Aperam Stock Analysis – AMS: APAM, OTC: APEMY – You Buy Cyclicals When Things Look Bad, Not When Good

This Aperam stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger long-term investing potential, so as would Buffett say; I start with the As.

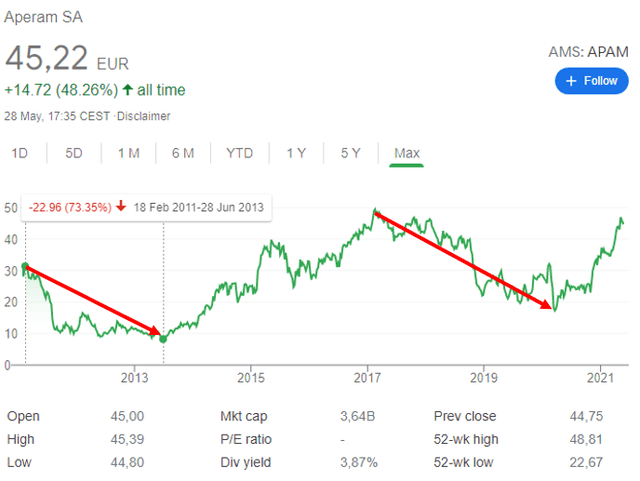

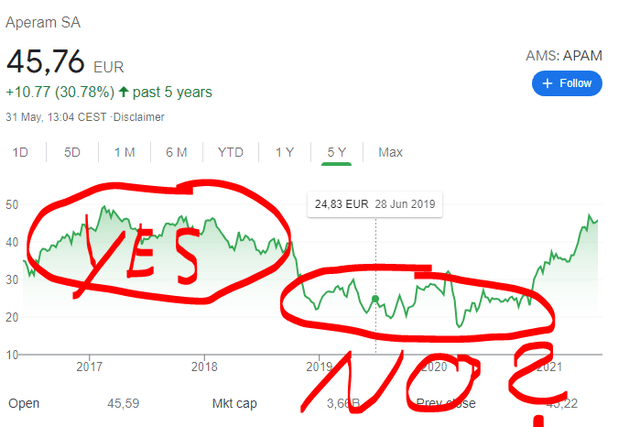

Aperam Stock Price Overview – AMS: APAM, OTC: APEMY

Aperam is in the steel business which is extremely cyclical and that is reflected in the stock price too.

There are practically no competitive advantages in the steel industry which means that you totally depend on market prices. Thin margins mean a steel business makes a lot of money in good times and operates with losses when steel prices are low. Consequently, steel stocks follow steel prices and the environment is extremely volatile, especially if the company has significant leverage which I suspect is the case with Aperam because of the common 75% stock price drops shown above (actually it was the case as the company transformed – this might create an opportunity as usually the market paints all players with the same brush).

Aperam is traded on the Luxembourg Stock Exchange, Euronext Amsterdam and Euronext Paris, Aperam shares are also cross-listed on Euronext Brussels. There is also an OTC listing with OTC: APEMY.

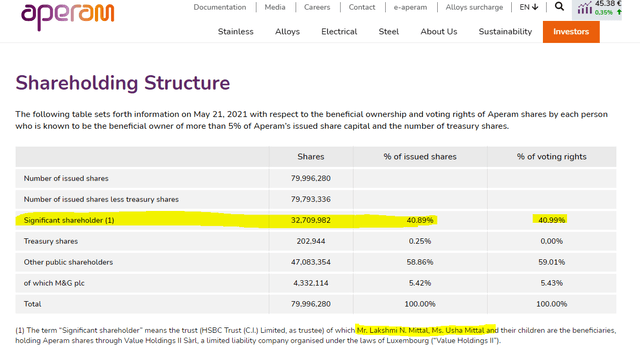

Aperam is controlled by Lakshimi Mittal, the Indian steel magnate and CEO of ArcellorMittal. Aperam was spun-off from Arcelor Mittal in 2011.

Let’s take a look at the business, the financials and see what is Aperam’s investing potential.

Aperam Stock Analysis – Business Overview

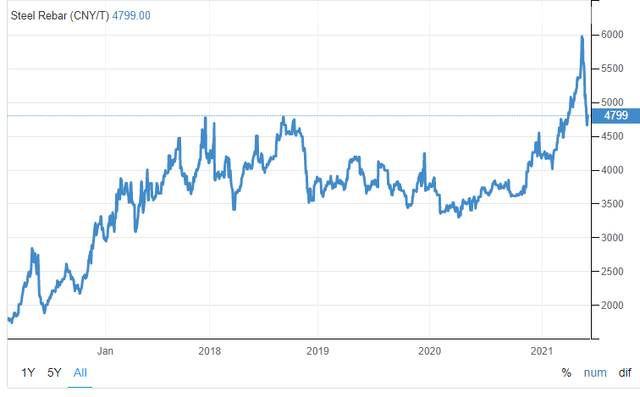

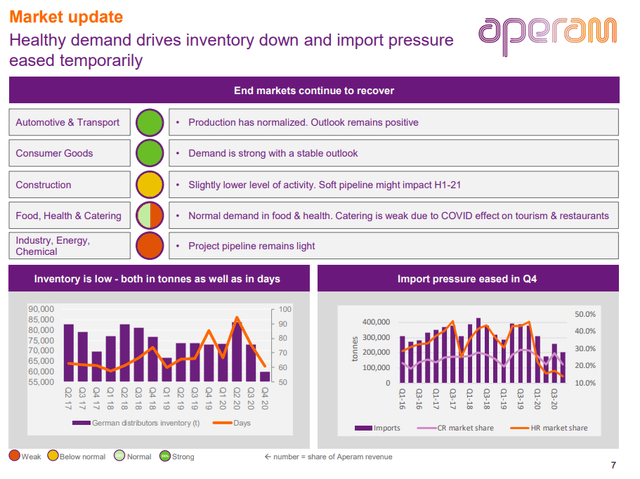

Aperam operates in the stainless steel and alloys business. Steel prices have been strong lately which bodes well for Aperam, but mind the cyclicality.

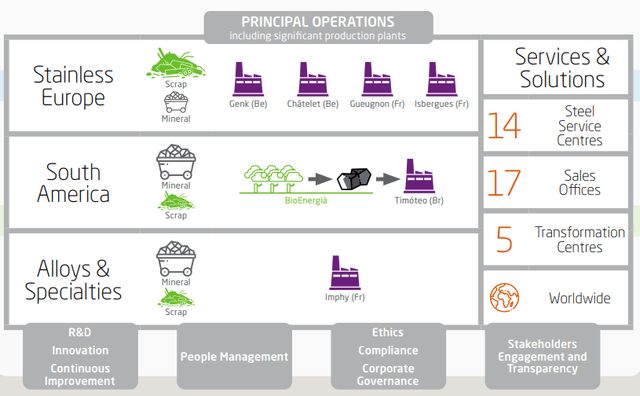

Aperam’s operations consist of steel factories in Europe where mostly scrap is used, one in South America where mineral is used and a allow and specialties factory in France.

There is a nice explanation about how the steel business works and how it impacts Aperam in their Annual Report, from duties, input prices, energy prices, global competition etc. I will not explain that in depth here to save space and focus on the business itself, namely the financials.

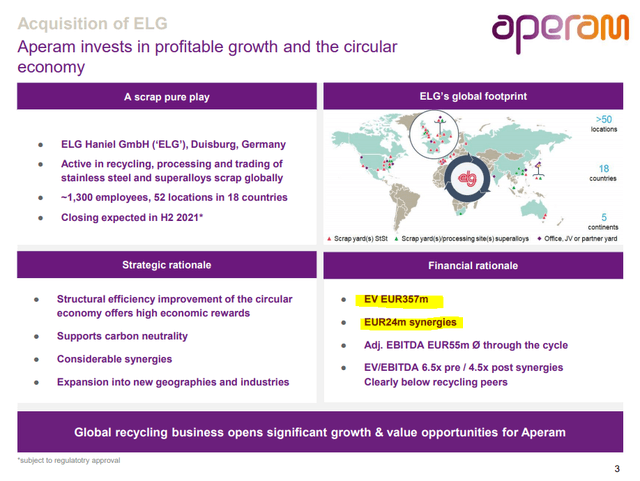

Aperam made a small acquisition recently by acquiring ELG Haniel.

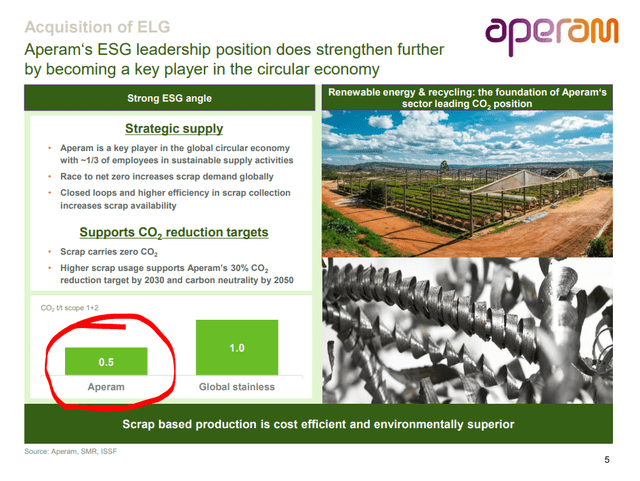

The company is pushing on becoming a green steel producer which is important these days to be included in indexes and get to sustainable financing.

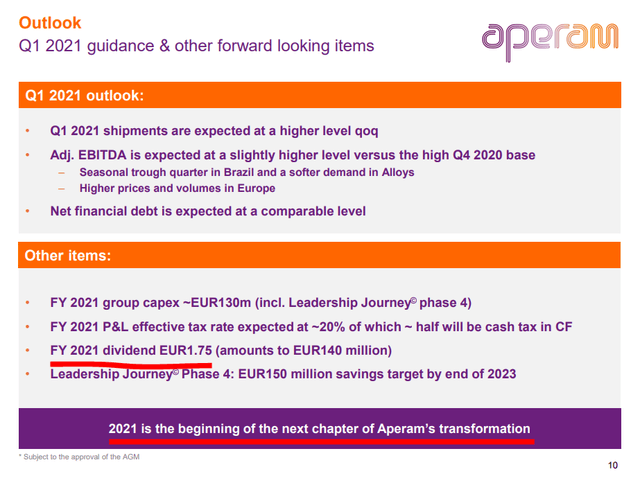

The business guidance for 2021 is positive, the dividend is planned and the investments should subdue beyond 2021.

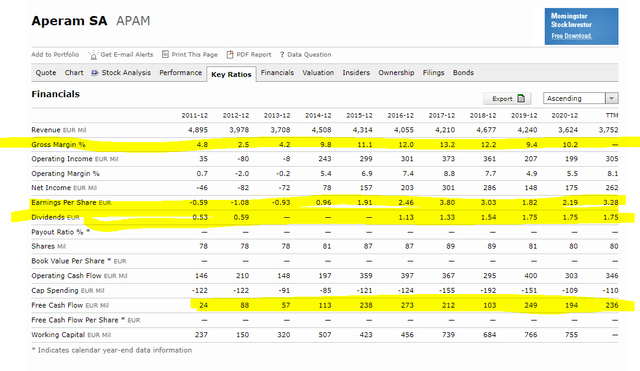

Aperam Stock Analysis – Financials

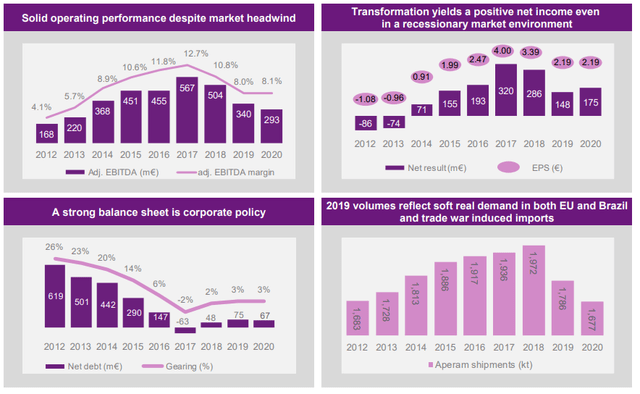

Aperam has been operating well since the 2013 Europe crisis environment. It has been also paying a dividend.

Gross margins are volatile and depend on steel prices.

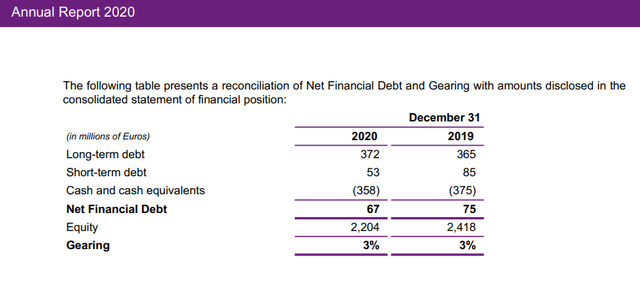

They had some debt in 2012 when they stopped dividend payments to lower it. Currently the company is net debt free. The debt structure will likely change now that they have acquired ELG Haniel, but still debt should be low.

The company has transformed itself from a financial perspective because, as we have seen by the stock price decline in 2012, it was too risky to operate with high levels of debt.

The goal is to be profitable even when there are cycle downturns as that those will come to the steel industry is one of the rare certainties when it comes to investing.

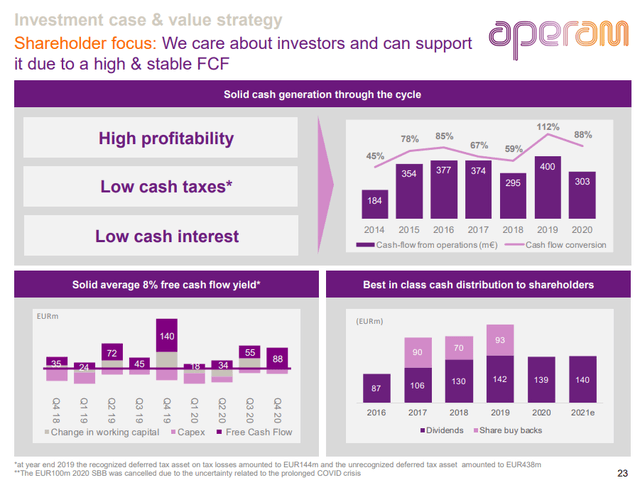

To value such a company one has to take the average cash flows and then buy when things look bad, but more about that in the investment conclusion below.

Aperam Dividend and Valuation

Aperam has buided for a dividend is at 1.75 EUR per share for 2021 plus they like to do buybacks when there is enough more cash than needed.

To put it simply, Aperam’s buybacks are stupid because they do them when the stock price is high and then don’t do them when the stock price is low.

Stupidity at its best but that is how it is. However, when it comes to investing in such a business one has to focus on the cyclical averages.

For a valuation, I have used the current dividend of 1.75 EUR per share, assumed 3% growth and if I expect an investing return of 10% while the market is happy with a 5% dividend yield, the time to buy a stock like Aperam is below 30 EUR per share.

Aperam stock valuation – Source: Sven Carlin Research Platform (free template download)

Aperam Stock Analysis – Investing Conclusion

Aperam is a typical cyclical stock. This means you have to buy it when things look bad, when valuations are negative and dividends cut.I prefer to avoid cyclicals when all looks rosy as it does now. I have put Aperam on my comparative table list using the above average cycle valuation. If and when the stock falls under 30 EUR per share, I will take another look.

Given the cyclicality of the sector, it is very possible we will see the stock below 30 EUR again. Such a price would represent a buy with a margin of safety as it would also be close to book value. Buying now could still do well, but doesn’t offer a margin of safety from an investing perspective

About the author: Sven Carlin Ph.D. is a dedicated investing educator and stock market researcher focused on finding investment opportunities with a value investing perspective. His research is summarized on the Sven Carlin Research Platform where he covers many stocks and shows his portfolios. The educational part is shared on YouTube and the Free Stock Market Investing Course.