Forgotten and hated – Is IBM stock a buy now after 10 years of being down?

I’ll start this IBM stock analysis with a summary first, followed by the standard stock analysis you expect from my work.

IBM (NYSE:IBM) stock analysis content:

- IBM stock key points summary

- IBM stock price overview (Lower than Buffett’s 2011 buying level and 2017 selling level)

- IBM business analysis (Hybrid cloud focus and NewCo spin-off)

- IBM fundamentals (IBM dividend & buybacks)

- IBM valuation and risk and reward investment conclusion (excel model included)

- IBM is a high conviction short pick with Jim Chanos on EPS jinxing – I discuss the numbers

Here is the IBM stock video analysis, article continues below:

IBM stock key points and issues summary

The main issues the market sees for IBM are the following (I’ve read approximately 30 analysts reports and listened to the latest conference calls):

- Lagging industry peers in growth

- Leverage growth on declining revenue and income

- Continuous stagnation and weak performance

- Red Hat questionable merger rationale

- Beating analysts’ estimates in only 2 of the last 8 quarters

- Revenue estimates down from $80 billion to $76 billion for 2021

- 2022 EPS estimates cut from $15 to $13 due to COVID

- Reducing employee count – thus not trying to grow and leading to high skill loss (example: Lisa Su – left in 2007, currently CEO of AMD that has a market cap close to IBM’s now)

- Former CEO Rometty’s compensation went from $16 million in 2012 to $158 million in 2019 while the market capitalization went down significantly. To me personally, a picture like the following tells me the CEO is focused on herself and on the ivory tower she lived in, but that is just a subjective perspective and hopefully things change now with the new CEO

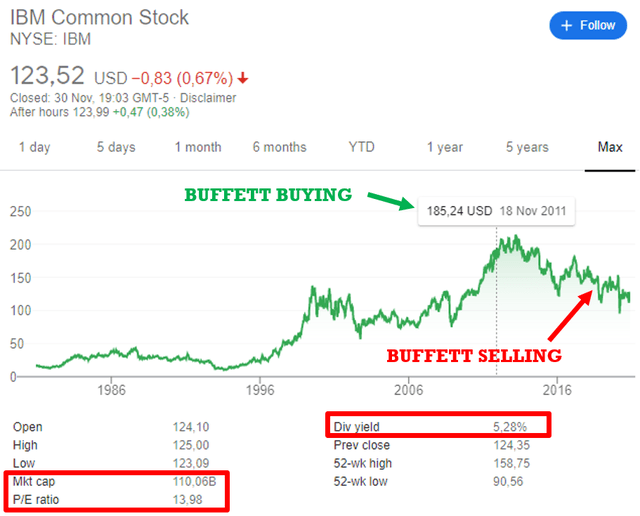

- Buffett bought $10.7 billion in 2011, took a look and sold

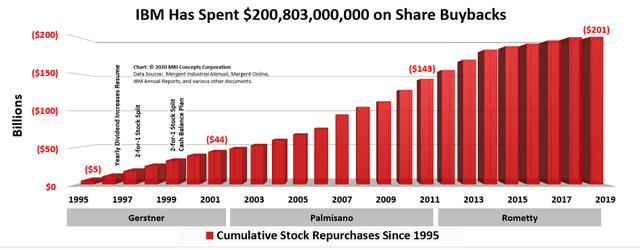

- IBM spent $200 billion on buybacks over since 1994 – almost twice the current market capitalization

- IBM will split in 2021, thus it will spend two years focusing on how to split instead of focusing on how to grow

- No buybacks till debt ratios improve – around 2022 at first

- M&A strategy is unclear, also unclear where will the discussed growth come from

- Quantum computing is too early to create profits in this decade

- Cloud will be a commodity in the future, with thin margins given the already strong competitive environment (think: Amazon, Microsoft and Google).

All, I mean all analysts, are focused mostly on future growth – a 5% yield is irrelevant in today’s investment world. But, if the above would be any different, you would not have an opportunity to buy IBM stock at free cash flow yield of 10% and dividend yield above 5%.

IBM’s issues are really bad but at some point, it will not be possible to get worse and things will turn for IBM. The CEO is positive (Q3 2020 conference call):

“All of this will contribute to accelerated growth for our company in the future and we expect to deliver sustainable mid-single-digit revenue growth upon completion of the separation of NewCo.”

If the growth targets materialize, a cash flow yield of 10% and growth of 5% growth, is a great investment in my book and should reward IBM shareholders well over time.

Let’s dig deeper and see whether the market might be biased due to the disastrous performance IBM delivered over the last 10 years or IBM has structural issues that will keep it on a downward path for another decade. In case of a turnaround, IBM could deliver good returns to shareholders alongside the already great dividend of above 5%.

IBM stock price analysis – bad decade

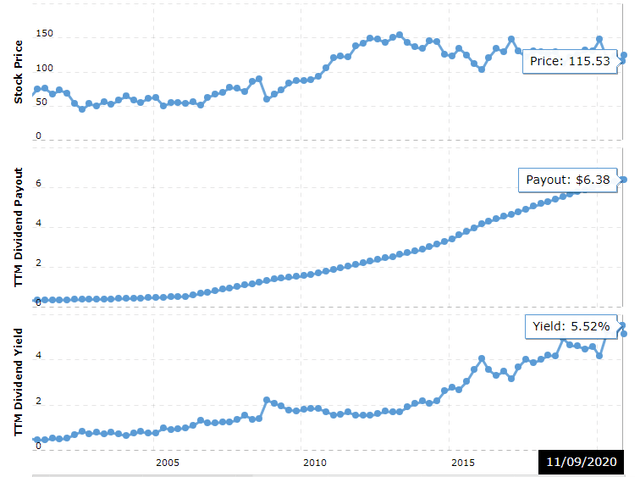

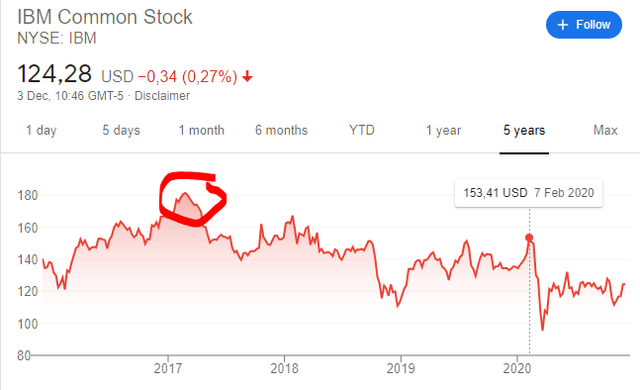

IBM stock didn’t perform well over the last decade. It is not just that it is down 34% since 2011, it is also the fact that the market (S&P 500) is up 175% since. Such underperformance must, at best, bring a sense of disgust to IBM shareholders and I assume many have capitulated over the last 10 years. Even Buffett capitulated on his position in 2018 when he announced Berkshire sold its complete IBM stake they had started buying in 2011.

However, when something is unloved and forgotten, it could be a great turnaround investment opportunity. I believe that after 10 years of hatred, it is a good time to take a look at IBM stock. Plus, the dividend yield is high at 5.28%, the PE ratio is relatively low at 14 and IBM has announced an interesting spin-off that might make the market reconsider the way it is looking at IBM’s stock.

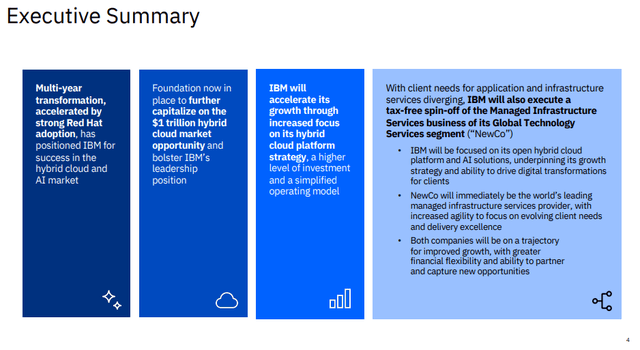

IBM business analysis – the investment story

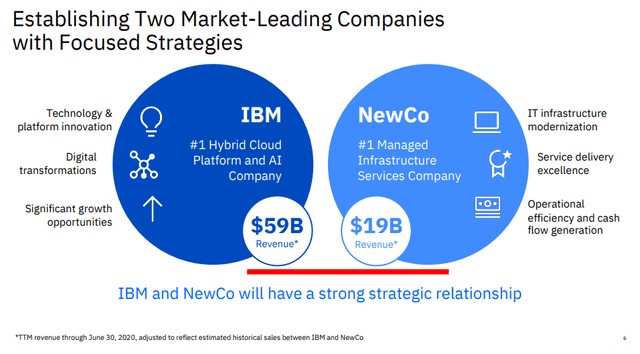

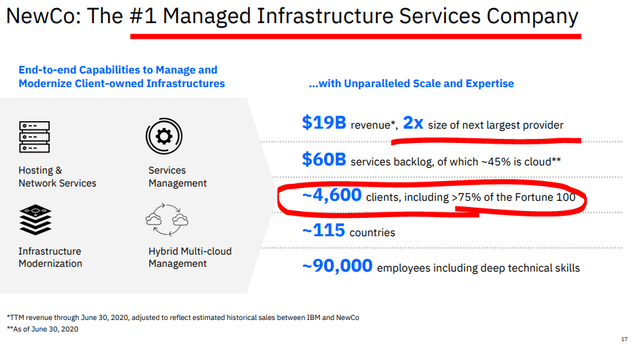

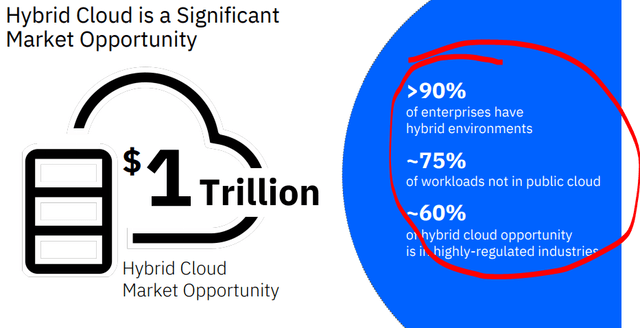

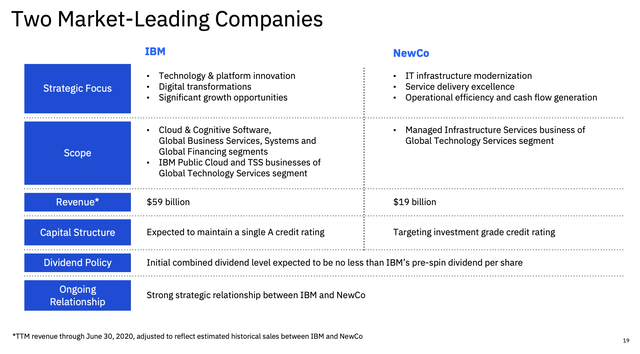

The latest strategic update presentation from October 2020 summarizes IBM’s business position and strategy. The focus of IBM will be on the open hybrid cloud platform where they see a $1 trillion market opportunity while the spin-off will focus on the managed infrastructure services.

The spin-off will be tax free and the company called NewCo.

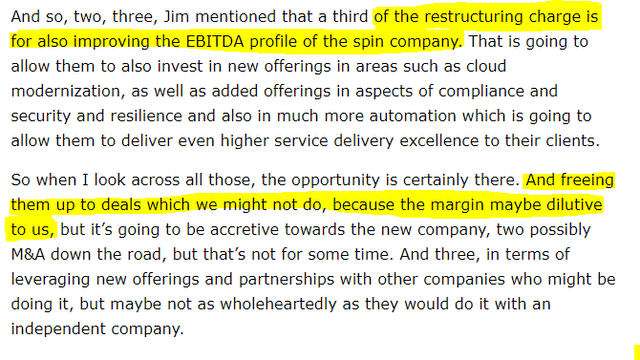

NewCo should remain a leader in its own space and have more flexibility for smart M&A than what IBM can’t do now because it would hurt their margin levels.

Margin levels issues is what has been presented as one of the reasons for the spin during the last conference call. Unfortunately, this confirms the thesis that IBM is about doing what they think pleases Wall Street and not really focusing on what pleases shareholders over the long-term: growth and consequently higher cash flows.

For me, it is crazy that IBM will not think about an acquisition because it would dilute its margins. Business is about increasing profits and there are many different profitable businesses with either narrow or wide margins. Thinking about margins to please Wall Street is what would put the nail in the coffin for me and IBM’s stock as an investment and is probably the reason for the terrible performance in the past. However, they say things will change after the split.

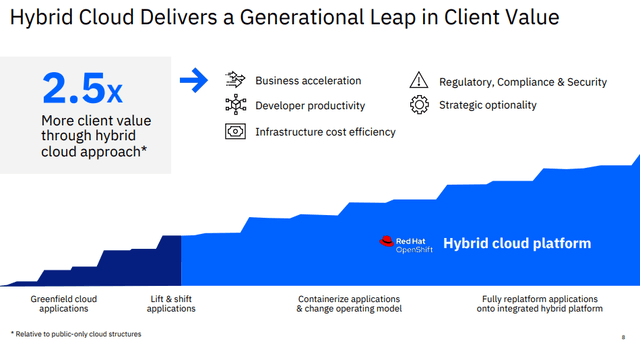

The plan is to offer more value through a hybrid approach for customers.

This should represent a trillion-dollar market opportunity.

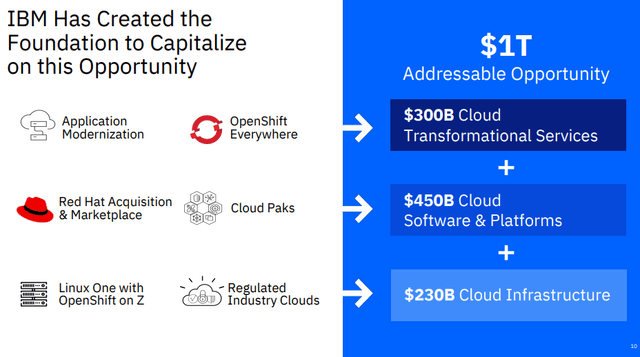

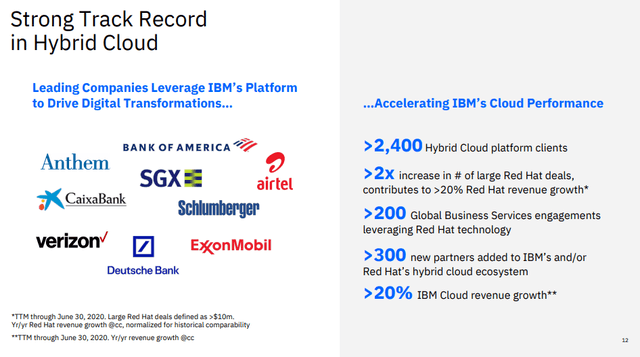

The Red Hat acquisition should be of significant help there based on the integration of other cloud systems with IBM’s hybrid offering. IBM acquired Red Hat for $34 billion in 2019.

The CEO forecasts mid-single digit growth for the new IBM going forward.

The main business issues are of a competitive nature; IBM has a strong foothold in many sectors, especially as an IT solutions company for many regulated industries where change will be slow to come. However, competitors have been slowly but surely chipping away market share and eroding IBM’s moat.

On the positive side, IBM has many technologies it is working on like quantum computing, Kubernetes, power systems, IoT, mainframes, public cloud, private cloud, hybrid cloud, AI, security, blockchain, power systems, software, containers, etc. so there is a lot of potential, but potential is one thing, fundamentals are another.

IBM stock fundamentals

There are two ways to look at IBM’s fundamentals. From one point of view one could say the company is paying $5.7 billion in dividends per year and promises to keep increasing the dividend. They are making $12 billion in free cash flows that gives a free cash flow yield of 10%, which is great compared to many other investment opportunities out there.

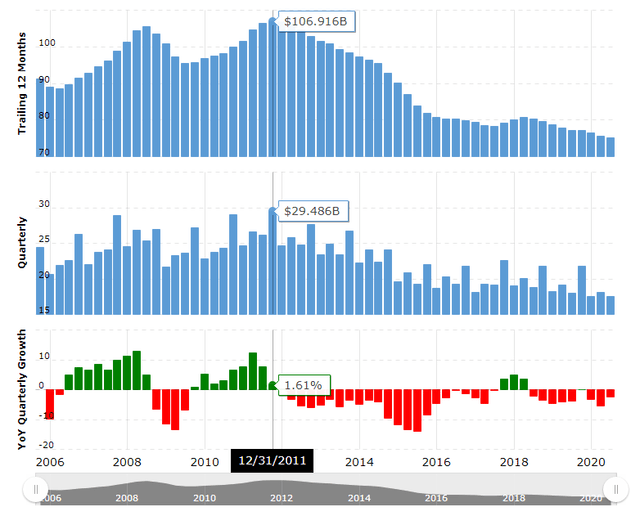

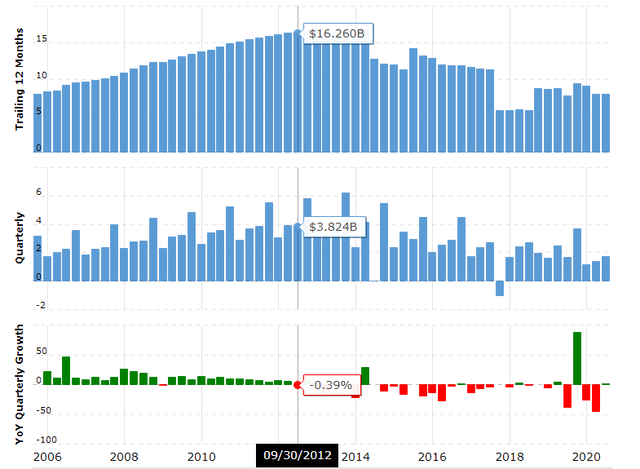

On the negative side, IBM’s revenue decline has been terrible.

The same holds for net income that went from $16 billion in 2021 to the current $8 billion.

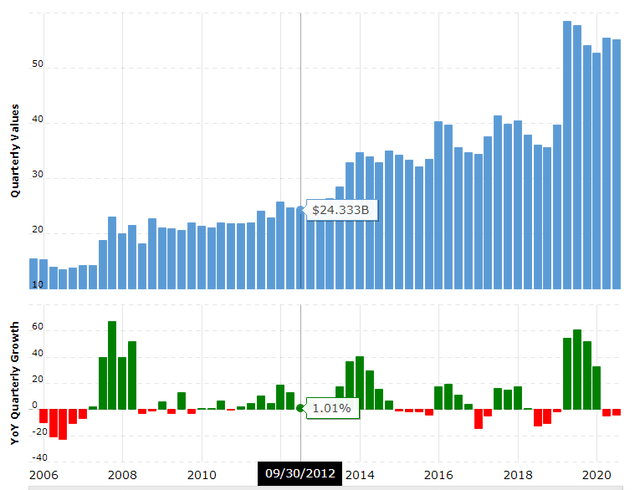

On top of the declining business metrics, long-term debt went from $24 billion in 2012 to the current $55 billion.

The current fundamentals always reflect what happened in the past while investing is about the future. If they manage to revert debt growth, revert revenue and net income growth, IBM could easily give you a 100% investment return in a relatively short time.

Before we try to estimate IBM’s future, let’s take a quick look at IBM’s dividend and especially the buybacks disaster over time.

IBM stock dividend and buybacks

IBM has increased its dividend for the past 25 years but what it paid out in dividends over the last 7 years is similar to the increase in long-term debt and dividends don’t cover for the decline in market capitalization. So, not much value has been created there. To make things even worse, pure value destruction has happened with buybacks.

Since 1994, IBM has spent $200 billion on buybacks. Given the current market capitalization is $120 billion, the company didn’t do much good with those buybacks and is one of the most horrible examples of capital destruction through poor capital allocation in history.

It is very hard to move on from the catastrophic historic performance but moving on and looking forward is something we must do as investors. We invest now for the future, not in the past, even if past ghosts might keep hunting IBM.

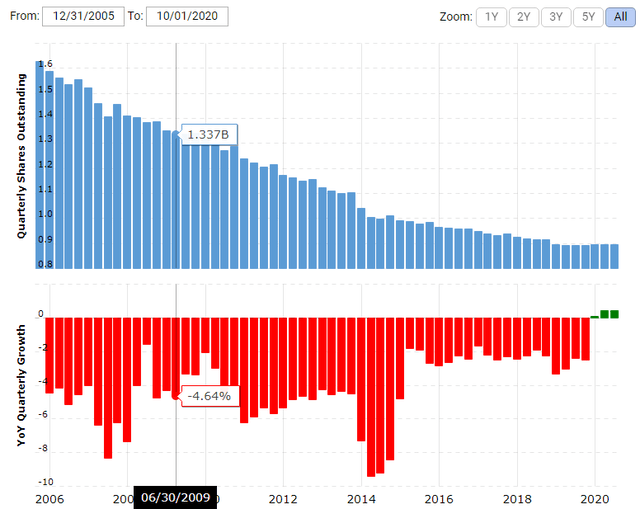

The number of shares outstanding has decreased significantly, but over the last years the decrease has slowed down significantly and buybacks have been stopped since the Red Hat acquisition.

Let’s put the above into a valuation and investment perspective.

IBM stock valuation and investment thesis

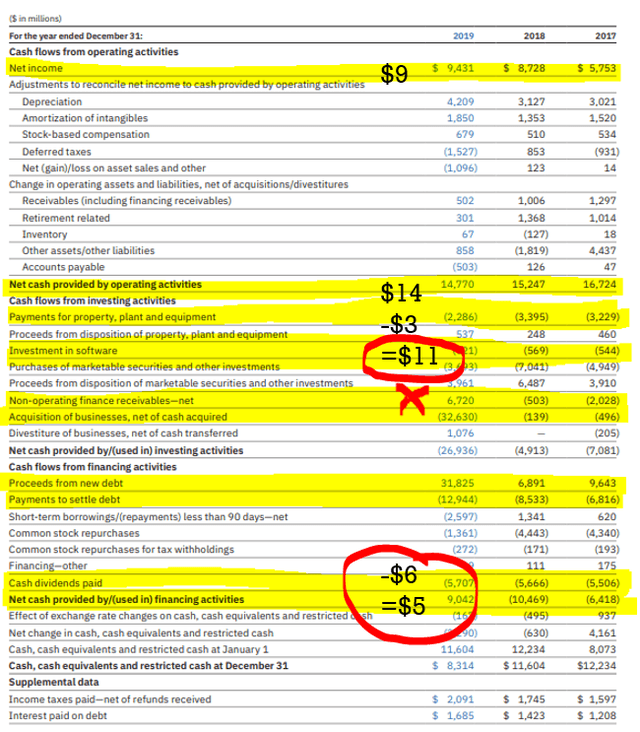

Not considering accounting cosmetics, we have free cash flows of around $11 billion per year that give a cash flow yield close to 10%.

Of the $11 billion, $6 are used to pay a dividend and the other $5 are available for other things where the management said it will focus on lowering debt up to 2022.

After 2022 they will probably do other acquisitions to try and find more growth, especially if the current plans don’t really work but that is just an assumption. They could also push more on buybacks or increase the dividend.

$11 billion of free cash flows is what we have with IBM. Of that, half is delivered to shareholders through a dividend and the company is committed to grow the dividend. That is the first part of the valuation.

The second part of the valuation includes guessing what will the future bring:

- Will IBM really grow 5% per year? Or will at least the new IBM, without NewCo grow 5% per year?

- Will NewCo manage to grow at all or will it be just a place where they park things with lower margins and negative outlooks?

- Will the Red Hat acquisition deliver as expected?

- Will capital allocation be terrible in the future as it has been terrible up till now?

There are many uncertainties with IBM and the certainties that are there now, like the legacy business and sticky customers that will not change what works, are there but seem not enough to make a great investment case.

I think the uncertainty, the terrible allocation of capital and the horrific revenue performance based on its leading position is what made Buffett sell. I feel that he simply got fed up with the management destroying so much value.

Future investment returns from IBM depend on whether the above can change. If IBM keeps doing what is has been doing the last 10 years, expect it to be taken over by a tech company growing fast with a high valuation and a larger market cap that will shake things there. That would be the bottom and end of IBM.

If they manage to turn things around, then we could see stock levels last seen before the COVID-19 crisis hit, or even 2017 highs around $180.

Unfortunately, there is not a catalyst inside the company that looks poised to change things forward except for the cosmetic spin-off announced.

The best investing strategy with IBM stock would be to closely follow and watch for signs of hope. I am not going to do that because just looking into IBM for the last few days has made me feel bad, I can only imagine how long-term IBM investors feel. I feel I can find better and you can check my other stock analyses here.

IBM stock price forecast

On the stock, I feel the current level offers a relative bottom because I don’t think it will go below because of the 10% free cash flow yield if offers. Further, if they manage to reach just two quarters of growth where they beat analysts’ expectations for once, the stock will easily rebound 30 to 50%.

The dividend is relatively safe, they would really need to do terrible things to be left without the $6 billion necessary to pay one, so if you think 5% is enough for you to own this and wait, it might be interesting.

IBM stock forecast:

60% – IBM keeps the dividend stable (both IBM and NewCo) – I think the size of the company, the customer list and the already installed business, offers a strong margin of safety for at least the dividend going forward.

20% – IBM manages to enter a growth cycle of 5% per year, gets rerated by the market that is then happy to pay a price to free cash flow ratio of 20 and the stock doubles.

20% – IBM keeps losing business, has debt issues, they are forced to cut the dividend what pushes the stock down 30% and the paid-out dividends up to that time don’t cover for the loss of capital.

Somehow, I feel this is a stock better to be left to pension funds. They need to own it based on the market capitalization, it gives them a good yield, but I think rational retail investors can find better risk and reward opportunities, be it to buy or just to follow. This except if you are a dividend investor with a large diversified portfolio, I feel the dividend is mostly likely to stay for longer.

Here is the video discussing why Jim Chanos has IBM as his highest conviction short pick. IBM declares earnings of $10 per share but if you look at the SEC filed financial reports, they will be lucky if then get to $6 for 2020. Using $6 or $10 as a base for future growth and valuation leads to enormous differences.

If you got value from this IBM stock analysis, please check my other stock analyses.