Palfinger Stock Analysis – Good But Not Good Enough

Palfinger stock analysis content:

- Palfinger stock price overview

- Palfinger business overview

- Palfinger stock fundamentals

- Palfinger dividend

- Palfinger investment thesis

This Palfinger stock analysis is part of my full analysis of the Austrian stock market. Here is the list with all Austrian stocks analysed.

Palfinger stock price overview – VIE: PAL

Auch! Over the last 15 years, stock market investment returns for Palfinger investors have been zero. The only reward they got was the dividend and that isn’t much with a 1.58% dividend yield.

The company is a family owned business, like many Austrian businesses are, where the Palfinger family owns 56.6% of the company.

1999 IPO investors did pretty good as the stock increased 4 times, but the 15 years of negative performance are a thorn in the eye. Let’s see whether the next 15 years might be better for Palfinger shareholder.

Palfinger business overview

Palfinger makes hydraulic lifting systems.

Given the above figure, Palfinger’s business depends on activity in the construction sector, agriculture, forestry, infrastructure, railway, transports etc. In short, it depends on economic activity.

Let’s take a look the fundamentals and financials.

Palfinger stock fundamentals

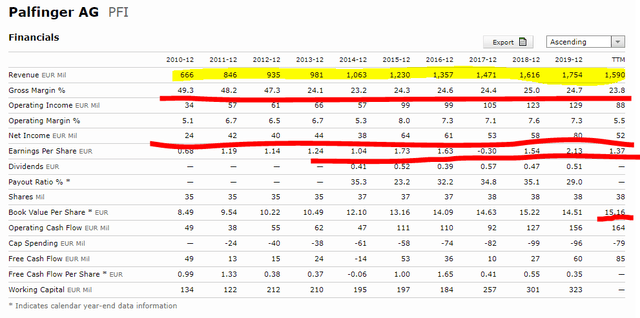

The company managed to almost triple its revenues over the past decade which is not bad. Also, net income tripled when comparing 2010 and 2019.

Given the current stock price of EUR 22, the stock is still trading above book value and at a price to earnings ratio of 20+. Also, given that the company managed to reach earnings of EUR 2.13 only in 2019, these are the issues we have to see about. To become a good investment Palfinger should grow earnings to at least 2 EUR per share and keep the constantly above that level.

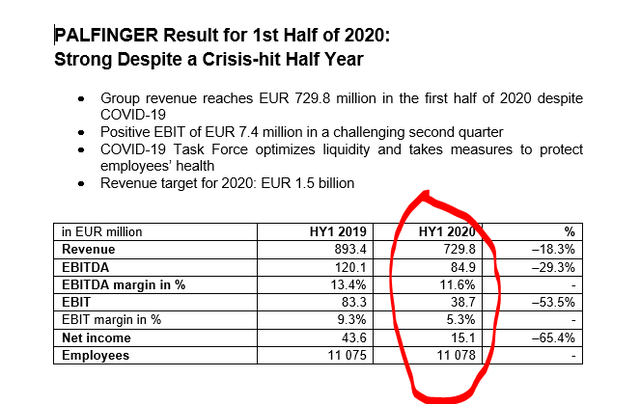

The recent COVID-19 environment certainly didn’t help with the situation as revenues declined 18.3% over the first six months of 2020 and net income declined 65%.

Total debt to assets is 63% which is on the higher side of Austrian family owned businesses and makes it even riskier as an investment.

Palfinger dividend

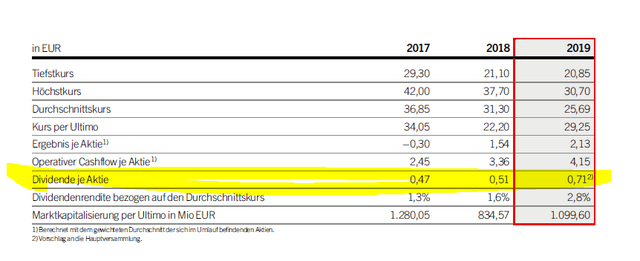

They have been increasing the dividend over the last years, but it is still a small yield and given the business environment, where they don’t really have a competitive advantage, I don’t see how they can perform much better. If they had one the margins would be better.

Palfinger investment thesis

There are businesses that are good family businesses but that don’t really have the strength or the advantage to do greatly over time. The family cashed out in 1999 at the IPO, and is receiving a dividend that is likely ok for them.

PALFINGER AG pursues a continuous dividend policy, which provides that approximately one third of the annual profit is to be distributed to shareholders. It is unlikely the dividend will be high next year.

The way for this to be a good investment would be through an acquisition. However the stock price is constantly above any kind of attractive level for a buyer. Free cash flows have been between 10 and 50 million EUR per year over the past decade. Thus, at a market capitalization of EUR 830 million, it is hard to find a buyer willing to pay 20 times free cash flows in such a cyclical sector.

To conclude, given that there is no competitive advantage, that the activity depends on the general economy, also interest rates given that those buying such tools also look at the financing behind the purchase, I would say Palfinger is a good business but not more than that. Investors can likely expect a volatile dividend ahead and, a higher stock price when there is a good business year. All typical for a cyclical stock.

I think there are better stocks out there. Please check my Stock Market Research Platform for businesses that will do better over time, pay higher dividends, make more money and are less sensible to general economic activity.