Nokian Stock Analysis – Buy After The Dividend Cut

- Nokian is a great business operating in a niche market. Past growth has been 8.1% per year and even higher excluding currency issues.

- The company, banking of past success, has entered a new growth cycle. However, their expansion coincides with a contraction in the market.

- The lower revenues and increased capex requirements could lead to a dividend cut, that should be the best opportunity to buy this cyclical stock.

Nokian Stock Analysis Approach – Introduction

This research report, giving a micro analysis of Nokian’s business with the focus on how their story evolves over time, is based on a full tyre stocks sector analysis with a macro overview.

For those who prefer watching, here is the video on Nokian, article continues below.

I have listened to all the presentations from Nokian’s 2018 Capital Market day and to their last conference call where, unfortunately, the story completely changed. For example, in October 2018, the management expected the Russian market to grow at 6%. Actual growth over 2019 was -2%. Given the subdued environment and low visibility, we have to establish a range for the value of the stock, expected returns, risk, margin of safety and then you can see how, and at what price level, this could fit your portfolio, or not.

Figure 1 Nokian Tyres stock price – how things change quickly, from exuberance to gloom

Let’s see what is the real value. I will try to estimate long-term earnings in line with the outlook for the environment and Nokian’s competitiveness.

Nokian Renkaat Oyj Business Overview

Nokian Tyres is a Finnish company selling tyres, mostly winter tyres in Nordic countries, Russia, Eastern Europe and the United States.

Figure 2 Nokian is a 4-country business trying to enter other markets Source: Nokian Investor Relations

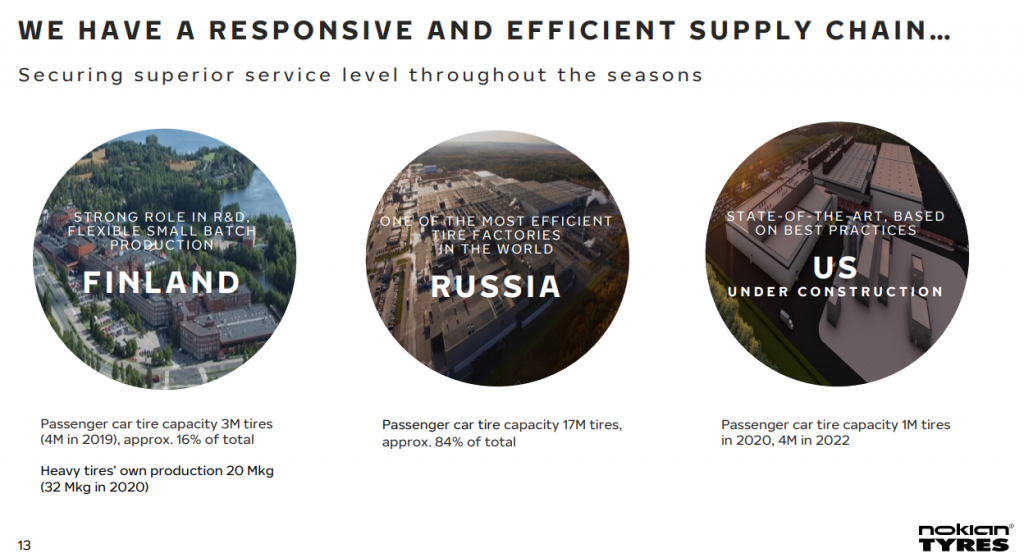

They are pretty well established in Nordic countries and Russia with set distribution networks and market leadership. For example, they own most of their Vianor network in the Nordic countries. Their plan and hope is to grow in the rest of Europe and the United States. They have built a new factory in Dayton that will supply the North American market with a yearly capacity of 4 million tyres and options to grow capacity to as much to 12 million tyres yearly by simply enlarging current construction. In 2020, the Dayton factory is expected to produce 1 million tyres alongside a slow ramp-up.

Figure 3 Nokian’s production capacity is not fully utilized Source: Nokian

The situation is the following; we have 4 million production potential in Finland that is going to be curtailed to probably 2 million due to the current situation in the markets. Workers will have many days off over the next year. The Russian facilities can produce 17 million and Dayton should be able to produce 4 million. In short, they, as many other tyre producers have capacity oversupply and therefore can flood the market easily. It is hard to estimate when will the market situation return to the 2018 level as car sales in Europe, Russia and North America have actually been declining.

Global vehicle sales overview

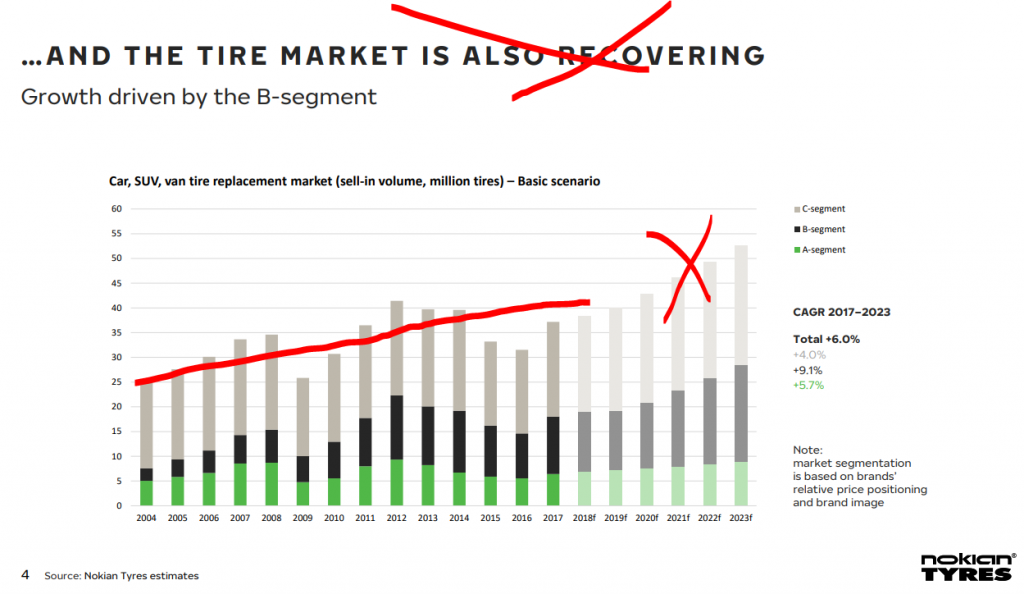

In their 2018 October Capital markets day, Nokian presented a pretty bullish outlook for their business expecting above market growth rates.

Figure 4 Nokian’s growth outlook for replacement tyres Source: Capital day 2018 presentation

They are not present in China as there is no regulation for winter tyres, even the above 2% growth estimation for Russia was too optimistic (their estimate was 6%) and Nordics have also slowed down. Further, the North American market is also in a slowdown.

Figure 5 Total vehicle sales in the US is flat and at risk of a slowdown Source: FRED Economic Research

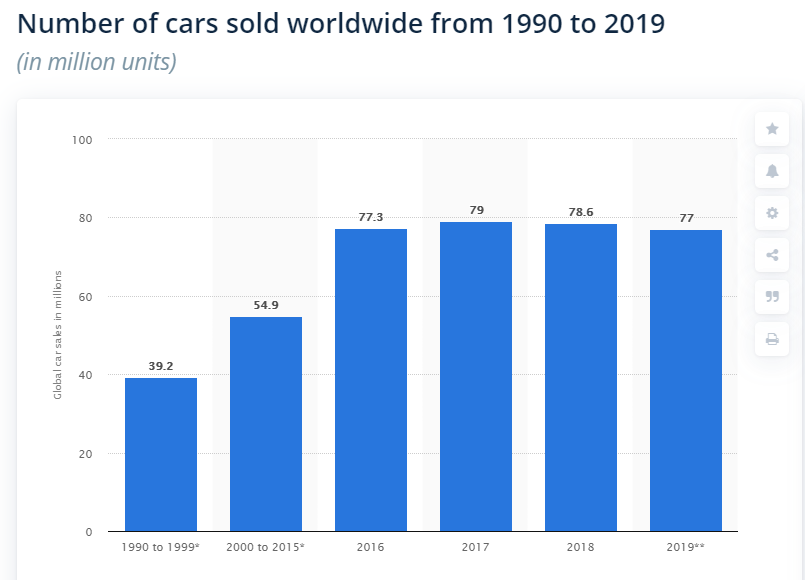

If I take a look at past numbers, Nokian really enyojed a tailwind over the last 20 years as yearly global car sales almost doubled from 1999. But, over the recent years, new car sales peaked. Russia was the growth engine for Nokian, alongside Central Europe.

Figure 6 Global car sales per year Source: Statista

The number of cars on the road went from 670 million in 1996 to the current estimation of 1.3 billion. The number of cars is expected to reach 2 billion in the future, but not in the markets Nokian is focusing on as Asia will be the main driver of that growth.

Globally, car sales have seen their best days. The consequences can be seen reflected in stock prices of most auto makers.

Figure 7 Global car sales per year Source: Bloomberg

The above boom in car sales pushed earnings for the whole sector up, from new tyres to replacement ones. We now have to estimate what will the market look like over the next 10 years, that is the only way we can get a fair and a risk free value for Nokian (what is the value for you will depend on the kind of investor you are).

The outlook for the industry

It is likely that automotive sales will see limited growth in Europe and North America in the future, perhaps even a decline given all the new technologies announced like car sharing and autonomous driving. Demographics certainly don’t help. EU automotive demand has boomed over the last 5 years thanks to ‘free money’ and 0% car loans. Nokian is basing their growth estimations on the premise that the party is going to continue, both in Europe and in the US.

Figure 8 Past car sales trends in the EU by category from 1995 to 2018 Source: SIUlisse data

However, car sales have been subdued lately in Europe.

Figure 9 Car sales in Europe Source: Bloomberg

The above tells me that I don’t know whether Nokian will face similar tailwinds in the future as it enjoyed in the last 5 years in Europe.

Nokian stock risks and outlook

Secondly, something very important for Nokian is the Russian currency, a weaker ruble is also not good given the high amount of sales there. This has also been the reason why their revenue didn’t grow since 2013 as the ruble lost 50% of its value against the euro.

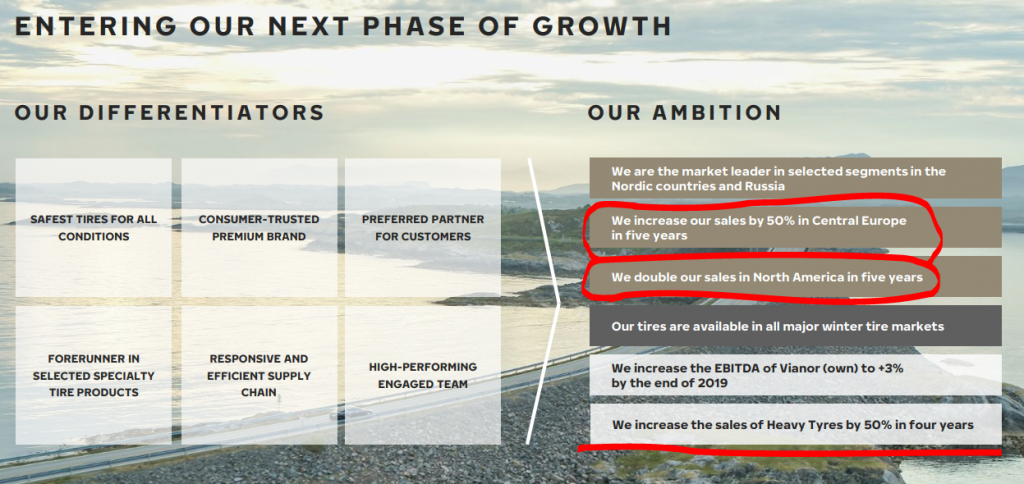

Nokian’s growth ambitions have been pretty bold; 50% sales growth in Central Europe, double growth in US and heavy tyres sales up 50% too.

Figure 10 Nokian’s positive growth ambitions were baked into the 2018 stock price

Source: Nokian

On net sales of 1.6 billion with 12% of it in the US, 27% in Europe and 12% of revenue from heavy tyres, a back of a napkin growth calculation would say that we have to add 200 million in revenue from the US, another 200 million from Europe and another 100 million from Russia and heavy tyres. Thus, Nokian’s estimations for growth are to add 500 million in sales over the next 5 years or to grow at 5% per year. Given the current market decline, lower sales, it is unlikely the company will grow as planned because to grow, the only option is to gain market share from others, which is a costly option. (note: Russia has been the key market for Nokian over the past decade and more. However, the replacement tyre market there grew from 25 million in 2004 to the current 40 million per year).

Figure 11 Nokian’s Russian past tailwind Source: Nokian Capital day – Russia

Nokian – outlook and investment scenario

You never know what will happen in the future, but when it comes to investing I always look for situations that can’t get worse because then the only thing left is upside. With Nokian, the situation is tricky. They had set their strategic plans during exuberant times and high car sales of 2017 and 2018 that they announced during the ill-timed October 2019 Capital market day, just when the decline in the sector started.

If there is no market growth over the next few years, given that all producers have a lot of production capaicity, the pricing pressure in Central Europe can continue and spread around while the American experience might end up as a flop, or big delay, especially if we have a stronger economic slowdown.

Nokian – financials

The good thing about Nokian is its low debt, actually negative net debt, with very little long-term liabilities. This allows it to weather storms and also to mitigate possible mistakes like the timing on the Dayton facility might be (you can never foresee these things).

The combination of high capex requirements targeting growth and a soft market could lead to a few years of negative cash flows. Given the conservative nature of the management (low debt), it is possible that they will cut their dividend. As a dividend cut is never ever priced in a stock price, if that happens, the stock will fall a lot, especially as it is considered a safe dividend stock in Finland, practically a blue-chip. The current 6% yield shows the market is already expecting a future cut.

Figure 12 It is unlikely that the strong earnings trend continues Source: Morningstar – Nokian

Nokian stock investment outlook

I hope Nokian manages to weather the coming storm, that they hit their growth targets and that they can expand market share. However, for me, the risk reward of this investment is not tempting at this level. The average earnings per share over the last ten years have been of €1.94. I assume the company will be able to deliver such earnings in the future and also grow them by 25% over the next decade, alongside their revenue growth plans. Thus, on earnings per share of €2.5 going forward, a good buying price if you wish for a 10% return is €25. If you wish for a 15% return, your buying price should be €16.6 (unlikely to reach that, but you never know the factor combinations that might influence the stock price like a recession in Europe, a dividend cut and delays at Dayton etc.).

I’ve read some analysts’ reports on Nokian and Nordea (October 2019), for example, doesn’t see any structural changes that could dent future underlying growth with a €36 price target. It is likely they are right with their estimations, but I don’t fancy the risk of the negative outlook I described above that includes a structural change where their markets don’t see organic growth anymore. For investors that seek low risk, high reward investments, Nokian’s stock price in the teens would justify another look. On the other hand, investors that are holding large diversified portfolios, should be happy holding Nokian given its low risk as a going concern and quality niche position. It is unlikely that you will lose money long term with Nokian. However, the upside is questionable at this point in time and not worth the risk.

Now, unlike other analysts, I am not expecting Nokian to confirm growing sales in North America and Central Europe to jump into the stock. On the contrary, if they cut their dividend, see slow starting sales in Eruope and in the United States due to a weak market there, if the ruble loses a bit of its value, then this might really be in the teens when the worst will probably be over. Thus, at that point the stock might be at €16 offering 100% upside over the next 5 years, when the actual growth will probably happen as the cyclical markets improve.

Nokian – 4 Investment Lessons

There are a few investment lessons that we can learn from this analysis:

- Catching a falling knife

Many say you should never catch a falling knife. I find such an investment approach fallible because you paint every situation with the same brush. Nokian stock is a falling knife but at some point, it will be a buy.

What is the differentiating factor? Well, fundamentals.

Businesses, especially the automotive sector is cyclical, and you have to approach investing there from that perspective. At some point it will rebound as the cycle turns. You can never know that beforehand, but what you can know is what is the book value of the business, what will the average earnings and growth be across cycles, does the debt level allow the company to weather any storm?

- How good of a business this is – long-term risk estimation

I don’t think people can lose much with this investment. It is either going to be bought by somebody when it achieves enough scale or it is going to continue to grow. It is going to be cyclical but that is the nature of the business. So, the business isn’t that risky form a survival perspective, but as we see above, the stock is risky from a volatility perspective. Don’t worry, this is completely normal for a cyclical stock. By investing in businesses that will hardly ever go bust, you eliminate a lot of pain from your portfolio.

- A dividend cut is never priced in beforehand

Many see the 6% dividend as a margin of safety that gives protection to the stock price. What often happens is that the dividend is cut and then panic follows. So, never ever is a dividend cut priced into the stock price. If Nokian is forced to cut its dividend, I suspect the stock will be in the teens.

- Past growth, doesn’t mean future growth

When a company is a growth stock, like Nokian has been given the 8% yearly growth rate.

The question is always whether the company can continue to grow. Here no past numbers can give you an answer, only a common sense analysis of the business model. Keep in mind you will never be right here, nobody, not even Nokian knows about the future. So, the only thing you can do is to estimate from a risk reward perspective. How much money you make if it happens and what is the probability for it given the environment? And, how much money you lose if growth doesn’t happen and what is the probability given the environment? That is investing.

If you wish to read more such analyses where I search and wait for low risk, high reward analyses, please check my Stock Market Research Platform. If you wish to learn more about investing, please sign-up for my free Comprehensive Stock Market Investing Course.