Adidas Stock Is Better Than Nike, But Other 3 Factors Matter Even More!

I received many questions about Adidas stock when I analyzed Nike stock in June. My conclusion for Nike’s stock was overvaluation from a fundamental perspective and risky because:

- a growth slowdown is happening and what makes things worse,

- the management is attempting to conceal the slowdown with financial engineering.

- Nike has an extreme PE ratio which makes the stock even riskier.

In this article I’ll discuss Adidas stock as an investment opportunity and compare it to Nike stock and explain why long-term investors will continue to be better off investing in Adidas stock for the long-term.

Adidas vs Nike stock video analysis:

Analysis content:

- Adidas stock vs Nike Stock price movement

- General business environment for both Nike and Adidas based on Q2 2020 results

- Strategic comparison and risks

- Adidas and Nike Stock fundamental comparison

Through the analysis I’ll also touch on the core investing concepts one has to think about in this environment where Adidas and Nike come as amazing examples:

- The risks of growth investing – Both Nike and Adidas stock prices have long-term growth priced in

- Do fundamentals matter at all in this market?

- Financial engineering – is it ok to take debt to push the stock higher? Nike’s debt bonanza.

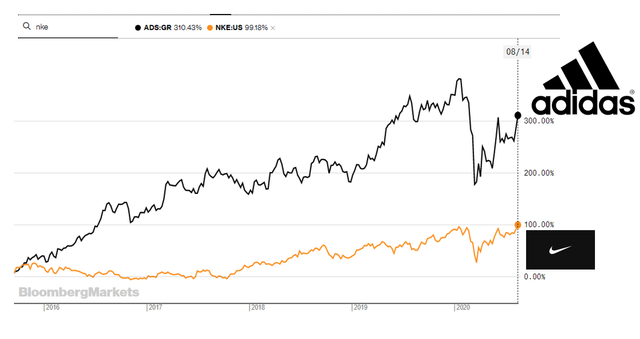

Adidas stock vs Nike stock price movement

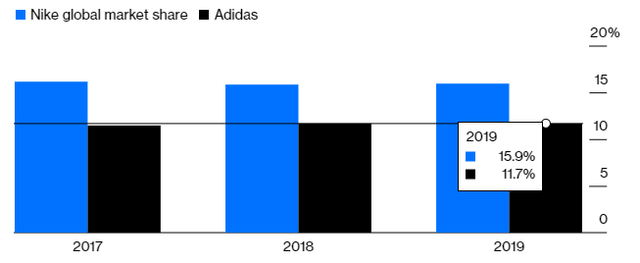

Over the past 5 years, Adidas stock has been a much better investment as it rewarded shareholders with a 300% return compared to Nike with a 100% return.

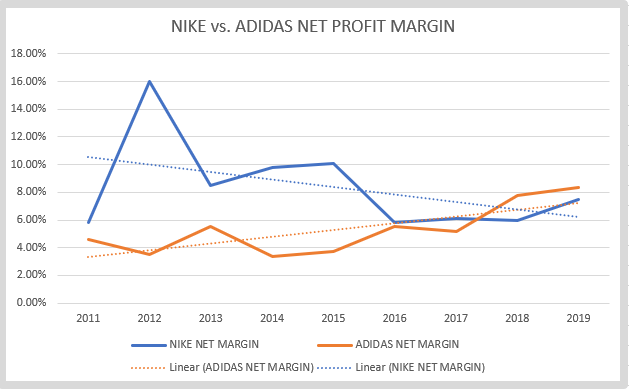

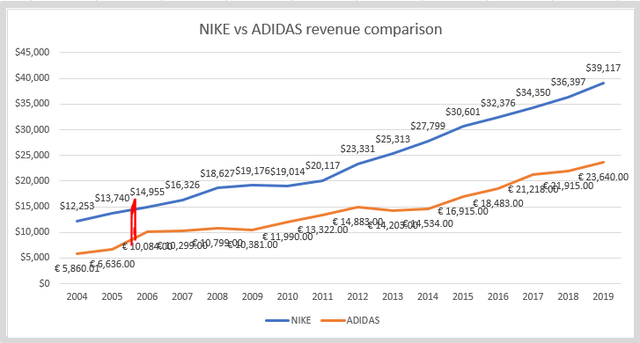

The better performance is because Nike reached its plateau a while ago while Adidas, likely copying what Nike had done already, managed to increase net profit margins from 3.3% in 2014 to 8.3% in 2019. The trend with the net margin development is clear, Nike’s net margin has been declining while Adidas managed to increase it by 300%. The consequence is the above stock price performance.

Let’s take a look at the latest results before making a fundamental comparative analysis.

Nike vs Adidas Q2 results

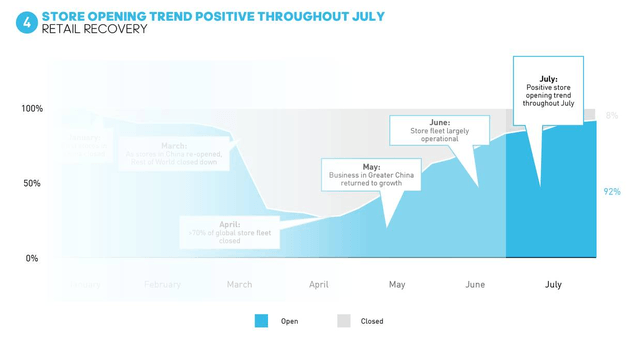

The good thing for both companies is that the retail environment opened up again and the number of stores open and selling shoes is slowly coming back to normal.

This means we can expect better results in the coming quarters and a return to normalcy for both companies. However, and I might go on a limb here, I am worried about something other than COVID-19 when it comes to both Nike and Adidas.

Strategic comparison – the elephant in the room

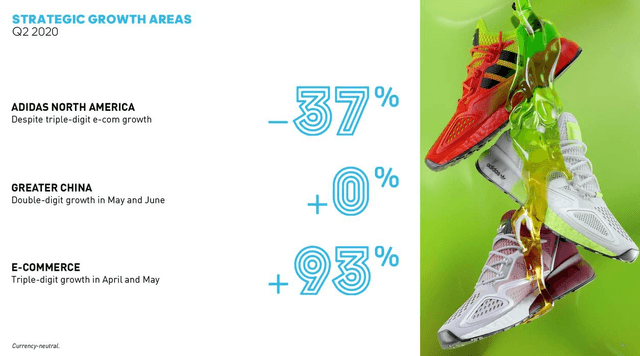

Both companies have a similar strategy. Their focus for growth are emerging markets and the online business that has had a huge boost due to COVID-19.

Also, as the world develops and the global middle class expands, the general expectation is that both companies will have a larger customer base and continue to grow over the coming decades.

However, there is one tiny concern I have that might compromise the positive expectations for Nike and Adidas. A recent UBS study on likes on TikTok found that up and coming brands like Prettylittlething, Fashion Nova, Shein and Gymshark had each more likes than Nike, Adidas, Lululemon, Skechers and Puma combined.

This doesn’t have to mean much, but just a small decrease in demand compared to expected demand growth over the next decade, could have a severe impact on investment results. For now, both companies have a stable market share and grow as the market grows. But, any decline in market share would likely lead to a change in the market’s perspective on the investments, consequently translate into a lower market valuation for the stock. That is the biggest risk I see, especially as the stocks aren’t cheap.

Let’s look at the fundamentals to see what is baked in the price.

Adidas and Nike stock fundamentals

Over the past 20 years, Adidas grew revenues faster than Nike but that is mostly thanks to the acquisition of Reebok in 2005. Since then, revenue growth has been somewhat similar, especially over the last 10 years.

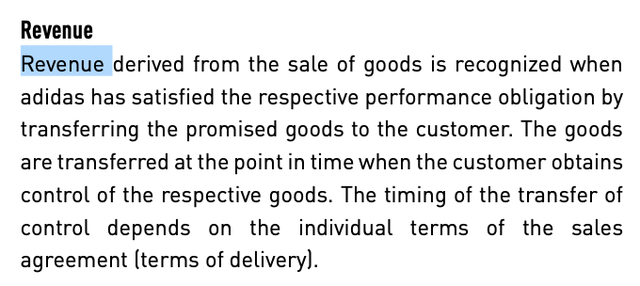

A very important note on revenues here. Nike, in order to keep revenue growth as high as possible, something that I would call window dressing, recently decided to recognize revenues when the item is shipped and not when the sale is actually made. For example, when your spouse orders 3 pairs of shoes and then returns two, Nike would account as 3 pairs sold while Adidas as just one pair sold. This increases profits for a short period of time, but that is what Nike needs to keep the stock going up. As the online arm of each business is growing rapidly, the discrepancy between recognized and real revenues might backfire for Nike at some point in time.

We have already discussed the fact how Adidas managed to reach Nike’s margin levels in the last few years which allows us to make a valuation comparison. When it comes to margin expansions in the future, I don’t think there will be significant future differences between the two companies as each will quickly implement what the other does in order to preserve or increase margins.

In the video above discussing the stocks, I might have an Addidas hoodie but all my sneakers are from Nike because a friend that had a high management position at Nike with their European headquarters in Hilversum, The Netherlands, took a job for Adidas in Herzogenaurach in Germany. The point is not that I got lots of Nike shoes for free, but that know how is quickly exchanged between the two companies. Back to earnings and fundamentals.

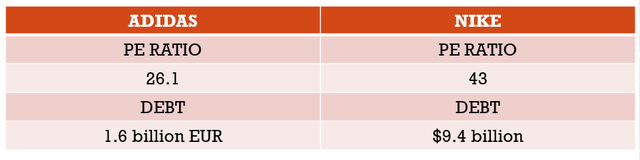

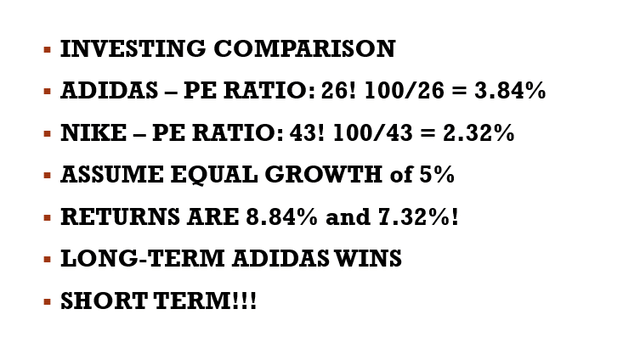

Adidas earnings per share were 10 EUR in 2019. On a stock price of 261 EUR it gives us a price to earnings ratio of 26.1. Nike’s earnings per share in 2019, which I am taking as a normal benchmark year because fiscal 2020, that finished in May was impacted by COVID-19, were $2.49 that gives us a PE ratio of 43. Thus, from a valuation perspective, Adidas is a much better investment than Nike.

Debt and PE Comparison – Adidas stock vs Nike stock

Further, from a debt perspective, both balance sheets look strong and I have no concerns for the companies.

But, Adidas has also a better balance sheet.

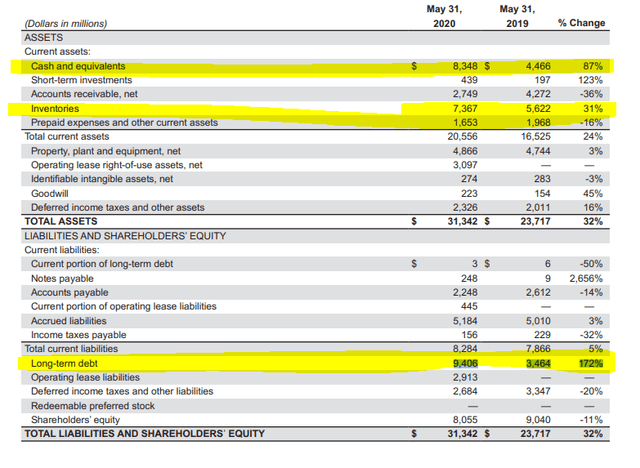

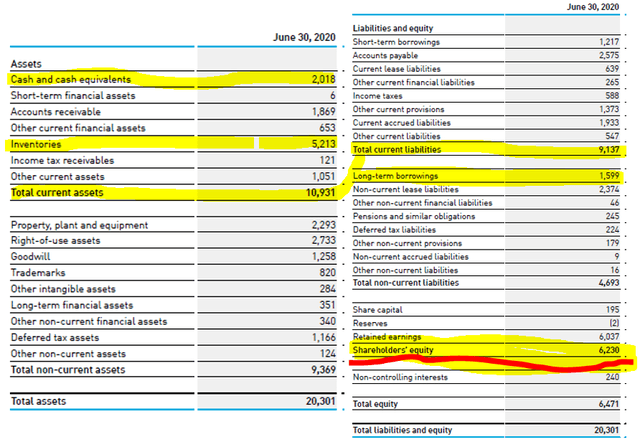

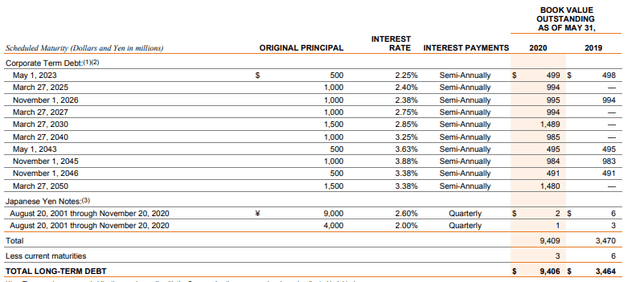

Shareholder equity is 6.2 billion EUR with Adidas on total assets of 20.3 billion EUR while with Nike, equity is $8 billion on $31 billion of total assets. Plus, during Q4 2020, Nike issued $6 billion of bonds in order to take advantage of the available cheap liquidity.

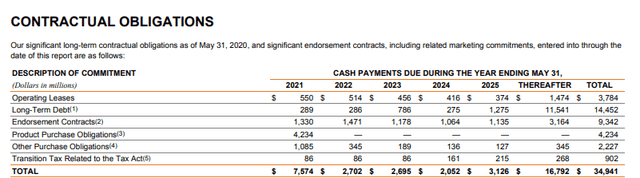

In addition to debt obligations, Nike also has $9.3 billion to pay in endorsement contracts for a total of $34 billion in future debt obligations. $34 billion in debt is approximately 10 years of earnings which tells me how Nike is continuing to play it risky on the financial engineering side. Interest rates seem low, but if the return on that capital isn’t higher all the time, the financial engineering will backfire.

If Nike’s has a bad year, there could be a trifecta of bad impacts for shareholders:

- A much lower valuation due to lower growth estimations.

- Debt becomes an issue only when things turn for the worse.

- Other brands start to gain in market share.

Of the above, the bad thing that could hit Adidas would be the market share loss to other up and coming brands, partially a lower market valuation and debt shouldn’t be an issue as the long-term borrowings amount to only 1.59 billion EUR.

Adidas vs Nike stock investment comparison

As both companies are keeping their market share stable while growing in line with market growth, I would say Adidas is the better investment for the long-term because it has a lower PE ratio, has much lower debt levels and is involved in much less financial engineering.

However, in the short term, thanks to the buybacks, dividends, huge liquidity and growth at all cost attitude with Nike, the stock could outperform Adidas stock but investors have to be ready to get out in time; before the debt, the growth slowdown and social media trends become a burden for Nike.

Whether it is healthy for a company to take on as much debt as possible ($9 billion at the moment) to engineer higher and higher stock prices and better fundamentals can be discussed. Such actions usually work very well while things are good, but as it was the case for Lehman Brothers, can backfire. As long as the market is happy with that and is willing to lend money to Nike at a 2.35% interest rate, Nike will keep benefitting from the engineering but keep in mind such games usually come to an abrupt end. When? I wish I knew!

As for Adidas, the PE ratio is 26, which results in a business yield of around 4%. Add the likely growth of around 5% per year over the next decade to the 4% return and you have a nice 9% return ahead. If the market for both companies grows at 5% per year, Nike’s stock return should be 200 basis points lower due to the higher valuation.

Adidas vs Nike stock – expected returns

The basis of the expected returns for both Nike and Adidas is growth. That is what makes these risky stocks in my opinion, because as we have seen in my Delta of the delta growth stock analysis article, small changes in growth rates can have huge impacts on stock prices. So, see how that fits your investment requirements and compares to other investment options you have.

All in all, Adidas stock continues to be the better, safer investment when compared to Nike stock.

To conclude, we life in a world of endless financial engineering so valuation metrics don’t mean much short term. If interest rates remain close to zero, Nike’s 0.9% dividend looks like an amazing investment and the stock might even double because a 0.45% dividend yield is still better than 0% what many of us get at the bank. I will explain here the connection between asset prices and interest rates.