AT&S Stock Analysis – An Interesting 5G, IoT, Connection Stock (Possible Double)

AT&S Stock Analysis – Quote

AT&S Austria Technologie & Systemtechnik AG

FRA: AUS

VIE: ATS

This AT&S stock analysis is part of my full analysis, stock by stock of all the stocks listed on the Austrian Stock Exchange. Austria is one of the cheapest stock markets globally at the moment so please check the Austria Stock List for interesting investments.

AT&S Stock Analysis – Business overview

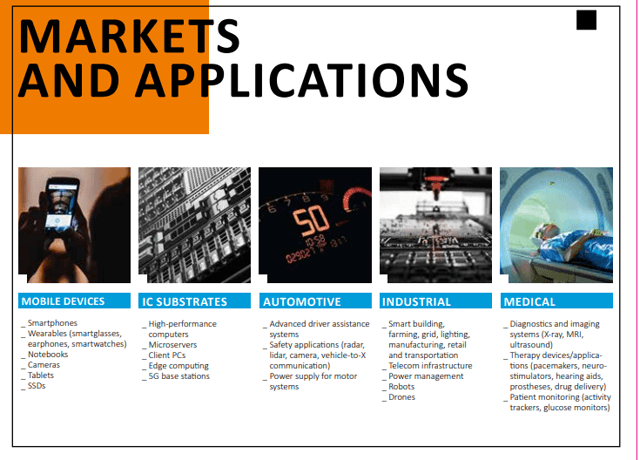

AT&S stock also known as AT & S Austria Technologie & Systemtechnik Aktiengesellschaft designs and manufactures high-end printed circuit boards and substrates for semiconductors.

Their products are used in many applications and the sectors are definitely growth sectors.

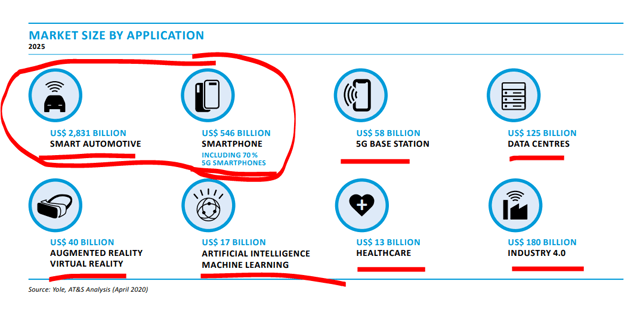

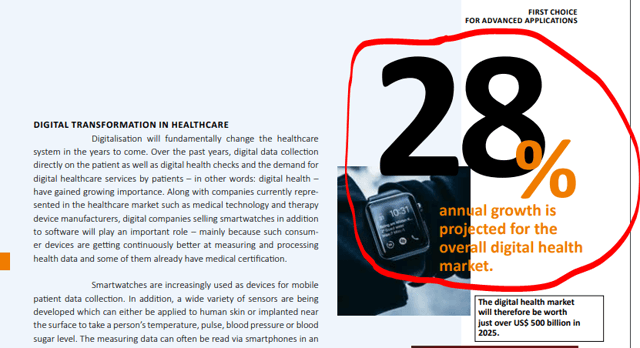

This is the expected market application by 2025:

I guess, that the other segments like AR, AI, healthcare etc might reach much higher levels by 2030, which could make AT&S stock boom, but that is the next step probably and a story for beyond 2025.

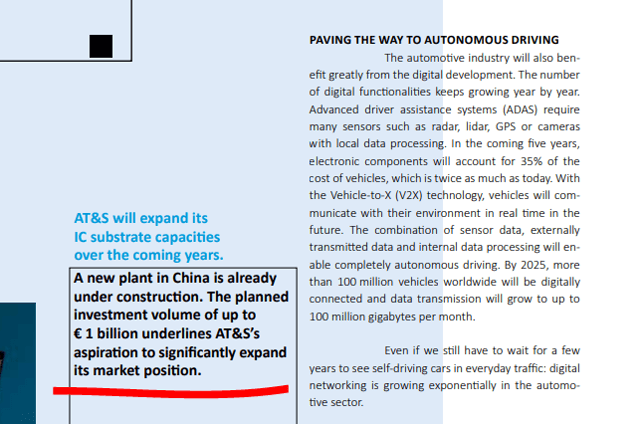

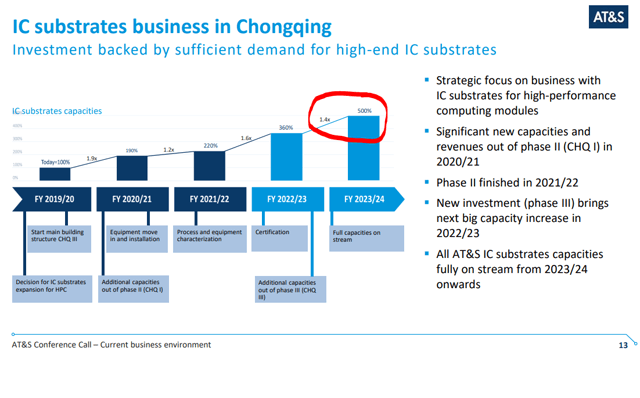

They are investing heavily in to IC substrates production, 1 billion EUR. This is based on the expectation that 100 million vehicles will be digitally connected by 2025 and the growth in data transmission.

All in all, the company sees significant opportunities in the 5G sector, from smartphones, automotive connectivity and other. Network providers are expected to invest $1.1 trillion into the 5G infrastructure between 2020 and 2025 while 24 countries in Asia already have 5G with South Korea being the leader.

The company says it is the leader for circuit boards and IC substrates.

But there is not only communication growth ahead, new technologies will change the way we live in many ways, from autonomous driving to medical treatments.

AT&S Stock Analysis – Management outlook

I have read the management’s outlook and they seem very positive, here are some of my notes:

- plants not fully utilised in 2019

- didn’t meet goals economically due to powertrain future uncertainties, trade wars and weak industrial activity in Europe (this tells me they don’t have a clear competitive advantage)

- Significant business expansion ahead

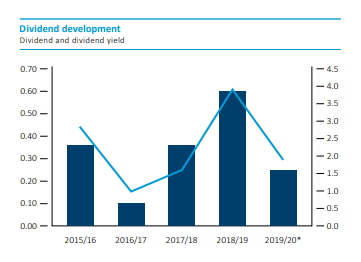

- Dividend of 0.25 EUR per share proposed

Planning ahead:

- In the 5G sector – preparing circuit boards for modules, 5G base stations, antennas etc.

- Significant investments in IC substrates to cover future demand based on data explosion demand where they expect to see many contracts arriving and they will have the capacity ready.

- Investment in Chongqing should bring another billion in revenue.

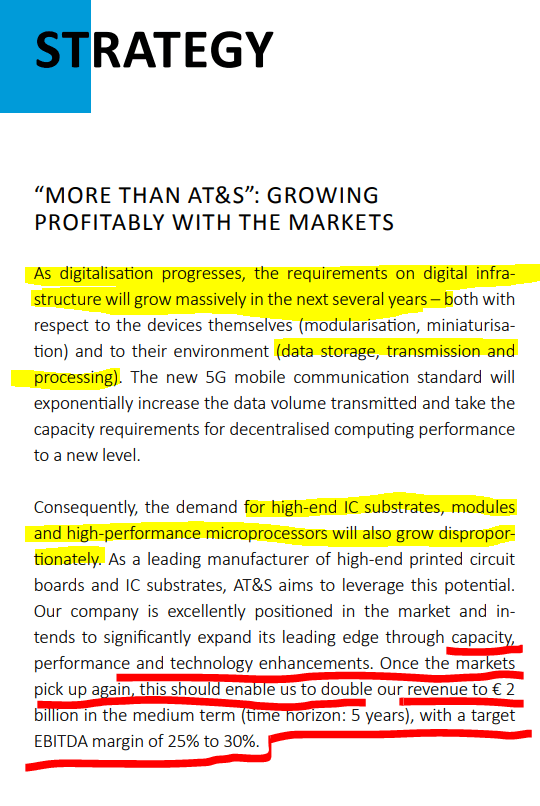

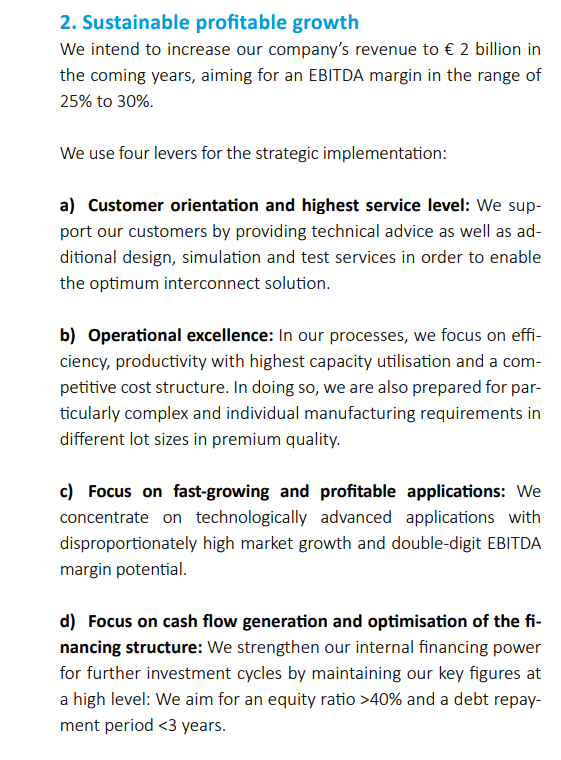

The strategy summary:

I’ll use these metrics in the fundamental analysis.

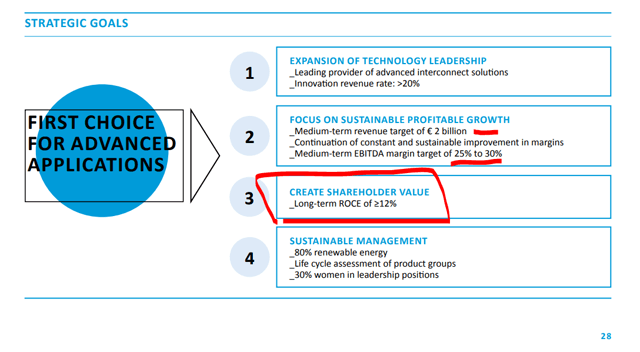

The way they will do it:

This should lead to dividends:

AT&S Stock Analysis – Fundamentals

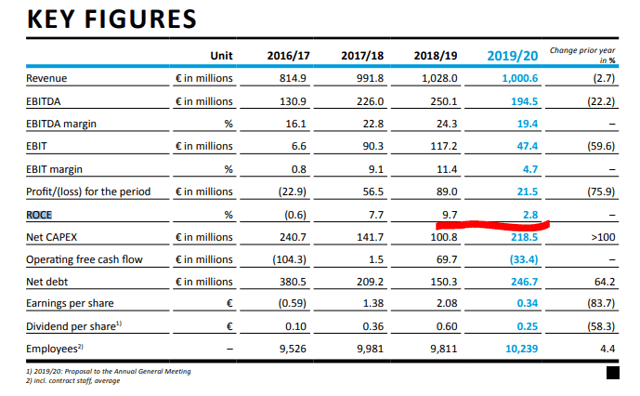

They are mostly using EBITDA for the financial performance but we can easily work out the owner’s returns from that.

Their target is to reach 2 billion EUR in revenue by 2025 with an EBITDA margin of 25% which is similar to the margin achieved in 2018.

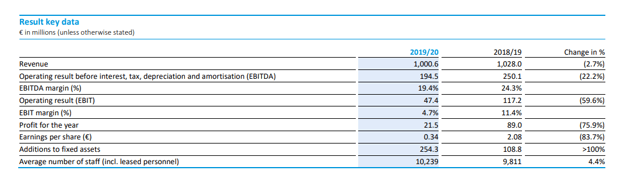

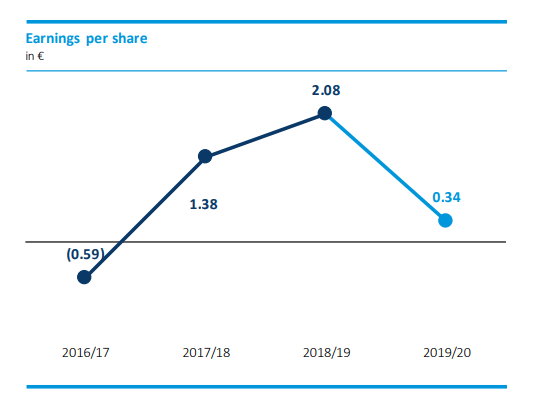

In 2018, the earnings per share were 2.08 EUR. If I double that by 2025, EPS should be 4.16 EUR which is not bad compared to the current price or 16 EUR as I am writing this.

However, the earnings are not linear and depend on the demand for their products. In times of high demand and new technology applications AT&S will likely see higher margins but if 5G is delayed, the benefits of new technologies might disappear quickly as others catch up or copy.

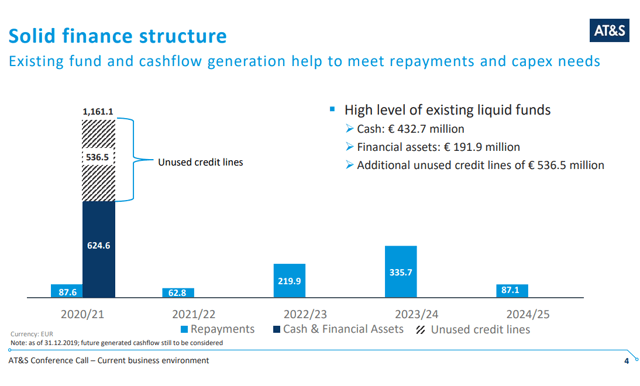

The company’s financial situation looks good and the debt shouldn’t be a burden.

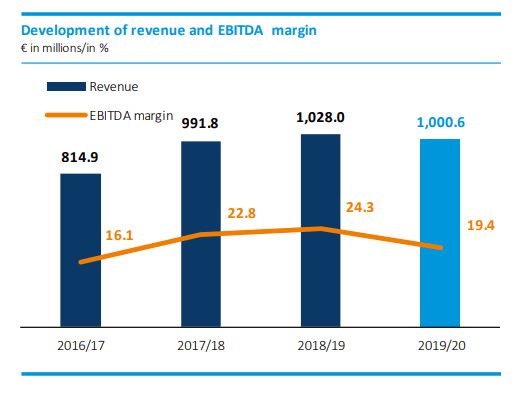

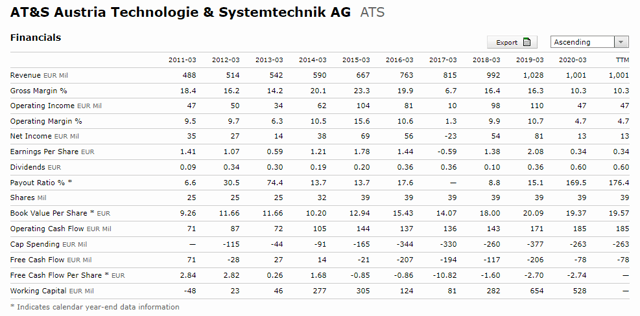

A look at historical fundamentals shows how the company doubled its revenue over the last 10 years. Margins have been volatile, consequently earnings and the dividend too but operating cash flows have been relatively stable.

The company has been investing heavily and spent 1.5 billion EUR in capital expenditures over the last 5 years. Compared to the 659 million market cap it is a significant number.

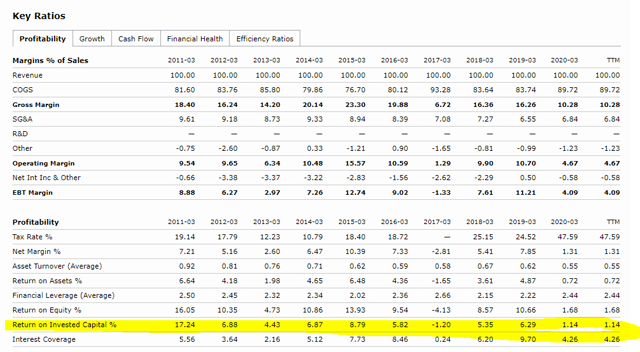

The return on invested capital hasn’t been high and the free cash flows have also been mostly negative. However, the question is what is going to happen next.

The book value is close to 20 EUR per share and above the current stock price, a rare find in today’s investment world.

AT&S Stock Analysis – A look into the past

Whenever I hear such growth promises, I first like to check whether the management achieved on their past promises.

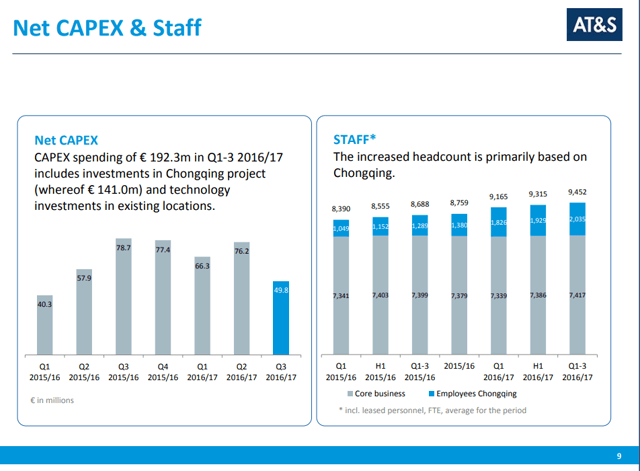

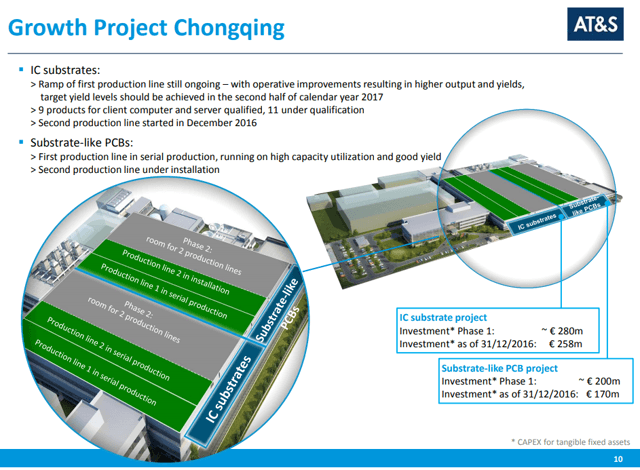

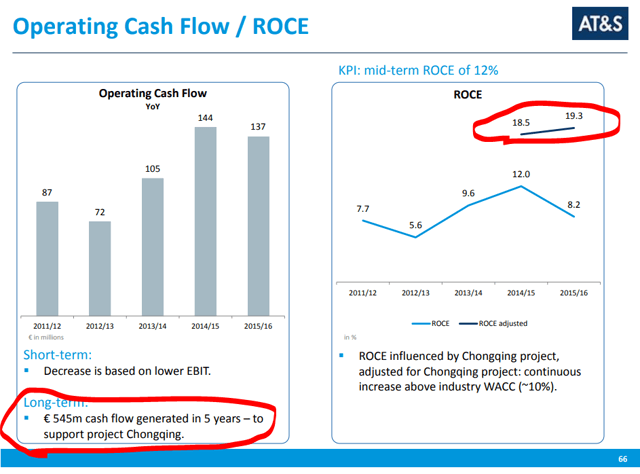

In 2017, their main focus was the development of Chongqing, where they plan to grow further at the moment.

The Chongqing project from 2017

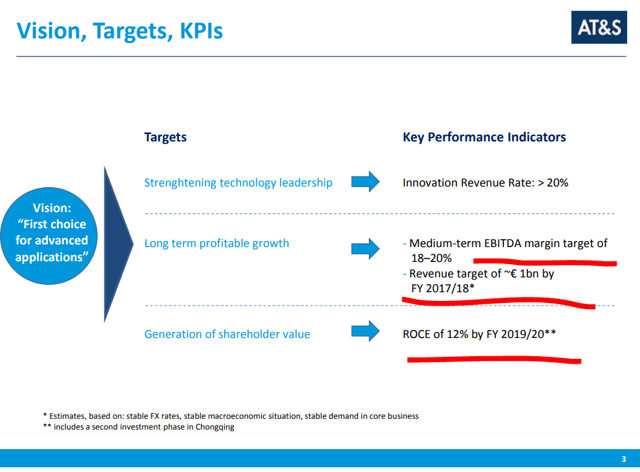

The following was published on their Capital Markets Day in 2016:

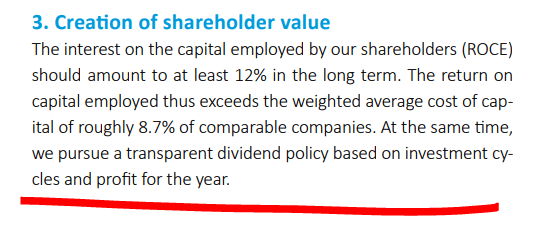

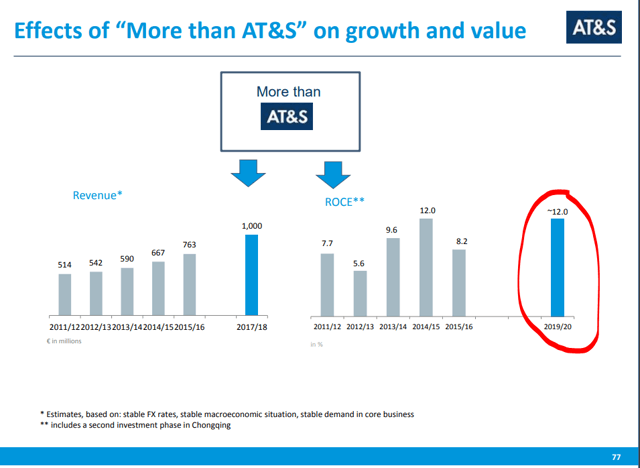

They did hit the 1 billion by 2018, they didn’t hit the 12% ROCE level. However, they have been constantly investing in stage 1, 2 and 3 of their plant which significantly burdens financial metrics. In a few good years, they could do really well.

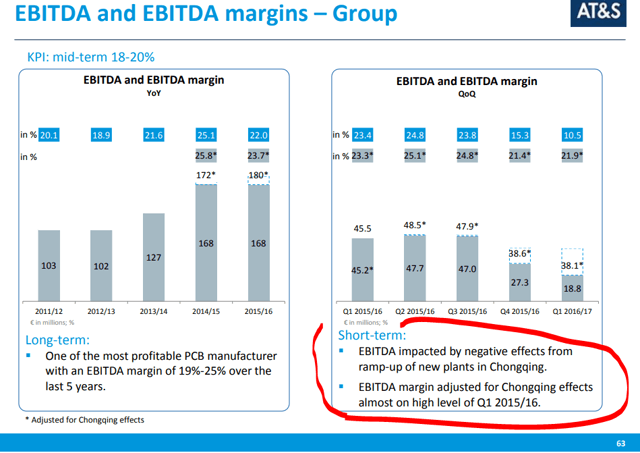

And the metrics become much better.

Their target for 2020 was 12% ROCE.

They were close in 2019, but far in 2020. Although there were different impacts lately.

AT&S Stock Analysis – Conclusion

A company that plans to quintuple production over 5 years, is priced reasonably.

Pays a dividend, albeit volatile, but might be growing in the future. The dividend yield is low, so the investment thesis will depend on their success when serving all the cool industries mentioned within this article.

It is definitely a stock to follow because if they can hit the growth expectation and then more when catching the next trends in the related industries, this can easily be a 10-bagger going from the low current base and with good management behaviour. I am going to follow this, put it on the covered stocks list on my Stock Market Research Platform.

AT&S Stock Price Analysis

The investment returns haven’t been stellar since the IPO on the Frankfurt stock exchange in 1999, but then again, we must consider the exuberance at the times. The stock is definitely volatile but the book value might give it a margin of safety which is key when investing in capacity companies like these.

This is definitely a Lynch growth stock, growing in a not so fancy industry – it is not chips or something – has a fair valuation and high potential. One to watch for the future earnings growth as would Lynch do.

The AT&S Stock Analysis is part of the full Austrian Stock Market Analysis make by Sven Carlin for the Sven Carlin Stock Market Research Platform.

If you wish to receive such analyses to your inbox, please subscribe to my newsletter: