Metso Stock Analysis – Another Great Business From Finland

Metso stock analysis is another interesting analysis of Finnish businesses. I recently analyzed Nokian Tyres, another good business where you just have to wait for the right price to make a great investment of it. Metso stock is a similar situation.

Metso Stock Analysis – Business Overview

Metso is the shovel and picks seller to miners. As long as the mining industry grows, and given constant global growth and development, there will always be some work for the company.

Metso Oyj is a Finnish industrial machinery company focusing on providing technology and services for mining, aggregates, and oil and gas, recycling, pulp and paper and other process industries. The company employs over 13,000 people in 50 countries. Metso’s shares are listed on the NASDAQ OMX Helsinki, Finland.

Metso stock gives you a piece of a a good business, but a cyclical one and therefore the time to look at such businesses is when things look bad. In 2009 Metso’s stock price was around €8, now it is above €33, thus the market capitalisation increased 4 times, but that is not all.

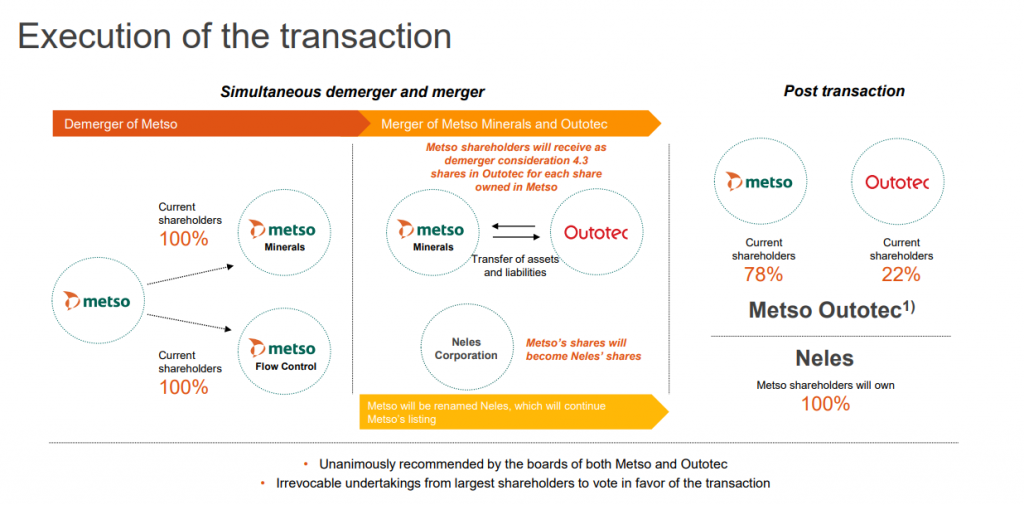

On top of the great performance, in 2013 Metso demerged Valmet Corporation that is in the business of paper, pulp and and power. There we should add €3 billion in market capitalization and another dividend yield.

Plus, they are doing it again, the will make their Flow Control business become a separate company again. Plus, the are merging with Outotec, another Finnish mining equipment company.

They expect the flow company to be re-rated by the market.

So, Metso already delivered significantly in the past. The time to buy this was in December 2018 or January 2016, now the valuation is fair and the upside is not really that stellar. The business will do well, but what you can expect slow and steady growth.

This is a stock to watch when the mining business slows down due to low commodity prices. Mining will survive, so will Metso, thus watch for the rebound. The LTIF fund that we are analysing acquired Metso in December of 2018.

However, the cycle in the mining industry has just begun. In order to prevent the formation of supply gaps, miners need to constantly invest in new mines, new equipment and due to the commodity slump over the past years, investing has been soft. However, going forward investing is picking up, Metso’s back-log is at record highs and it is also likely that the stock will follow.