Norfolk And Southern NSC stock analysis (A Cash Cow)

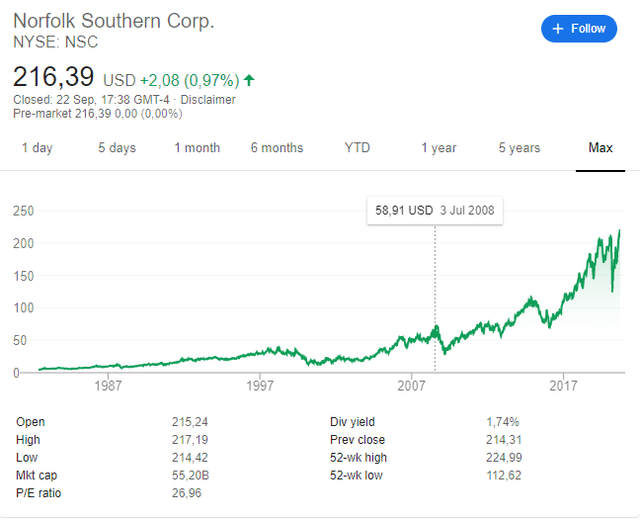

Norfolk and Southern stock price analysis

NSC stock is another railroad stock that has done really well. Shareholders have been significantly rewarded as results improved and valuations expanded.

What interest us now is not what happened, but whether Norfolk Southern is now a good stock to buy. In order to give an answer here is the content of this Norfolk Southern stock analysis:

- Business overview

- Norfolk Southern stock fundamental analysis

- Norfolk Southern dividend and buybacks

- NSC stock investment thesis and comparison

This NSC stock analysis is part of my full railroad stocks sector analysis. Here is the:

If you prefer enjoying a coffee and listening to the content, here is the video on rail stocks, article continues below.

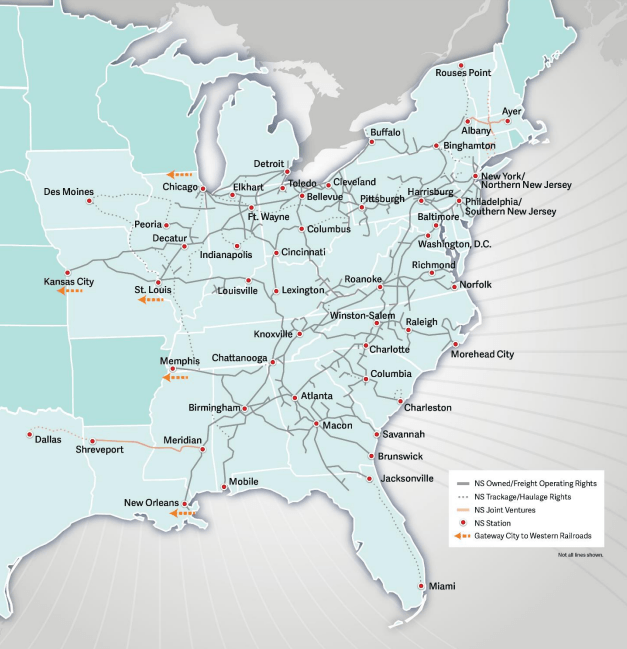

Norfolk Southern business overview

Norfolk Southern is another class-1 North American railroad focused on the east of the country.

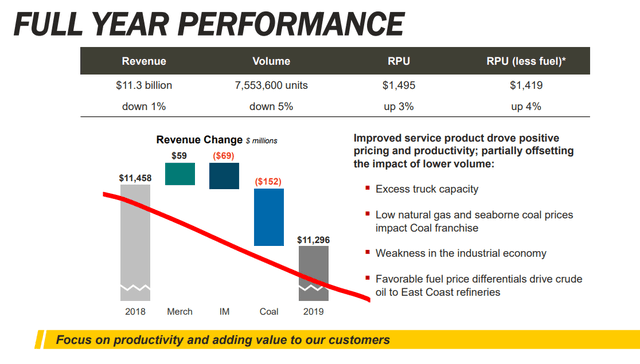

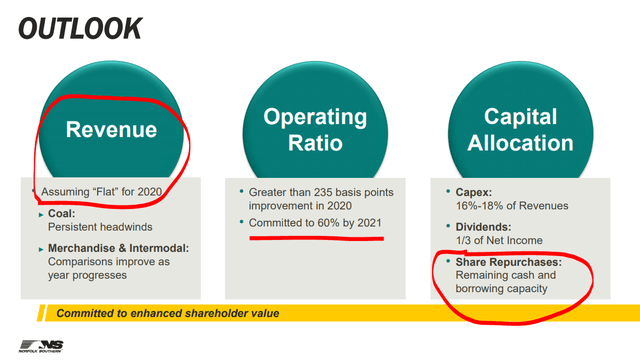

Unfortunately, NSC is one of the railroads out there that is seeing its revenue decline over time.

The market seems not to be concerned by the revenue decline as the whole focus is on improving operations and profitability to increase buybacks. So, let’s discuss that which seems the key.

NSC stock fundamental analysis

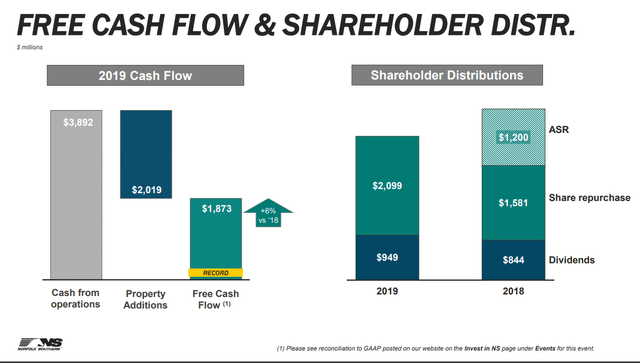

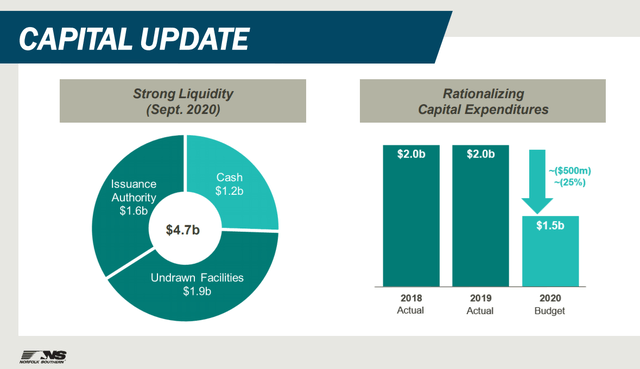

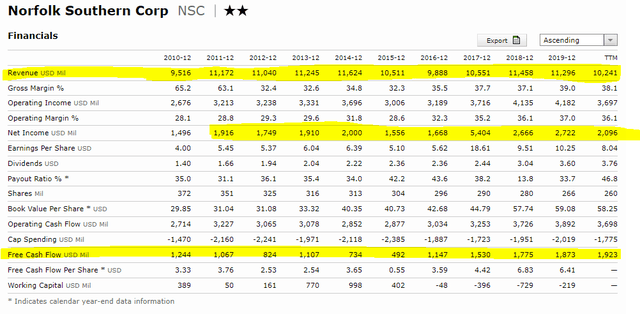

Free cash flows have been $1.8 billion in 2019, likely to remain around that number in the future as capex requirements have been stable.

There will be some savings on capex in 2020 but I assume capex will be stable at around $2 billion long-term.

Nothing much to add here, it will all depend on what happens with the economy and demand while operational improvements should keep cash flows high.

Norfolk Southern dividend and buybacks

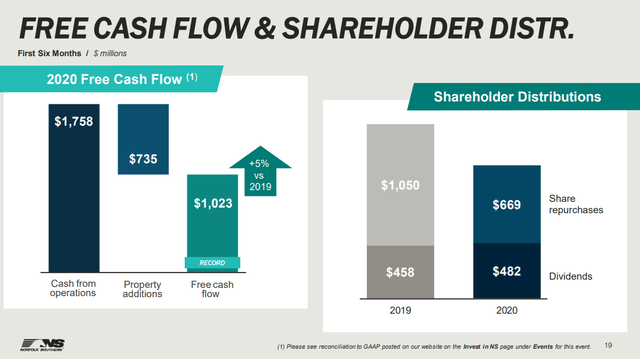

The company spent $955 million on dividends in 2019. At the current market capitalization of $55 billion it gives a yield of 1.7% which falls on the higher end of the dividend yields in the rail sector.

Share repurchases have been a bit lower in 2020, but I assume the focus will remain on maximizing those.

The company’s focus is to maximize buybacks so this is a pure cash cow to be milked as much as possible given that growth will be tough to create. This is also an indication for other railroad stocks that still hope to reach growth, growth that at some point has to stop because of natural forces.

Revenues didn’t grow at all for Norfolk Southern over the past decade but free cash flows doubled. This allowed for a 30% decline in the number of shares outstanding thanks to buybacks and for a 150% increase in earnings per share, even if net income didn’t increase that much.

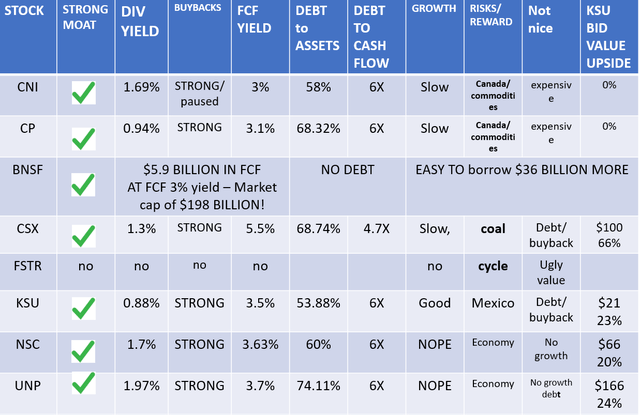

All in all, I would say the company will most probably keep making $2 billion in free cash flows per year in a good environment. This gives it a 3.63% cash flow yield which is in line with what other rail stocks offer.

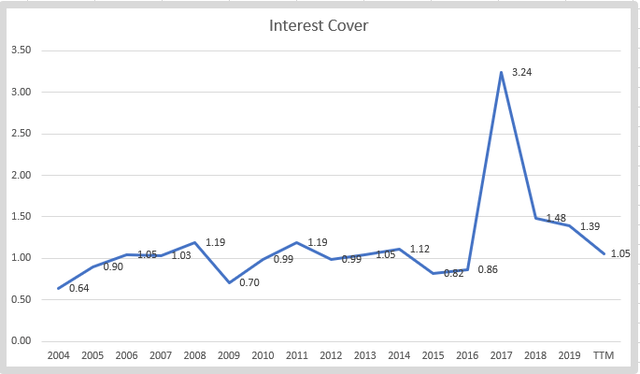

Interest cover is on the lower end for rail stocks.

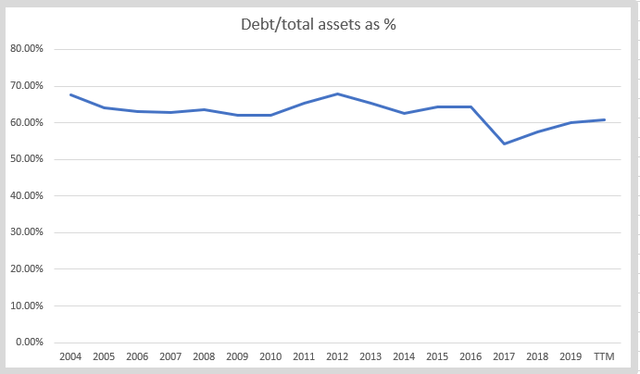

While debt to assets is average at 60%. Long-term debt is $12 billion which is 6 times cash flows, also is in line with other rail stocks.

NSC stock investment thesis and comparison

NSC doesn’t differ much from other railroad stocks. Debt, free cash flows and business risks are all in line.

Compared to the KSU takeover bid, there could be a 20% premium on the stock price but I think few can come up with $66 billion to take it over. I would argue there are better investments out there even if the management will do whatever possible to keep the stock going up. That is bound to stop at some point in time so think about switching to stocks that offer a better long-term outlook. If you with to stick to railroads, Burlington through Berkshire might be an idea.

For more information on other railways stocks, please check my comparative railway stocks article with links to detailed analyses such as this one.

Transportation stocks at multi year lows are airport stocks, another sector I have analyzed lately.

If you like this comprehensive approach to investing, please subscribe to my newsletter to be notified when I analyse a new sector. To check my past analyses, covered stocks and portfolios, feel free to check my Stock Market Research Platform.