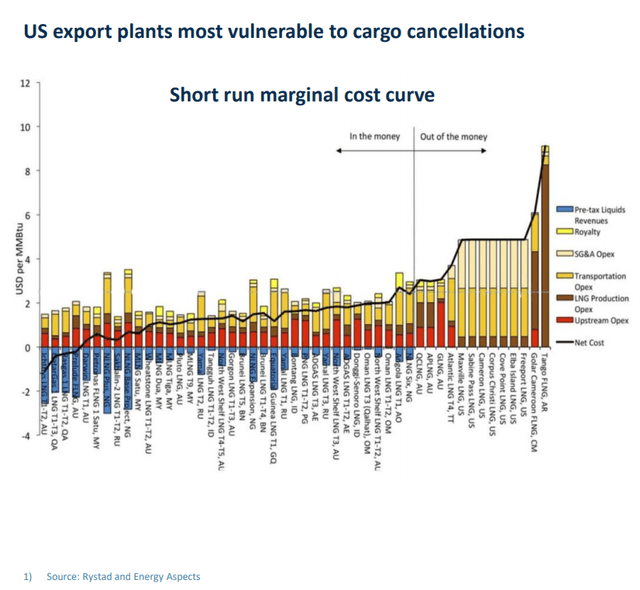

Perhaps the most impactful chart for Cheniere is the global cost curve chart for LNG. Being in the highest cost percentile while heavily loaded with debt, isn’t a great situation to be in.

Cheniere’s future, the future beyond the fixed contracts already in place, depends on the competitive position US LNG will be 10 to 20 years down the road. That is an uncertain situation and therefore the market offers a high return for those happy to take the risk.

Given the contracts Cheniere has, cargo cancellations are unlikely, but what is possible are difficulties in renewing long-term contracts. If beyond 2030, there are just 5 years of operations left because LNG is cheaper from some other parts of the world, LNG stock would not be priced as a bond, but as a cash flow stream with a limited life. Let’s say, that from 2030 to 2040 we could have 10 years of $4.3 billion in free cash flows, that should be worth $30 billion in 2030 which would give you no return over the next 10 years from current market levels. I think this is the risk and reward.

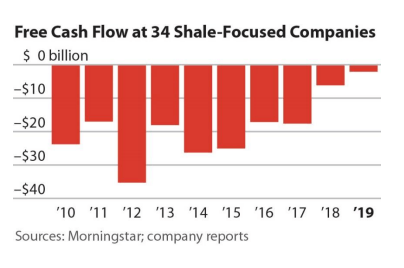

The outlook for US shale competitiveness is still murky as shale operators continue to have red ink on their financial statements.

Shale competitiveness is one of the key long-term investing factors for natural gas and LNG and I will dig deep into the issue so please consider subscribing. Also, this is just an introductory discussion on LNG and Cheniere, I’ll be looking deep into the natural gas sector globally which should give me better insights into what are the best risk and reward investments and, most importantly, at what level could there be low risk, high reward investments.

For more analyses like this one, please sign up for my newsletter or check my Stock Market Research Platform for the Premium view. Here is a copper stocks sector overview which is and overview of what my aim also for natural gas stocks.