Auckland Airport Stock Analysis – Good Business

I continue with my analyses of airport stocks so don’t forget to check the full airport stock analysis list here.

Here is the Sydney Airport stock video comparison with Auckland stock. Article continues below:

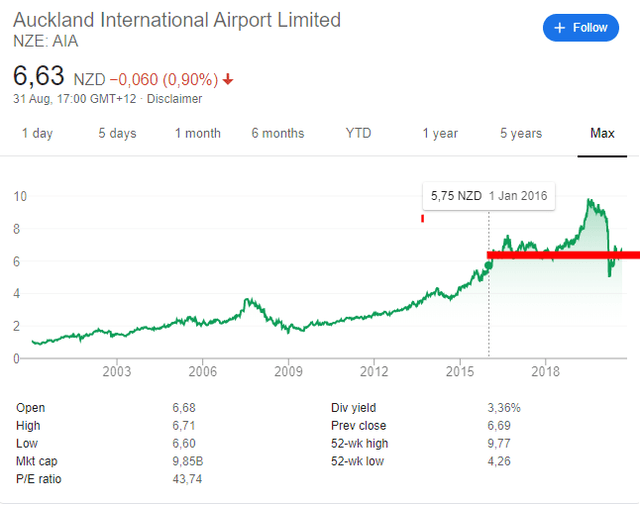

Auckland Airport stock price action and overview

Auckland Airport stock, similar to Sydney airport stock, is down approximately 50% from its 2019 peak.

Auckland Airport market capitalization is NZD 9.85 billion and the stock trades on the New Zealand stock exchange with ticker AIA. Auckland Airport stock also trades on the Australian stock exchange:

ASX: AIA

And in North America on OTC with the ADR:

AUKNY

1 ADR represents 5 normal shares.

This Auckland Airport stock analysis will give a:

- Business overview

- Fundamental analysis

- Dividend discussions

- Investment conclusion

Auckland Airport business overview

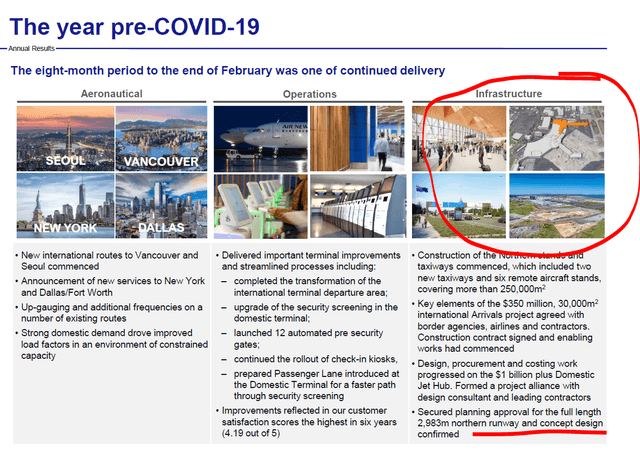

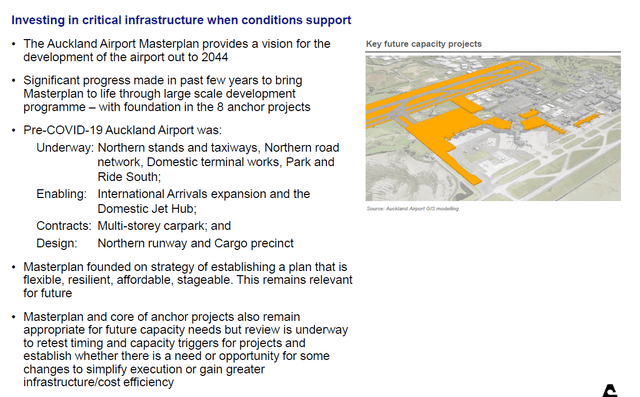

Pre COVID-19 for Auckland airport was in high growth environment with lots of new investments alongside plans for even a new northern runway.

Given the current situation, the high level of investments will resume when things improve.

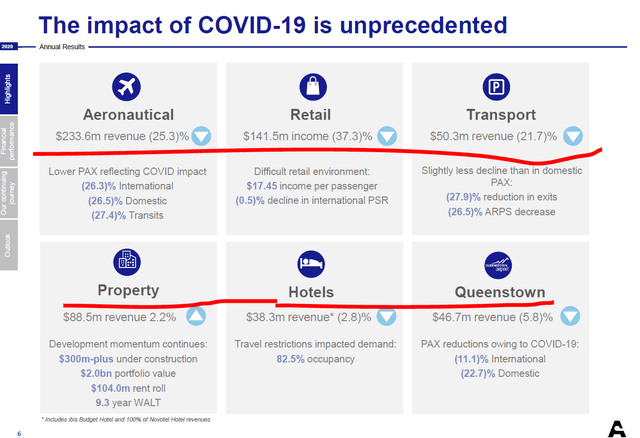

In the mean-time, we as investors have to focus on what is there now and what will be the likely cash flows when things normalize. For now, metrics are significantly down but still show what the business is about. The revenues are divided by aeronautical, retail, transport, property, hotels and Queenstown Airport.

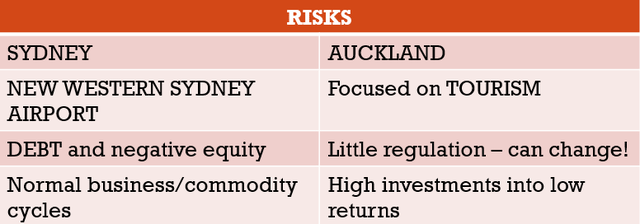

The main risks when it comes to investing in Auckland Airport come from changes in tourism, tighter regulations and possible lower than expected returns on the high investments. I would love to visit New Zealand so I don’t know whether it will go out of fashion, but it is one of the risks one has to keep an eye on.

Let’s take a look at the fundamentals.

Auckland Airport fundamentals

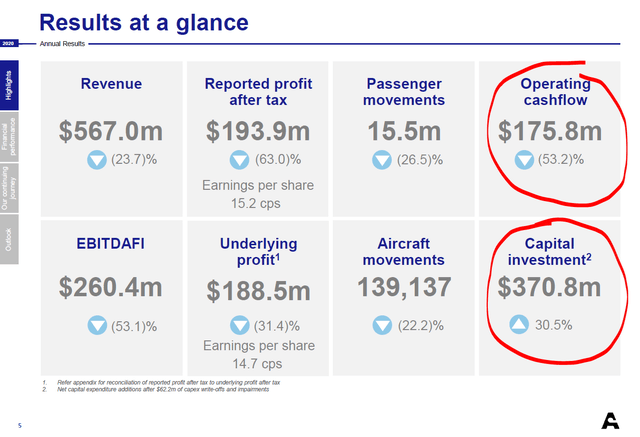

Logically, due to COVID-19 there has been a significant decline in all financial metrics but in order to understand this as an investment, we need to focus on what is likely to be there when the situation normalizes.

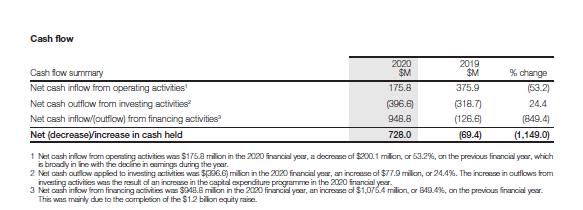

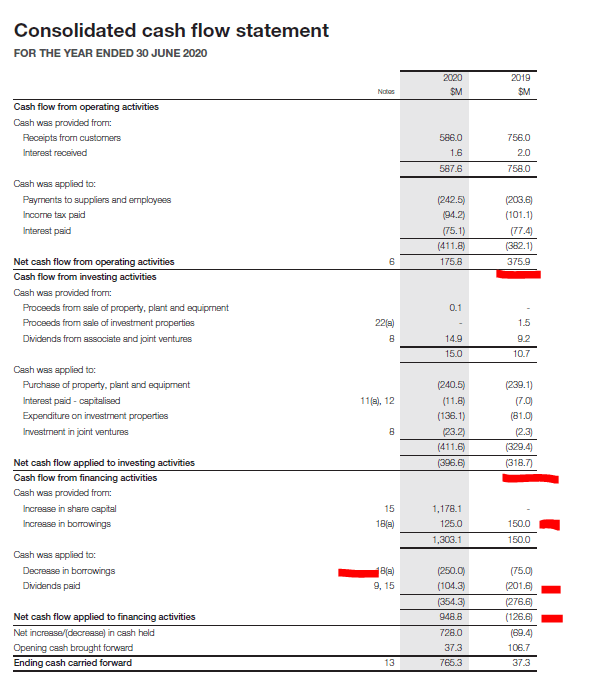

Cash flows in a normal year should be double the cash flows in fiscal year 2020 that ended June 2020. Thus, around NZD 350 million. That covers the high capital investments that are needed to cover for the growth plans.

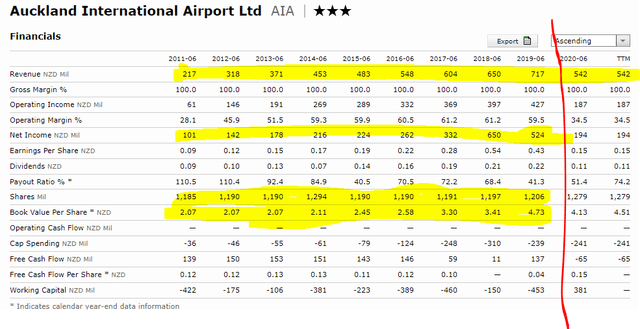

Revenue growth has been staggering over the past decade, book value has more than doubled despite the generous dividends and the share count didn’t increase significantly.

One must note here that book value increases have also come from asset revaluations but as the airport has a huge landbank of 15,000 hectares, it might have the right to do so.

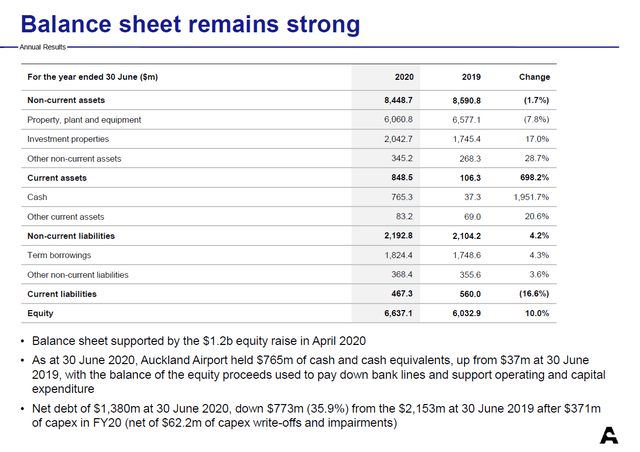

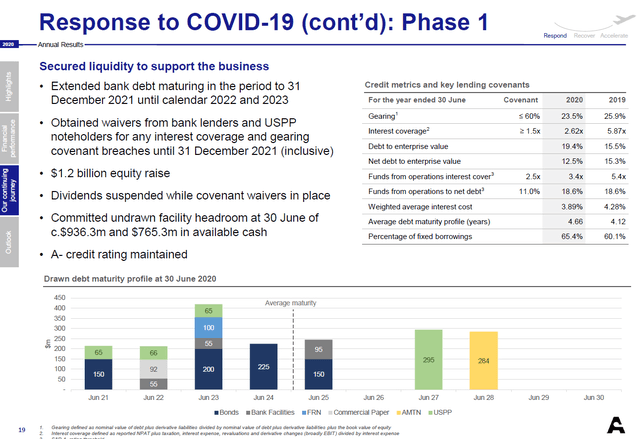

The balance sheet is strong and the recent NZD 1.2 billion equity raise strengthens it and allows for investments and safety until the COVID-19 situation improves.

There is a huge difference between Auckland and Sydney airport. Sydney has no shareholder equity while Auckland’s goes up to 6.6 billion NZD. The debt with Auckland is also just 1.8 billion NZD compared to Sydney’s AUD 9 billion. Auckland Airport’s strategy is a less risky one from a capital structure, shareholder reward perspective.

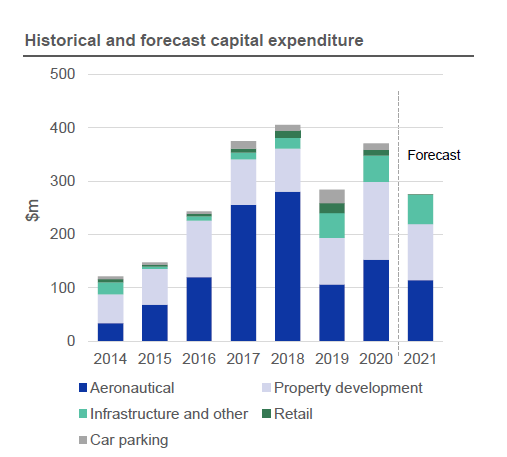

Also, Auckland has been heavily investing in development and will continue to do so.

If it is likely the company continues to spend NZD 300 million per year, we have to deduct such cash flows from the contribution to shareholders. When the investment cycle finishes, it will likely bring to higher cash flows and higher dividends.

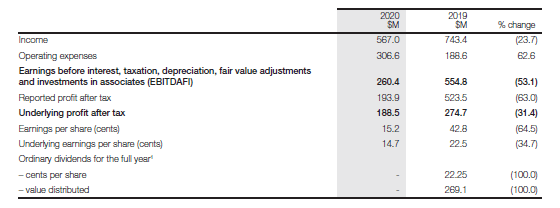

On EBITDA of 554.8 million in 2019, the company distributed 269 million in dividends or 22.25 cents per share.

As long as they are growing, they are keeping their divided by issuing debt. But we can say the value created for shareholders per year is around 300 million per year, in a good year.

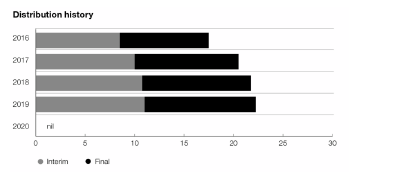

Business growth allowed for constant distribution growth up till COVID-19.

If we focus on cash flows and take an average 100 million sustaining capital expense, we can say the value created for shareholders per year could be around 300 million.

Auckand Airport stock valuation and investment thesis

300 million of cash flows on a market capitalization of almost 10 billion gives a 3% return and thus it is all about growth. It is likely there will be more growth as tourism develops in the world but for now, Sydney Airport stock is cheaper and looks like less under the impact of cycles. If the company manages to grow earnings 5% thanks to the investments, long-term returns should be around 8%.

However, there will be cycles, pandemics and who knows what that might lower the long-term growth rate.

My conclusion is simple, for similar growth prospects based on global air traffic growth, European airports are much cheaper than both Auckland and Sydney airport.

I understand low single digit investment returns are attractive when interest rates are at zero, but that can too change over the long-term.

If you enjoyed my airport stock analyses, please subscribe to my newsletter: