ASM International Stock Analysis – This Is What I’m Looking For

This ASM International (AMS: ASM) stock analysis is part of my full analysis of every stock traded on the Amsterdam Stock Exchange. My goal is to find stocks to invest in that offer 10-bagger long-term investing potential, so as would Buffett say; I start with the As.

I’ll first give a business overview of ASM International NV, discuss the stock price, compare it to the fundamentals and consequently make an investment conclusion.

ASM International stock analysis – business overview

ASM has a leading position in atomic layer deposition (ALD). ALD makes it possible to create ultra-thin films of material that are necessary for chipmakers to make better and better and more complex chips. Given the expected growth in the chip industry, ASM expects ALD technology to be the fastest growing in the industry as chip makers focus on smaller geometries, more complex device structures and new materials.

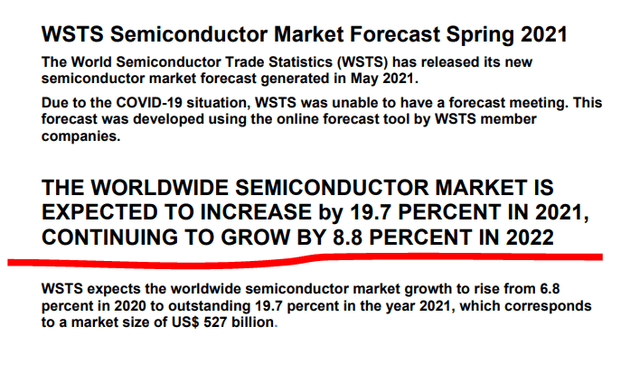

The WSTS market forecast is for semiconductor industry growth to be at 19.7% in 2021 and then continue to grow at 8.8% in 2022. We have discussed how TSMC expects 15% revenue growth ahead and Intel is also stepping up with their investment in chip fabrication.

All this activity and specialization should be very good for ASMI but the growth in demand for ALD tools is also attracting bigger competitors like LAM Research and Applied Materials that will certainly take some market share from ASMI but still, structural sector growth is always a positive. Let’s see how the positive trends reflect the ASMI stock, the fundamentals and the investment case.

ASM stock price overview – AMS:ASMI

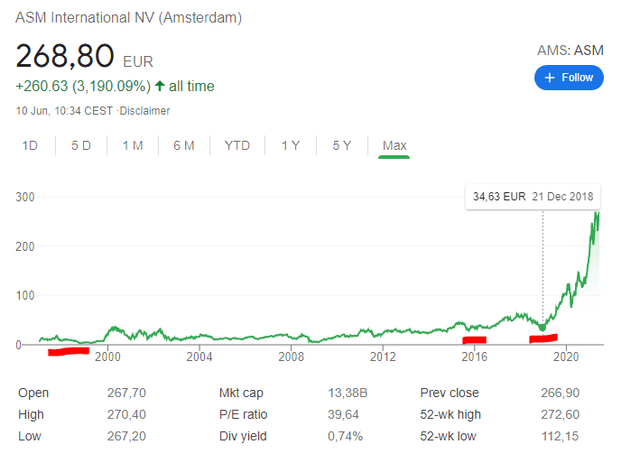

Of course, it is too late to catch the growth in the semiconductor space with ASM stock because the stock is up 8 times since 2018. The situation looks similar to ASML stock that I discussed in my video overview of the EuroStoxx 50 Index – ASML stock is very exuberantly valued.

Let’s see the fundamentals that will tell us whether it ASMI stock is also exuberantly valued despite the potential growth going forward.

ASM stock analysis – Fundamentals

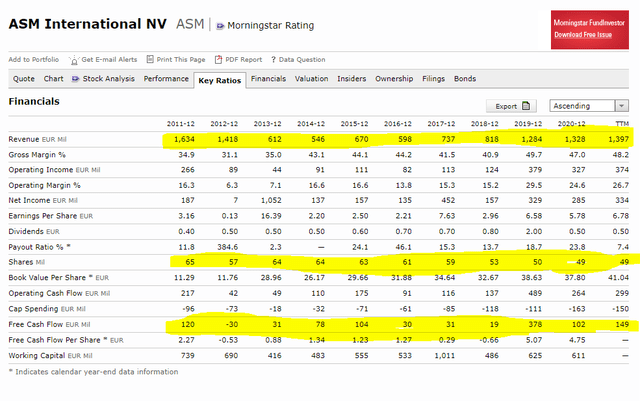

Revenues have been growing since 2014, slowly and steadily up to 2018 and booming since. The company has also been doing buybacks since 2018 and net income is around 300 million EUR per year. Free cash flows are much lower as ASMI has to invest heavily to compete with bigger players.

A digression here: As I am a researcher, I am always curious about what I should had seen before the stock went up 8x already.

So, what I see is the 2014 to 2017 period with slow and steady growth, a decline in margins in 2018 and lower free cash flows, likely due to investments. But those investments are the ones that allowed for the boom afterwards. Growth rates increased, margins improved, net income went up 3x and the stock went up 8x as the market became exuberant and expanded valuation.

My conclusion is that one has to look for a good business that is doing well, investing but still under the radar. In 2017, the company had a market cap of below 2 billion EUR, low cash flows and was under the radar, but was doing buybacks already, was growing, so the quality was there. Good to learn. The funny thing is that the management told us what was going on in the 2017 annual report where another interesting fact is that they had 800 million EUR in cash from selling a stake in ASMPT.

In 2018 the market cap was below 2 billion EUR on the good numbers above. A perfect example of what to look at when it comes to investing:

Look a few years ahead of the market and look for quality already there that can be scaled but is not yet recognized by the market. When the market recognizes what is going on, expect an improvement in fundamentals and an increase in multiples that create 5 or even 10 baggers.

ASM International stock analysis – Investment case

Anyway, back to ASM stock now, sales are 1.4 billion EUR and net income is just below 400 billion EUR which means the PE ratio is 35. 35 is not that crazy for fast growth expected ahead but it was sure better when the PE ratio was 10 in 2018. They should triple net income to get back to a PE ratio of 10 which they will likely achieve but if demand slows down when they do it, we will have a contraction in valuation and the business might be doing great while the stock price might go nowhere. So, at this moment there is a bit too much exuberance in the semiconductor sector and consequently the risk related to investing in ASM stock is also high. I will come back to it when things cool off, if they ever cool off.

For investing in ASM stock now, I have this valuation issue as I personally prefer finding something like ASM stock before the market gets crazy about it. This is also the reason why I focus on looking at stocks lists, one by one; here or there I find something very interesting. So, I’ll continue with my Dutch stock list and I am sure I’ll find an ASM 2015 to 2017 like stock – I only need one such business in a year and I’ll do great.

Here is a video (to be available soon) discussing my investing strategy why I believe it is possible to find stocks like ASM stock before those explode and enjoy 2x to 10x upside over a period of 5 to 10 years. If you 5x on average every 7 years, in 30 years you have made 625 times your initial investment – well worth the effort.

About the author: Sven Carlin Ph.D. is a dedicated investing educator and stock market researcher focused on finding investment opportunities with a value investing perspective. His research is summarized on the Sven Carlin Research Platform where he covers many stocks and shows his portfolios. The educational part is shared on YouTube and the Free Stock Market Investing Course.