BE Semiconductor Stock Analysis – Expensive Cyclical, so Wait!

BE Semiconductor stock is part of the currently extremely hot semiconductor market. However, the semiconductor industry is a cyclical and therefore the best low risk high reward investments are made in cycle downturns, not in exciting times. 6 stock categorizations by Peter Lynch.

This BESI stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger potential, so as would Buffett say; I start with the As. Here are the Bs already.

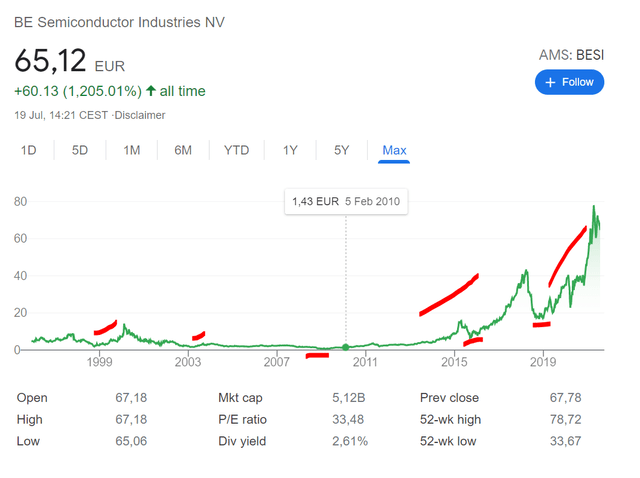

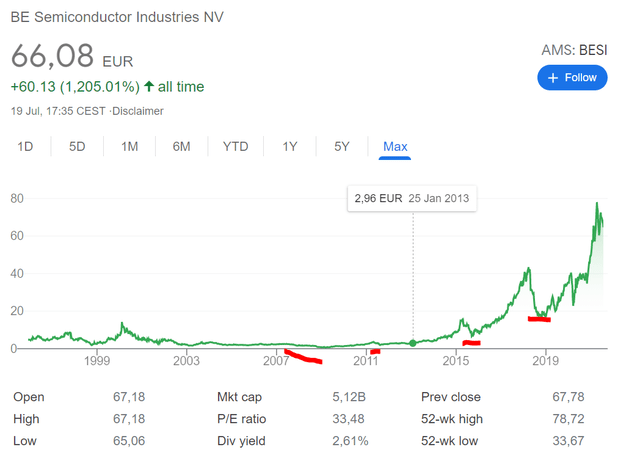

BE Semiconductor Stock Price overview

BESI stock has consequently done well in cycle uptrends but also very badly in downturns.

The business has improved after each cycle which is a strong positive, but now one must think about whether it is a good buy at the moment?

BESI Stock Analysis – Fundamentals & Business

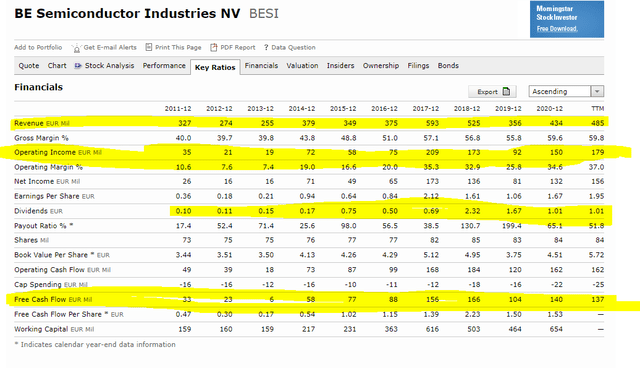

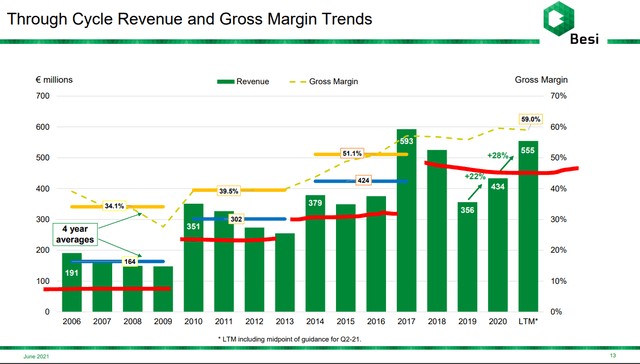

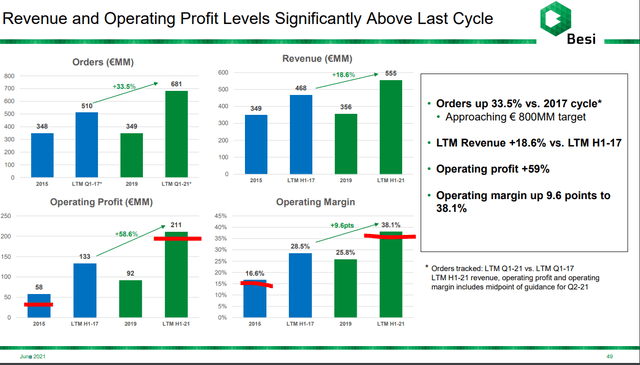

Revenue growth has not been so stellar to justify a 50x increase in the stock price over the last decade. Profits have been more stable and growing faster, but still cyclical.

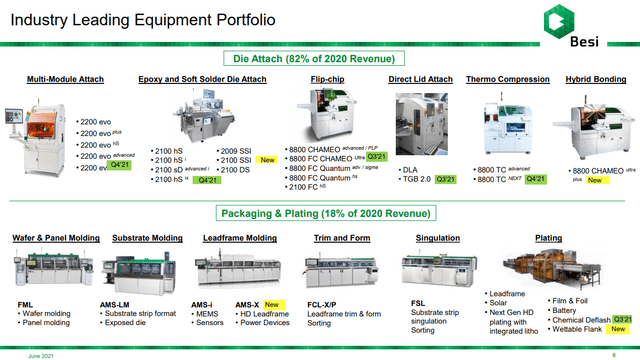

BE Semiconductor is a machine supplier to the industry.

Revenue averages have been increasing through cycles, but this also tells us a new cycle is forming and usually after a cycle boom, there is also a cycle downturn.

Over the last 15 years, BE Semiconductors has seen 9 years of declining revenues – something to keep in mind for when to invest. The years with declining revenues are the best periods to buy a cyclical stock, BESI stock is no different.

BE Semiconductor stock buying points

At the current moment, BESI stock is at historical highs and the forecast is positive – usually the time to avoid buying a cyclical if you are an investor that looks for low risk and high reward stocks.

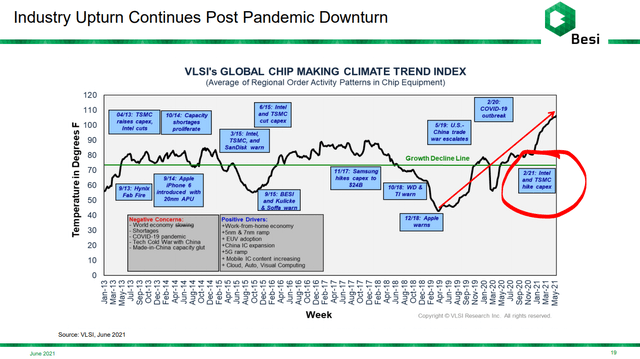

As Intel and TSMC have hiked their capex, it is a really good time for companies like BE Semiconductor.

And the long-term is also positive.

But, for investment purposes and return maximization, one must keep in mind the cycle.

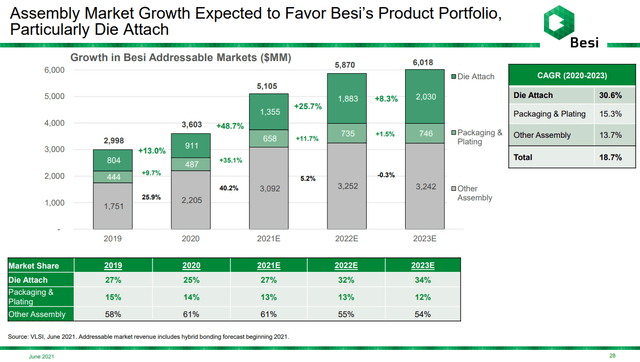

They see the market doubling over the next 3 years, but that also means many will step up investments.

Consequently, margins are also extremely volatile.

BESI stock investment thesis

If you think the current environment for semiconductor production will last forever, then you might want to pay 10 times 2021 revenues for this company, but if not, if there is even one short and bad period in the coming few years, your returns might not be stellar.

Even they reach net income of 150 million EUR in 2021, that is a forward PE ratio of 34. If the double revenues in 5 years, the PE ratio could be 17 in 2026, and then the valuation will depend on what is the outlook for the company from 2026 to 2031 – something too hard for me to estimate, especially given the bad times the company had in the past.

I’ve looked at many companies in the space (ASM stock analysis, ASML stock analysis), and each has its own new tech – what tech will prevail? Hard to know.

The sector is one to look at when all looks bad, as would Benjamin Graham say: “Be greedy when others are fearful and be fearful when others are greedy” – I know you heard this quote many times, but it can never be overused because it summarizes all you need to know about investing.

To know when to be greedy, subscribe to my newsletter: