CCEP Stock Analysis – Leave It To Index & Pension Funds – There is Better

Coca Cola (NYSE: KO) is the mother company owning the formula to make the famous drink. The business model is one where the mother company sells the syrup to bottlers around the world that you can own too as Coca Cola usually owns just a small stake into these distributor companies.

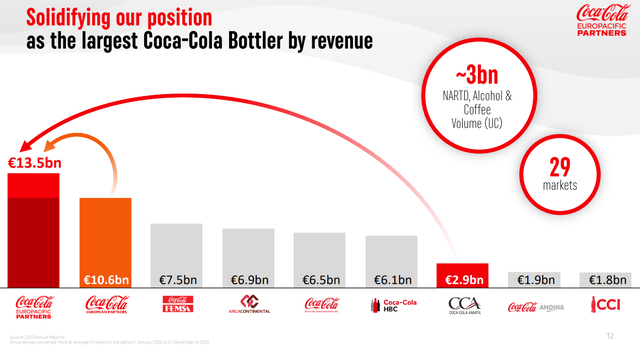

I’ll quickly make a Coca Cola Europacific Partners (CCEP) business overview, discuss the fundamentals, and conclude with a valuation and investment thesis for CCEP stock which is the largest Coca Cola bottler in the world.

This CCEP stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As. Here are the Cs already.

CCEP Stock Overview – NYSE: CCEP Stock – Leave It To Index Funds

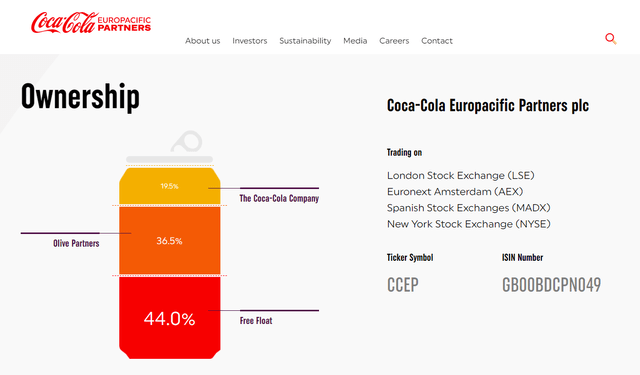

CCEP stock is traded in London, Amsterdam, Madrid and New York. The free float is 44% while KO owns 19.5% of the company.

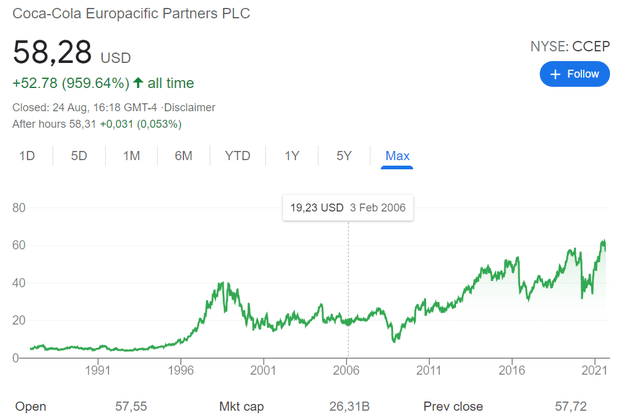

CCEP stock has been doing good for shareholders over the last 3 decades and the stock is up 10 times since the 1980s, not including dividends.

KO has done even better as the stock is up 30 times not including dividends.

CCEP Stock Analysis – Business Overview

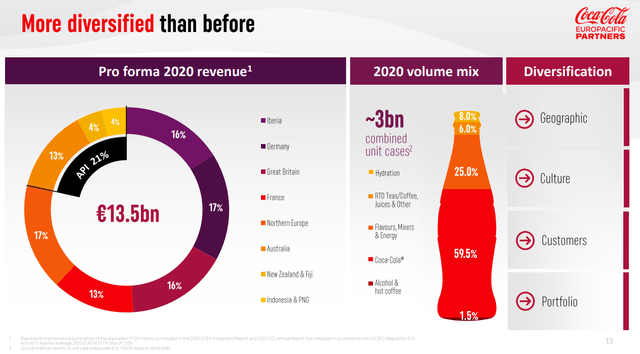

The business has distribution rights in Western Europe and Asia Pacific that covers a population of 600 million. The main product is Coca Cola but also Monster beverages and all other related products from tea to water and the currently expanding hot coffee market.

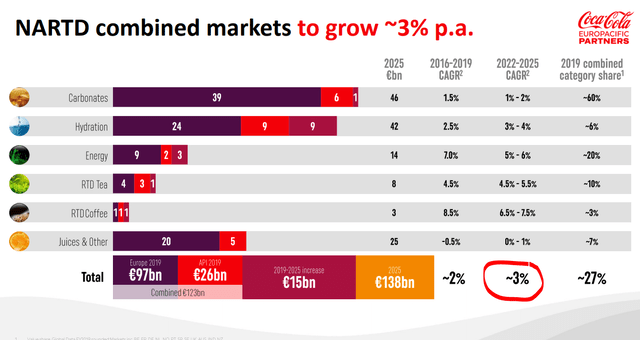

CCEP Stock Analysis – market – Source: CCEP Investor Presentation

The expectation is for the NARTD – nonalcoholic ready to drink – market to grow 3% per year.

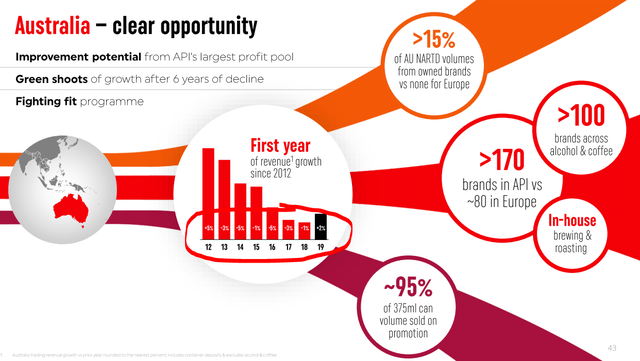

CCEP Stock Analysis – market – Source: CCEP Investor Presentation

The company expects growth ahead, but a developed market like Australia had not been growing between 2012 and 2019, only to see demand fall again in 2020. The 2020 drop was due to Covid-19, but still, I see a change in consumer behavior as the key risk for a business like CCEP.

I know people are in the habit of buying these soft drinks filled with sugar, but for a long-term investor like me, I feel things might change, as it has been the case in Australia.

In short, the reward might come from further growth, especially from countries like Indonesia if people there start to kill themselves with Coca Cola while on the other hand the risk comes from the population shifting away from soft drinks.

The reality will likely be somewhere in between, with new products like no sugar or kombucha making a difference. Therefore, it all depends on valuation and how the stock price versus the fundamentals fits your investment requirements.

CCEP Stock Valuation

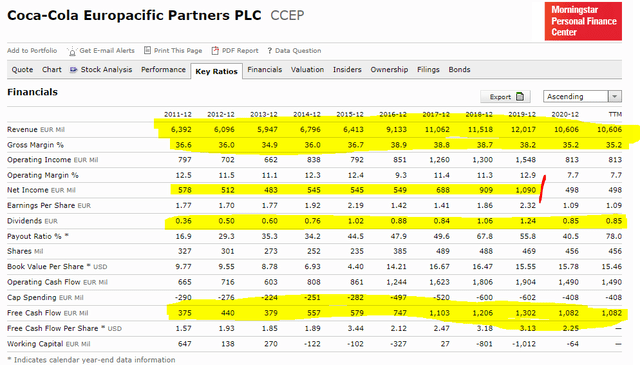

The business has been growing over the last decade, has seen improving margins, increased earnings and most importantly a triple in free cash flows that has also allowed a triple in the dividend.

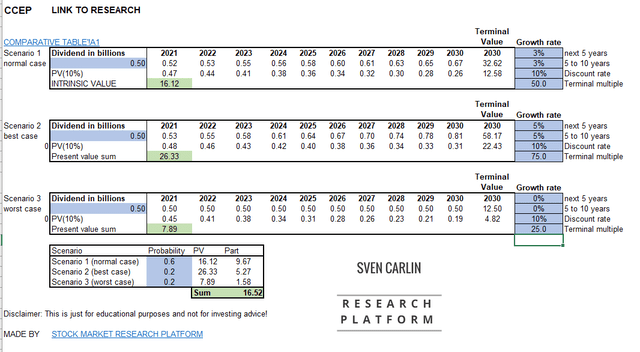

If they make on average 1 billion EUR in free cash flows per year, with a market capitalization of 20 billion, I get to a free cash flow return of 5%. They pay out just a fraction of that in dividends as the rest is reinvested in growth and their target is for a 50% net income payout ratio. Thus, we have to make a valuation estimating 3% growth on the dividend and a likely 2% dividend yield long-term.

If I put the above into my model with a required 10% return, CCEP stock is absolutely overvalued.

However, we are all different as investors and if you are happy with a lower return than 10% for a good business like CCEP is, with a strong brand and huge sales, you might be happy with a lower return.

If I expect only a 3% return (discount rate), 5% growth in the dividend ahead and the market remains happy with a 1.33% dividend, only then I can say CCEP stock is fairly valued.

CCEP Stock Investment Conclusion

The thing is that companies like these are mostly owned by pension funds that don’t really care much about valuation or your pension – they just buy whatever, mostly based on market capitalization, with their funds keep the price going higher and higher.

We as retail investors might be able to buy these businesses at fair prices only during crisis times. Such times are definitely not now.

For comparison, I feel Berkshire is still a much better investment than CCEP. At current levels Bekrshire offers a 6% investment return, while CCEP a 3% one. Plus, BRK has more cash, better businesses and is growing similarly.

I will continue looking to companies listed on the Amsterdam Stock Exchange with the hope of finding just one that might create value for retail investors. If you enjoy such an investing attitude, consider subscribing.