Nestle Stock Analysis – 5% Enough For You Given The Value?

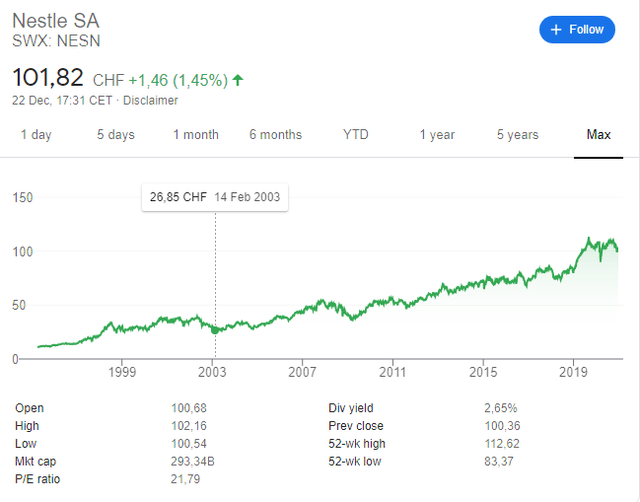

Nestle Stock Price Overview

Nestle, like Unilever, is another historical compounder. Shareholders have been rewarded extremely well over time not even considering the additional returns from the strengthening of the Swiss Franc CHF.

However, the dividend yield is relatively low for a company that has been seeing declining revenues over the last years (albeit measured in CHF). On the other hand, I enjoy my Nespresso so we could say that the company has a strong brand and customer loyalty. Let’s analyse Nestle stock so that you can see at what price level is Nestle a good fit for your portfolio. Here is a video analysing Nestle stock while also discussing Unilever and Kroger.

Nestle Stock Analysis – Business Overview

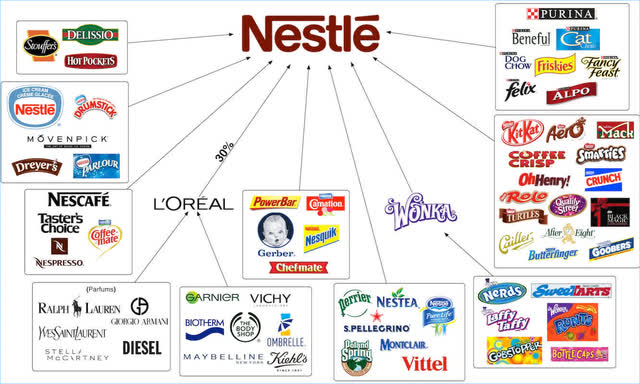

I don’t think I have to spend too much time discussing Nestle’s business given the global reach of its brands.

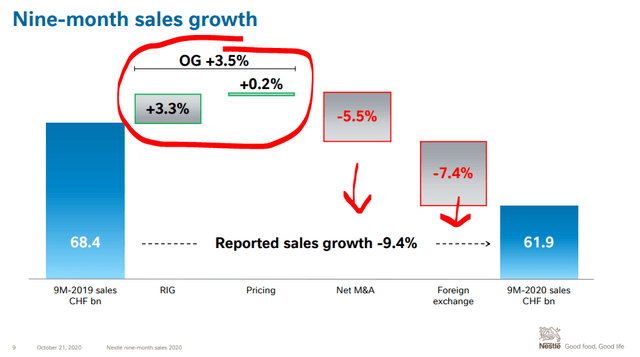

The problem with nestle is not that much growth as it is the case with Unilever because Nestle, thanks to the quality of its brands, can still reach organic growth of 3%, the problem is the Swiss Franc and asset sales.

Companies like Nestle and Unilever focus on maintaining what they have and therefore sell all the businesses with lower margins. I would assume long-term growth to be slower than the 2020 3% because the lockdown boom will likely subdue.

Nestle’s business quality is certainly of the highest globally as it sells products we all enjoy, global middle class growth will likely help its growth over time and thus it is unlikely we see nasty surprises. Therefore, it is all about the price you are willing to pay to have a good business like Nestle in your portfolio.

Nestle Stock Intrinsic Value

To calculate the intrinsic value of a stock you need to know what is the value that it delivers to the shareholder. I’ve looked at Nestle’s cash flow statement and the real free cash flows are around 11 billion CHF per year. They have disposed of businesses for 15 billion CHF over the last two years but I will not use that for valuation purposes as those are one of effects.

From the above operating cash flows, adjusting for acquisitions and disposals, I am deducting 4 billion CHF of capital expenditures for tangible and intangible assets, another half a billion for other activities and I get to 11 billion of free cash flows.

This gives me a shareholder value yield of 3.7% when compared to the current market cap. Sales are stable in Swiss Francs and compared to Unilever the company is actually growing when you include the constant strengthening of the CHF.

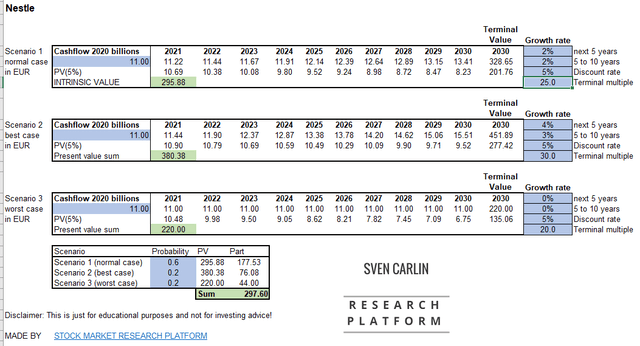

I would assume Nestle will likely continue to grow over time given the coolness of its brands and therefore I assume a growth rate of 2% for the long-term. By using a 10% discount rate which is my minimal required rate of return and a 25 multiple in 2030, the normal case intrinsic value is 200 billion CHF.

In the best-case scenario, with a higher multiple and higher growth rates, the present value goes up to 255 billion CHF while in the worst-case scenario with no growth and a lower terminal multiple the present value falls to 150 billion.

My average valuation of 202 billion CHF is way below the current market capitalization of 293 billion CHF but with a discount rate of 5%, the intrinsic value is close to Nestle’s current value.

So, if you are happy with a 5% long-term return from an investment, a relatively safe investment like Nestle, you might consider and compare Nestle stock with your other portfolio positions and opportunities. I don’t think 5% is bad in the current zero interest rate environment and that is also one of the reasons why the stock had done so well over the past decades with declining interest rates. Before concluding, it is always good to mention a few risks related to the investment.

Nestle Stock Investing Risks

The main risks are interest rates changes and lower valuations. If we see an inflationary period ahead due to all the money printing where Nestle isn’t able to transfer input price increases to customers, with consequently declining margins and a lower valuation, things might get ugly. Further, if there is a crisis, customers might go for the cheaper product versions. I know your dog loves his Purina and you love your Nespresso, but in difficult times it could be something to save on.

Another risk comes from niches companies like Nestle or Unilever do not organically serve. Small “authentic” brands, digital brands with strong social media presence and local Asian brands for example. They try to remedy through acquisitions but the competition there is really fierce and constantly evolving.

All in all, we could say Nestle is a fairly priced great business but offers no margin of safety at current levels.