Intel Stock Analysis – Apple 2016 Déjà Vu

Intel stock analysis content

- Intel’s stock price action overview

- Intel’s business cycle and current situation in the sector – are the headwinds temporary or structural for Intel?

- Intel’s stock fundamentals – PE ratio of 10 for a tech company

- Intel stock dividend and buyback yields

- Intel stock valuation model

- Intel stock investment conclusion – investing in great businesses with tailwinds

It is a long analysis so if you prefer watching or listening, here is the Intel stock analysis video form, detailed analysis Intel stock article continues below:

Intel stock price overview

Intel Corporation – NASDAQ: INTC

Intel stock caught the eye of many investors because it is a household name and it has a very low price to earnings ratio of 10 (based on 2020 earnings guidance) alongside giving exposure to the tech growth megatrend.

Given the current investment environment of low interest rates and high valuations, you don’t encounter such situations often, especially in the tech sector. Plus, if we look at the cyclicality of Intel stock since 2018, it often went below $50, but not much below, and then it usually spiked up.

One must keep in mind this is a cyclical stock within a cyclical growth industry. As the market is myopic and always focused on the short term, it might be a great investing opportunity as the next stock spike might be like the 2017 spike where we never saw those lows again.

Intel stock vs Apple stock 2016 comparison

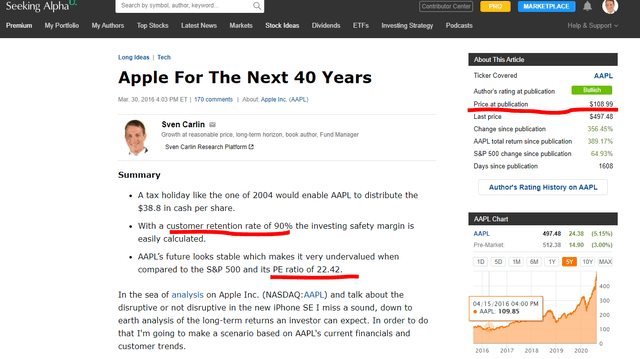

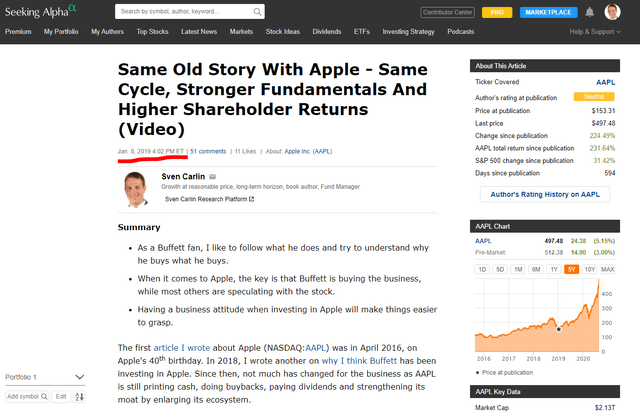

Intel stock now reminds me of Apple in 2016 when I wrote an article on how a good company like Apple that has strong cash flows, a stable customer base and is exposed to a positive structural tailwind, can’t trade at a PE ratio of 9 for long and how it was a bargain. (disclosure: I was long AAPL in 2016, sold too early but that is another topic)

Then, in January of 2019, I made a video (I didn’t have YouTube in 2016), where I explained the typical cycle that often hits Apple stock because the market and especially analysts, can’t understand and model cycles.

I discussed how Buffett was buying Apple’s business while most others were buying the stock. Having a business owner perspective on Intel will make things much easier to understand from an investing perspective.

When it comes to Intel stock, if the company can deliver on long-term growth, stable cash flows, do buybacks and pay a growing dividend to reward shareholders, it is possible the future situation might be comparable to the developments Apple shareholders enjoyed over the past 4 years.

Why is Intel stock going down?

Before investing in Intel stock, we must also understand the market’s perspective because it will give us the opportunity to spot the right time to buy. The right time to buy is usually when the bad news don’t really affect the current fundamentals and you are happy buying what is there even if the worst scenario develops.

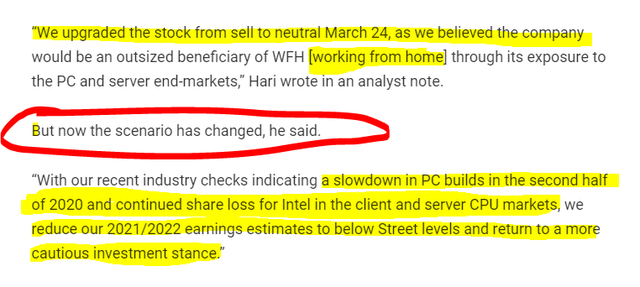

The most recent stock drop related to the Q2 earnings announcement was due to the 7nm product delay of 6 months which will give competitors more time to gain market share.

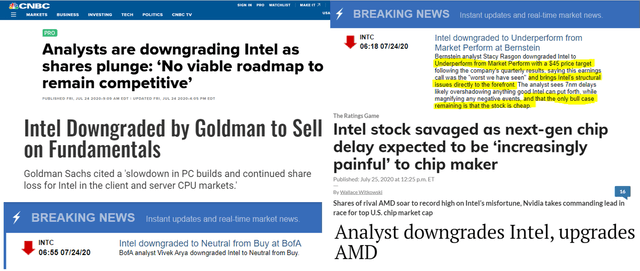

This announcement led many analysts to downgrade the stock as their models gave a lower value for the stock. Also, most of the questions during the conference call were only about the 7nm issue.

Intel stock downgrades

The thing is that you must always be very careful when listening to analysts. Their job is to model what is known and project stock values over the coming quarters. As we mentioned Apple stock earlier, when I was working for Bloomberg as a researcher in 2014, I remember how Apple was hated by analysts. Consequently, when the stock was downgraded the most was usually the best time to buy Apple stock.

Intel is in a similar situation to where Apple stock had been in the past. After the last earnings report, many analysts have rushed to downgrade Intel.

Analyst Toshiya Hari from Goldman Sachs downgraded Intel stock to sell from neutral and cut his price target to $54 from $65.

Also, on the last earnings call, Intel stock was:

CUT TO HOLD by Deutsche Bank, Roth Capital, and Bank of America.

CUT TO SELL by Northland, Bernstein, Exane, Barclays, and Raymond James.

Some analysts described Intel stock now as nothing but a cheap stock! This is because their job is to make analyses that model earnings on what is known and their price targets are usually set for the next 12 months.

If you are an investment bank with big clients, the easiest thing to sell to a client is to tell them the stock has catalysts that will push it up over the next months. So, you earn the trading commission, retain the client where you get 1% through a commission of his wealth no matter what happens. Telling them it will deliver a good 2.38% dividend yield but that the stock can also fall another 20% is a tough sell.

Intel doesn’t have any significant catalysts ahead. This makes all those short-term noise investors sell the stock, which causes a price drop because if the stock will not go up, it will most likely go down.

Dividends, earnings and buybacks are too boring factors in today’s market to even discuss because you aren’t cool if you do so. However, what pushed Apple stock from $90 to the current price? Dividends, earnings, buybacks and a low starting valuation!

The thing is that on Wall Street, the 3 years up to 2023, when Intel’s 7nm product will eventually hit the market, are an eternity and that is what Wall Street doesn’t like and doesn’t understand. But, as Seth Klarman says, a long-term perspective is the greatest advantage we value investors have!

On product delays, it is not the first time Intel had issues, it is actually normal in the sector:

- 2012 delay of 22nm Ivy Bridge

- 2013 delay of 14nm Broadwell release to 2015

- 2018 delay of 10nm production to 2019

- 2019 delayed 7nm production to 2021, now to 2022 or 2023

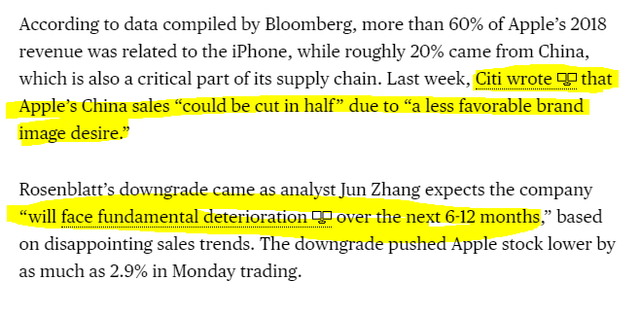

Another funny comparison with Apple. We could summarize the analysts’ opinion on Intel that the latest delay will cause a fundamental deterioration of Intel. Look what some analysts were saying about Apple in July of 2019:

This is the news, the noise, now we have to compare what is the actual value of the stock and compare it to the stock price which is a result of the noise in the short-term, not of fundamentals. As would Benjamin Graham say: “The market is a voting machine in the short term and a weighing machine in the long-term.”

The market has voted, let’s see what is the business outlook and what will be the weight of the fundamentals over the long-term.

Intel’s business cycle and current situation

Within the semiconductor industry, it is all about being first in developing and putting to market the latest chips. If you don’t do that, you miss the high margins you get before the competition comes in and you lose market share for future developments. This is what plagues Intel at the moment but we must not forget Intel is not just about the 7nm chip.

Over the past 3 years, Intel has been constantly losing the nod game with their chips but has still managed to grow revenues, earnings and cash flows.

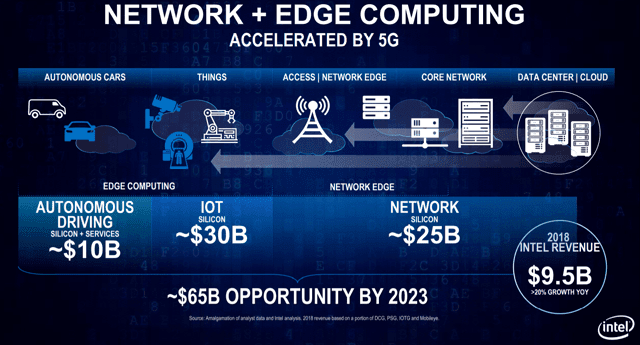

Their strategy is to lead the AI, 5G and autonomous revolution.

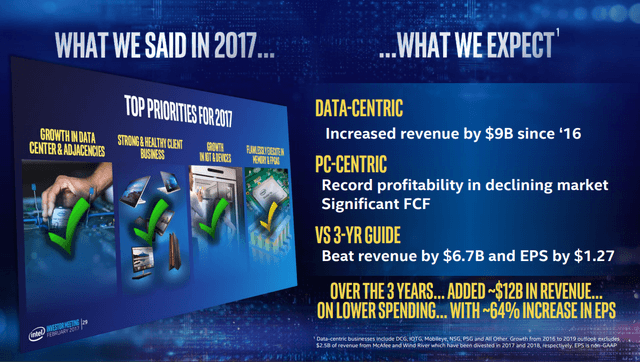

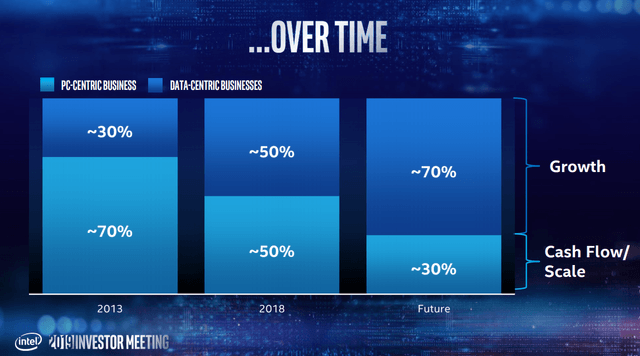

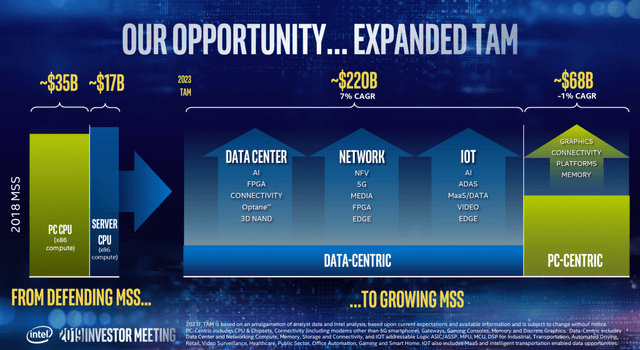

The data centric business segment is expected to be a bigger and bigger part of the company. The data centric businesses include DCF, IOTG, Mobileye, NSG, PSG and all other.

It is expected that the data centric sector will grow faster than the PC-centric business and represent a much bigger market opportunity for Intel.

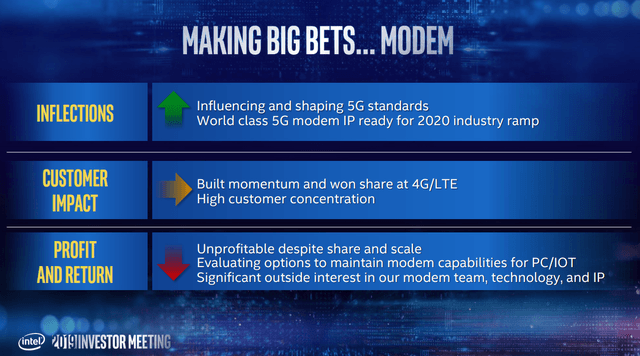

The company will make big bets on Modem:

It has good products to cater for 5G needs:

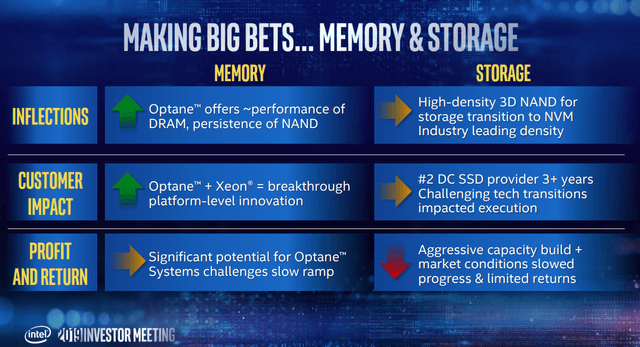

Memory and storage:

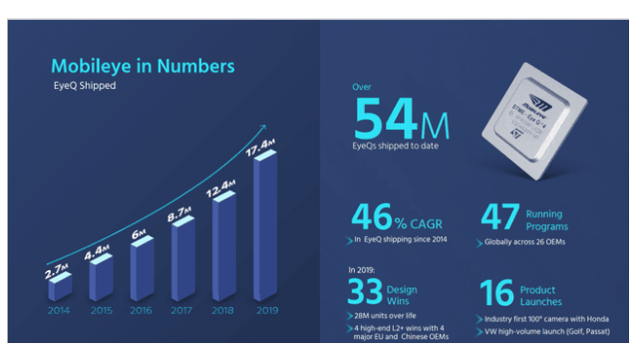

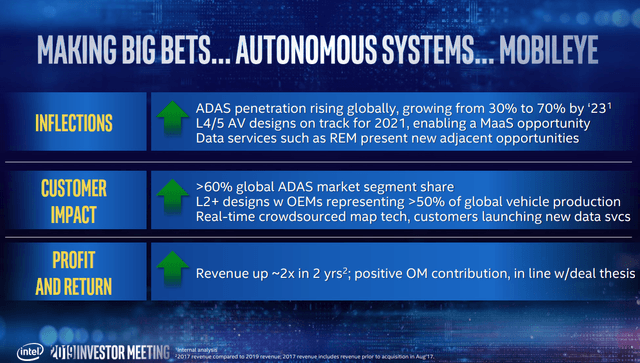

And on autonomous systems with Mobileye that has implemented cameras into 17.5 million cars in 2019.

The above and the growth rates are a big deal from a tech perspective but the market doesn’t care because it is old boring Intel.

Also, something Wall Street doesn’t see is that most of the benefits from the above data centre technologies should come over the next decade and not immediately. So, what analysts model is slow growth. Something shunned by most investors in today’s high growth environment where profitability doesn’t matter and growth is what pushes stock prices higher.

At the last conference call, Intel’s CEO, Bob Swan highlighted the following as example of where the company looks for growth acceleration ahead:

Intel is positioning itself to take advantage of what is the next stage in the internet of things.

“We’ve built scale businesses indexed to key technology inflections such as cloud, AI, 5G, and the intelligent and autonomous edge”

It is constantly adding new products in various areas.

“we launched our third-generation Intel Xeon Scalable processor Cooper Lake, which is the first mainstream server CPU bfloat16 support, which increases AI throughput by reducing the amount of data required for the same accuracy.”

Selling picks and shovels to the tech industry.

“In Q2, both our cloud and comms service provider businesses grew more than 40% year-over-year as critical cloud-delivered applications continued to scale and 5G build-outs accelerated. Leading cloud service providers, including Alibaba, Baidu, Facebook and Tencent, announced they are adopting our third-gen Intel Xeon Scalable processors into their infrastructure and services.”

My car at the moment doesn’t have any computer in it. I wonder if that will be also the case in 10 years.

“The largest opportunity we see at the edge is the $230 billion 2030 TAM for ADAS, data and mobility-as-a-service technologies.”

For now, Intel is covering ‘only’ 20% of the global automotive market.

“we were excited this week to announce a significant design win with Ford. Design wins to date in 2020 include multiple new ADAS production programs representing cumulative volume of over 20 million units.”

Their ‘old’ processors are not to be written off yet.

“The Core S and H series processors for desktop and mobile gaming deliver speeds out of the box reaching up to 5.3 gigahertz, making them the world’s fastest gaming processors, and our new 10th Gen Intel Core vPro processors delivered uncompromised productivity and hardware-based security for commercial PCs. “

Despite the increase in competition, their guidance for the full year is:

“We are now forecasting revenue of $75 billion and EPS of approximately $4.85.”

For investors that wish for stability and security, slow growth with a positive long-term outlook alongside a PE ratio of 10, Intel has all what you might need. And, as long-term investors, we must also care about what comes beyond 2023. Given the above, we might see higher growth, better margins on growing demand which means the earnings could be much higher and the valuation too.

In order to achieve the above, Intel spent more than $13 billion on R&D yearly over the past years which is 3 times more than AMD and NVIDIA put up together. Also, the company is doing acquisitions that are risky and might be questionable now, but when you invest into a high growth area, you just need a few winners to do really well.

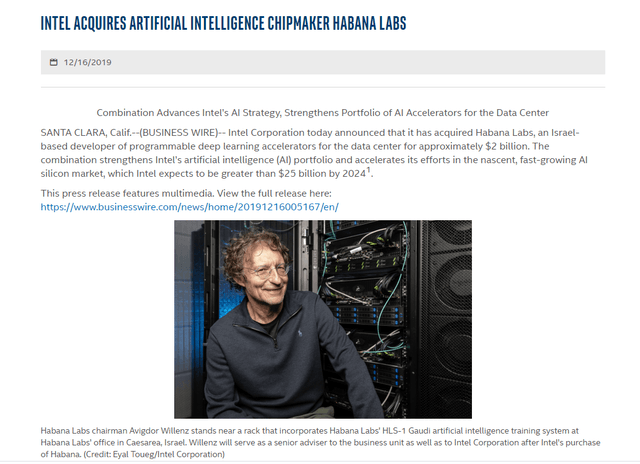

In 2017 the company acquired Mobileye and recently added Moovit to the picture with a $900 million acquisition. (more on Mobileye’s growth plans) In 2019 Intel acquired artificial intelligence Habana labs for $2 billion where it expects to cater for a $25 billion market by 2025 that can grow exponential afterward.

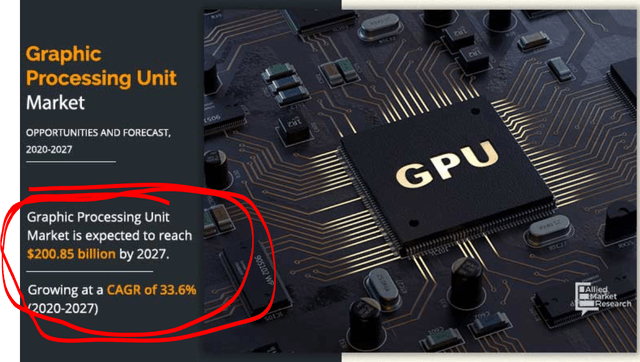

Further, there are sectors like the graphic processing units that are expected to explode over the next years and if Intel manages to get a share of those markets too, we don’t have to worry about revenues, earnings and dividends. As Intel is spending significantly more on R&D than the competition, we might get some good news down the road.

And, it is not like Intel is not already a player there. Intel has 10.21% of the steam GPU market, AMD has 14.9% and Nvidia 74.75%. Even if the market share remains at 10%, 10% of $200 billion is $20 billion in 2027.

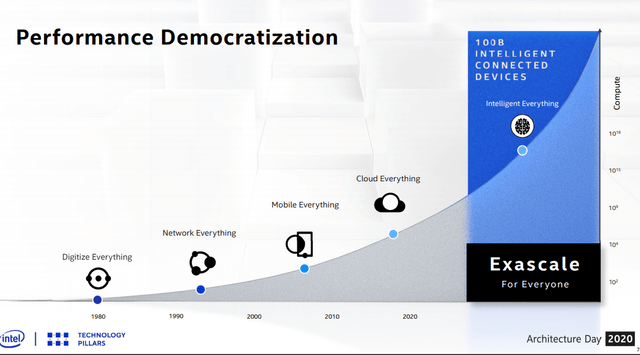

Apart from specific segments like GPU, if the world in 10 years follows the below expected development, I don’t think we will have to worry about Intel’s growth.

It is actually impossible to estimate the growth rate over the next 10 years, but it doesn’t even matter with a price to earnings ratio of 10. A PE of 10 assumes no growth, so any growth ahead is good from an investing perspective.

I would say that given the current sales, the market share in various segments and the history, Intel has and will keep having a wide moat in the field which will likely lead to a growth rate similar to the market’s growth rate.

Further and what matters most to us investors, I think I am safe to say the industry Intel operates in, is a growth industry.

According to the last quarterly information, despite all the setbacks over the last years, Intel’s business keeps growing and the company keeps shipping more and more products.

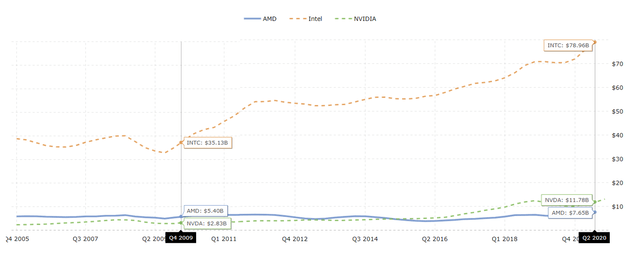

Of course, there will be competitors that will grow revenues at a faster pace, but I don’t get all the worries surrounding Intel given that Nvidia’s revenues are at 15% of Intel’s revenue and AMD’s at just 10%.

The most important investing fact here is that the faster AMD and NVDA grow, the better it will be for Intel too. Everybody is so focused on the competitive environment that they miss out this is a growth sector with strong tailwinds.

Every company will make mistakes, like AMD and NVDA did in 2015 when both companies had declining revenues. So, Intel will make mistakes too, but will also do good things based on its investments and market position.

Given the above, I believe the most important question we have to find an answer to as investors is whether Intel will grow or not over the next 10 years. If yes, then at current valuations, it will likely be a good investment.

How good will it be? That is impossible to know because it depends on factors developing in the future. My best investments over the last 20 years have been those where I would buy something because I was happy with the safe, stable and relatively certain things the investment offered. I feel intel offers stability and thanks to its product offering also a high level of certainty when it comes to future earnings. Positive developments can only bring upside.

Let’s take a look at the fundamentals and give a perspective on what could be the dividends and valuations in the future.

Intel’s stock fundamentals

When it comes to fundamentals, the fundamental value of a company, also called intrinsic value, is the sum of all the discounted cash flows created by the company from today to judgement day as would Warren Buffet define it.

To estimate future cash flows, you should know the future which is impossible, at least for me. What we have to do is to create scenarios, estimate likely outcomes and as value investors, focus on what is more certain. So, we leave any uncertain positives as a pure bonus.

Given what we discussed above, the moat in its core business and the growth coming from new businesses, I would say the most likely outlook for Intel is for it to double revenues (1 in the table below) again over the next decade. Over the past decade revenue growth has been 7% per year.

Despite the growth, gross margins (2) have been declining at a very slow pace while operating margins even improved over the last years. Net income (3) more than doubled at a growth rate of 10% per year. Earnings per share increased even more because the company has been constantly doing buybacks (7) and has lowered the number of shares outstanding by 24%. Apple has been applying a similar strategy. Dividends (5) have doubled too while the pay-out ratio remained small as the company is investing into the future and preferring buybacks.

Capital spending (9) has been growing, which is good because it keeps Intel’s moat intact in many areas. But, the free cash flows (10) are still very strong and give a free cash flow yield that is above 10% which is a remarkable in the current market environment.

If Intel continues to produce cash flows close to $20 billion per year alongside 7% to 10% growth, you will not have to think worry much about your investment in Intel over the next 10 years.

Intel stock dividend and buyback yields

On top of the above, Intel recently announced that it will accelerate its stock buyback plan and I would expect to see other announcements when the current plan is completed. Such a statement shows Intel’s dedication to rewarding shareholders which is an extremely important factor, especially when the stock is cheap. Most companies increase buybacks when the stock is expensive and thing are going good and don’t do them when the stock is cheap due to headwinds.

A $20 billion repurchase plan gives an implied buyback yield of 9%. According to the latest financial report, on June 27th, the number of shares outstanding has already been 100 million lower than the above reported number by Morningstar.

Let’s imagine Intel spends $10 billion on buybacks per year over the next 10 years. This means it would buy back half of the number of shares currently outstanding at current prices. Even if earnings remain flat by 2030, earnings per share would double. Consequently, I don’t think the stock would keep trading at below $50 where the PE ratio would be at 5.

Just the buyback activity is likely to bring 100% growth to Intel’s earnings per share over the coming decade. If revenues grow another 7% per year, you already have a 15% yearly investment return as earnings would be likely to quadruple by 2030.

On top of revenue growth and buybacks, you also have a dividend.

Intel dividend

Intel’s dividend is also important, has been doubled over the past decade and will likely continue to be increased as the business grows.

The dividend yield of 2.68% ads to the above double-digit yearly return. Plus, it is also likely the dividend will grow over time and further increase returns.

Intel balance sheet

A look at the balance sheet shows how Intel’s debt went up over the last quarters but that is just as the company is taking advantage of the high liquidity on the markets and low interest rates. Total long-term debt (3 below) is $36 billion which is less than two years of free cash flows. So, not a major concern. Plus, short term assets (2) are twice the current liabilities which also indicates strength.

Let’s put the above into a valuation model so that you can make an investment decision.

Intel stock valuation model

A conservative value investing thesis would one where Intel doubles its revenues over the next 10 years and increases earnings by 150% over the same period thanks to buybacks while the dividend keeps slowly growing and increases 100%. Given the investments in growth through R&D and acquisitions, we can estimate the same from 2030 onward. Earnings growth of 150% over 10 years implies a 9.5% growth rate.

If the valuation doesn’t change, which I find unlikely if the company keeps growing, doing buybacks and interest rates remain so low, the returns investors can expect are in line with the earnings growth rate plus the dividend yield. We are already at 13.15% on a yearly basis.

Intel stock valuation model with a price to earnings ratio of 10 in 2030 on a 9.5% yearly earnings growth rate.

If in 2030 the market recognizes Intel as a quality growth company and the stock starts trading with a PE ratio of 15, the yearly return would be a staggering 17.7%.

Intel stock valuation model with a price to earnings ratio of 15 in 2030 on a 9.5% yearly earnings growth rate.

If Intel reaches a PE ratio of 20 in 2030 thanks to all the growth areas it is exposed to, the stock price could reach $268 for a yearly investment return of 21.8%.

Intel stock valuation model with a price to earnings ratio of 20 in 2030 on a 9.5% yearly earnings growth rate.

If I increase Intel’s PE ratio to 37.5, the current PE ratio for Apple, the returns become incredible.

Intel stock valuation model with a price to earnings ratio of 37.5 in 2030 on a 9.5% yearly earnings growth rate.

If Intel’s valuation changes for the positive sooner, then the stock could reward shareholders with good capital gains and even higher returns in a shorter period of time. However, if the news keeps to be bad and disliked by analysts, I would not be surprised to see a lower price to earnings ratio of 8 or even 7. This is the risk and reward of investing in Intel at the moment.

Now, when I find a business that offers such good returns, I always wonder what am I missing. Charlie Munger says that an investor can expect returns in line with the return on invested capital the business can deliver.

Intel’s returns on invested capital have constantly been in the double digit area and often above 20%. If the company can continue to keep returns on invested capital in the double digits over time, that is likely to be our investment return too.

Intel stock investment conclusion – investing in great businesses with tailwinds

The numbers we ran above look really good, Intel’s business looks good and the company has been around for a while, so it has proven itself. Yes, the growth is likely to be slow ahead, definitely not linear (something Wall Street hates) and there are no immediate catalysts expected in the form of great news. So, as one analyst said: the only reason to invest in Intel is because it is cheap.

I would say that is a great reason to invest in something, especially when it is very likely there will be many positive catalysts from 2023 to 2030 as most of the sectors Intel is investing in boom. Thus, a great business at a fair price.

On the risk side, losing market share to AMD, having lower cash flows in 2021 and 2022, alongside high investments in acquisitions and R&D and consequently lower earnings, might put even more pressure on the stock and push it down to $40, perhaps even to the thirties for a while. That could easily happen if more bad news comes out and we already described how the market is a voting machine in the short-term. If you invest in Intel stock, be ready to wait a while for your returns, but given the quality of the company, the long-term outlook, the buybacks, I think it is a worthwhile wait.

My action and portfolio strategy

I’ll start with a 7% portfolio exposure. The above discussed possible returns fit my required investment returns and the buyback activity might create a support for the stock.

If there is more bad news in the form of noise but the fundamentals remain strong and the long-term outlook positive, I will be ready to make Intel a core position within my portfolio and take even more advantage of the market’s irrationality and short-term focus.

Over time, I’ll follow Intel closely, update after earnings and compare Intel’s likely returns with other investment options I have. If you wish to have me update you on Intel and the other stocks I follow, you can check my Stock Market Research Platform where you get the summaries of what I do for less than $1 a day.

If you would like to be notified when I publish an analysis, please subscribe to my newsletter: