Evoqua Stock Analysis – NYSE AQUA – Recent IPO where the management doesn’t convince – 50% downside risk

Evoqua stock analysis is part of a full Waste Management stocks sector investing analysis alongside a list of 15 waste management stocks, all analyzed.

Evoqua stock analysis

Evoqua Water Technologies provides water treatment equipment and services; like filter press, intake rebuilds, and electrocatalytic services, as well as sludge dryers, digester covers, captivator systems, and other related technologies to the industrial, commercial, and municipal water infrastructures.

AQUA stock is a recent IPO and it behaved as many recent IPOs do. First it goes down and then back up.

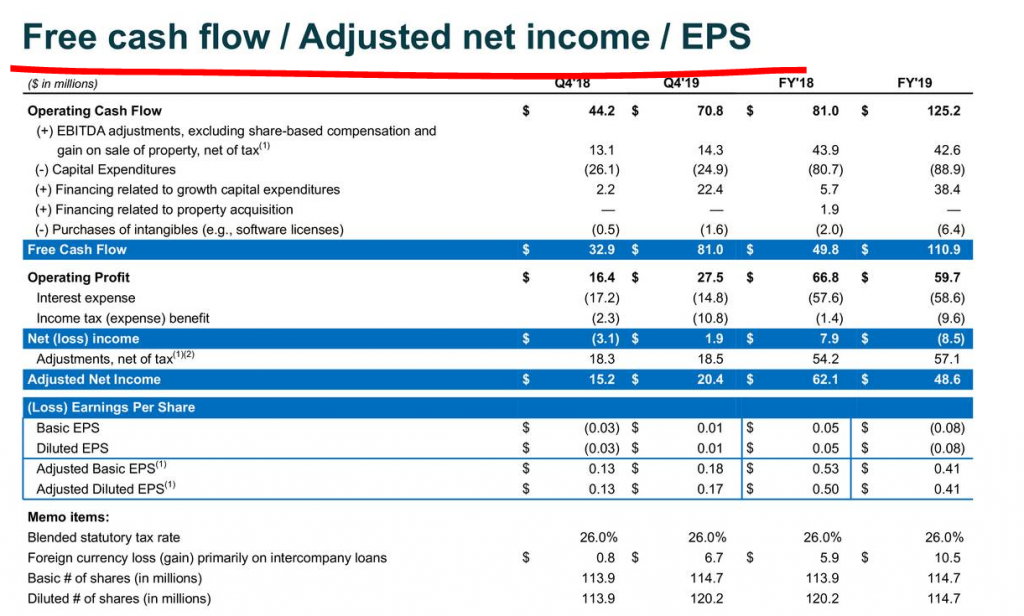

AQUA stock business overview

AQUA’s business is a two-tier business, including both services and products. Growth has been steady and stable over the past years. Expected growth for 2020 is between 1% and 5%.

Growth in revenues for AQUA hasn’t been stellar but the company became free cash flow positive, which is always good.

AQUA’s management forecasts future growth to be between 3% and 5% but given the number of acquisitions they make, growth might even be faster. In 2019 the company acquired ProAct, IsH20TOP, PureWater and 60% of Frontier water systems.

The company delivered $90 million of free cash flows in 2019 but also $34 million in restructuring costs, $20 million in share compensation to management plus $20 million in other losses and expenses.

AQUA looks like something that could be a good business, but the management is making a mess of their financials. Everything is adjusted, from EBITDA, earnings to cash flows and they do that year by year. This makes me think they are not really there to reward shareholders as much they are there to reward themselves.

However, if they do well, keep growing and improve margins, the market might rerate this like it has been the case with other similar stocks like Waste Management, but it is too much of a long-shot for me.

Another issue is the frightening debt levels where the debt is higher than the tangible assets. Tangible assets are $1 billion while total debt is $1.3 billion. Actually, AQUA’s stock tangible book value is negative.

Sven Carlin Ph.D., the author, is an independent stock market researcher and investor managing the Sven Carlin Stock Market Research Platform.

Those who want to learn more about stock market investing can join the Free Comprehensive Stock Market Investing Course.