OMV Stock Analysis – A 5.6% Dividend Yield Is Good, But…

This OMV stock analysis is part of my full, stock by stock, analysis of the Austrian Stock Market. You can find the complete list of Austrian stocks here. If you prefer watching here is the video, full OMV stock analysis article continues below:

OMV stock price and stock overview

OMV stock is still down 50% from the November 2019 peak. I find it always incredible how the market can’t grasp the cyclical nature of oil stocks pushing them to sky high valuations in good years and punishing them in bad years. But, we are here to take advantage of the fundamental opportunities the irrational market often creates.

OMV stock ticker: OMV – traded in Vienna, Austria

OMV ADR ticker: OMVKY – 1 share equals 1 ADR

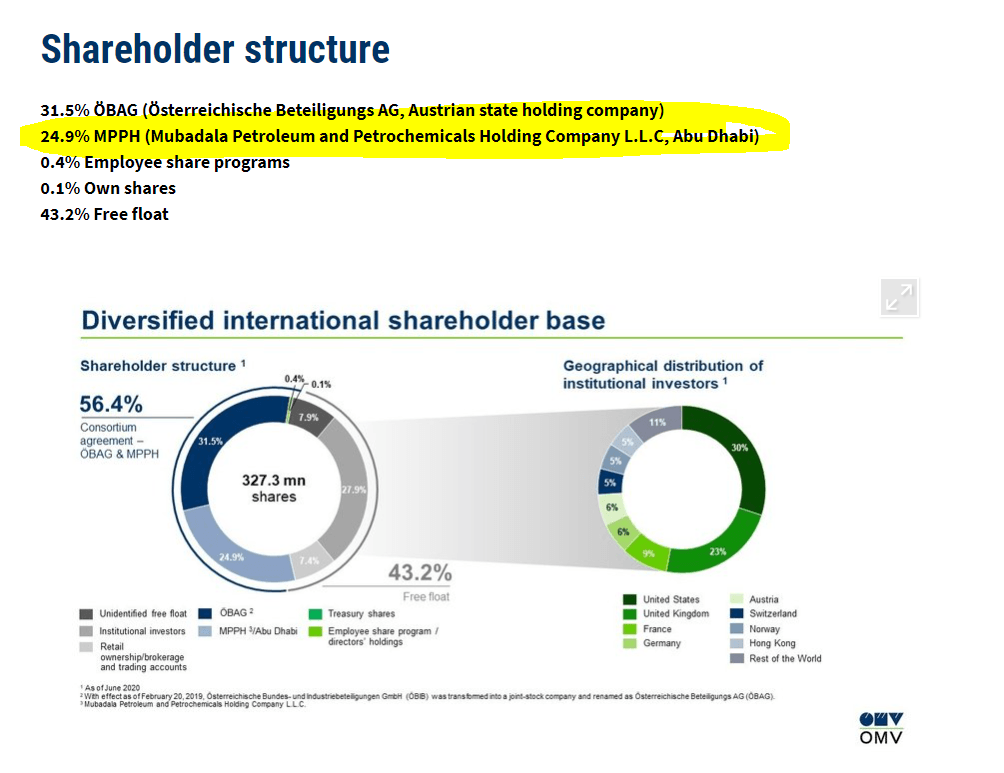

OMV is a mostly government owned company and it does transactions with related parties like the recent Borealis acquisition. This is often a red flag, alongside the government/political ownership but let’s look deeper.

This article will analyze OMV stock by covering the following:

- OMV business overview

- OMV stock fundamental analysis

- OMV stock dividend

- OMV stock valuation

- OMV stock investment conclusion

OMV business overview

OMV is an integrated oil company. Therefore, OMV’s profits depend on oil prices and margins related to refining, byproducts, regulations etc.

Given the scale of OMV’s business, the best way to value it is by looking at how it performs at a certain oil price level. I prefer using a low oil price of $40 so that I have a margin of safety when making an analysis where the any upside comes as a bonus.

If you look at how OMV markets itself, it is not much different from other oil majors, so they don’t have a clear competitive advantage like Gazprom has in the form of low production costs, huge reserves and pipelines that you might want to base your investment on.

Further, within the oil business it is always about balancing between opportunity and risk. OMV is now cutting on investments, limiting acquisitions and project and even divesting things. As others do the same, in a few years we might see undersupply and an oil price spike. At that point, it will be time to sell and then wait for a new bottom in the cycle.

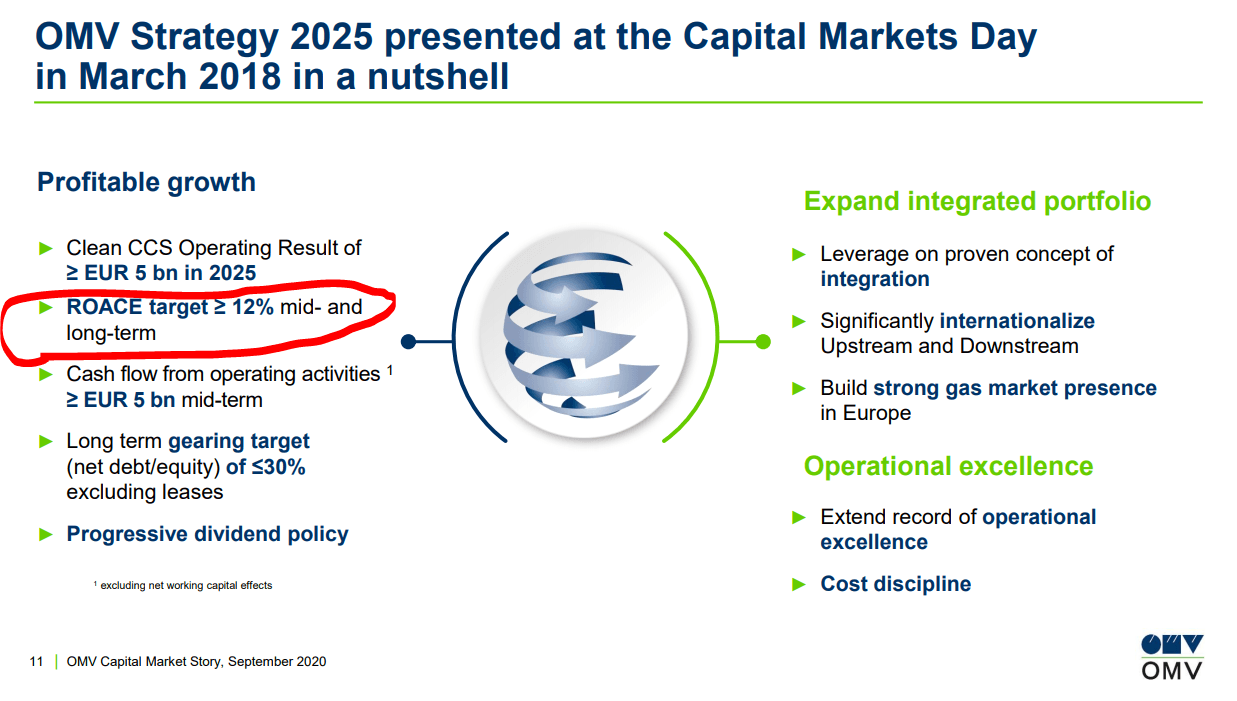

OMV’s target is to keep growing and to have a ROACE (return on average capital employed) of above 12%. That is the target most oil companies have but it is a target that doesn’t depend on the company. The ROACE result depends on oil prices and what your competition does.

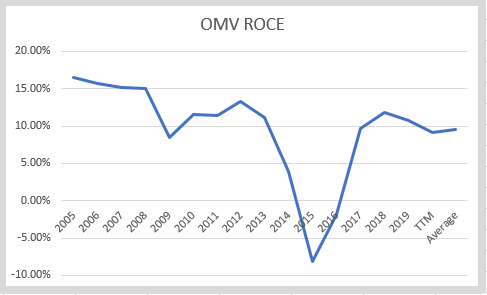

OMV’s ROCE will remain volatile and will depend on oil prices. I would expect its ROCE to decline in 2020 given that oil prices might remain low for longer so they will definitely miss their average target. But, for us investors, the key is to buy when cheap and nobody likes it and sell when the financial environment is exuberant about oil stocks.

The key with cyclical stocks is to buy when the fundamentals and metrics look bad, because that is usually the time the stock is cheap and sell when things look great. The best time to buy OMV stock was 5 years ago, when the ROCE and net income were negative.

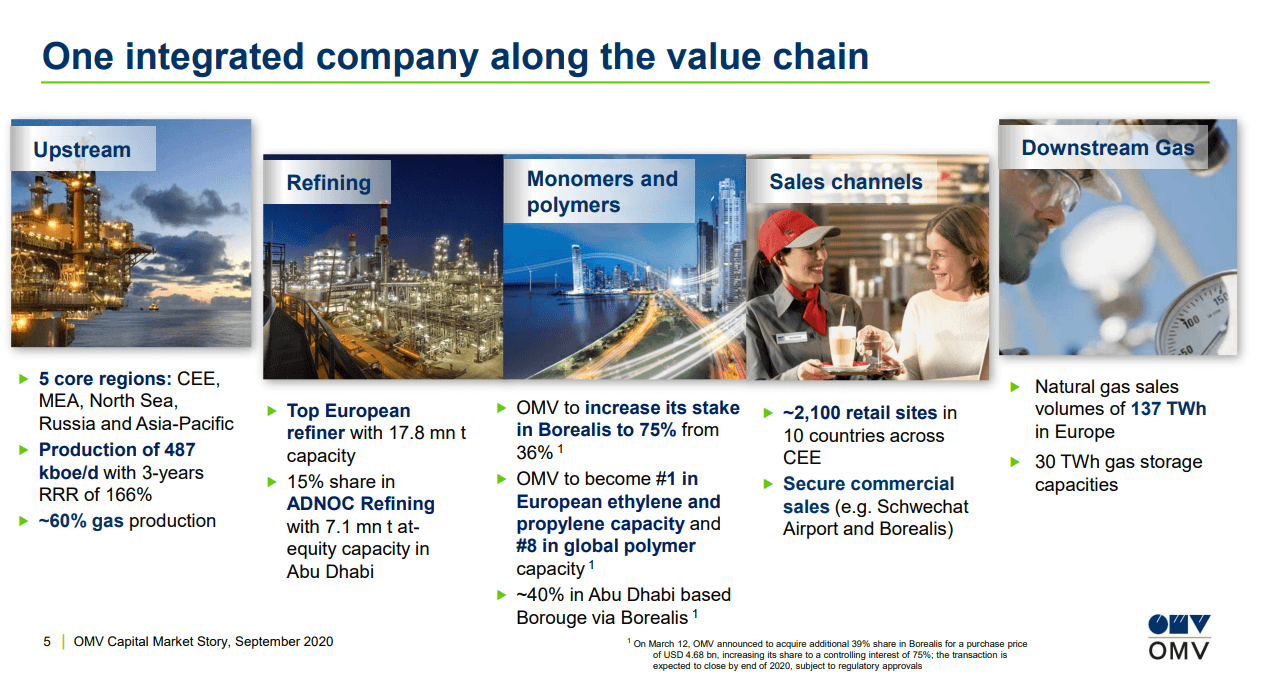

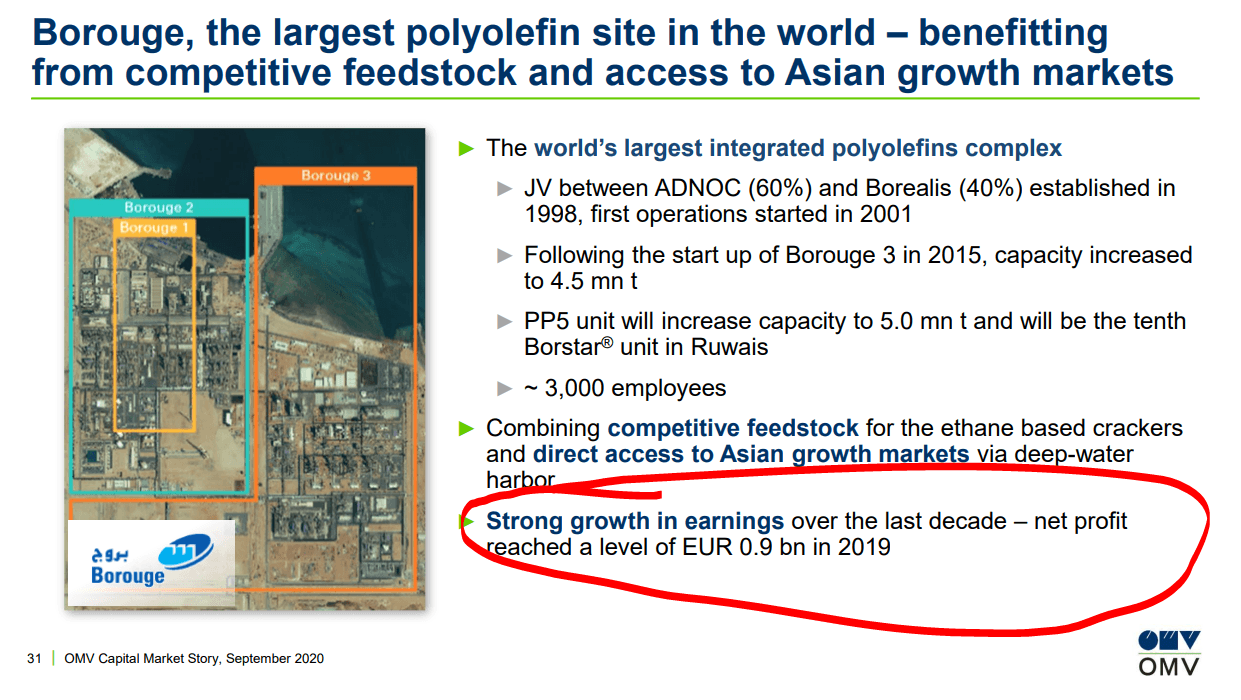

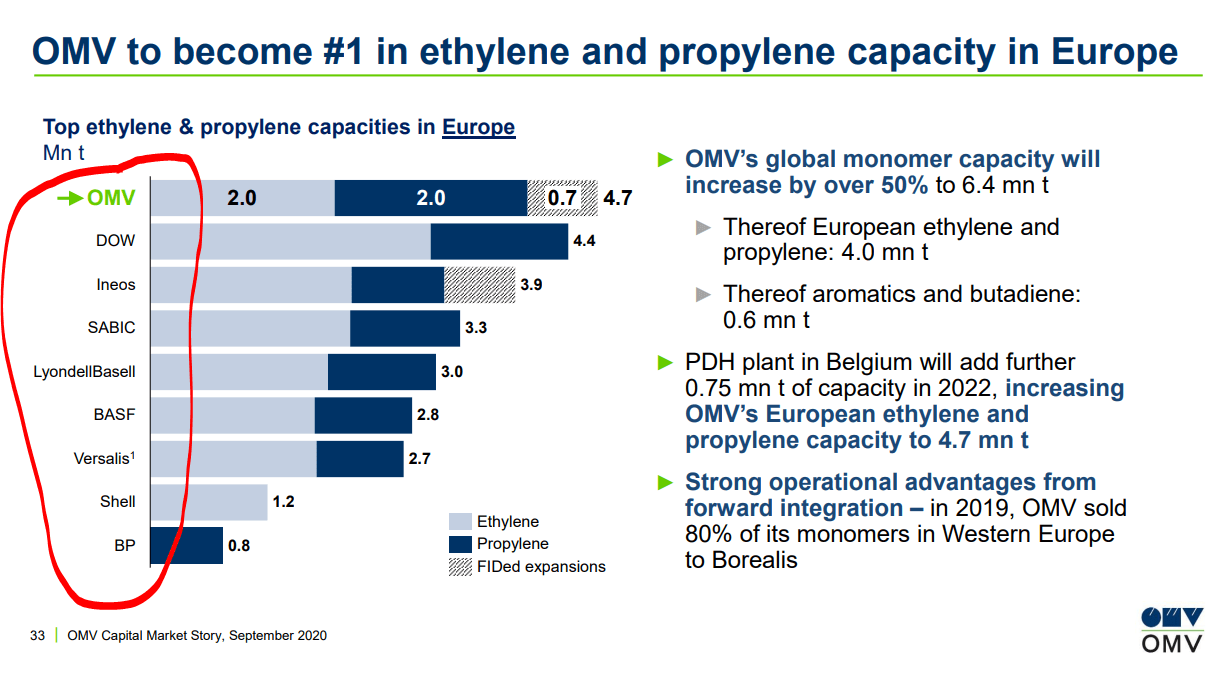

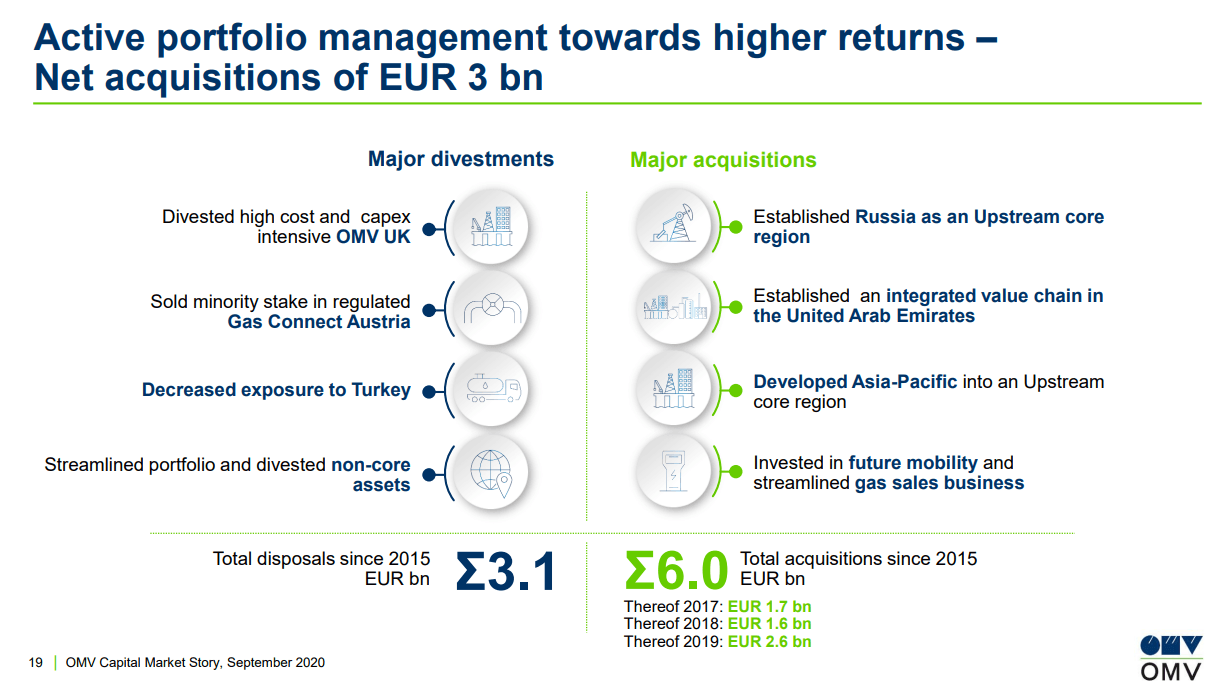

OMV recently increased its stake in Borealis and the deal was announced on March 6, 2020. Given that the owner of Borealis has also a stake in OMV of 24.9%, it is always tricky to assess these transactions between related parties. You don’t know whether the owners are taking advantage of you as a small shareholder or increasing value. Borealis is the world’s eighth largest producer of polyethylene (PE) and polypropylene (PP), and OMV decides to go heavy into that business now when prices are low.

OMW will pay $4.68 billion for a 39% stake in Borealis that has made 0.9 billion EUR in net profit in 2019. Given prices of what Borealis is selling are down, OMV paid approximately 12 times 2019 earnings, likely to be much higher in 2020 earnings. They actually bought at peak earnings because the company has been growing earnings over the last years. Why am I not surprised given it is a government owned political business?

It is a purely cyclical, extremely competitive business where margins depend on investments made in the sector in relation to demand and given the low interest rates, your competition can decide to invest in now facilities at any point in time.

It seems the most important reason for the acquisition is to make OMV look more sustainable.

Another typical activity for oil businesses is that they sell the things that didn’t work and invest in new projects.

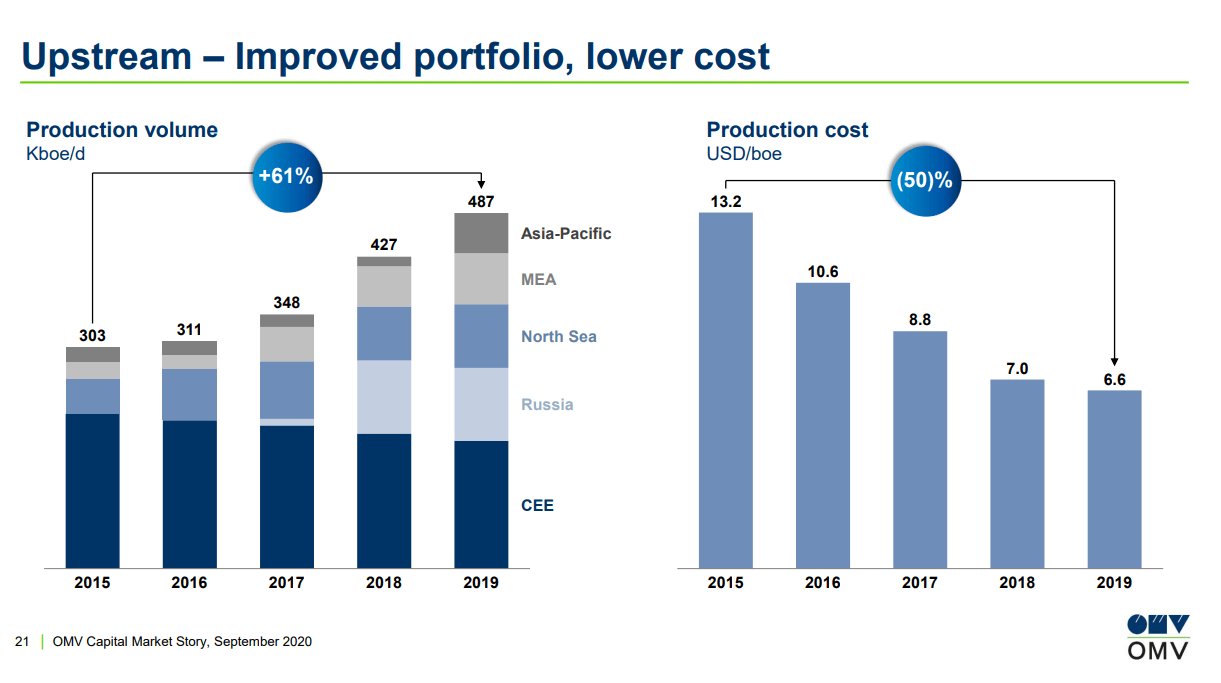

The good thing is that they lowered their production cost which should allow them to be profitable at any oil price level.

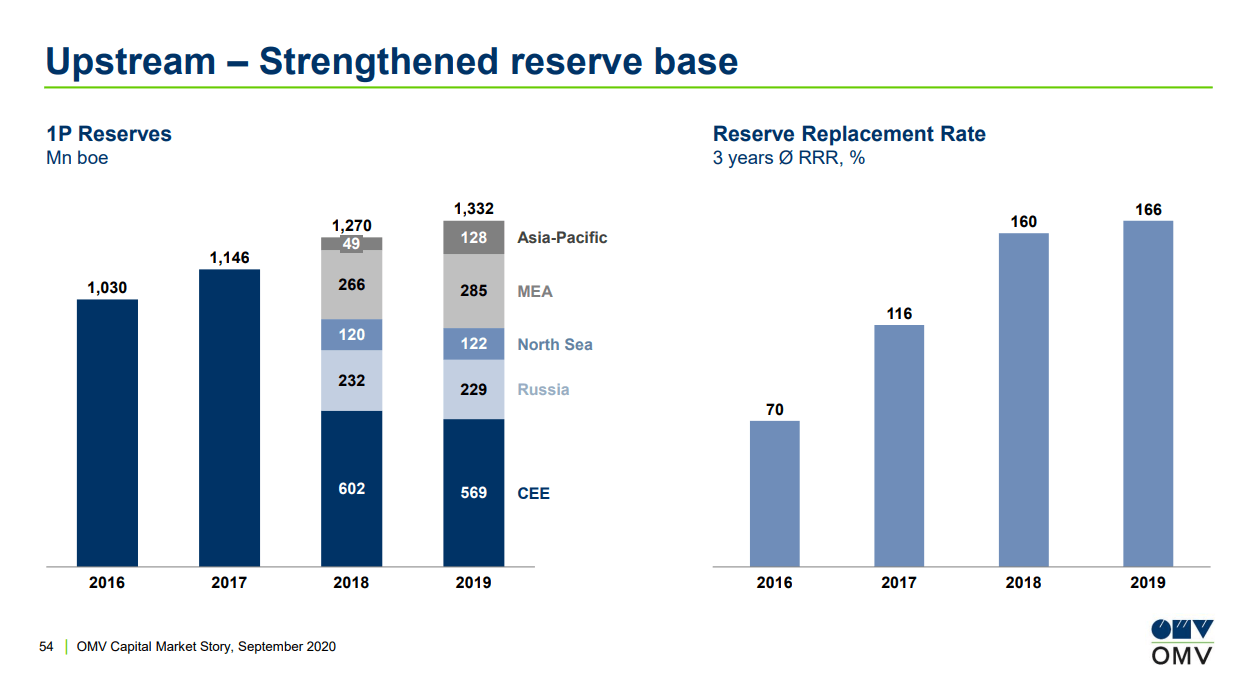

However, if they produce 487 Kboe/d (182.5 mn boe) and their reserves are 1,332 mn boe, they need to replace there reserves at a relatively very fast rate because they have only 7 years of production ahead. This short-term situation can be very costly if replacing reserves becomes costly or more difficult due to the lower investments. However, 7 years is normal within the oil industry but I would prefer it was much longer because it will and it does require a lot of investment to keep up.

Let’s see how the above impacts fundamentals and what we can expect long-term as investors.

OMV stock fundamental analysis

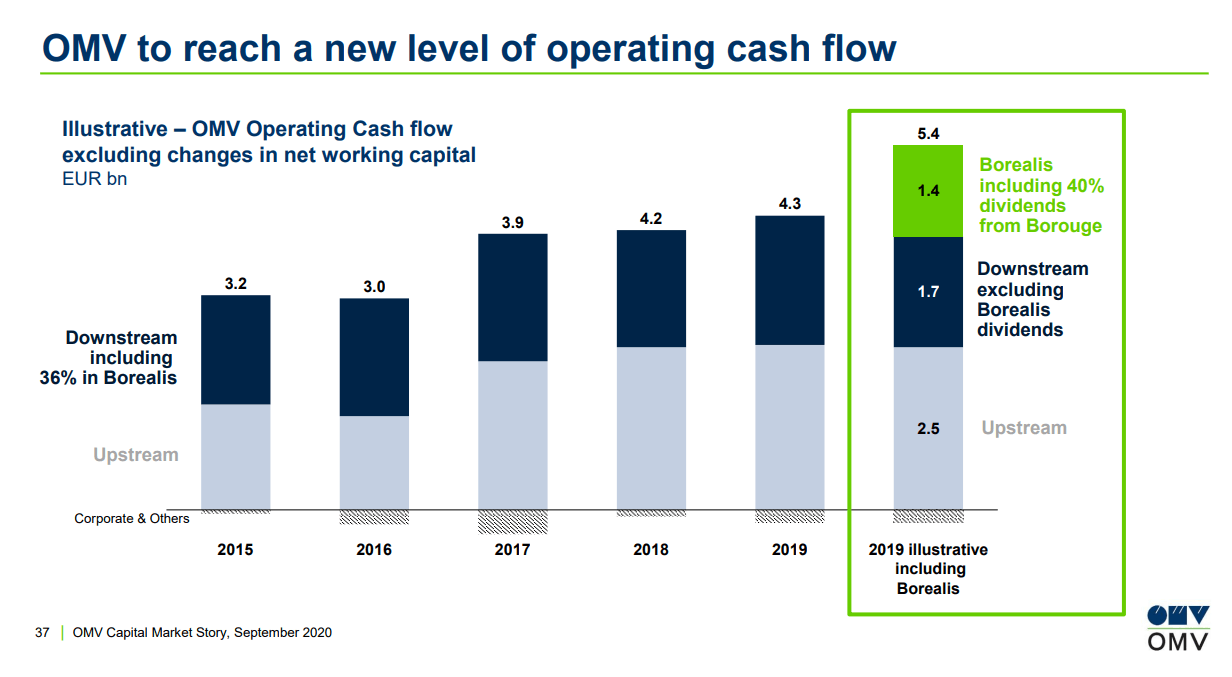

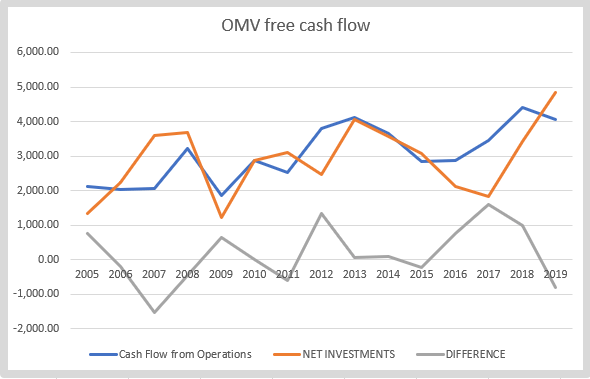

Operating cash flows have been good over the past 5 years but operating cash flows are a nice marketing metric, nothing more.

If I look at operating cash flows from their balance sheet, deduct what they spent for PP&E, business acquisitions and investments, the free cash flows aren’t much.

On a cash flow basis, I don’t know whether OMV has the capacity to create real shareholder value.

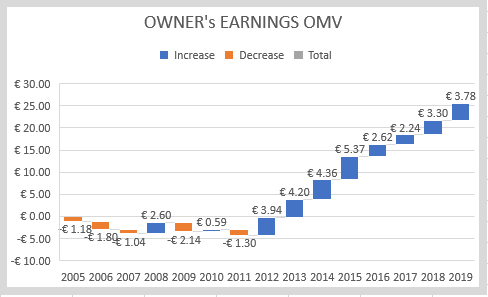

If I take a look at earnings, those look good over the last few years, but the situation has been really ugly prior to 2012. Cumulatively OMV did create 25 EUR of shareholder value over the past 10 years, but that is just 2.5 EUR per year, which is low and much of that is invested somewhere where we don’t know whether value will keep coming like it is the case with Borealis.

The owner’s earnings average of 2.5 EUR are close to what the dividend is, so best to value OMV stock on a dividend basis.

OMV dividend analysis

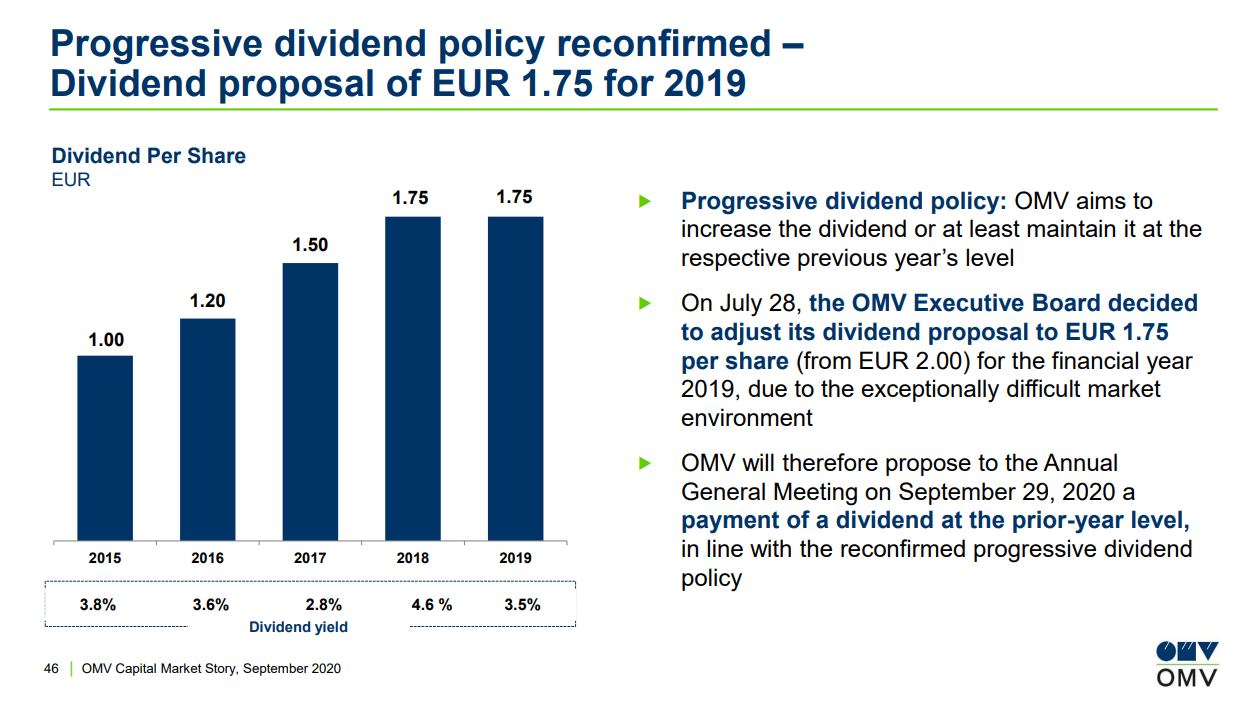

OMV is a dividend stock and their current proposed dividend of 1.75 EUR gives a yield of 6.4%. To pay that, they need 570 million EUR.

I think they will be able to pay such a dividend for longer as 570 million is not much given their balance sheet, the easiness of getting in debt in Europe and the constant investments they make to keep production up.

However, I also feel that OMV will always remain a complicated, ugly business dividend payer. A company without a clear advantage that can only benefit from higher oil prices for a while before the competition comes in. Buffett would describe OMV’s business as a business that requires significant investments to remain competitive and where little remains to shareholders. Given that the sector has headwinds coming in the form of renewables and environment requirements, it is unlikely OMV can offer more than the dividend.

OMV stock valuation and investment strategy

Therefore, to value OMV, as an investor, there is nothing else to focus on than the hope to get a dividend and keep getting that dividend for longer.

I would love to use the 5 billion EUR in operating cash flows for valuing the company, but you see how even the market gives OMV a market capitalization of just 8.8 billion EUR, thus the stock is trading at 1.76 times operating cash flows.

On what is the value of OMV’s stock, it all depends on oil prices and the market, nothing else. If oil prices don’t rebound, and OMV gets into a rough patch, the stock might easily crash another 50%, especially if the dividend is cut. The ugly truth is that it this will happen at some point in time because OMV doesn’t have any competitive advantages, it is simply a price taker.

From a long-term investing perspective, I don’t like investments where I know there is an end to them, even if the dividend looks attractive. A 5.6% dividend yield for 10 years isn’t much if you get nothing afterwards. Even if you get just 50% of what you invested into it, despite the dividend, it does not turn into a great investment.

I think there are much better long-term investments out there than OMV so I’ll focus on those and leave OMV to pension funds and other index funds that have to buy it because of its market capitalization, geographic and sector exposure.

In the short term, anything can happen, they just need 285 million to push their dividend up 50% and consequently push the stock price higher too. That might happen, especially if oil prices go up, but it will likely be a short-term consolation prize. Be ready to sell if that happens.

All in all, I think there are better stocks to invest in for retail investors. Please subscribe to my newsletter to get notified when a new analysis is published and check my Austrian stock list for other interesting Austrian stocks, some much better than OMV.