AT&T Stock Analysis – Undervalued, But Sell When Not Limping

Here is the AT&T stock analysis video, article continues below. For more stock analyses check my blog or my YT Channel.

AT&T Stock Price Analysis – not going well

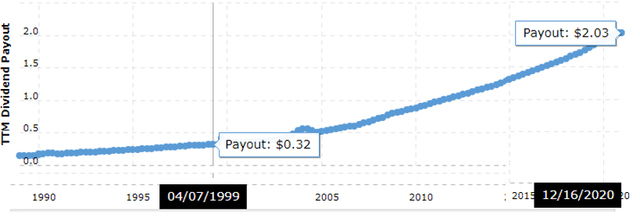

AT&T’s stock price shows the risks of investing in something perceived as safe. On one hand, yes, the company has quadrupled its dividend over the past 15 years, but the stock price didn’t really go anywhere and has been hit hard, especially over the last few years.

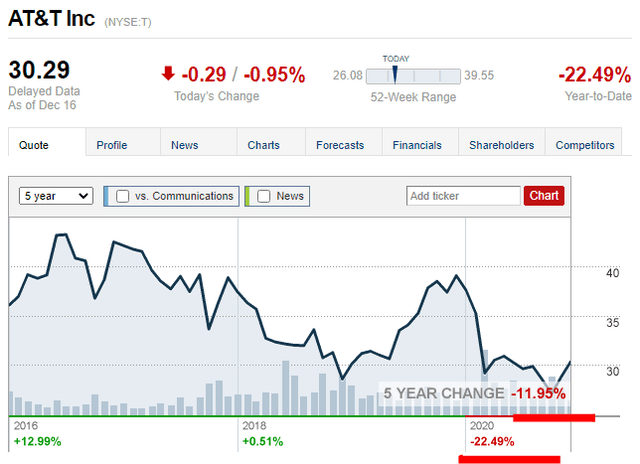

Over the last 5 years, AT&T’s stock performance has been terrible, especially when compared to the S&P 500 that is up 78.54%.

AT&T stock 5 years performance – Source: AT&T quote CNN Money

AT&T stock 5 years performance – Source: AT&T quote CNN Money

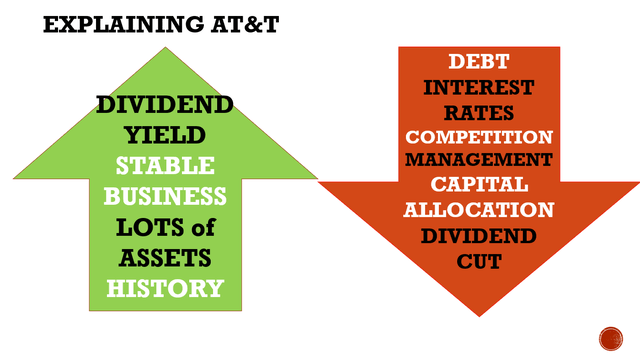

To me, the above shows the risks of investing in things that seem certain but really aren’t. AT&T always looks like a company with a huge stable business that leads to a safe dividend and you always wonder why is the stock punished so hard, why is the yield so high and how the market is very wrong.

Well, it is also possible that the dividend is the just a tree, but the company is doing whatever it can to keep the tree in your focus (constantly increasing dividends over time) and not let you see the forest, the forest of debt in AT&T’s case.

Plus, instead of sticking to things that are certain, the company constantly tries to please Wall Street, or greedy shareholders, and does acquisitions that don’t really add much value to shareholders.

Further, the management is still working on transforming the company, implicitly saying that what had been done isn’t really good.

And there is no guarantee that the new transformations will be beneficial for shareholders. Creating a diversified telecom and media company sounds good, but it is risky, very risky. The problem with transformation strategies and big acquisitions is that most of those fail.

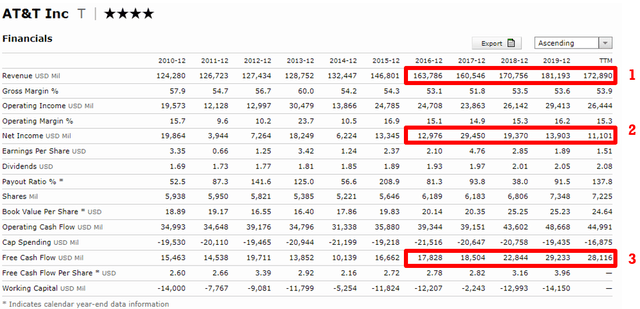

But, if you are an investment banker, selling a M&A idea to a company like AT&T that has a slow revenue growth issue (1), declining net income (2) but high cash flows (3) that allow it to tap debt markets easily, it’s easy as pie. In a world where the key is growth, the management is desperate to give the impression they are busy, working hard and growing, so they are desperate for acquisitions.

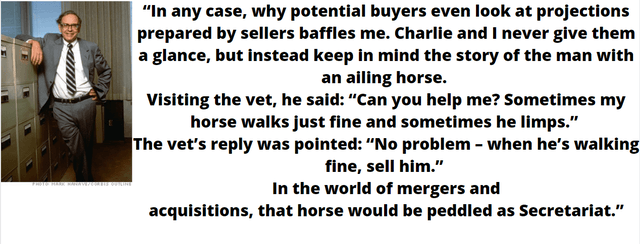

The problem with acquisition is that people forget how markets, economies, nature; actually, everything is cyclical. Therefore, most acquisitions are done in really good times when the buyer can find the money and the seller get a good price for his business. As Buffett puts it, the problems arise when the cycle turns and the horse starts limping again.

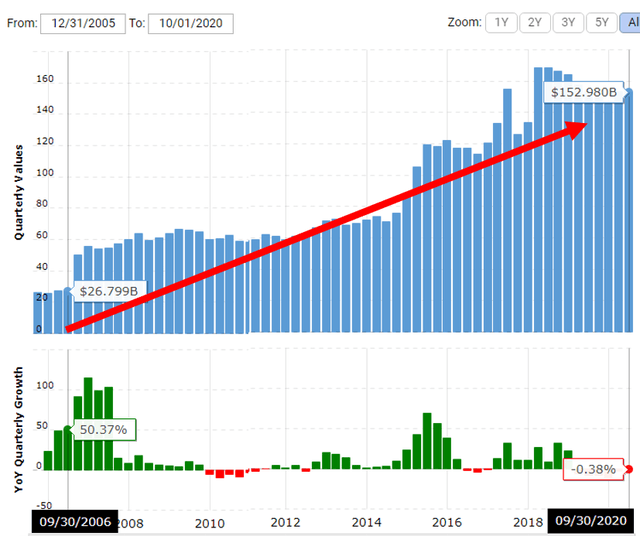

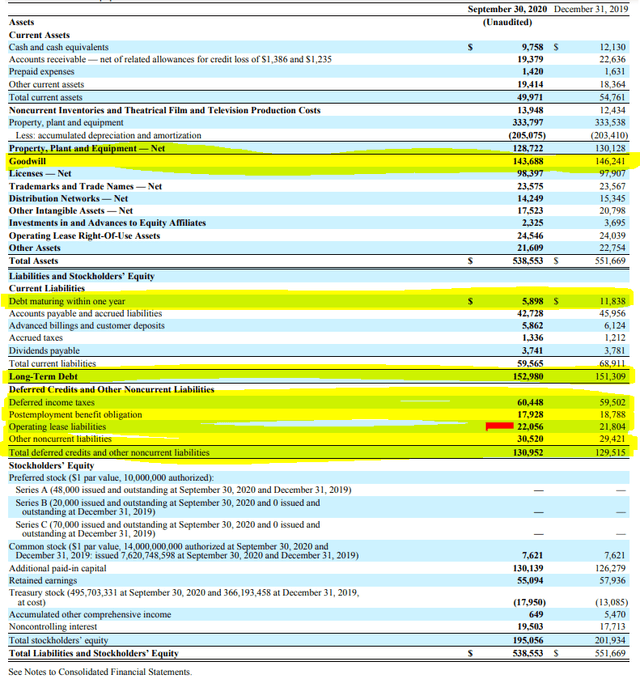

Fortunately, AT&T has no plans to make new acquisitions in the coming 3 years, but you never know. Past acquisitions led to an inflating balance sheet where debt went from $27 billion in 2006 to the current $153 billion. (we are at $159 billion if I add the current portion of long-term debt)

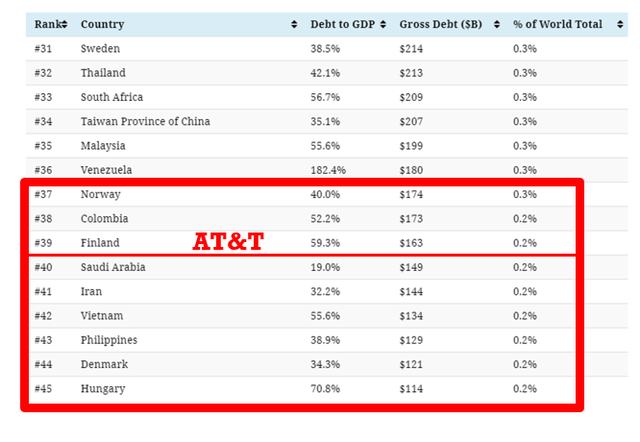

The funny thing here is that if AT&T would be a country, it would be ranked 40th on the global debt level list.

As A&T needs $14 billion to pay its dividend per year, and those numbers were lower over the last 10 years, we could say the company hasn’t created any value since 2005 because when I divide the $125 billion increase in debt over the last 15 years, I get $8.3 billion. This means that the last 15 years of dividends have been financed by issuing debt.

I am sure AT&T can’t continue like this for long and that is one of the negatives that is reflected in the current stock price. On the other hand, there have been acquisitions, investments etc. but with no revenue growth, you can only squeeze so much.

AT&T’s story is similar to the IBM story that we discussed here: IBM stock analysis. However, the above is the past and we must look into the future as the stock is low and might represent an opportunity.

AT&T stock analysis – business outlook

We don’t have to spend much time on AT&T’s business. There are 4 segments where the core of the business is still communications.

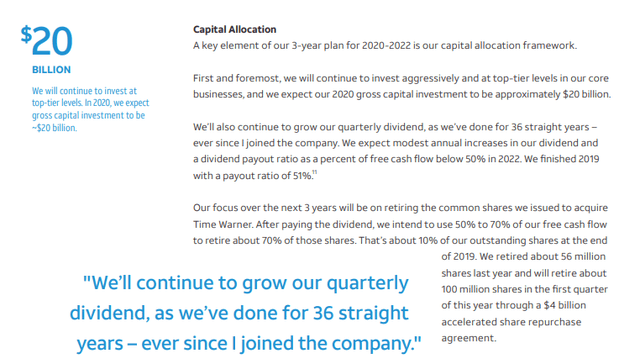

The company expects to see stable revenues in the future and to keep free cash flows at around $28 billion per year. Of those cash flows, the capital allocation plan is the following:

- $15 billion for dividends

- Remaining for share repurchases and debt retirement

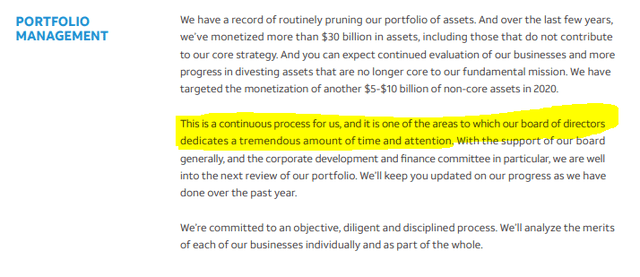

While reading the annual report I also found something interesting which is their focus on asset sales where the board dedicates immense amounts of time.

My thoughts here are that they are not focusing on organic growth, so in 3 years they will be bored again, the results of the previous acquisitions will not be stellar, revenues will start declining, cash flows too, and they will search for a new acquisition and there will be an investment bank that will deliver the idea for sure, and even do everything to find the money.

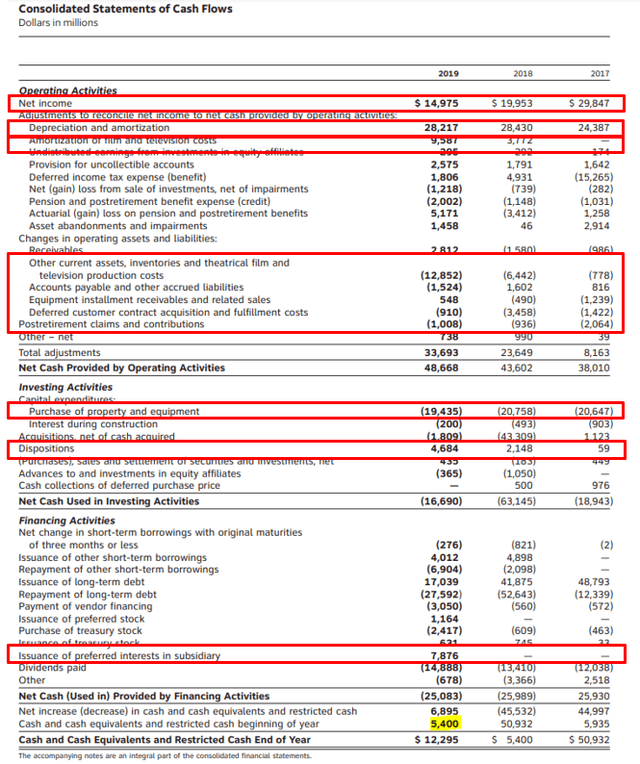

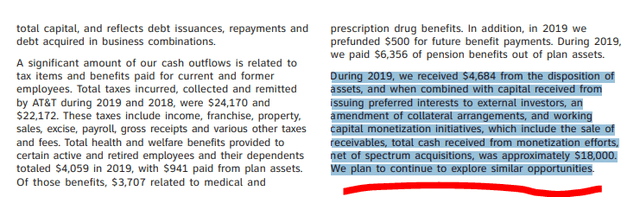

Before valuing the company, I have a problem with their expected free cash flows of $30 billion per year because I see them in the cash flow statement, but I can’t find the $30 billion in asset sales monetization over the last few years. I can only find $4.6 billion in 2019 and $2.1 billion in 2018.

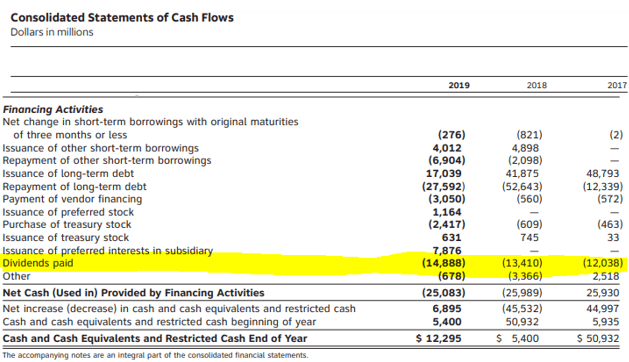

When it comes to what really matters when investing; how you reward shareholders or repay debt, in 2019 AT&T paid $15 billion for dividends, $2 billion for repurchases net of issuances and increased its cash position by $7 billion while lowering debt for $12 billion but also issuing preferred shares for $9 billion. So, after all the mumbo jumbo I get:

$15 dividends +$2 buybacks + $7 cash + $12 billion decrease in debt – $9 billion issuance of preferred shares = $27 billion which is in line with what the company says, but I miss the billions from the asset sales.

By looking deeper, I found the explanation, the issuance of preferred shares is included in their cash flow calculation through the issuance of preferred shares. However, I still don’t find the $30 billion the management discusses have been sold over the last years or $18 billion over 2019.

So, yes, asset monetization improves the looks of the balance sheet, but the reality is that without that AT&T would have just enough for the dividend, buybacks and a bit of debt repayment which is an issue, a big one.

AT&T stock analysis fundamentals – the big debt issue

In total, when I add the debt and the future obligations that are debt, but called differently, I see $250 billion of debt obligations that the company will have to pay one day that is the main problem with AT&T. Comparing with countries again, the Russian government debt gets to $232 billion.

The problem is that if there is any kind of small slow down in the business, increased competition and free cash flows fall from $28 billion to let’s say $25, AT&T would be in a pickle.

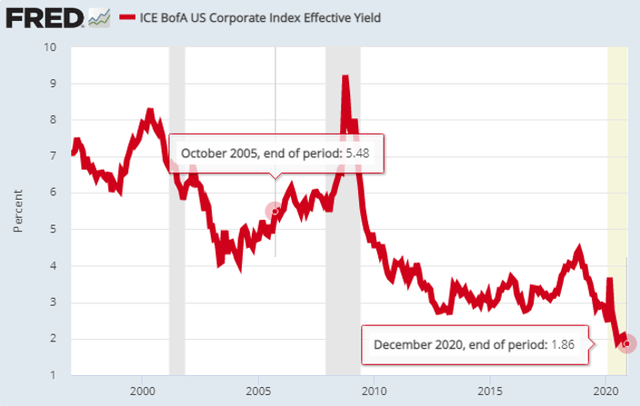

Keep in mind interest rates on debt are at historical lows. The US investment grade corporate bond yield is at 1.86% which is almost 400 basis points lower than in the 2000s.

Imagine the hit to AT&T if interest rates would go up due to inflation. I believe inflation is already here but hasn’t yet been acknowledge through statistics but the day will come, and then trouble will come. Given the competitiveness in AT&T’s business, the constant fight for customers by racing to the bottom with prices, it is likely the company will not have much pricing power which means that debt costs and other costs would start going up while revenues would grow slower than inflation.

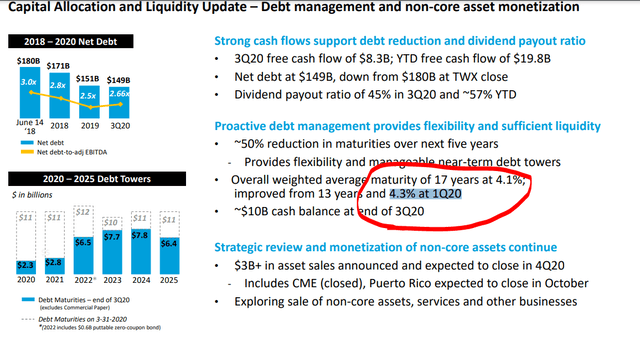

Interest costs on $159 billion at 4.1% are $6.5 billion per year, if rates for AT&T spike, and that is something that can happen fast if bondholders panic, the whole historical AT&T behemoth could crumble under the weight of its debt.

With ‘only’ $25 billion in free cash flows, there would be only $10 billion left after paying the dividend, if $4 is spend on buybacks, $6 remains for other – on the $250 billion debt pile, it takes you 40 years to lower it or better to say never.

Plus, with $25 billion in cash flows, the free cash flow to debt pile is 10, that is a lot.

AT&T stock valuation and investment strategy

We have explained AT&T but let’s see now how the above fits AT&T’s current stock price.

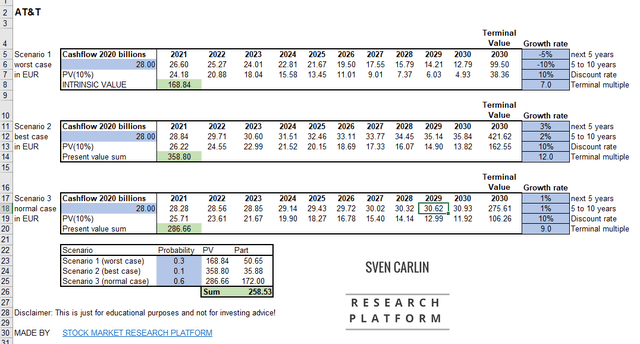

You can download the above AT&T valuation template here if you wish.

With a 10% discount rate and a 30% chance of a bad scenario, 10% of a best scenario and a 60% chance for a normal scenario where revenue grows at 1% per year, I get a value for AT&T of $258 billion which puts AT&T, with the current market cap of $221 billion, in the undervalued basked.

However, the market might be more focused on the difficult possible times ahead. On thing is mathematics, the other is the market’s perspective. If the worst-case scenario really happens, and cash flows decline significantly, bond holders might get scared, refinancing might become an issue involving asset sales (don’t forget in crises you need to sell the gems), which could bring AT&T’s market capitalization quickly down to $100 billion.

Plus, there are other risks like the USD for international investors where a currency depreciation might eliminate all the benefits of a strong dividend.

From my personal standpoint, I can find companies paying a 7% yield, growing 5% per year on top of the dividend, that have pricing power, natural moats and a debt to free cash flow of 1. So, I’ll stick to those and not follow AT&T despite the fact that it is undervalued because for me, it is also important to sleep well when investing.

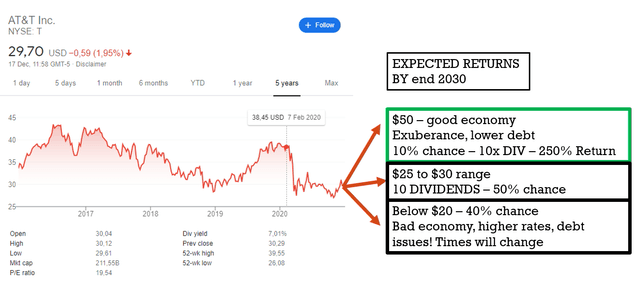

If you are long or consider going long AT&T, I agree on the undervaluation thesis, the high dividend and the strong cash flows produced by the business. However, given the debt pile, AT&T looks like a horse that sometimes walks just fine and sometimes limps.

I think the horse is still limping currently as the stock price is below $30, so be sure to sell the stock when it looks like AT&T is walking just fine because, I am sure the horse will limp again in the future and perhaps even drop dead due to the huge debt in the long-term.

So, the short-term investing outlook would be the following and it is a positive risk reward proposition. The 7% dividend yield gives you a good return in case of things remaining as is, the positive upside is higher than the downside.

On the long-term, I must say I am a bit more concerned because the probability of inflation is much higher while the competition for AT&T will only intensify and as the company is focused on selling assets, thus on a short-term perspective, the long-term outlook isn’t good.

Yes, AT&T is undervalued but be sure to sell the horse when it is not limping.

I am not going to follow AT&T because I can find companies with similar dividend yields, high single digit growth rates and much lower debt levels. You can check what I do on my Stock Market Research Platform.