Waste Management Stock Analysis – Moat and Scale, but Easily Down 50% in Next Downturn

Waste Management stock analysis

Waste Management stock analysis is part of a full Waste Management stocks sector investing analysis alongside a list of 15 waste management stocks, all analyzed.

Waste Management stock is the leader of the waste management industry with a stock market capitalization of $47 billion. Up to 2012 the stock didn’t look like anything spectacular but since then it has really boomed.

What is the difference between Waste Management and the other waste management stocks we discussed up till now?

Well, scale and moats!

Waste management managed to increase margins thanks to its integrated business and moat, as you can’t build new competitive landfills. Not in my back yard (NIMBY) might be something familiar to you😊.

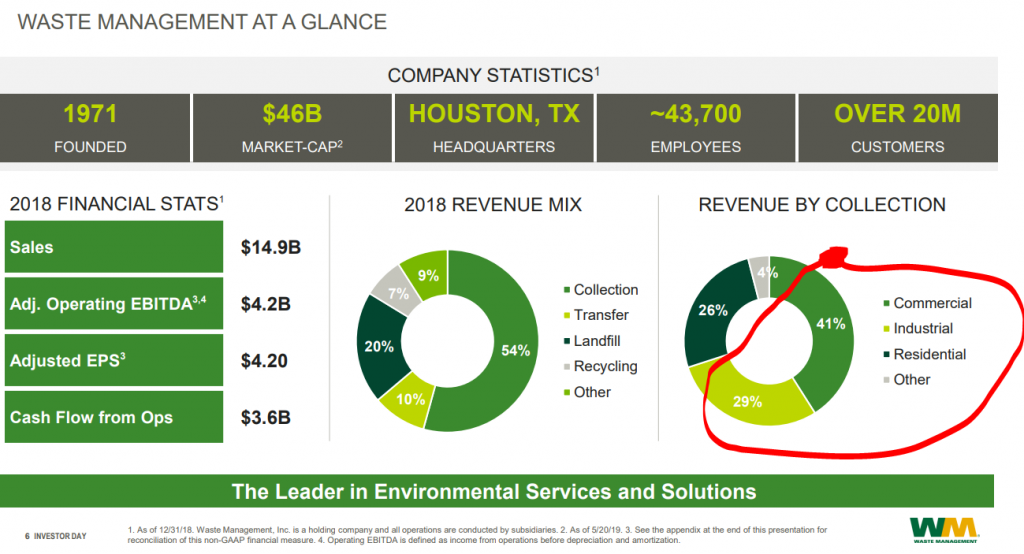

Source: Waste Management – Morningstar

As the business numbers improved, so di Waste Management’s stock price to earnings ratio improve. From an average PE ratio in the low teens, the valuation expanded to the current 27.31 which is a huge valuation for a company that hasn’t been really growing much.

So, the company got rerated by the market but I still see risks, especially as the company is dependent on the economic cycle as 70% of revenue comes from industrial and commercial clients.

The impressive network of landfills and short haul routes that gives it a competitive advantage is what makes the company a great business.

Waste Management stock – future investment returns

But, when it comes to future investment returns, given the price to earnings ratio of 28, there must be significant growth ahead to justify such a high valuation and a dividend yield of 1.83% seems a bit high. If I compare it to Visa stock, that I recently analysed. Visa has a price to earnings ratio of 33 but is growing at 15%, compared to WM’s expected growth of 4% in a very positive economic environment.

Given that there will not be an amazing population growth rate in the US, we can’t expect WM do grow much. Therefore, I see it as an expensive investment where the stock is being pushed up by buybacks and increased dividends. In case of a recession you can easily see this down 50%.

Now, you might wonder why do I analyse stocks like Waste Management that are clearly overvalued when you look at the stock price or price to earnings ratio?

Well, finding out what worked in developed markets will give me great insight when I’ll look into emerging markets. If I find a company that can build a moat there, offer similar economies of scale, grow also thanks to population growth and economic development, I could be looking at a big winner, similarly to what was the case with Waste Management over the past decades, up 30 times not including dividends.

It is unlikely that WM stock repeats the performance over the next 3 decades, but I might find a business somewhere else in the world that will do something similar.

Sven Carlin Ph.D., the author, is an independent stock market researcher and investor managing the Sven Carlin Stock Market Research Platform.

Those who want to learn more about stock market investing can join the Free Comprehensive Stock Market Investing Course.