Beijing Enterprises Water Stock Is a Great Dividend Growth Stock With A 5% Starting Yield

Beijing Enterprises Water Group Limited Stock Analysis HKG: 0371

If you prefer watching or multitasking, please enjoy the video version of my Beijing Enterprises Stock Analysis. Article continues below.

I have recently started with an analysis of Chinese stocks. I am going through my long list of stocks where I make a deep analysis on the businesses I find interesting. It is a work in progress but I hope to find a few nice ones from the hundreds of potential investing opportunities out there.

The one that looks the best from a look at the first 50 Chinese stocks on my list, is Beijing Enterprises Water Group Limited (HKG: 0371). As it looks really good, I am happy to share my analysis and initial overview.

The article starts with a business overview, continues with a financial analysis focusing on the main issues, touches on the sector and general business environment for the company and concludes with my investment opinion and strategy.

Beijing Enterprises Water Stock – Overview

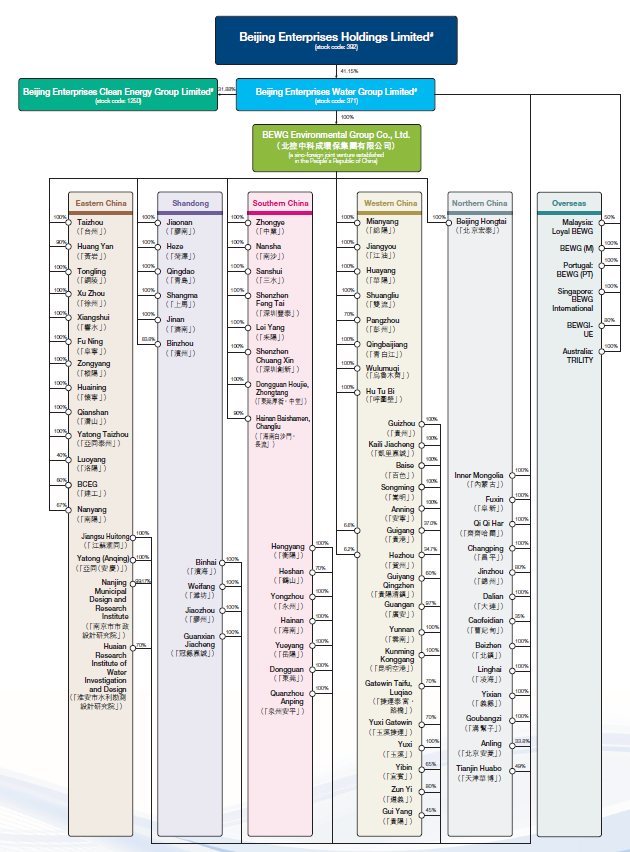

Beijing Enterprises Water is owned by the government through Beijing Enterprises Holding (HK:0392) that owns 41.15%. Consequently, Beijing Enterprises Water owns 31.88% of Beijing Enterprises Clean Energy Group Limited and 100% or less in many projects across China and 6 projects overseas.

32% of the company’s profits come from water treatment services – Sewage and reclaimed water treatment services, 12% is from water distribution services, 47% comes from construction services for the water environmental renovation where 50% of that is within a BOT strategy (build, operate, transfer). The final 9% comes from technical services and sale of machineries for the water environmental renovation.

Beijing Enterprises Water has many projects under operation but its target is to significantly grow and even reach 100 projects overseas from the current 6. Given China’s One Belt One Road strategy and growing economic force, they might even be able to do it. I am amazed by the infrastructure projects being build by Chinese companies in Europe as Chinese companies are usually the lowest bidders. Further, and what might be the key, the foreign operations are extremely profitable. The company makes HKD 33 million in profit on HKD 180 million in revenue overseas.

Aditionally, the management targets to double profits too. As the company has a strong foothold in China already, it will be able to leverage its scale and continue to grow.

Growth in 2018 was 17% and 1H 2019 has been similar. Thus, we have a growth stock here with good fundamentals and a relatively high yield.

The company owns many small water and sewage treatment projects across the country.

Over the last 3 decades China grew extremely fast and didn’t care that much about ecology. However, policies have been changing and it is a great benefit for companies like Beijing Enterprises Water.

When a business is related to policies, there will always be risks, but you have to look at it from a long-term perspective – are the risks structural or temporary? As it was the case with the Chinese solar industry, the risks are often just temporary.

It is good to mention that there will always be risks when investing in China, from currency risks to operational risks, but one has to compare the risk and reward to other opportunities and then make a decision. In any case, when investing in China, always expect extreme volatility because it is a young market where most investors are gamblers, not investors, which is something to always keep an eye on and take advantage of.

Beijing Enterprises Water business overview

Beijing Enterprises Water business is water treatment, construction services and technical/equipment services for water environmental renovation.

The water business treatment includes 937 water plants including 771* sewage treatment plants, 139 water distribution plants, 25 reclaimed water treatment plants and 2 seawater desalination plants.

The Group had 23 comprehensive renovation projects under construction during the year. The projects mainly located in Zhejiang Hangzhou, Zhejiang Taizhou, Chengdu Jianyang, Guangdong Heshan, Malaysia Terengganu, Inner Mongolia, Sichuan Luzhou and Beijing Liangshuihe.

The build-operate-transfer business was one of the biggest contributors during 2018, total revenue for construction of BOT water projects was HK$8,698.6 million (2017: HK$6,647.1 million) and profit attributable to shareholders of the Company was HK$1,654.1 million (2017: HK$1,133.4 million).

Beijing Enterprises Water – Notes from annual and interim report

I’ve read the recent interim and annual reports in detail and the following are a few notes I wish to share on the finances, the interesting receivables accounts and ongoing dilution.

Beijing Enterprises Water – Financial overview

A look at the balance sheet tells us that the largest value is found in ‘amounts due from contract customers’ and ‘receivables under service concession agreements’ as the two accounts make 51% of total assets.

The business works in a way that the company builds the plant and then has receivables for a long period of time from the customer. Until the project is completed, receivables are recognized as ‘amounts due from contract customers’ but upon completion of construction and acceptance by the customer, the amounts recognised as amounts due from contract customers are reclassified to receivables under service concession arrangements for BOT arrangements and trade receivables for other construction contracts.

So, the company is financing the projects, that is a normal way of doing things and therefore the liabilities don’t have to scare us that much. Further, the company is selling stakes in individual projects in order to turn the business model into an asset light model.

On the liabilities and equity side, we must deduct HKD 14 billion from the total reported equity and we get to an equity balance of HKD 29.7 billion. Thus, the real price to book value is not 1.1 as Morningstar reports but 1.33. (always check the numbers yourself)

On the liabilities side, we have relatively high trade payables and a high leverage level where bank borrowings are equal to actual equity. However, given the safe contracts with government entities, it is likely the contracts will be honoured.

Given the nature of the business, it inevitably creates negative cash flows for as long as the business grows and now projects are being built. However, in the long-term, the cash benefits should be substantial and the company will be able to use more and more of its own capital for growth.

Speaking of cash flows, the dividend pay-out ratio is around 30%. 30% is still good on the single digit PE ratio.

Beijing Enterprises Water – dilution

Over the last years, there has been slow but constant dilution of shareholders. However, the dilution is usually part of a partnership where the partners inject cash into the company and the shares are issued at the current stock price level. So, no real harm done there as the money is used to either finance new projects or service project debt. Also, over the last 5 years, the number of shares outstanding went from 8.8 billion to 9.6 billion while revenues increased 3 times.

Beijing Enterprises Water – Business environment

Before making an investment conclusion whether Beijing Enterprises Water stock is a stock to put on our watchlist, we have to check about the underlying environment. I prefer to invest in sectors with tailwinds.

Water and sewage sector analysis

Given China’s fast urbanization and lack of earlier focus on water and sewage, it seems the market has a positive long-term tailwind. A 2012 China water risk article discusses how a regulator framework change is necessary. That is exactly what happened over the last years and Beijing Enterprises Water has been benefitting from it.

A Science direct article titled ’Optimizing operation of municipal wastewater treatment plants in China: The remaining barriers and future implications’ has its abstract start with the following:

“China’s national development strategy now prioritizes environmental protection over economic growth, which has driven a rapid development of China’s wastewater sector.”

The article concludes that there is still plenty of work to be done as the situation is variegate and 40% of sludge disposal is still an issue. A positive for BEWG.

Additionally, many articles discuss China’s water problem, thus you don’t want to pollute what you have.

All in all, China has been working hard to improve the environment issue and will probably continue to do so over the longer term. Plus, there is also the global opportunity for the company where the overseas business is extremely profitable and the management wishes to focus on that too. I would conclude the business environment analysis with a positive mark as the tailwind looks strong, both form a Chinese and global perspective.

Beijing Enterprises Waters – Investment Conclusion

The upside is pretty significant because it is unlikely that a company growing 16% per year in a sector with positive tailwinds trades for a long time with a PE ratio of 7. If the company grows 100% over the next 5 years and the valuation expands to 14, the investment return could lead to a 4 bagger as both earnings and the valuation double!

I recently analysed 15 Waste management stocks and the stock analysis of companies like Veolia and Suez Environment showed that a PE ratio of 20 isn’t uncommon with dividend yields below 5% and no growth. Thus, Beijing Enterprises Water has the benefit of growth and a low PE ratio in comparison. Over the past decade, it hasn’t been uncommon for the stock to be valued with a PE ratio above 20.

Beijing Enterprises Water – Investing risks

On the downside, changes in the regulatory framework can always hit the business and a few analysts’ reports that I read, suggest that investors are concerned about policy overhangs and a slowdown in the macro economy. More specifically the concern is related to a possible decline in revenues from the construction services sector. However, we have seen that construction is just a part of the business, the backlog still looks strong and it is unlikely construction will totally stop.

The debt is also a risk, especially from the currency perspective of a foreign investor. If the Chine currency devaluates 30%, the stock will follow.

To conclude, China Enterprises Water is cheap as are other Chinese utilities. When it comes to investing, it is about whether you wish to invest from an absolute perspective where it is likely you will get a good return in the long-term from this business or whether you wish to invest on a relative basis, where the stock can be hit temporarily due to weaker economic growth and environmental policies. This reminds me of the carnage when China decided to lower subsidies for solar industry that later proved not that of a big deal.

From an earnings perspective, the company has a PE ratio of 7 and a dividend yield of 4.76% that will probably be bigger in the future as the 2019 interim dividend was higher than both last year’s interim and final dividend. A PE ratio of 7 leads to a business return of 14.28% per year while any growth on top of that simply adds to the return from investment. Therefore, there is significantly more upside compared to the downside.

Beijing Enterprises Water stock price entry point

As for what is a good entry point price to buy Beijing Enterprises Water stock, the right entry price depends on you. If the stock becomes a 4 bagger in 5 years due to earnings and valuation expansion or, just to be conservative, 10 years, you are looking at a 14.8% return from a current standpoint. You have to compare that to other investment options you have and see how the stock, business and risks fit your investment requirements.

From my personal standpoint, I have put China Enterprises Water on my watch list and I am going to compare it to other investment opportunities, cover it over time and also compare it to other potential Chinese investments that will come up as I continue researching Chinese stocks.

About the author: Sven Carlin Ph.D. has been an accounting professor at the Amsterdam School of International Business and is now an independent stock market researcher and investor. His passion for investing and teaching led him to create a YouTube channel on investing that has turned into one of the biggest value investment channels on YouTube.