$13 Million-Dollar Investment Bank Managed Stock Market And Bond Portfolio Review

A month or something ago, I was contacted by an investor that had just set up a portfolio with an investment bank. He told them that his risk tolerance is minimal and that he would like some capital appreciation in the long term. He asked me to review the portfolio and that is what we are going to do now.

Here is the video version, while those who prefer reading, can find the article below.

The topics:

$13 million-dollar investment bank managed stock market and bond portfolio review:

- US equity portfolio exposure & issues

- International equity portfolio exposure

- Fixed income portfolio

General banking fees and value for money

- Discussion about fees and risk reward opportunities

Investment strategy

- Portfolio management

- Risk and reward

- What would I do differently?

Stock market and bond portfolio review

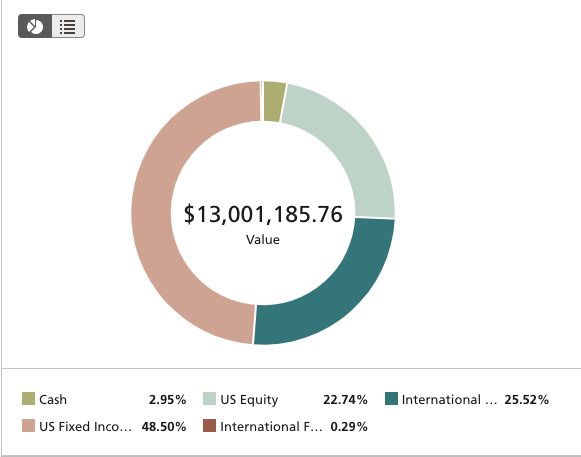

Here is how the portfolio has been structured:

US equity is 22.74%, international stocks 25.52% and as the requirement was low risk, 48.5% has been placed into US fixed income. This has been done by putting the money into 3 different bank funds (more about bank fees later). The yearly management fee is 0.9%.

Let’s start with US equity exposure.

US equity portfolio exposure

The portfolio positions are listed from the largest to the smallest. The client automatically replicates the positions held by the 3 funds within his account.

The largest position is Advance Auto Parts (AAP). I don’t know whether the fund bought the stock at the bottom in February of 2018 or it was a long term holding as the unrealized gains and losses in the above table go back to when the portfolio investment was made, which is February 2018.

AAP, has had free cash flows between $300 and $500 million per year over the last 10 years on a $10 billion market capitalization. I would expect the return there to be around 4% in the future. Auto parts are a competitive business but can be recession proof.

The next position is Comcast (NASDAQ: CMCSA), a company that recently won its bidding war and acquired Sky Plc for $38.8 billion. The all cash offer will put more pressure on Comcast’s balance sheet that already has $114 billion in liabilities. Plus, Sky Plc has had operating cash flows of around $2 billion per year in the last 10 years. This makes it a stretched acquisition as the interest on the debt will be close to the $2 billion of free cash flow coming from Sky.

Intercontinental Exchange (NYSE: ICE) is another stable company with high free cash flows and a potential return of around 4 to 5%. Free cash flows are $2 billion on a $42 billion market cap.

Danaher is the 4th largest US portfolio position (NYSE: DHR) is another stable company with $3 billion in cash flows on a $70 billion market cap.

Progressive Corp Ohio (NYSE: PGR) is an insurer and Kroger (NYSE: KR) is a grocer with similar characteristics as the above businesses. All have dividend yields of around 2%, stable business models, we can call them recession proof business models, and price to cash flow ratios of around 20 that should lead to a return of around 4 to 5%.

If we look at other portfolio positions, those mostly replicate the above. All good companies and fairly priced by the market. The portfolio also holds Google or better to say Alphabet (NASDAQ: GOOGL), American Express (NYSE: AXP), Mastercard (NYSE: MA) and we could easily say that the US equity portfolio reflects the client’s wishes: safety and quality.

US equity portfolio potential issues

I have two issues I want to discuss. The first is the value added in relation to the charged fee and the second is the fund management cost environment and investment process which is possibly even more important than fees.

Investment fees and value added

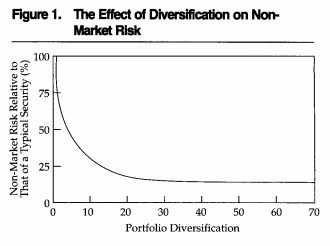

The first issue with the US equity portfolio part might be that there are 26 positions. If we look at professor and 1990 Economics Nobel prize winner Sharp’s seminal work on risk: Risk, Market Sensitivity, and Diversification, published in the Financial Analysts Journal in 1972, we see that as soon as you pass 20 positions in your portfolio, the risk equals the market’s risk.

Source: Risk, Market Sensitivity, and Diversification – CFA publications

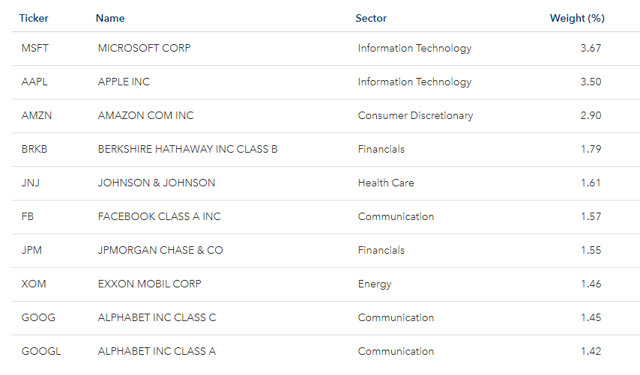

We have seen that the expected returns from a price to cash flow standpoint will be around 4 to 5%. However, if we look at the top positions of the S&P 500, their price to cash flows don’t differ much from the ratios of the analysed portfolio and the businesses in the S&P 500 can be considered of quality too.

Source: iShares S&P 500 ETF

Microsoft (NASDAQ: MSFT) has a cash flow yield on price of 3.75%, Apple (NASDAQ: AAPL) of 8%, Amazon (NASDAQ: AMZN) of 1.8% but we might argue that in 10 years, AMZN might have higher cash flows than Kroger. Berkshire (NYSE: BRK.A, BRK.B) is a diversified portfolio focused on US equity by itself, it holds great businesses and it has a price to free cash flow ratio of around 4%.

This leads me to the question, is the 0.9% yearly fee our friend is paying for the above portfolio justified? One can buy the S&P 500 for a yearly fee of 0.04% which is 22.5 times smaller than what is being paid to the investment bank or there is always the option to simply buy Berkshire and let Buffett and his fellows manage the money at no cost practically.

To conclude on the investment fees, I don’t think that in this case, paying a yearly fee of 0.9% adds any kind of value given that the stocks might look a bit more conservative than the S&P 500 but such bet is based on past performance and not part of a strategy. In this digital era world, one might argue that Amazon is more defensive than Kroger.

Investment fund behavior

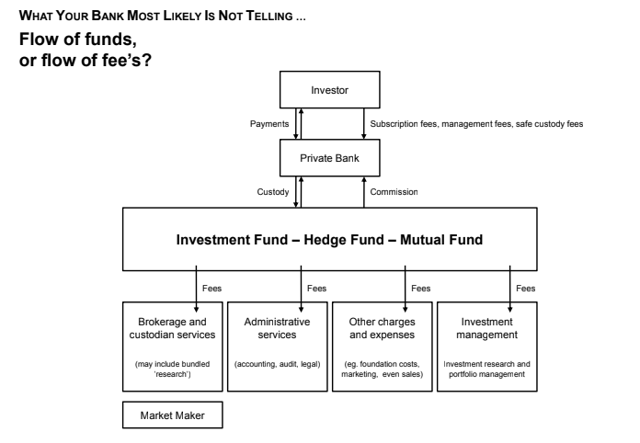

The thing when it comes to banks is that there is a lot your bank is not telling you.

Aside from the 0.9% yearly management fee, the bank makes money as they buy and sell through their own broker, perhaps they are even the market maker for the security, they pay for research, marketing costs, administration etc. that might not be included in the first fee you pay but might be included in the costs of the second fund that you actually don’t see. In this case, as the clients owns the positions directly, only the brokerage, custodian and market maker fees come into account, but that is still something extra.

Investment fund management process

Now, there is another thing when it comes to investment funds that is not discussed much. When things go well, all is good, but when things go south, some clients might want their money back. The investment manager is put into a tough spot because he then has to make investment decisions based on external inputs which might not be in the best interest of other clients. For example, if I manage a $1 billion portfolio, there is panic in the markets and clients want to cash in on $300 million. Liquidity usually dries up on the market too at such moments and you cannot sell your positions easily, especially your bond positions. (Remember that the positions discussed above are part of a much bigger fund)

The investment manager has no option than to sell the most liquid assets which might be the best assets to hold in the long term. Further, an investment manager has to be invested 100% all the time. Investment managers, collecting a fee of 0.9%, don’t have the option Buffett has. Buffett has $114 billion dollars practically lying on Berkshire’s bank account waiting for a market panic so that he can buy stocks on the cheap. (Buffett’s cash is invested in short term US Government Treasuries with an average maturity of 4-months – can be considered as cash)

This is something few think about when things go well, but crucial when things go south. Our friend has no influence on that and unfortunately this is where things often go wrong with funds managed by investment banks. An investment manager has to do as ordered, not as he wishes or what would be in the best interest of the client.

International stock portfolio overview

The international part is 25.52% of the whole portfolio and has a total of 68 positions. Since the inception of the portfolio, the performance of the international part has been really bad as almost all the positions are down with some like Ryanair (LON: RYA) down 34%. This is nothing strange given that international stocks and emerging markets have really suffered during 2018.

The largest position is Medtronic (MDT), followed by Unilever (UN), Compass Group (CMPGY), Aptiv (APTV) and Ryanair (RYAAY). There is a little bit of everything there with Tencent (TCEHY), BHP Billiton (BHP), the Indian Icici Bank (IBN), the Russian version of Facebook – Yandex (YNDX) and some interesting Chinese stocks like 58.com (WUBA) or South American payment processors like Cielo SA (CIOXY).

Now, Medtronic (NYSE: MDT) – the world’s largest medical device company makes most of its revenues and profits from the U.S. healthcare system but is headquartered in Ireland for tax purposes. Thus, this is not an international stock but goes under the international portfolio. Free yearly cash flows have been around $4 billion over the past 10 years and the market cap is $120 billion.

Nevertheless, holding 69 stocks doesn’t move the needle and we can expect them to perform equally as the market does. Therefore, one can simply buy the Vanguard Total International Stock ETF (VXUS) for a fee of 0.11% per year.

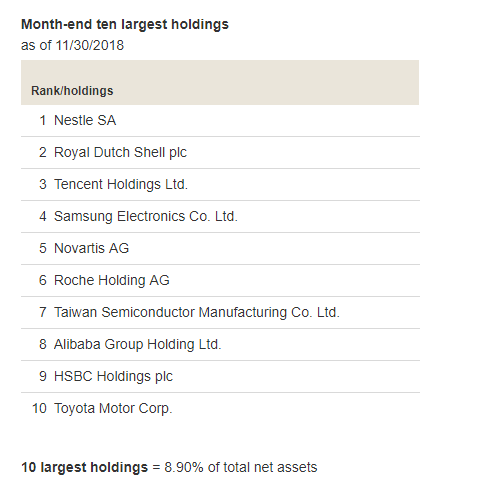

If I compare Vanguard’s top 10 positions and the portfolio we are analysing, I see that Royal Dutch Shell pls (NYSE: RDS) is in both portfolios, same as Tencent (TCEHY), Novartis (NVS), Roche (RHHBY) and Taiwan Semiconductor (TSM).

Source: Vanguard

So, a portfolio I am paying 0.9% to be managed has 5 positions that are also in the Vanguard Total International stock ETF top 10 positions with a management fee of 0.11%.

Let’s see if there is more value added in the bond portfolio.

US fixed income portfolio

48% of the portfolio is placed into a bond fund and the holdings are the following.

The majority of the bond portfolio is in US Treasuries, 18% of it, with maturities ranging from 2021 to 2026. The yield on those is less then 2% or around that. Then there is a bunch of other corporate bonds with yields between 1% and 4% on average and maturities ranging from 2022 to 2028 on average.

Now, the first thing is that if 9% of the total portfolio is in Treasuries, why would you ever have to pay any fees on that as with a $13 million dollar portfolio you can simply buy them yourself. Or, if you want, the Vanguard Treasury ETFs has a fee of 0.07%.

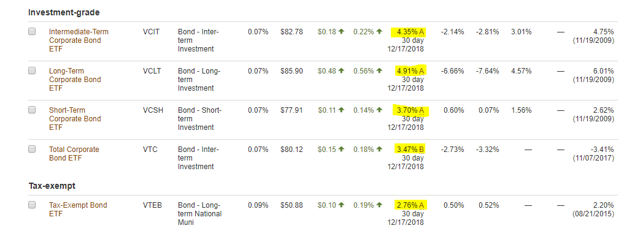

Secondly, the investment grade US corporate bond ETF from Vanguard, offers much higher yields for minimal fees.

Source: Vanguard

Source: Vanguard

On a portfolio of 66 bonds, 60 excluding the Treasuries, I simply don’t see any difference except the huge fees. The intermediate corporate bond ETF, has a yield of 4.35% and is managed by Vanguard.

Conclusion – portfolio management and risk reward

The holder of this portfolio hoped that I can manage part of his portfolio and perhaps create an all-weather portfolio for his holdings. I declined because my current investing focus accepts a little bit more risk as we are focused on long term return maximization which isn’t what the goal of this portfolio is. I am completely devoted to what I do and creating another portfolio alongside building mine would be impossible. On the all-weather portfolio, I am partly working on it, but an all-weather portfolio focuses first on neutralizing risk and not that much on maximizing returns. You cannot get high, Buffett like returns with an all-weather and that is why I cannot focus my whole work around it and this portfolio. I takes at least a year of hard work to build a portfolio.

Secondly, if I would have to manage the money as required, the way explained above would be one way of doing it. I cannot charge $117,000 per year for the above as the investment bank is doing, I simply can’t. Well, you have it above for free.

What we actually did is that we have created a smaller part of the portfolio to follow my portfolio that I manage on my Stock Market Research Platform. This should add a bit more diversification as it is focused on absolute value and not that correlated to markets. Plus, there are some hedges too.

Portfolio risk reward

Now, what we still have to discuss are the risks of the above portfolio in relation to the rewards. We have seen that the yield on Treasuries now should be around 3%, and the return on equities could be at 4%, up to 6% on the international portfolio. Given the 10-year maturity of the bonds, that is what the holder can expect, deduct 2% inflation and you have a real return of about zero on the bond portfolio which would be closer to 2% with Vanguard.

50% of the portfolio is in stocks and given that the number of stocks held is 90, one should expect equal to market returns, US equity markets and international equity markets. The biggest risk here is a contraction in valuations. If global investors start to require a 6% investment yield in place of the current 4%, that could lead to a decline of 50% on global stock markets and a similar decline within the equity portfolio. Also, as bonds are priced in relation to interest rates, I would expect a significant decline in the bond portfolio too.

Thus, the upside is limited but the downside is pretty big. This is because there is no strategy behind the discussed portfolio, it is over diversified, there are no hedges in place, no real diversification as we have seen bonds and stocks move in correlation during the turmoil of the last few months.

What makes me sad is that most pension funds are managed in the above way with outrageous fees. In a video on Canadian pension funds I discussed how fees go up to 2% per year for practically nothing. This is outrageous and the first thing I would tell people to do is to start educating themselves about what can be done when it comes to investing their hard-earned money.

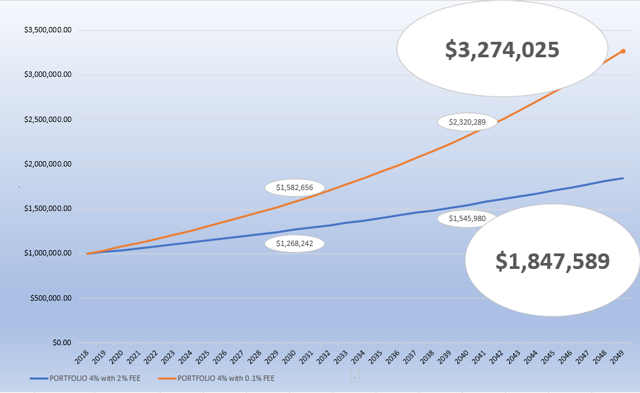

Perhaps, individual stock picking the way I do it will not be for most, but lowering a management fee from 2% per year to 0.1% makes a hack of a big difference within a portfolio. Actually, it makes almost a 100% difference on a long-term portfolio over 30 years based on current market return expectations.

If all that you change in your financial life and investment portfolio is that you get a lower fee or even eliminate fees, the above is how much it affects a $1 million portfolio over a 30-year period and 4% market returns per year. The differences are staggering.

Investment strategy

From a general perspective, an approach like the one discussed above offers no strategy, it is a purely market following and extremely diversified investment. Thus, such a general approach certainly doesn’t deserve to charge a 0.9% fee. The lack of alpha, the lack of an investment strategy, a portfolio that resembles an index is just part of what is not good in story we discussed up till now.

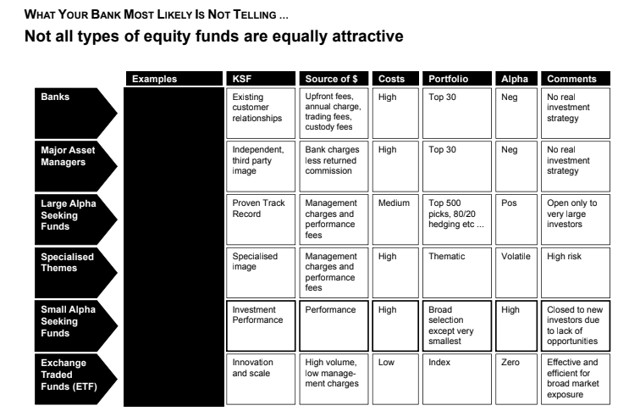

The following chart shows how there are different investment strategies and the one discussed today is probably the most obsolete. However, banks still manage to sell it to clients due to a lack of financial education.

My opinion would be that the investor should first create a clear strategy about what is the goal for his funds and then put that goal into a risk and reward perspective within a well-diversified portfolio based on a well-balanced strategy.

Such a strategy is what we focus on so if you enjoyed this kind of investment educational content shared above please follow, subscribe, like and share.

About the author: Sven Carlin, Ph.D. is passionate about investment research and value investing. He also manages the Sven Carlin Stock Market Research Platform based on long term value and business investing principles.