Suncor stock analysis – Oil Stock Owned by Buffett (Cheap Stock)

Suncor stock (NYSE:SU) has been one of the most required stocks for me to analyze since the oil stocks crash started in March. The reason why people want me to analyze Suncor is because the business is owned by Warren Buffett, it looks like one of the best businesses in the sector with great long-term assets and low production costs, a strong dividend, a good balance sheet, but the stock keeps going down.

Suncor stock price overview

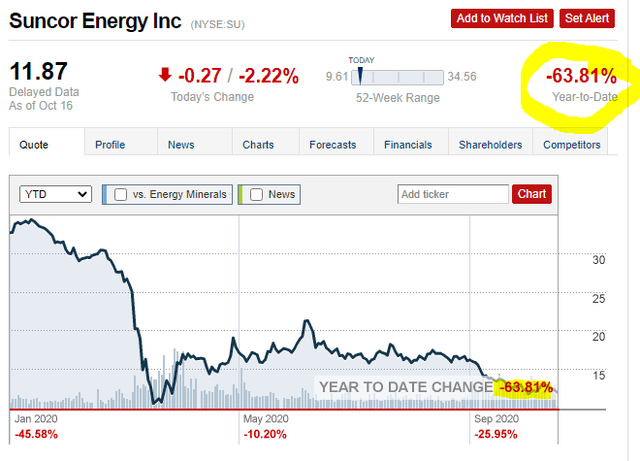

Suncor stock is down 63% year to date and at the March 2020 Covid crash lows. This means the market is not positive about the long-term outlook given the price destruction despite Suncor’s 5.5% dividend yield, likely sustainable.

It is either the market is totally irrational or, smart money knows something retail investors don’t? This Suncor stock analysis will be focused on the risk and reward of investing in Suncor and also on finding out why the stock is falling, despite the presumed business quality.

Here is the video analysis that also includes the comparison with RDS stock. Article continues below while RDS stock analysis is here.

Suncor business overview

I’ll start by discussing Suncor’s investor presentation and then continue by looking the other side of Suncor’s business, the one the management will not discuss in its presentation but is affecting the business.

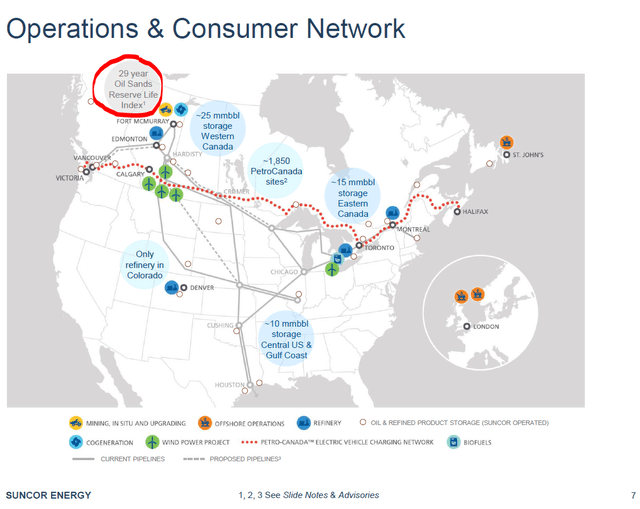

Suncor produces and distributes oil and oil related products in Northern America.

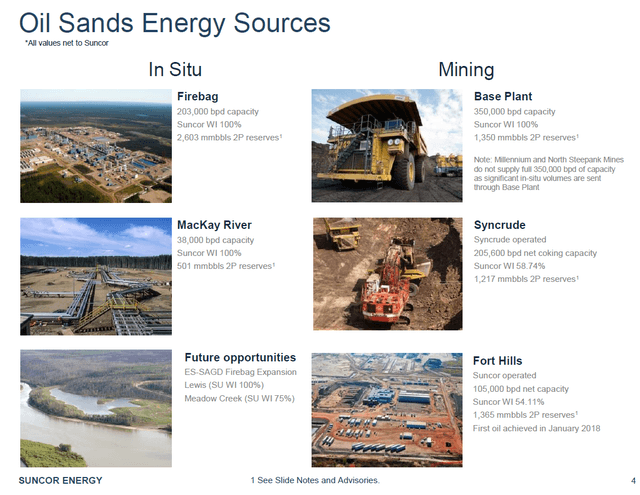

The core of Suncor’s operations are in situ and mining oil operations alongside distribution and refining.

The benefit of the above is a long mine life where the negative are the high upfront investments. But once the investments are made, cash flows should follow.

A first problem is location, in order to sell the oil you need to transport it and the current political environment might not be favorable for new pipeline construction.

Perhaps the company will have more luck with the Trans Mountain project that could be operation in 2023 as some regulatory hurdles have been cleared. Apart from the negative publicity, sooner or later the product is sold, so even without new pipelines the company should do as it has been doing.

Suncor stock fundamentals

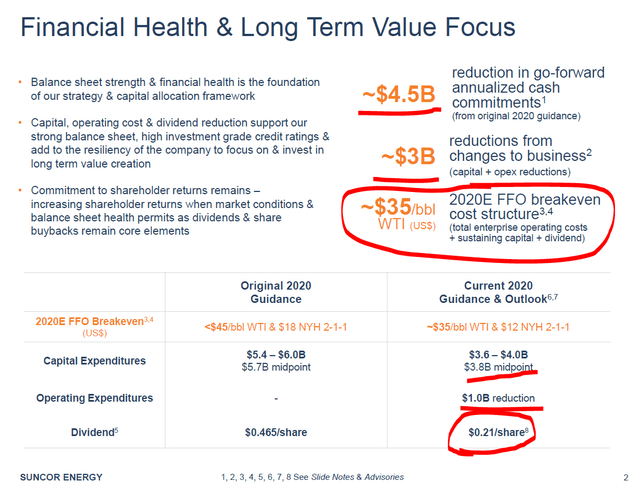

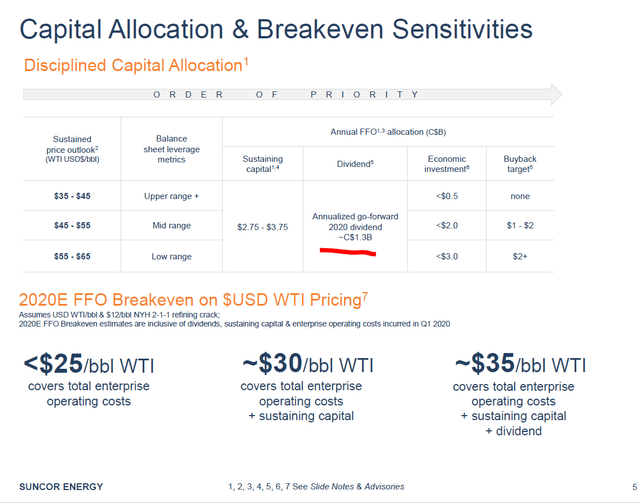

In short, the company is saying that with oil at $35 it can still make money, pay a dividend and wait for better times.

Their plan is to keep paying C$1.3 billion, USD $0.98, billion for dividends as long as oil prices stay above $35 which is something that should cover their operating expenses, sustaining capital and dividend requirements. At the current market capitalization, the yield should be around 5.4%.

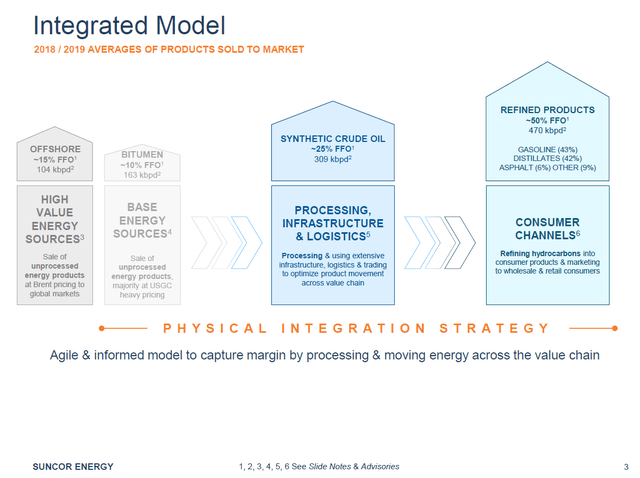

The company makes 50% of funds from operations from selling refined products directly to customers, 25% by transporting and trading products and 25% from the sale of unprocessed products.

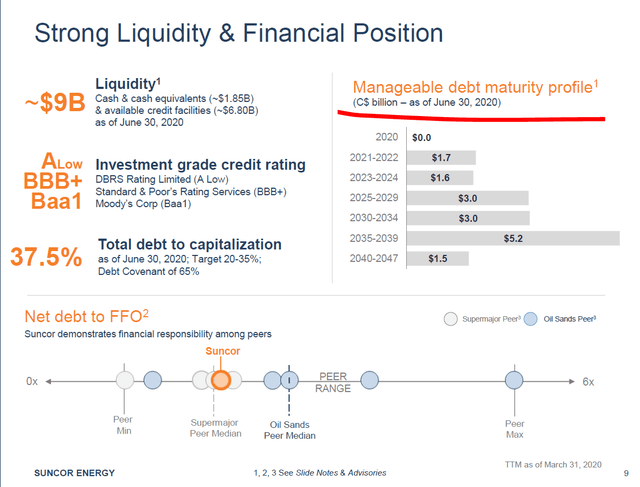

According to the company the debt is manageable and the maturities are far away. But still, the company has C$16 billion of debt (USD $12.12 billion).

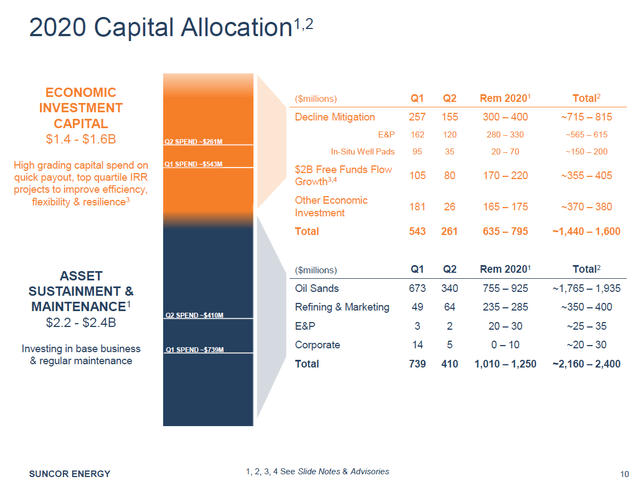

The capital spending for the year has been lowered from C$5.6 billion to C$3.8 billion but as soon as oil price go up, capital spending will increase by C$3 billion. This means that for the long-term sustainability of the business, they need to spend approximately C$5 to C$6 billion per year.

Suncor saved on capex in 2020 – Source: Suncor Investor Relations

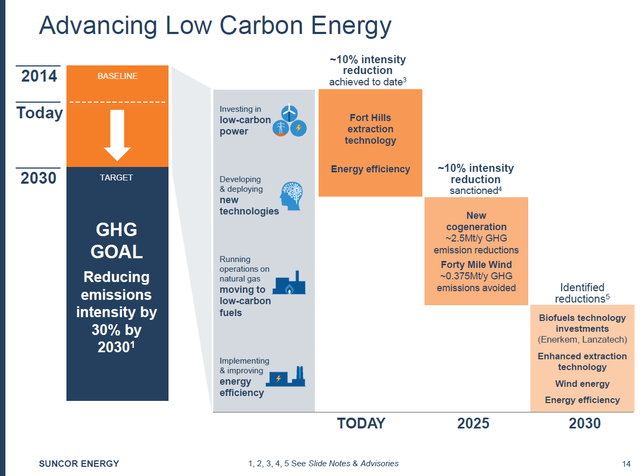

The company looked eager to lower its carbon emissions but those plans have been mostly shelved due the current COVID situation and the required savings.

The company stopped its C$1.3 billion cogeneration project for electricity production and also stopped working on the C$300 million windmill. Such actions among other actions made KLP, Norway’s largest pension fund, divest its Suncor stock position. Institutional investors selling because of their own rules is often a big sign for opportunity. (note: the oil produced in Norway that filled the pockets of the pension fund emits no CO2 – hahaha)

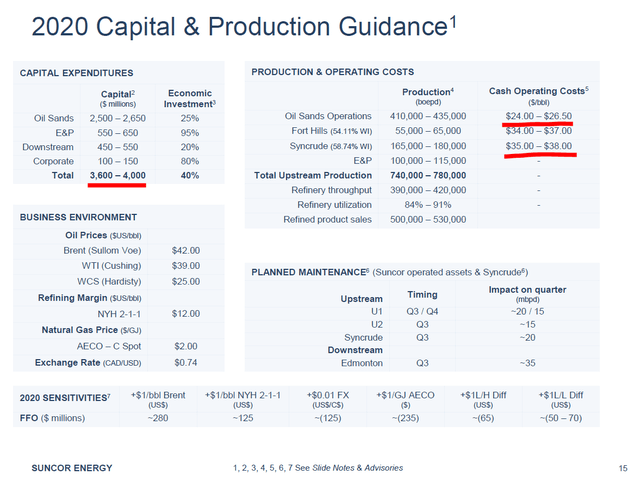

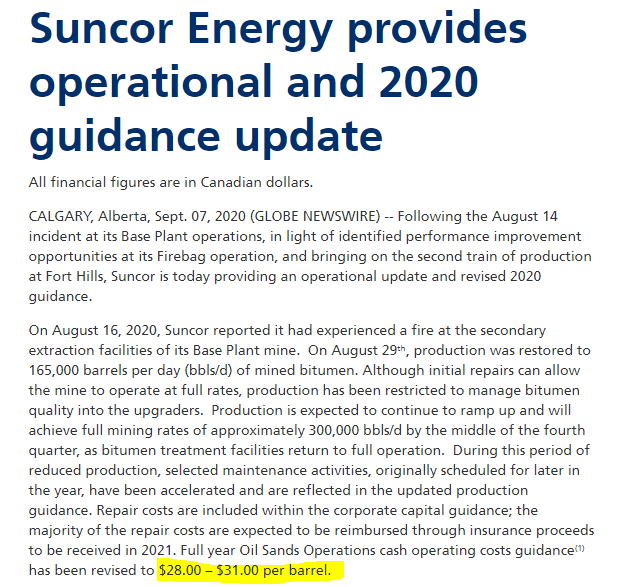

Now, let’s start with the bad news. On the 17th of August 2020 there was a fire that impacted base plant mining operations. Consequently, production guidance for 2020 has been revised downward and costs upward. Oil sand operations operating costs have been increased from the above shown C$24 to C$26 range to C$28 to C$31.

The lower production and higher costs alongside low oil prices puts the dividend and plans detailed above in question. Plus, the second COVID wave and subsequent lockdowns certainly don’t help.

As it all firstly and foremostly depends on oil prices, let me make a cash flow valuation on the basis of the discussed above in relation to various oil price scenarios.

Suncor stock cash flow valuation

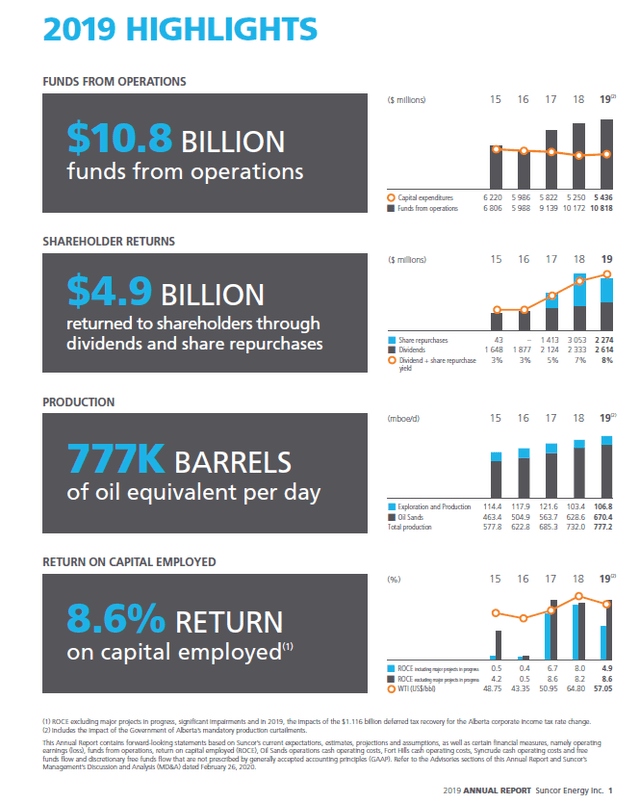

2019 was a good year for Suncor, with distributions to shareholders reaching C$4.9 billion or $3.7 billion. On the current market capitalization, the free cash flow yield is 20% which is high, but in line with what the 2019 cash flow yield is also for other companies like Royal Dutch Shell.

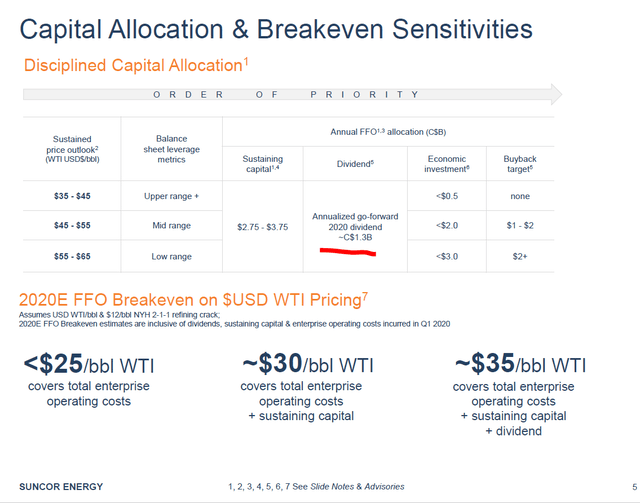

The company says that with lower prices, they can still find C$1.3 billion for dividends, but they have to also cut C$2 billion of spending. The C$2 billion cut in spending can only be temporary because if not production can’t be sustained, so they need to keep spending at C$5.5 billion over the long-term. This tells me that with oil price at $35, net long-term returns from Suncor should be around zero.

To keep the dividend there and production stable the need at least $50, where they would increase the necessary spending back to C$2 billion and then perhaps have another billion left for buybacks. Thus, with oil at $50, you can expect a free cash flow yield of C$2.3 billion from Suncor.

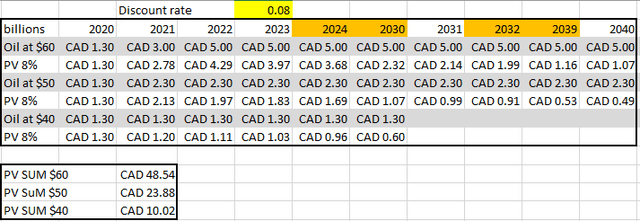

With oil at $60, we are at 2019 levels where free cash flows should be C$5 billion, payments to shareholders around C$3.5 billion for dividends and buybacks while the difference would be used to lower debt.

If I assume the situation being as is for the next 20 years. I am being conservative and taking the final 6 years of production to cover for the costs of cleaning up etc. With oil at $60, the present value of Suncor with an 8% discount rate is C$48 billion or $36 billion, with oil at $50, we are at C$23 billion or $17.42 billion and with oil at $40, I have assumed that the company might pay dividends for the next 10 years and that will be about it.

What the market is actually pricing Suncor at now is oil at $50 for the longer term, and not oil at $60 how most western companies expect. I have recently looked at Lukoil and they make their assumptions with an oil price of $50 while other Russian producers go even lower, to $40. Plus, it is interesting that Lukoil has stopped focusing on growth and switched to buybacks and dividends as the most valuable strategy for shareholders, something few western producers do as it is all about growth there. Growth in a sector with headwinds can be a very costly strategy.

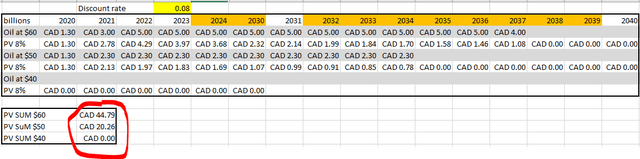

Now, if this would be a business that is surely a going concern forever, we could disregard the debt of C$16 billion but this business, as all mining businesses, has a finite life. If I deduct the C$16 billion of debt that will have to be repaid at some point in time from the long-term cash flows in the years prior to 2040, I get an even lower value for Suncor.

Suncor stock dividend and investment conclusion

The one thing related to oil stocks that I am 100% sure of is that oil prices, and consequently oil stocks, will be extremely volatile. Just a $10 change in oil prices changes Suncor’s free cash flows by a few billions, and the same applies for other oil stocks.

The thing retail investors might not be pricing in is the time limit on operations, at some point, without significant investments in new production, it will be over for an oil company and that has to be included in the valuation. The new investments will not be profitable if oil prices are not at a certain level which will depend on demand and competition.

On top of the valuation that assume business as usual for Suncor, we know that will likely not be the case as the recent fire showed. Another thing I am pretty sure of is that there will be many issues ahead, from production issues, environmental and likely legal issues among other possible issues.

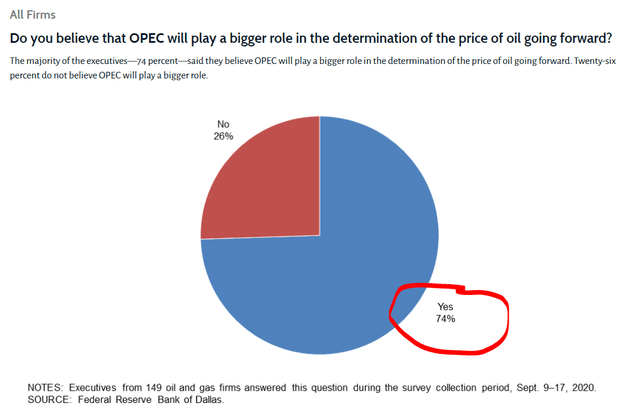

Thus, I would say, Suncor is actually fairly priced by the market now from a long-term investing perspective. The recent decline could be thanks to the negative news from the fire and general bad sentiment, but it all will depend on oil prices. OPEC+ still controls what is going on and 74% of North American oil executives think OPEC will have an even bigger impact on oil prices.

FED’s oil interview – Source: Dallas FED

On top of all the above, Suncor’s performance will also depend on what some people in Saudi Arabia or Russia decide which increases the discount one should use when analyzing a business like Suncor.

That is from an investing perspective and a long-term buy and hold strategy. From a more speculative, medium term perspective, it is likely oil will rebound and consequently the same will happen to Suncor’s stock. If in 2022 we see oil at $60, the market might price that for the longer term and consequently the upside for Suncor stock would be around 100%.

Suncor dividend

With businesses that have a finite life, I wouldn’t focus too much on the dividend. Suncor’s dividend in good with a yield of 5.5%, but to recoup you initial investment, you need 20 years if there is nothing more than the dividend. Therefore, don’t just focus on the dividend but me more opportunistic, big pension funds can’t trade as you can.

See how the above fits your portfolio, investment strategy and investment requirements.

Please subscribe to my newsletter to get notified when a new stock analysis is published.