Apple Stock Analysis Explains Investing Risk – Up 314% in 5 years

In my recent Intel Stock Analysis video, I discussed how Intel reminds me very much of Apple in 2016 because of the negative market sentiment combined with strong cash flows. Unfortunately, since 2016 a lot has changed for Apple stock.

Towards the end of the video I asked whether I should analyse Apple and discuss the stock’s hyperbolic rise. There has been a zillion positive comments so here we go. I’ll give my best to discuss all the key matters when it comes to investing in Apple stock today and the great market perspective that Apple’s analysis gives.

Thank you all for commenting and supporting my work.

Here is the Apple stock analysis video, article continues below:

Apple stock history

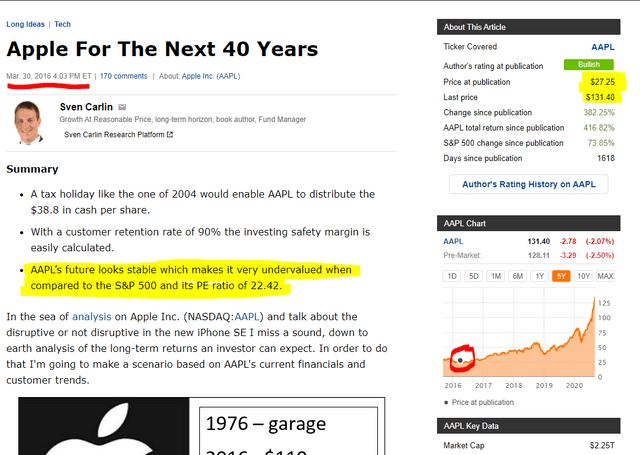

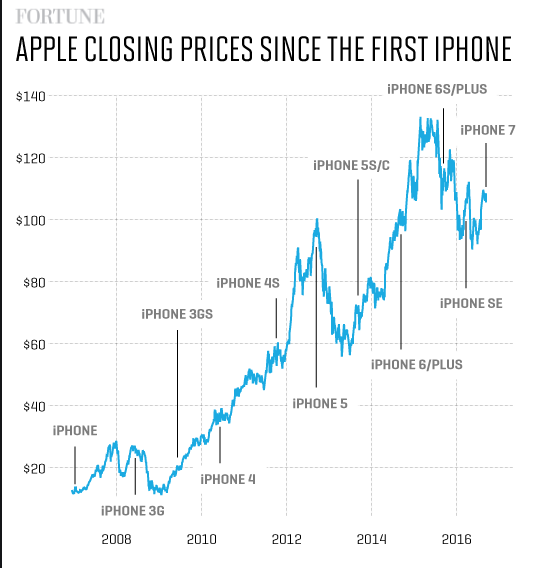

Apple has been a darling topic of mine since 2016. For Apple’s 40th birthday, I wrote an article arguing how Apple is very undervalued because it was trading at a PE ratio of just 10 compared to 22 for the S&P 500. The argument was a pretty simple one to make because Apple was and still is a great business, but it was incredibly cheap back then. Since, the stock quintupled.

The reason why Apple’s stock was so cheap and not loved by the market was because the business had been turning from its fast-growth stage into the slow growing cash cow stage.

Plus, the market didn’t understand Apple’s iPhone cycle; iPhone sales are usually pretty stable, but when the new model is loved the market becomes exuberant and turns into a downtrend, when there is nothing special about the new phone. They key is that the cash flows have always been huge, but the market prefers to focus on noise related whether next quarter sales will go up or down.

Compared to 2016, Apple is the same business as it was back then, but now the market loves it. Consequently, the stock price exploded.

Let’s discuss all the key topics related to Apple and to the stock market in general that will give you enough value and information so that you can make a proper investing decision in relation to your portfolio risk and reward requirements.

Apple stock analysis key topics

We will start with a discussion of Apple’s stock price action and then dig into the most important factors, that are not only important for investing in Apple, but are key factors to understand when it comes to investing in general and the long-term irrationalities growing within the market;

- Valuation – the driver of long-term returns tells you to expect 0%.

- Moats – those come and go, few are forever but Apple’s is stable, for now!

- Fundamentals – financial engineering increases risk!

- Buybacks – not smart at any price!

- Stock splits – just cosmetics!

- Short-term vs. long-term – are you an investor or not?

- Fundamentals – sacrificed for higher stock prices

- Risk – the essence of value investing.

These concepts pretty much sum up the current market, the likely future volatility, and Apple is the perfect stock to discuss it all.

Apple stock analysis content:

- Apple stock price action

- Apple’s business cycle, moat and market perception – earnings

- Apple stock fundamentals – earnings and cash flows

- Apple dividend

- Apple buybacks

- Apple stock split

- Apple stock valuation

- Apple stock summary of investing risks

- Apple stock investing forecast – long vs. short term

- Apple stock conclusion – it is your portfolio!

Apple stock price action – the valuation perspective

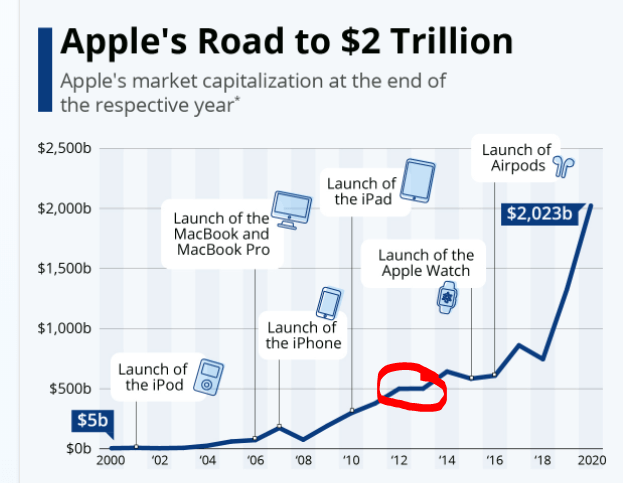

Since I wrote my article on Apple in 2016, the stock quickly doubled over the next two and a half years because it was irrational, from a valuation perspective, that a good business like Apple, having the largest weight with indexes, traded at a price to earnings ratio that was half of the average for the S&P 500. So, 100% the run from 2016 to 2018 was a simple return to the mean for Apple’s stock.

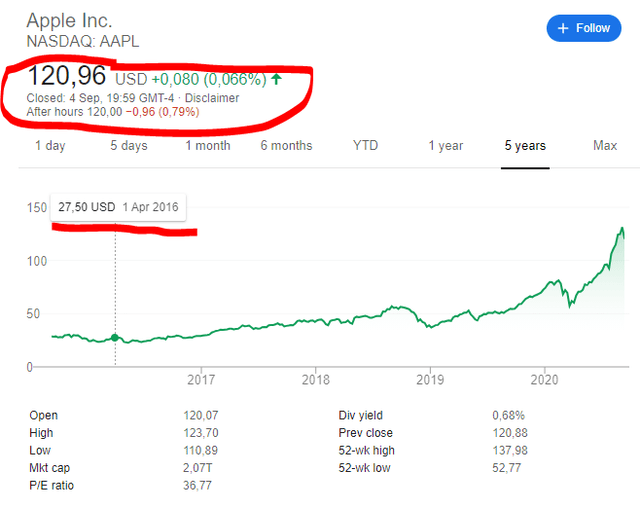

Early 2019 the stock crashed due to China related fears of boycott and other trade issues but that noise quickly faded, there was a crash due to COVID-19 in March 2020 and since then Apple’s stock more than doubled from the March low of $57 to the current $131. This part is not rational and increases the risk of investing in Apple.

The recent drop in Apple stock is likely to just be a correction given the forces driving the stock price that we’ll discuss shortly, but we have to expect high volatility ahead as there is a lot of money speculating in the market and there is risk from a valuation perspective.

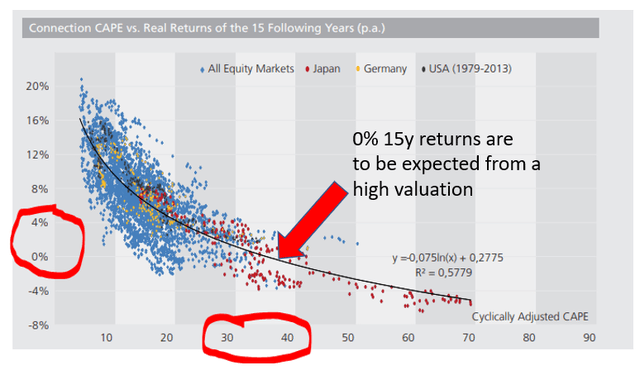

Historically, long-term returns have been low when valuations were high and vice versa. From a current valuation perspective, anything above 3% long-term yearly returns would be a huge positive for Apple and stock market investors.

The key valuation point for Apple stock is that the price to earnings ratio in 2016 was 10, now it is 40. Those that invested in 2016, I sold to early but did similarly over the period so no regrets, achieved amazing returns of 45% per year.

Given the valuation, I would say the probability of reaching such returns again over the coming years is measured in fractions of a percent. However, positive returns can be achieved if the market is happy with low single digit market returns. Compared to interest rates, stocks look cheap and if interest rates remain low for longer, stock are still extremely cheap.

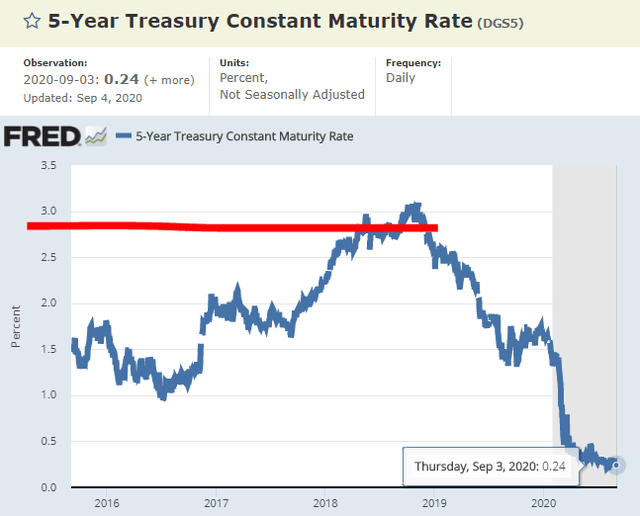

Apple’s 0.68% dividend yield is still better than the yield on the 5-year US Treasury note. Plus, Apple offers possible growth, inflation protection through pricing power and also the buyback yield is there.

Valuation is what makes a big difference when it comes to investing. I would argue that the increase from $27,5 in 2016 to above $50 in 2018 was a rational run-up. The PE ratio returned to the market’s mean as it went form the low teens to the mid-20s which is the S&P 500 average.

However, as the market can’t stay rationale, the stock is now trading at a PE ratio of 40, which is almost twice the market’s valuation. It is incredible how the market can change its sentiment completely in just 4 years. Of course, interest rates have had an impact on the market’s perspective, but Apple’s business didn’t change much. All in all, a higher valuation also means higher investing risks.

Apple’s business cycle, moat and market perception – outlook

The best way to see what is going on within a business is to read the last quarterly report and listen to the conference call.

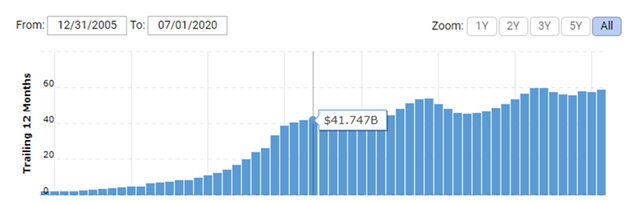

Over the last COVID-19 impacted quarter Apple managed to grow revenues by double digits in both products and services. iPhone revenues grew ‘just’ 2% while other products did much better as the working/studying from home thing happened. This has to be emphasized; iPhone revenue grew ‘just’ 2% to $26.4 billion, but is still making 44% of total revenues of $59.7 billion. Thus, even if iPhone sales are steady over the iPhone cycle, those still make a lot of cash for the company. Further, Apple is building its growth on top of the iPhone/Mac ecosystem and user base where service revenues have been growing in the high teens.

It had been six quarters of iPhone sales declining up till Q2 2020 and analysts all wonder about future growth, but I don’t think that matters that much. It would be nice for Apple, but it is more about the steady cash flows than the growth.

The next iPhone event that should come over the next few weeks will tell a lot about future stock price movements; if the next iPhone is revolutionary, the stock will be pushed higher, if it disappoints, the reaction will be negative in the short term. Unfortunately, we can’t know that before it happens.

As it mostly is the case with earnings calls, most questions were about the short term with back to school questions, TV production COVID-19, currency issues, current iPhone sales strength, gross margins, trade-in promotions and about the Christmas season. Not really something you can make a long-term investing decision on.

The one longer-term question was related to Apple silicon that will allow Apple to have a common architecture on all products and Tim Cook is very excited about it but can’t say much. My conclusion is that Apple also understands the iPhone will continue to be the cash cow while growth can be expected from other venues.

Apple’s moat – 10-year outlook

“If you are not willing to own a stock for 10 years, do not even think about owning it for 10 minutes.” -Warren Buffett.

If you can answer the question what will a business look like in 10 years, you also have a clear indication of your investment success. Apple has a moat because users are unlikely to switch to something else because the few hundred bucks difference in price isn’t that relevant in today’s world for most and the tech specifics are either not meaningful for the untrained eye.

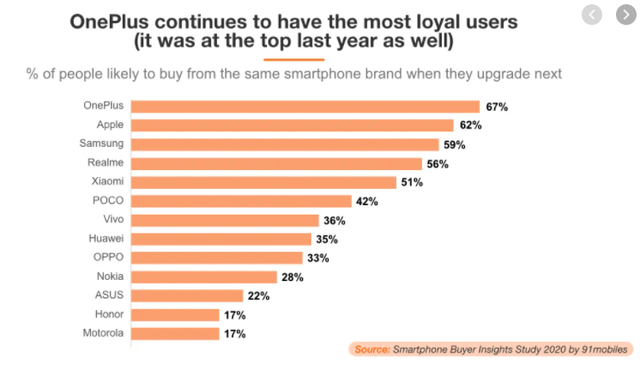

Therefore, we can say that it is likely Apple will still have a strong customer base in 5 or 10 years, but Apple products last long and I don’t feel the need to buy new ones that often. Plus, with a 62% loyalty rate, the acquisition of new customers will likely keep sales strong but growth might be questionable.

iPhone sales had been declining over the 6 quarters prior to the current one. The active base of 1.5 billion installed devices is likely to keep making sales over the next decade, but, except for some great technological improvements or surprise, it isn’t going to be magical as it was the case since the iPhone had been first launched. Also, something revolutionary from the competition might significantly dent Apple’s sales in the future.

We can say that it is business as usual for Apple and for now, the most probable outlook looks stable.

When it comes to investing into this market, ask yourself where can a business be in 10 years. Many of the hot stocks have business models launched within the last 10-years which means there is no barrier for others to entry. This could be very detrimental to your investment when the market turns its focus from the growth promises to the fundamentals as it was the case with Apple in 2015/2016.

Apple stock fundamentals – earnings and cash flows

As would Buffett, who through Berkshire owns more than 5.7% of Apple, say: The value of a business is the present value of all the cash flows created for shareholders from today to judgement day. So, we need to estimate Apple’s free cash flow to see what is its actual value.

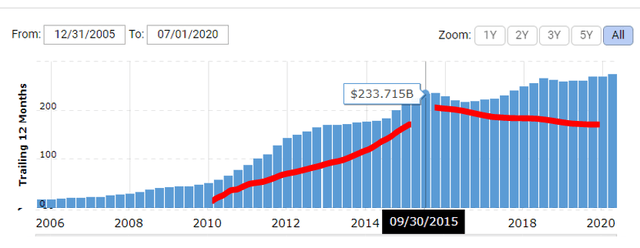

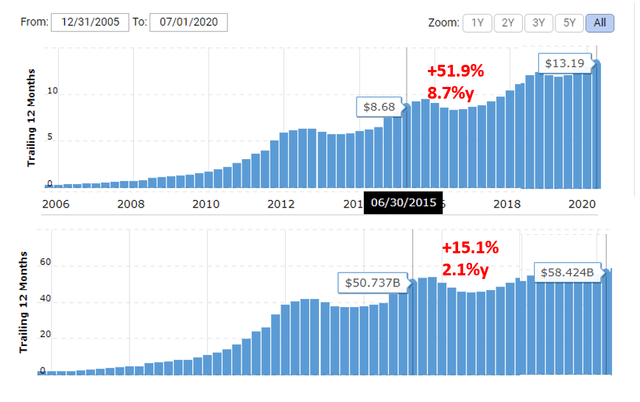

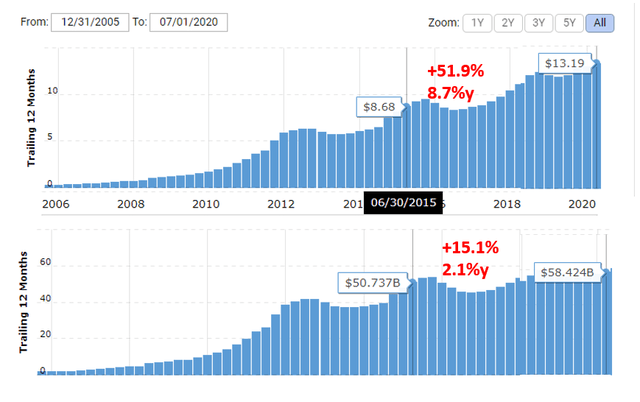

What is peculiar with apple is that over the last 5 years, net income grew only 15.1% or 2.1% on a yearly basis while earnings grew 51.9% or 8.7% on a yearly basis. This is due to buybacks that we’ll discuss a bit later.

The buyback activity has also skewed the accounting value so we are not going to take a look at the balance sheet, but we will discuss what Luca Maestri, CFO, said in the last conference call.

Apple’s goal it to reach a net cash neutral position. To do that they have to still spend $81 billion, likely on buybacks, on top of the $50 or $60 billion in cash that comes in on a yearly basis.

If that happens, it is likely Apple’s book value will go negative.

You might wonder how is it possible that a company making almost $60 billion per year in net income is having its shareholder equity decline extremely fast? Well, that is due to buybacks. If Apple buys its own stock on the market for $120 but its book value per share is $4.5, the cancellation of the share eliminates $115.5 off accounting value per share from the balance sheet.

Apple’s management has made a conscious decision to put cash flows and earnings per share as the key drivers of value. Therefore, balance sheet factors aren’t as relevant. The key factors are dividends and especially buybacks.

This is the difference between making great, low risk, long-term investments and speculating. Buffett always kept Berkshire as a financial fortress, adding new businesses constantly to create growth. On the other hand, many businesses now focus solely on buybacks no matter the stock price which might jeopardize their performance somewhere down the road. To lower your investing risk, pick those that think long-term and don’t do things just to please speculators or increase short term management bonuses. Unfortunately, Apple falls within the latter group.

Apple dividend

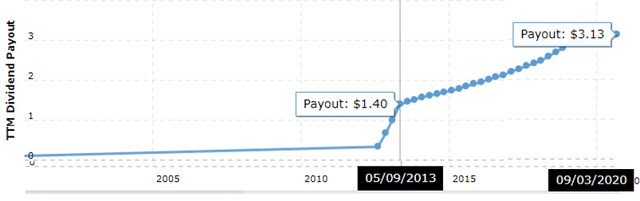

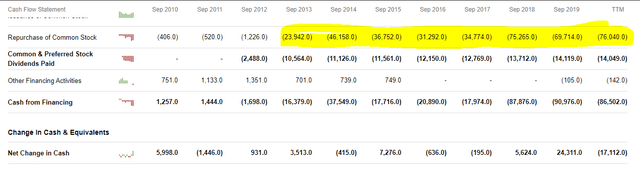

Since 2013, Apple’s cash outflows for dividends have been growing slowly. Those went from $10.5 billion to the current $14 billion.

But, the dividend per share more the doubled as it went from $0.35 per share (not adjusted for latest split in the below figure) to $0.78.

The dividend yield at current prices is 0.68% so really small and even if it continues to grow it is not a significant investing factor for Apple stock as are buybacks.

Apple buybacks

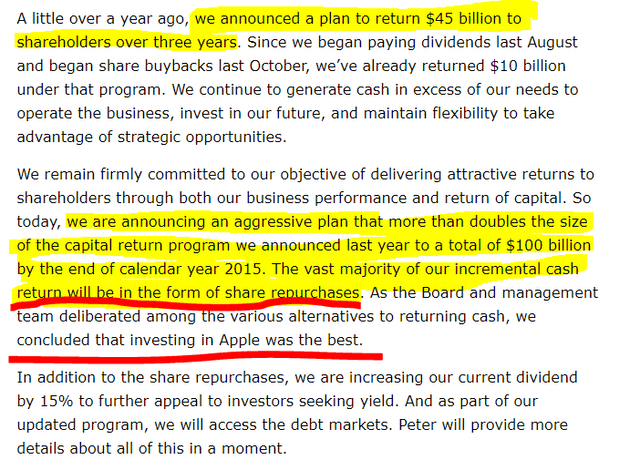

Apple’s buybacks started in 2013 when the company started to have excess cash and decided to return most of it through buybacks because they concluded: “that investing in Apple was the best”.

I completely agree with them, investing in Apple was the best, but it surely isn’t anymore. The stock price now is 8 times what it was back in 2013 while net income is just 42% higher than in 2012.

From my perspective, the value of Apple’s stock from a buyback perspective is now much lower than it was in 2013 and definitely not the best investment, even for Apple. However, the management can never say their stock is not the best because they would compromise their key goal which is a higher stock price.

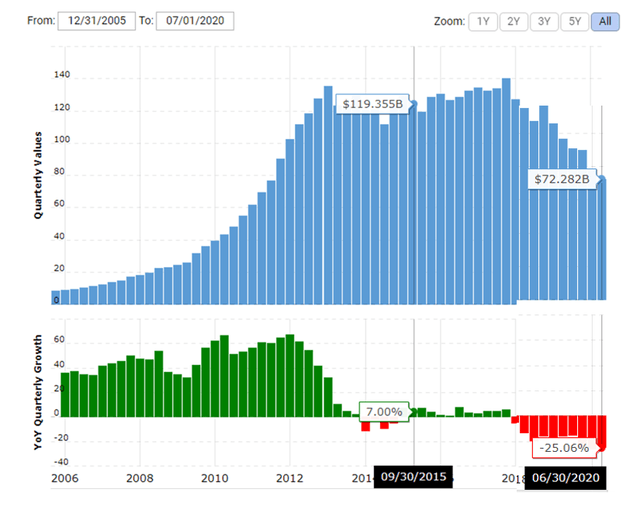

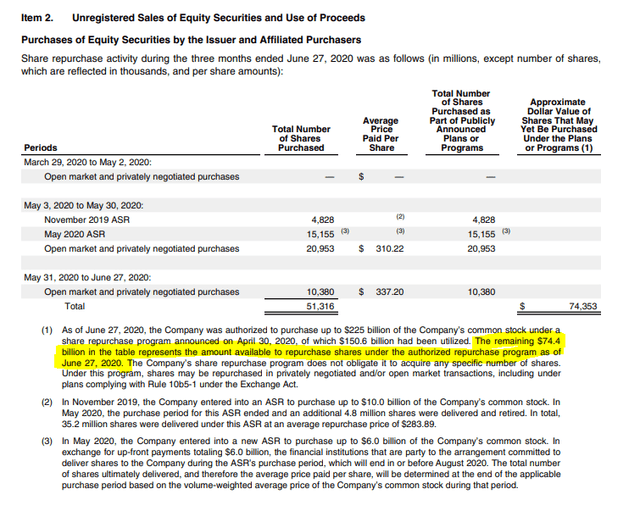

Despite the stock price being 8 times what it was, the buybacks have been significantly increased and continue to be the focus of capital allocation. There are still $75.4 billion remaining in the current $225 billion repurchase program. Apple is also doing accelerated share repurchases (ASR) where it pays an investment bank to buy stocks for them. The current ASR is $6 billion.

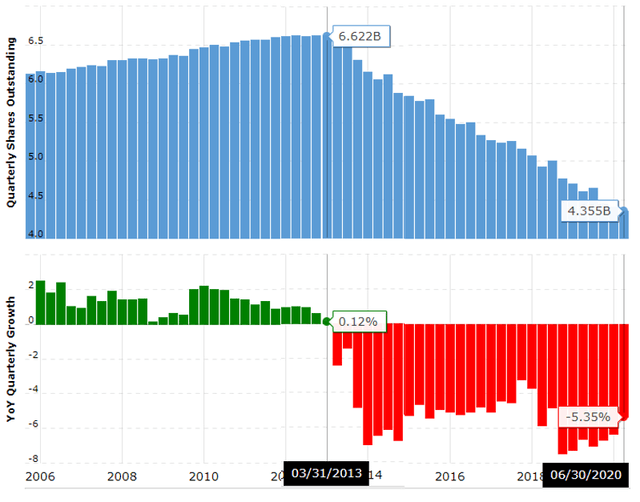

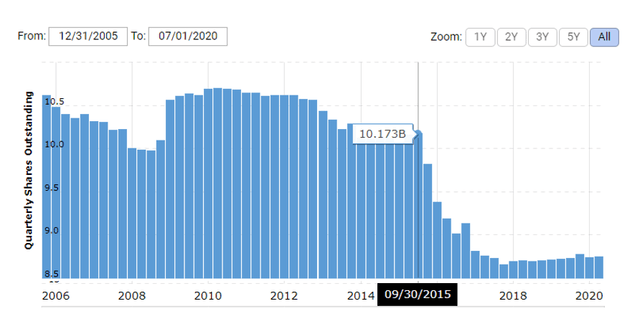

The past buybacks did deliver on expectations as the company lowered the number of shares outstanding to the current 17.1 billion from 26.48 billion, adjusted for the recent split.

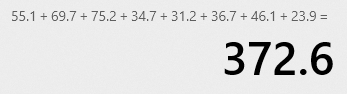

In total, Apple spent $372 billion to lower the number of shares outstanding by 35%.

That is definitely a great deal from the current market cap perspective of more than $2 trillion, but from 2013’s perspective, when the market cap was around $500 billion, they spent 75% of the market cap to buy 35% of shares.

The key with these buybacks is the following; the number of shares was lowered from 26.48 billion in 2013 to 22 billion by the end of fiscal 2016 where the company bought 4.5 billion shares for $136 billion or $30 per share. Since 2016, the Apple bought back another 5 billion shares but it spent $234 billion to do that, or $46.5 per share. Still ok, but 50% more than in the first buyback period. However, now the stock is at $120 and if the company spends all of its cash flow of $50 billion on buybacks that gives a meagre 2.5% buyback yield which is a quarter of what it would be at a $500 billion market cap.

I think that Apple’s management is high on its past buyback success because I can’t believe that they can’t find a better than 2.5% return out there at the moment in the form of an acquisition. I’ve recently discussed Intel where the market capitalization is $200 billion and the free cash flows are $20 billion. Thus, something Apple could easily take over and reach a return in the high single digits in the worst-case scenario. Not to mention the possibilities from combining the research power and market positions.

Unfortunately, I am not in Apple’s management team and I don’t get a bit more than a hundred million per year from vesting options as Tim Cook does.

If Apple’s focus isn’t on creating as much as possible of long-term value for a dollar spent, but on pushing buybacks as long as they can because things are going good with such a strategy, I think that no matter the current extreme valuation for Apple, the stock can go higher.

However, all these buybacks will cost long-term investors like pension funds and Berkshire a lot when a bad year comes, the company has lower earnings and doesn’t have the capacity to push the stock higher. This is a long-term issue and you can call me crazy for discussing it now, but a GE situation could happen to Apple too if they don’t think a bit more about the price of the buybacks they make. Unfortunately, Apple’s last statement about stock splits where they want to increase the shareholder base, shows the management is focused mostly on financial engineering for shareholder value creation.

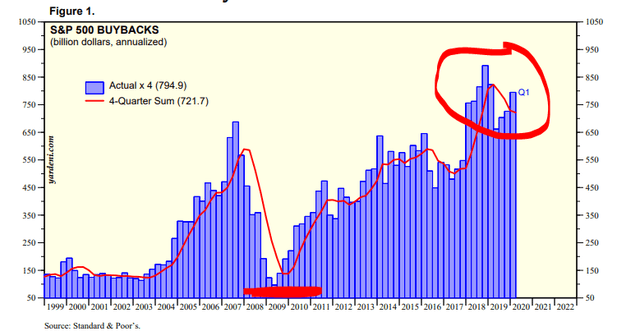

A similar approach is used by others. Now that the S&P 500 is at record highs, so are buybacks.

All business is cyclical, so at some point the liquidity for buybacks will decrease and that is a big risk both for the market and Apple.

An example of a company that did buybacks no matter the stock price is General Electric (GE). They did strong buybacks from 2015 to 2017.

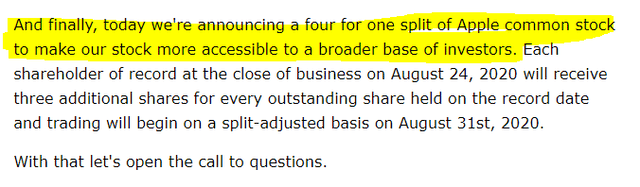

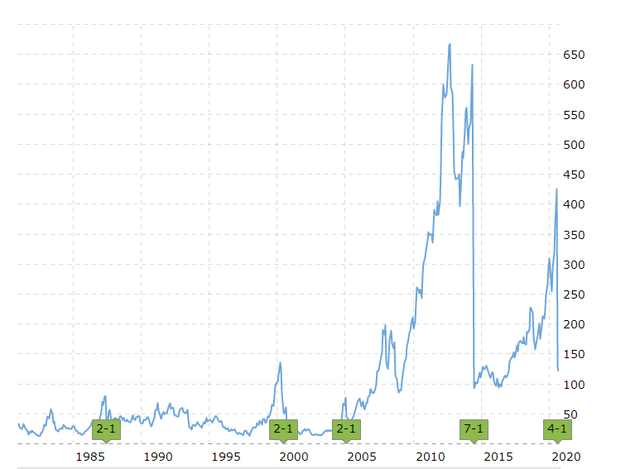

Apple stock split

When the management of the largest company in the world by market capitalization says how a stock split has been made “to make the stock more accessible to a broader base of investors” it means they are targeting all the Robinhood buyers and retail investors that don’t have more than $500 to spend on an investment.

Apple has been doing splits whenever the stock price would shoot up so the recent one shouldn’t be considered a factor at all but I’ve seen a lot of commotion about it in various investment groups so I just wanted to mention it here.

If you are an investor, focus on businesses focus on deliver value over the long-term. If you invest in businesses like Apple, that keep doing the same even if fundamentally different, make sure you move fast as the market might move for them.

Buybacks are the core of Apple’s capital allocation, splits are cosmetics, but valuations are what will determine your investing return.

Apple stock valuation

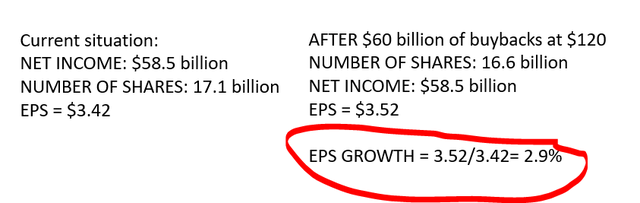

Buffett’s statement is; that investment returns are perfectly correlated to the performance of the underlying businesses. From that perspective, Apple’s earnings per share are now at $3.41 that on a stock price of $120 gives a price to earnings ratio of 35. Thus, the earnings yield is just 2.8%. EPS growth over the past 5 years has been great at 8.7% but given the expensiveness of the stock price, the buybacks will not create such a positive effect anymore.

If Apple spends $60 billion on buybacks now, it can buy back 500 million shares. Thus, by spending all its available cash flows in a year and also lowering their net cash position, they would lower the number of shares outstanding by just 2.9%. On equal net income, earnings growth due to buybacks would be 2.9%.

If net income remains equal, we can expect earnings growth of around 3% from buybacks. Net income growth was 2.1% over the past 5 years and we could assume it will be similar in the future so we could get to 5% investment returns over the long-term assuming the business remains as is.

Apple stock summary of investing risks

Now, 5% is not bad, but let me tell you this, if the market starts expecting 10% as a return from investing in good stocks, the stock might fall 50% easily and return to early 2019 levels. Thus, it might take you 20 years or more to get to your 5%.

Further, the iPhone was launched just a bit more than 10 years ago. Nobody knows what will Apple’s sales look like in 10 years. Will those sales double and will consequently net income double while buybacks push earnings per share growth even higher, or will the competition in the tech world be too much even for Apple? To find the answer to such questions we will have to wait for a decade, but this is the risk and reward of investing in Apple.

Apple stock investing forecast – long vs. short term

Despite the expensive stock and low fundamental returns, we must not forget there is $60 billion or more coming into the market to buy Apple stocks. Given Apple’s current valuation that is not what it used to be, but it might push the stock even higher over the short term. However, one day, as it is always the case, Apple will have to stop playing the buyback game, and that is a day I would not want to be an Apple shareholder.

Apple stock conclusion – it is your portfolio!

In short, the likely long-term fundamental return is 5%. The speculative return can be a positive 100% if the market is happy with a 2.5% long-term return and a negative 50% of more if the market requires a 10% return or more or if Apple’s business doesn’t grow as expected.

So, after a long article, it is actually pretty simple – the return you could expect is 5% all things equal and the speculative return is 50% up versus 50% down from current levels.

To sum up on the key investing factors using Apple’s example:

- Valuation – the driver of long-term returns – – it is funny how the market changed its sentiment regarding Apple, but a stock with a PE ratio of 37 is far riskier than one with 10, all else equal.

- Moats – those come and go – the iPhone is recent and with declining sales,

- Fundamentals – financial engineering increases risk because management focuses on stock prices and not on making financial and business fortresses!

- Buybacks – financial engineering – not smart at any price – a 10% buyback yield is much better than 3%,

- Cash flows – what really matters – – with Apple are similar to net income,

- Growth – real or engineered – hard to grow once you are big already plus the management is focusing on engineered growth, not real,

- Stocks splits – cosmetics and the larger investor base can sell very quickly based on news,

- Short-term vs. long-term – are you an investor or not? – short term the stock can go up due to buybacks and low rates, but long-term it will give 5%,

- Risk – the essence of value investing, the reward is small in comparison to other investing opportunities while the risk, that wasn’t there in 2016 has exploded – valuation is high, fundamentals are gone, growth is slow and mostly engineered, I would call it peak Apple stock.

This is what I do, I look for fundamentally good businesses to invest in like it was the case for Apple in 2016. For more info, please check my Stock Market Research Platform.