Covanta Stock Analysis – NYSE CVA – Dividend cut and bankruptcy risk is too high

Covanta stock analysis is part of a full Waste Management stocks sector investing analysis alongside a list of 15 waste management stocks, all analyzed.

Covanta stock analysis

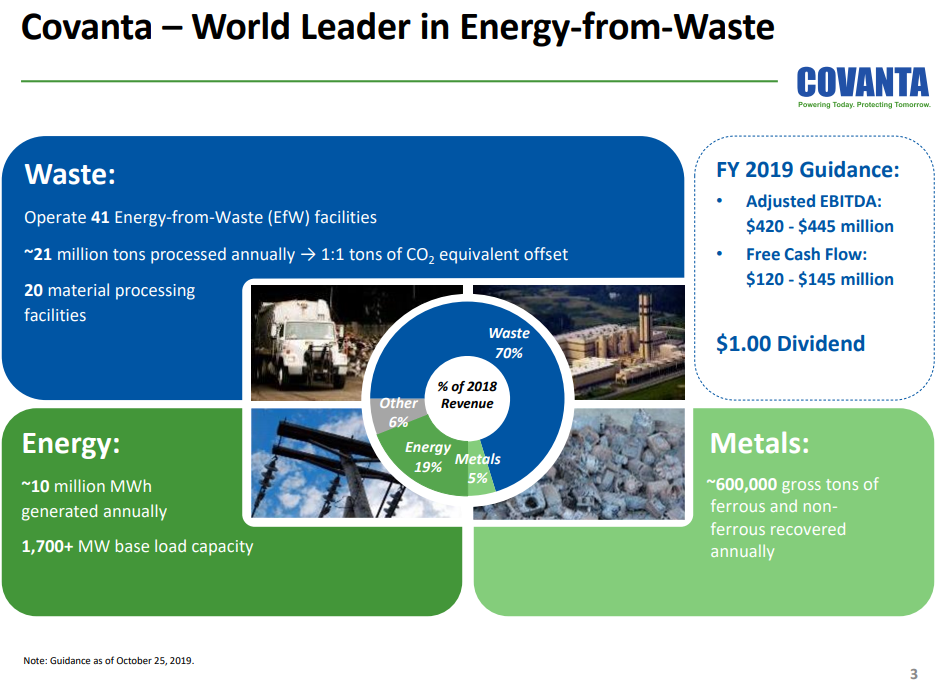

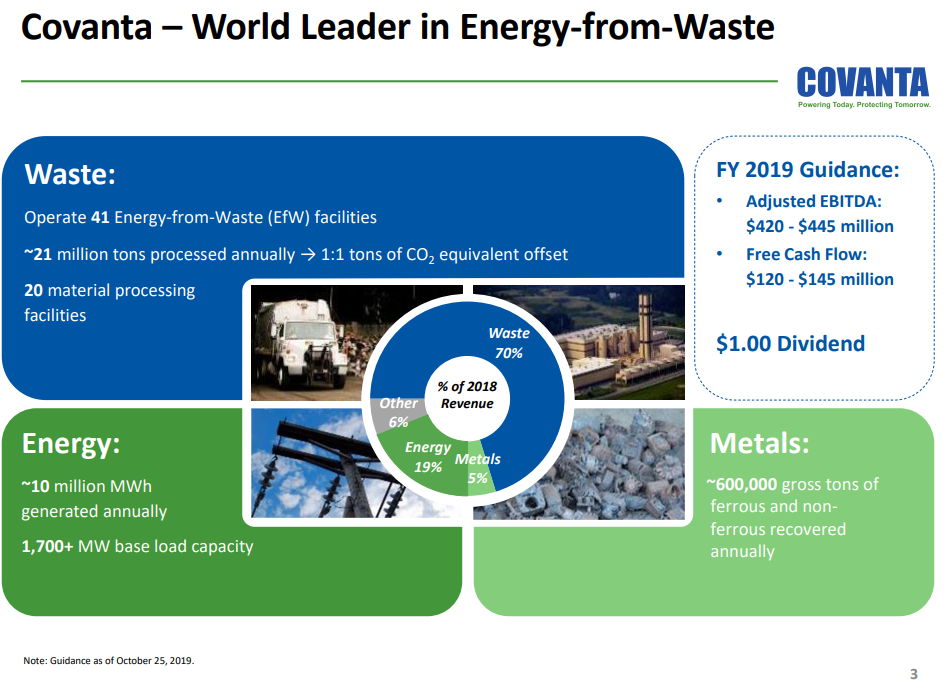

Covanta is a large global corporation that provides a variety of waste-management and incineration services. 70% of revenue comes from waste management while the rest comes from recycling and energy production.

The company expects to grow both organically and through acquisitions and is focusing on the ‘energy from waste’ sector.

It has 75% of the waste to energy market in the US and it plans to expand in the UK thanks to a joint venture operation with Green Investment Group.

Covanta stock price and financials

The situation for Covanta’ stock price hasn’t been great over the past years.

Covanta’s stock didn’t givenany return to shareholders for the past 14 years except for the dividend. But before discussing the significant dividend let’s discuss Covanta’s financials.

Revenues have been flat for the past 10 years, while operating income, net income, book value per share and cash flows all significantly declined. When all the important financial metrics are in a downward trend but the company keeps paying a big dividend, debt usually goes up. Covanta’s debt to equity ratio is 0.87 where total liabilities are $3.35 billion while total assets are $3.85 billion. This tells us that operations are pretty leveraged while there is no growth. But, before dismissing Covanta’s stock as an investment, we have to look at its outlook, business model and main possible issues like debt, contracted energy prices and dividend sustainability.

Covanta Stock dividend sustainability

Let’s start discussing the issues. Covanta says it operates in markets with high barriers to entry.

Would you like to have an ‘energy from waste’ facility in your backyard? Of course not. Therefore, it is costly for the company to maintain those as you have to change filters, improve disposals and you never know when you’ll get a lawsuit or lose your license. Operating in such a difficult environment leads to high cash outflows, increased debt and deteriorating book values over time. Plus, the energy sector doesn’t look attractive from a price perspective.

Market energy prices are much lower than Covanta’s contracted energy prices. In 2024 when the new contract transitions come, it will be difficult for Covanta to get new contracts above market rates as it currently has. So, from 2024, on top of the current cash tight situation, there will be even less money coming from the energy business.

Therefore, the cash situation of the company looks stretched. What kind of company pays out a dividend and the securitizes its receivables to get cash upfront?

Such behaviour is unsustainable because at some point you can’t borrow anymore. When that happens, debt investors panic and retreat, the company is not able to refinance and goes bust.

To conclude, given C02 emissions, the focus on less waste, Covanta is not in a good position. It could be that the dividend is the only thing keeping the stock price up and on a $2 billion market cap, there are plenty of individual dividend investors and ETFs, or even better waste management environmental index funds that hold this and keep Covanta’s stock price up. Al always, anything can happen but the risk is simply to high in relation to the reward. The company needs to be paying you a $1 dividend for the next 14 years just to give you your money back while we don’t know whether the company will be around in 5 years.

On the other hand, the company targets $250 million in free cash flow by 2025.

If that happens, the stock will be re-rated and probably trading around $4 billion. However, the risk of zero is too high when compared to the $4 billion upside. Investing in companies that have debt levels above their market capitalization is extremely risky. Plus, with the cumulative cash flows over the last 4 years being a negative $170 million, where are they going to find the money to keep paying the dividend or even, to survive?

Sven Carlin Ph.D., the author, is an independent stock market researcher and investor managing the Sven Carlin Stock Market Research Platform.

Those who want to learn more about stock market investing can join the Free Comprehensive Stock Market Investing Course.