YY Stock Analysis – Value Vs. Fraud

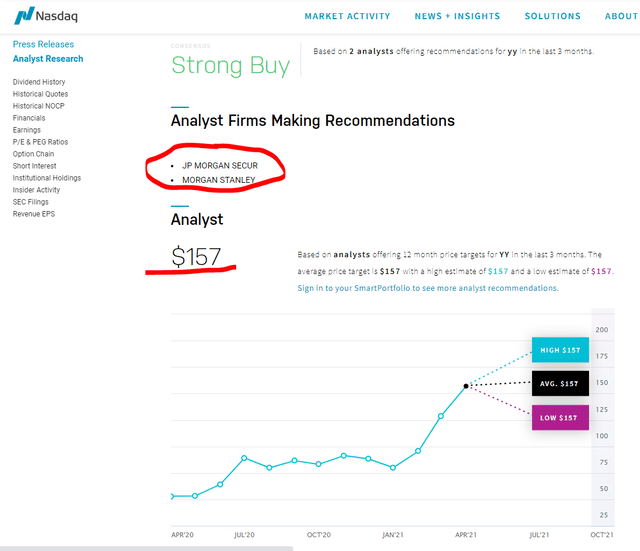

YY stock representing JOYY Inc traded on the Nasdaq: YY, is a Chinese company in the online streaming business. When it comes to investing in YY, most investment bank analysts have it is as a strong buy based on its high cash position and fast growing live streaming apps like Bigo Live and Likee.

On the other hand, Muddy Waters recently published a short report on YY stating how 90% of the company’s numbers are fake. However, Muddy’s report focused on YY’s Chinese business and not on the current business.

I have made an investigation into Bigo Live and found many inconsistencies so I would agree with Muddy on YY and say how the numbers represented in financial statements and Google play rankings could be fabricated. This means investing into YY stock is very risky and not a value investment at all.

This YY stock analysis will look at both sides so that you can make up your mind. We will start with a stock price overview, business discussion, a fundamental analysis, sum of parts valuation and conclude with the risk and reward investment thesis.

YY Stock Price Overview

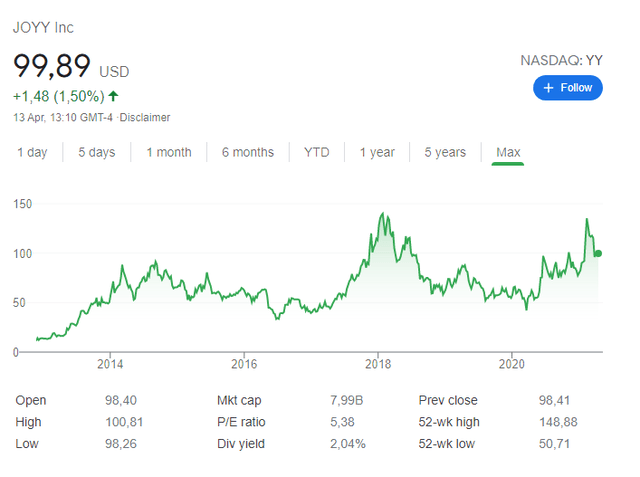

YY’s stock is one of the Chinese companies that rewarded shareholders well since its IPO in 2021. However, there have been some significant ups and down and currently YY is in another downturn. Part of the recent decline can be explained by the recent Archegos margin call sell-off that I explained in this video, while the upside since the bottom of March 2020 was thanks to the company selling its Chinese business YY Live to Baidu for $3.6 billion. (Baidu Stock Analysis – another strong buy according to most Asian fund managers).

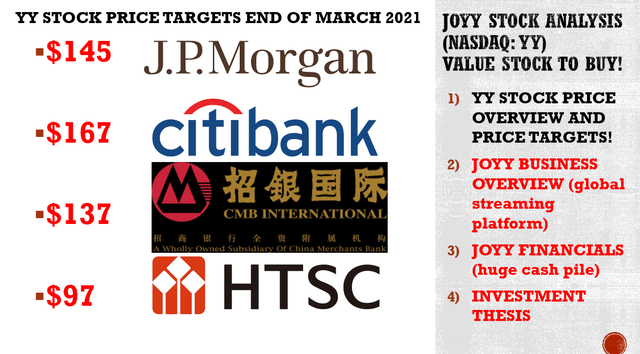

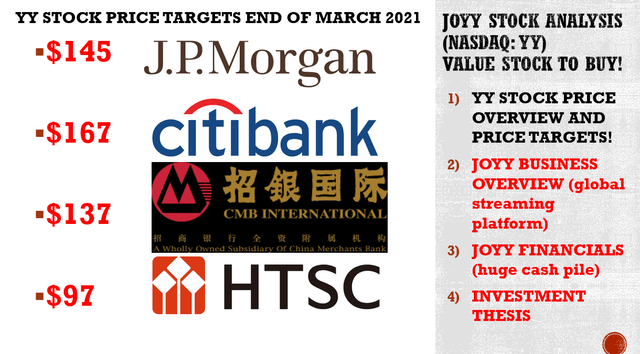

I have summarized below analysts’ YY stock price targets as of the end of Q1 2021 and I just have to add Deutsche with $134 and Morgan Stanley with $169. The main differences in valuations and price targets come from the different price to sales ratios applied to the remaining global live streaming business.

Price targets are one, but let’s first discuss the business.

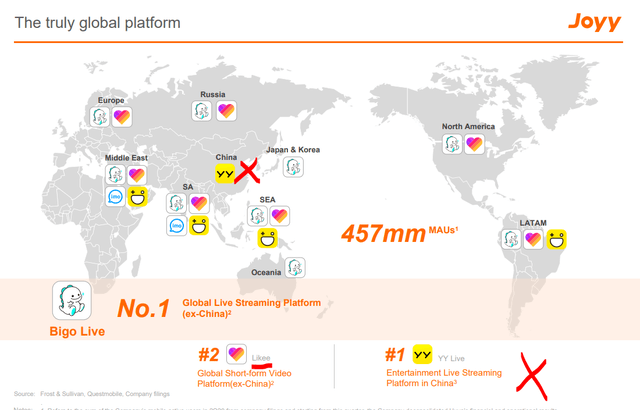

YY Stock Analysis – JOYY Business Overview – Bigo Live and Likee

JOYY is now a global streaming platform and not a Chinese one anymore as YY China has been sold to Baidu.

JOYY stock analysis – Source: JOYY Investor relations

The two key platforms going forward are Bigo Live and Likee.

BIGO Live is a gaming/entertainment live stream platform.

Average mobile MAUs of Likee are at 120.1 million according to what the company says.

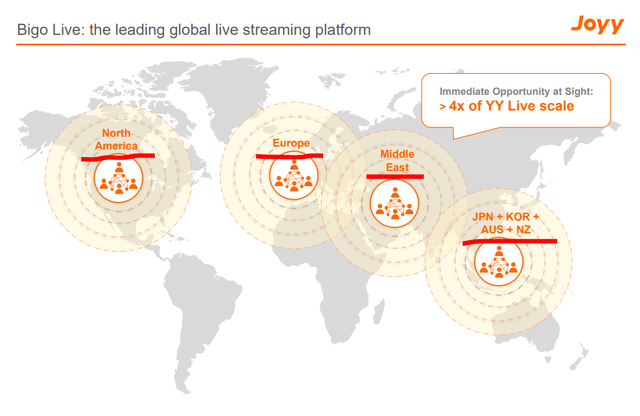

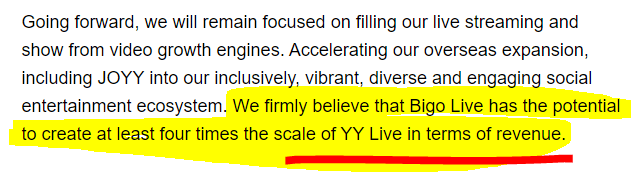

Their target is to achieve 4 times the scale they had with YY trough Bigo Live by expanding in North America, Europe, South East Asia and the Middle East.

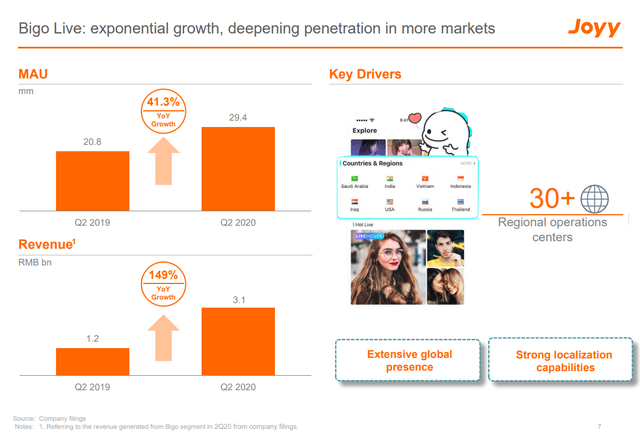

Bigo Live is what they call their ‘growth platform’ but the number of users isn’t staggering at 29.4 million in Q2 2020 and according to the last earnings (Q4 2020), actually declining to 28.7 million. This means that after the Covid-19 boom, the growth is not ‘exponential’ anymore and not even growth.

The average mobile MAUs of Hago decreased by 49.9% to 16.5 million from 33.0 million in the corresponding period of 2019 primarily due to the impact of the Indian government’s measures to block Chinese-owned apps in its local market.

As they sold YY Live, they are now going global and thus competing with Facebook, TikTok, YouTube and other platforms. The main question I focus on as an investor are related to the differentiating factors and moats.

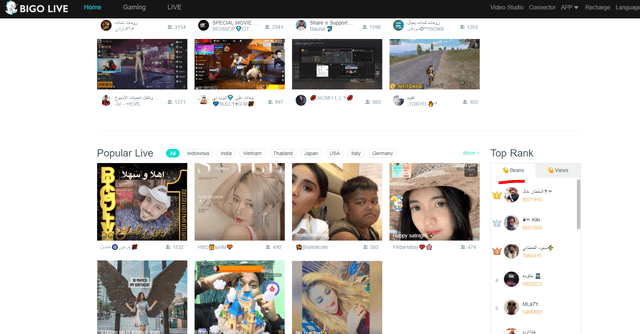

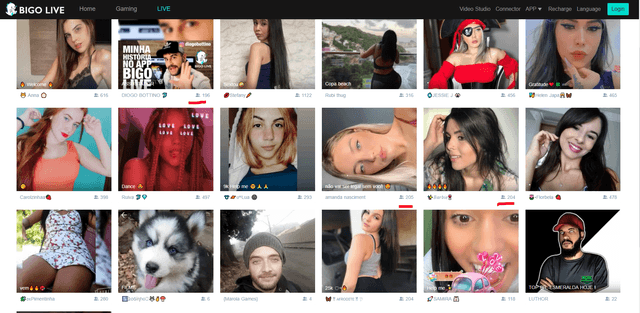

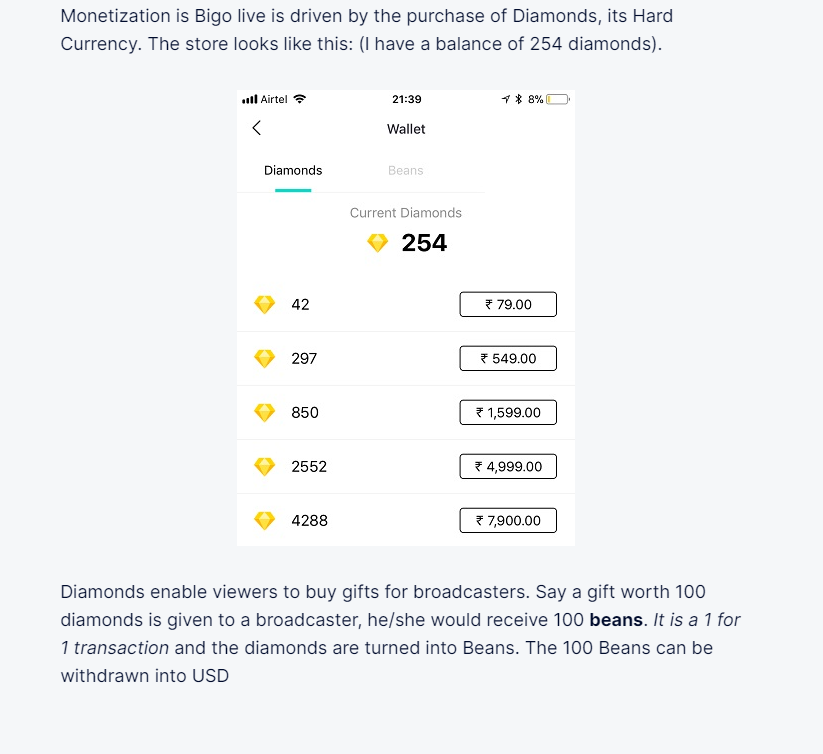

From a web search perspective Bigo seems like a gaming interactive platform and a dubious platform for girls collecting beans which is the currency broadcasters get paid with.

The live entertaining part of Bigo.

Of course, scantily clad girls will always attract a public, but if you look at the average number of views, the views and the number of performers area actually low and lower than 1,000.

Likee seems to be competing with Instagram or TikTok.

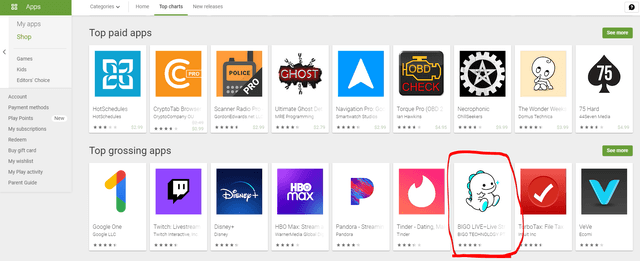

What is positive about Bigo is its ranking on the Google Play. Bigo Live is the 7th global grossing app.

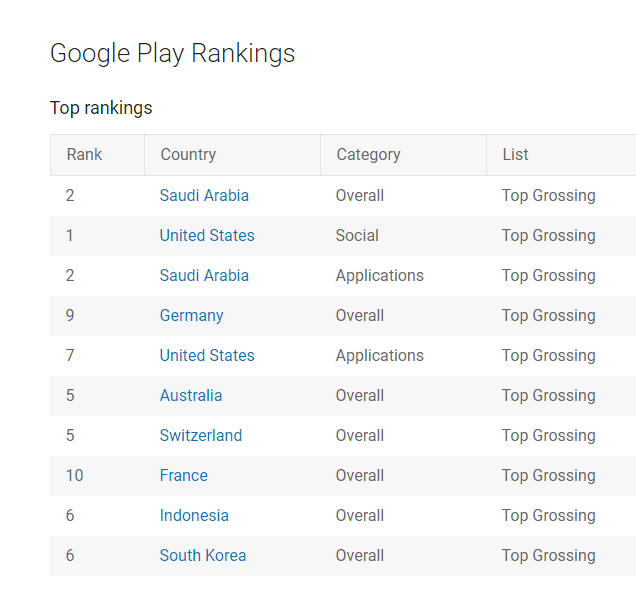

Also, the company’s market reach seems working as if I just look globally, Bigo Live is the top grossing app in the US, second in Saudi Arabia, fifth in Australia and tenth in France.

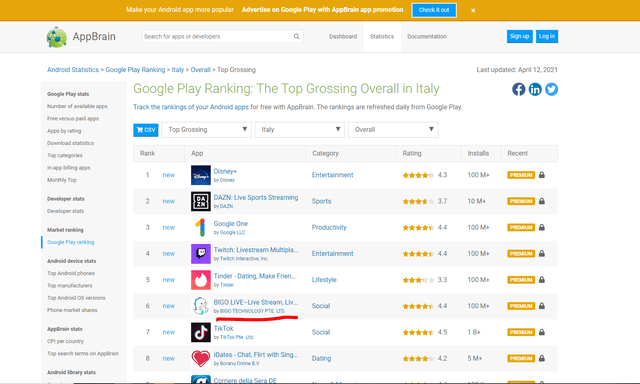

App Brain has Bigo as the sixth grossing app in Italy too.

The app Likee has more than 500 million downloads on Google and more than 10 million very positive reviews.

The company also reported Likee has more than 140 million active monthly users at the end of 2020.

So, it looks all great, the cash is coming, the apps are growing fast and therefore thanks to that the stock should be a bargain.

YY stock likely fraud perspective

I wanted to see whether the numbers showed by the company and on Google ranking are correct or perhaps manipulated. My findings indicate that a lot of the numbers above are fabricated in one way or another. I am not saying it is fraud because you are allowed to use bots to entice real users to more engagement, but it is a shady practice and it should actually be banned. Using advertising to rank better on Google is also something not illegal, but investors should know about the source of the growth. From an investing perspective, the business model is not sustainable and actually worthless. Let’s start with the real look at YY.

1) Nobody knows about Bigo in the US or Europe but the app is the top grossing app? Something is wrong there.

I have made an introductory video discussing YY and shared the bullish thesis the investment banks analysis have while also discussing the bearish thesis from Muddy Waters. I have asked my viewers to comment or send me insights into the business and their knowledge about it.

The video was published on Sunday 11th of April 2021 and by the time of writing this, the 13th of April, the video had 17,000 views and 520 comments.

Of those comments, none from US or Italian users ever heard of Bigo or Likee. Here is just one example. You can check the comments in my video for yourself, nobody from the US or Europe had anyone that knows the app.

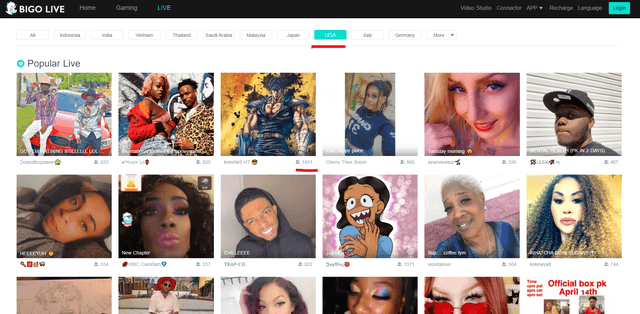

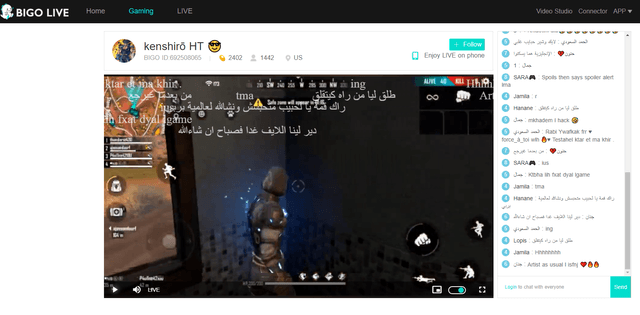

Further, I went onto the Bigo Live site for the US and found the following:

On Bigo Live USA there was a total of 24 broadcasters that a number of viewers between 100 and 1,500 and only Kenshiro had more than 1,000 views. Further, when I checked Kenshiro’s channel, none of the language was English.

So, for Bigo TV, I am looking at the sixth top grossing app in the US, but the total number of live views streamers allegedly in the US have around 15:00 Eastern Time is less than 24,000. Plus, the top US streamer is not from the US and most of the comments are in a writing I don’t understand.

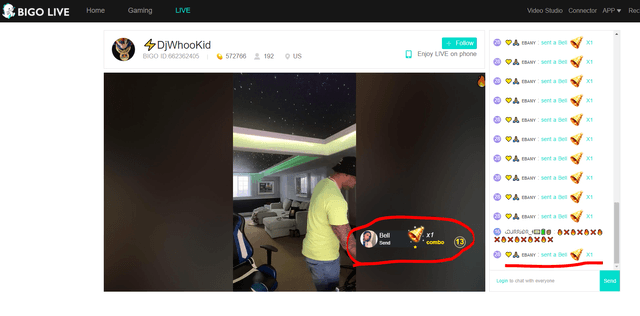

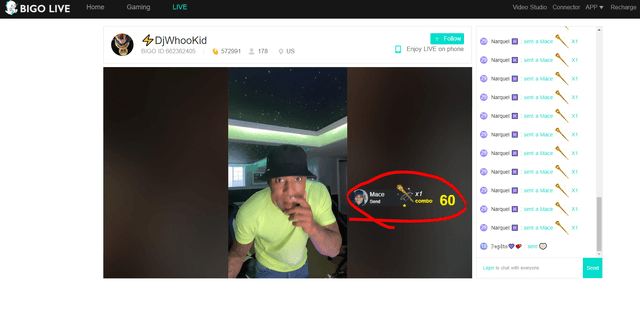

Then I checked DJWooKid and with just 192 live viewers, in the 15 seconds I managed to force myself to do research on what is going on with DJWooKid, he got a ton of comments and a ton of gifts from various people. The amount of beans (currency withing Bigo) he received was just going up and up while I was watching.

Just 30 seconds later, more gifts and the number of beans received automatically increased at staggering speed.

After looking at the above, and I urge you to test it yourself if you don’t trust me, my assumption is that most of the traffic is fabricated through bots in a push to make the app popular globally. Thus, as it is common with apps that have gifting incorporated, the app itself creates gifts to incentivize real viewers, if there are any, to gift. If the company counts these fake gifts or the gifts that performers have to give to other performers thanks to their contracts, the also the financials are fabricated and Muddy Waters is correct. I suggest you spend 15 minutes on your country’s Bigo, I am sure you will agree with Muddy Waters on the value of Bigo’s business.

Thus, I would argue that Bigo Live’s top grossing position on Google play is mostly fabricated by bots creating fake revenues. I cannot figure how can a live app with maybe 20,000 live views, of which we don’t know the share of real views, with terrible content, be among the top grossing apps in the US.

I checked the same for Italy, nobody of my Italian viewers ever heard of it but the app is the 6th grossing in Italy.

I have checked Bigo Live for Italy at 21:30 CET, which is prime time in Italy, and the situation is even worse than in the US. The number of channels live was similar, 24, but the maximum number of views for a channel was 366.

I checked the performer with the maximum number of live views and he was even interrupted by his grandmother while streaming. A little bit later, he and other performers were discussing how many gifts they gave to each other and whether they have reached their targets. The most ridiculous conversation I ever listened to but it showed me how the grossing data for Bigo is likely fabricated through a gifting loop broadcasters must adhere too.

From my research it seems that anyone who is live on Bigo gets a lot of gifts, which means it is all through bots or the company is actually paying people to be live. Secondly, I haven’t seen the contracts, but it seems performers are forced to pay others to create a circle of payments that is likely what makes Bigo a top grossing app. I have found here a good article discussing how the Bigo financial ecosystem works.

Broadcasters then can use again the currency to purchase vip status and further increase Bigo’s revenues.

The following picture summarized Bigo’s initial loop that allows it to be the top grossing app.

Apart from the above way of inflating grossing revenues, the next step is advertising in order to reach a high Google download ranking.

2) Bigo is pumping numbers by paid social advertisement in cheap advertising countries

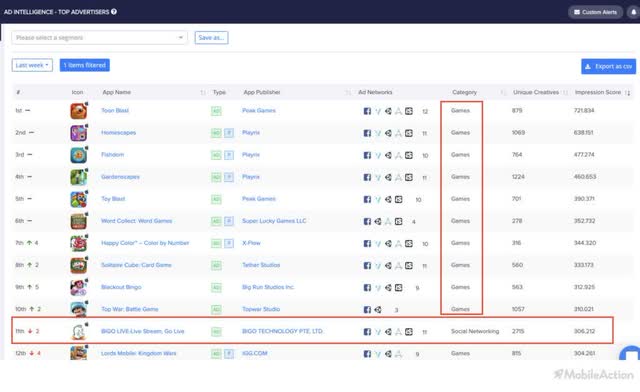

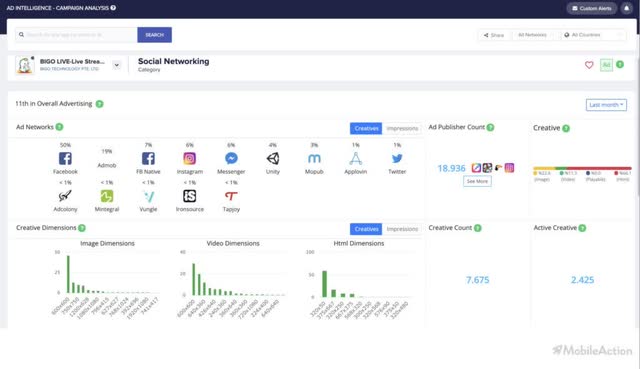

According to Mobile Action, Bigo is among the top advertisers in the world. The revenue loop explains the grossing rankings the advertising explains the download rankings. The usage here doesn’t really matter as long as numbers can be fabricated.

Bigo is spending money to advertise on 19,000 apps. Given the terrible quality of the app and content, they will have to constantly spend more on advertising to keep their numbers and rankings up. Not something sustainable at all in my opinion.

The only geography that I have had more than one viewer say they heard about Bigo was Saudi Arabia but they said they heard about it only through advertising.

The key here is that in Saudi Arabia Bigo grows through advertising. If the advertising stops, it is likely the app will simply disappear because it can’t compete with real apps like TikTok, Facebook, Twitch.

I have checked Saudi Arabia and the number of channels is 10 times the number in Italy or the US, but the number of live viewers is very low, approximately 100 per channel. What is interesting is that the views are distributed unanimously across channels which is something I find very hard to believe is real.

All the channels that you check, constantly receive gifts from various people, even if the number of people watching is low.

After spending half an hour looking at Bigo TV, I am concluding it is impossible this is an app that would genuinely rank anywhere on Google. The content is terrible, the traffic is likely created by bots and the company is probably financing it all.

3) I haven’t found a clear contract with Bigo available online for broadcasters

I have found one video on YT explaining how to be successful on Bigo and it says how you need to have an agency that pays you if you want to properly work for Bigo. So, Bigo is financing the agencies that consequently finance the performers, by setting an intermediary in between, Bigo isn’t related to what is going on.

How to be successful on BIGO TV.

If you go look at the reviews of the app, you will find some patterns (praise, issue, praise) within them which again suggest even the reviews are written by bots or paid by agencies.

Likee reviews – Source: Google

Applyzer shows where Bigo is most popular with downloaded apps too, but it is so in countries like Cambodia, Vietnam, Nigeria, Algeria, Pakistan, Malaysia et.

Bigo appl ranking – Source: Applyzer

The thing is that advertising on social media in the above countries is extremely cheap and you can get a lot of downloads. The downloads lead to a high ranking on google which makes good numbers, the sponsored or fake traffic adds to it and analysts that likely never checked the app, are excited which leads to high stock price targets. This is how a scam is made in these days, nothing illegal but, all you need to do to believe it is not creating value for shareholders is to check the app and the live performances on Bigo.

When starting to look at the YY stock investment thesis I have also summarized the financials and sum of parts valuations that the investment banks analysts made alongside Muddy’s report. You can find that below but my conclusion is that the value of YY, is likely to be the net cash you are going to receive through dividends when they get the money from Baidu and that is it. We will see how much will that be, but certainly not $8 billion, so the most likely outcome for YY stock is that it is going down. Of course, if bots aren’t the ones inflating the price too.

Before considering YY stock, please check the Bigo app so that when the stock crashes you don’t ask yourself ‘why why’ have you invested in YY stock.

JOYY stock analysis – financials

JOYY has a lot of cash on the balance sheet which makes it a value investment with 23.5 billion RMB or $3.69 billion in cash.

JOYY stock analysis – cash position – Source: 2020 Earnings report

However, most of the cash there emerged after share issuances and other financial transactions as Tencent exercised its options to buy Huya.

In 2019, compared to 2018, short term deposits and short term investments increased by 14 billion RMB. Goodwill increased by 13 billion RMB while total liabilities increased by 9.5 billion RMB.

Additional paid in capital increased by almost 11 billion RMB while the net increase of earnings was 3 billion RMB.

Source: 2019 20-F

Therefore, the cash is likely there somewhere but not created through business operations, just financial operations which is a minus when analysing the sustainability of the live streaming business model.

However, JOYY just sold YY Live and $3.7 billion in cash is expected to arrive from the sale of YY Live, pushing JOYY’s cash position is to $7.4 billion.

The company is also seeing positive operating cash flows but not positive free cash flows and the theory is that as the remaining platforms are still in the growth phase, net profits are logically negative.

From the above operating cash flow, I have to deduct YY Live operating cash flows. As YY’s cash flows in 2020 were 3 billion RMB, we could conclude other remaining platforms have 1.5 billion RMB in operating cash flows or $229 million. That is if the accounting is proper.

If Baidu paid $3.7 billion for 3.09 billion RMB ($474.1 million) in operating cash flows, the operating cash flow valuation for such a business is 7.8. Thus, the remaining $229 million in operating cash flows for JOYY could be valued at $1.78 billion from that perspective. However, given the countries the company is operating in, I would attach a much lower valuation and given the above business overview I made, I actually give it a valuation of zero.

Further, yes Bigo has seen growing revenues but also growing costs in line with revenue growth. Not something I would call scalable and we have seen how paying terrible performers to perform is something I don’t think will ever be profitable.

The remaining businesses are not profitable and depend on further monetization. This represents a risk because what often happens with the high-flying apps is that as soon as you try to monetize, you start losing members as we have seen above with JOYY’s apps in the past.

Going forward they expect fast growth and the even declared a dividend.

YY stock analysis – conference call and short selling reports

Whenever I look at a business, I always like to look at the conference calls, you get a better feeling of the numbers and the analysts usually ask the questions that emphasize the key risks and developments.

As usual, the management is banking on the growth potential with Bigo, promising 4 times the scale of YY Live in terms of revenue.

JOYY Q4 2020 conference call

Likee just started monetization and they expect good things, but discussing the moat or differentiating factor compared to others, they mention they content creators and user interaction.

JOYY Q4 2020 conference call

We will see how will this develop over time, it is a risk but if things develop well and Bigo reaches 4 times the scale of YY Live, you can then expect 4 times the value, thus around $14 billion. But I feel the ‘IF’ there is pretty big!

I have looked at app and search numbers, I see no growth and actually JOYY’s apps are not in the top positions. According to Applyzer, Bigo’s top position is in Cambodia and Vietnam, where it is still the number 6 on the social networking app ranking. Globally it is well spread but no position in the top 5.

Bigo appl ranking – Source: Applyzer

By taking a look at Google trends, there has been some increased search activity during lockdowns, but the trend is actually declining for Bigo. Countries with the highest search volume are Indonesia, Cambodia and Malaysia.

Search trends for ‘bigo’ – Source: Google Trends

Similarly, the situation doesn’t look much better for Livee.search trends have been declining and top countries are Nigeria, Kenya and Pakistan. I don’t think that will be easy to monetize and make profitable long-term. Plus, given you are not the top app, people will likely easily switch to something else.

Search term ‘livee’ trend – Source: Google trends

Competition is tough, and actually even Bigo on its own page where it discusses how to make money on Bigo, has a YouTube video explaining it.

How to make money on Bigo, – Source: Bigo

So, the remaining apps might not be that valuable but the cash most likely is, or isn’t it?

JOYY $7.4 billion cash pile

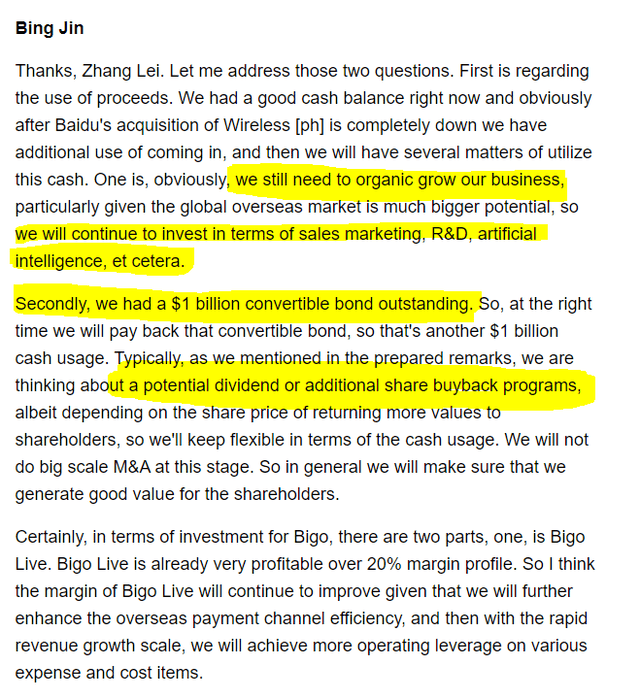

There has been more clarity on what their plans are with the cash during the most recent conference call; they will repay the $1 billion convertible note, invest in organic growth and pay a special dividend or do buybacks.

JOYY Q4 2020 conference call

Thus, if I deduct $1 billion to repay the convertible note, then another billion for organic growth investing, another billion for the 25% tax rate among other things, and the net cash position should be $4.4 billion leaving $4 billion of free space to arrive to the current market capitalization of $8.26 billion.

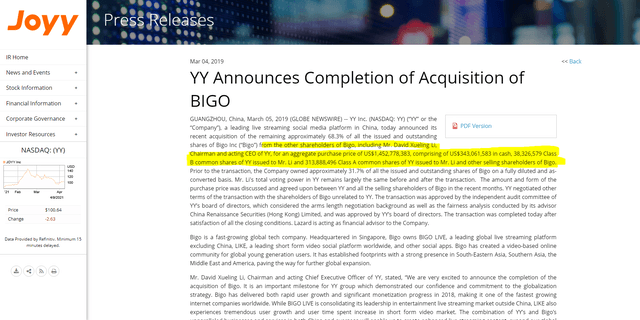

I would also be very careful when using the available cash at face value. In 2019 JOYY used its cash to acquire BIGO, where the founder and owner was of course JOYY’s chairman. JOYY paid $1.5 billion where Mr.Li got part of the $343 million in cash payment.

JOYY’s BIGO acquisition – Source: JOYY Investor relations

These transactions are terrible because when the CEO has various stakes in different related businesses, you never know whether his focus is to create value for himself or for other shareholders. This creates another significant risk when it comes to investing in YY stock. Yes, if the cash is fairly distributed to investors, and if the management’s predictions about Bigo are correct, the stock deserves to hit the mentioned price targets, but if not, it can get really ugly. Let’s first make a sum of parts valuation and then, speaking of ugly, Muddy Waters recently called the company a total fraud.

YY stock sum of parts valuation

The available cash is $4.4 billion. There is also a 31% stake in Huya (NYSE: HUYA) where we should get another billion.

Huya stock price

Thus, the remainder is valued at $3 billion which could be a fair valuation for the apps and would be at a price to sales ratio of 1.5. Interesting, but not a bargain. The remaining part of JOYY is really hard to value as it is so differentiated across the globe, competes with much more powerful entities and is actually not profitable. I don’t think the monetization process is comparable with YY Live because of the competition (Facebook and others are not allowed in China).

If Bigo and Livee decline in popularity as the company tries to monetize them more, there goes your $3 billion in value. Thus, the situation can get ugly for investors, and according to Muddy Waters, it is all a fraud.

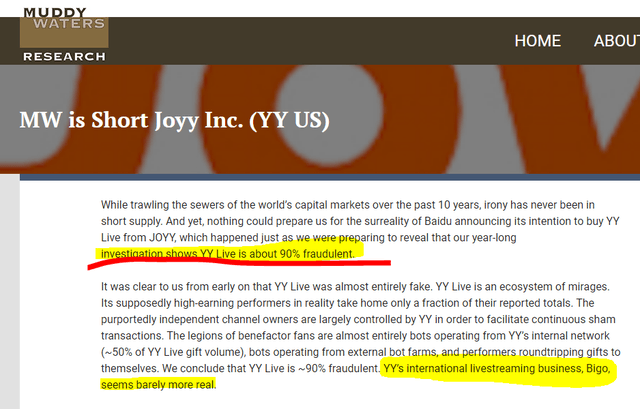

JOYY stock analysis – Muddy Waters report

Just after the Q3 2020 earnings, Muddy Waters published its short report on JOYY stating how 90% of YY Live is fraudulent and how Bigo isn’t much better.

JOYY stock analysis – Muddy Waters Report

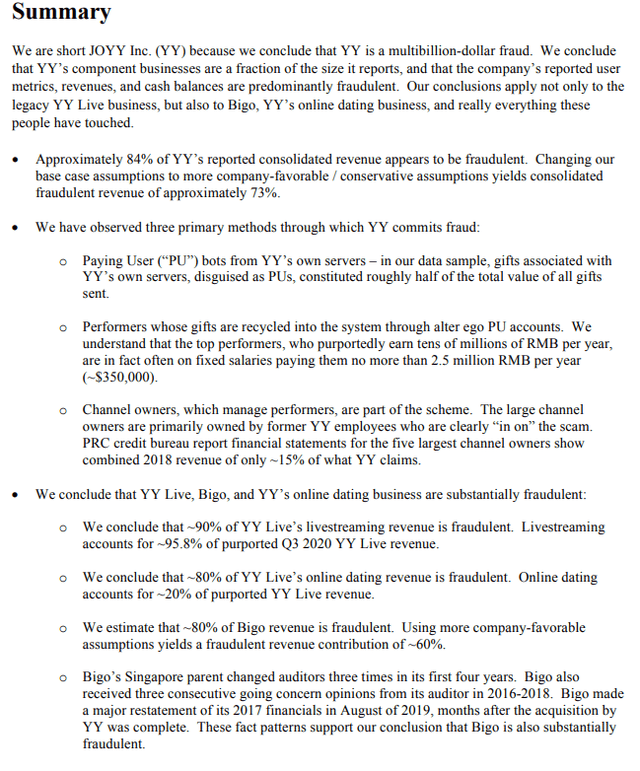

Here is the summary of the report but I urge you to go through it if you are interested in JOYY stock or just for investing education.

JOYY stock analysis – Muddy Waters Report

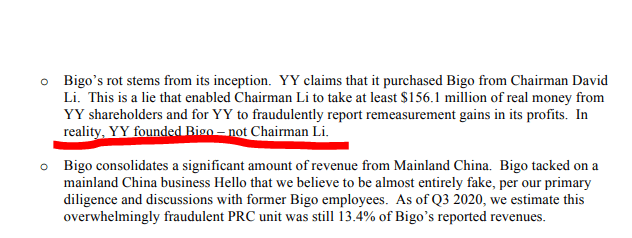

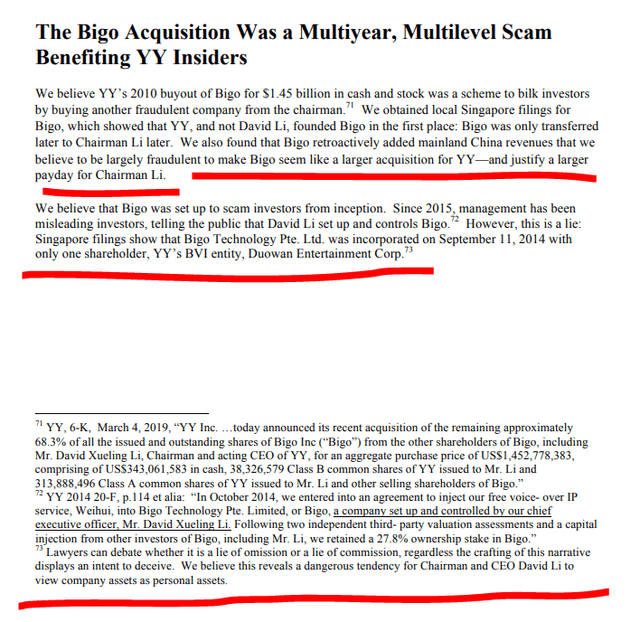

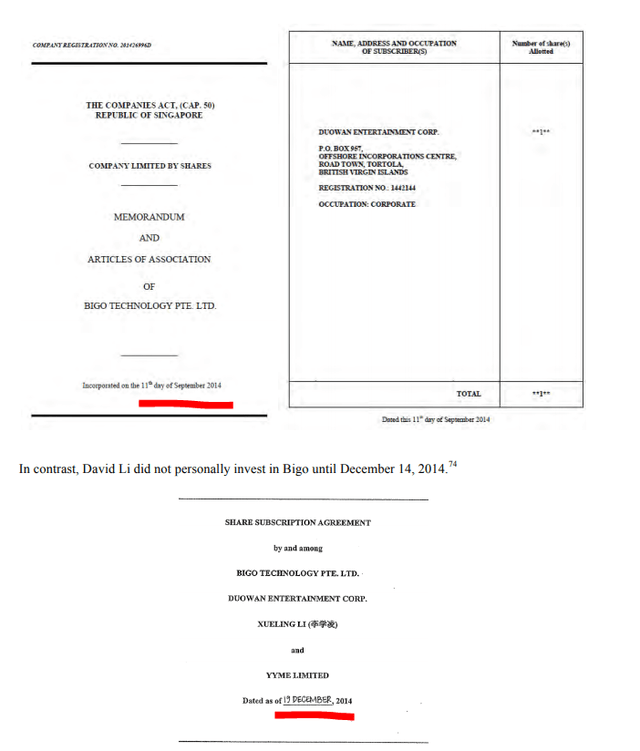

The summary of the thesis is that the numbers are inflated by bots, how the revenues are overstated and even the channel owners are related to the company. Their fraudulent estimation for Bigo is that 60% of is simply fake. To note, Bigo changed 3 auditors before they were bought out by YY and the CEO got his money. Muddy Waters states how actually YY founded Bigo and the acquisition was just a way for the Chairman Li to get money.

JOYY stock analysis – Muddy Waters Report

JOYY stock analysis – Muddy Waters Report

Bigo was founded in September 2014 and the Chairman invested in December.

JOYY stock analysis – Muddy Waters Report

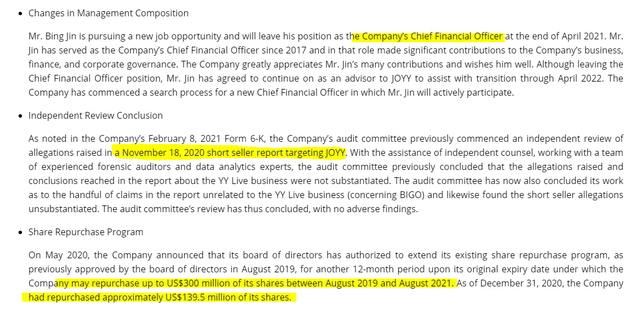

This is pretty big and the company hasn’t actually said the above is not true. The just refuted the report and said they will do more buybacks to show their conviction in the cash flows.

JOYY stock analysis – Company statement

They recently released a statement saying how an audit committee checked the Muddy Waters remarks and obviously said nothing has been found.

JOYY stock analysis – Forecast – Source: 2020 Earnings report

I went and checked the Form 6-K where I expected a detailed rebuttal of Muddy’s thesis. The form is equal to the statement above.

JOYY stock analysis – Muddy Waters Rebuttal – Source: JOYY 6-K

Baidu has backed the above statement but we haven’t seen the actual audit reports.

Baidu’s Muddy Waters perspective – Source: Baidu’s listing prospectus

I have looked a bit across the web and all the Muddy Waters rebuttals were related to how the market doesn’t agree with Muddy. Well, the market might be blind to fraud for a long time before something actually happens. It took 14 years for the Wirecard fraud to materialize itself.

JOYY stock investment thesis

We will see whether Muddy is right or not sometime in the future, but for me the risk of owning second grade apps that compete with Facebook or Google on a global scale, is too much given that I have to discount the cash and the value of the apps might actually be zero. For me, this is not a value investment.

Given the search trends on Google, the terrible quality content on JOYY’s apps, the growth financed by looping revenues and high advertisement spend, I would not invest in JOYY because I feel the risk there is huge. It might materialize, it might not, but why not go for more certainty when it comes to investing.

I don’t disagree with the price targets investment banks have on JOYY. If the company announces fast growth in traffic and revenue on its apps in the coming earnings calls alongside a big fat dividend when the YY Live money comes in, the stock might easily go to $150.

YY stock price targets – Source: Bank reports

However, that is not investing for me. I am a long-term investor and I seek businesses that will be still doing business in 10 to 20 years with a high degree of certainty, that have the possibility to grow and are fairly priced. YY stock might be fairly priced but the risk of Bigo and Livee being worthless in the future is too big to call this a value investment. Alongside the potential fraud in revenue growth numbers, number of downloads and active users.

YY stock price forecast

On one hand, YY stock can easily go up if the company spends on buybacks and increases the dividend so I wouldn’t rush into shorting this. On the other hand, the business is unlikely sustainable long-term which means it is not a great value investment, perhaps a ‘one last puff’ Benjamin Graham style, but be careful with those because for a margin of safety, the market can should be below $4 billion. All in all, too complex for me and I haven’t even made valuation as I do usually because the numbers simply don’t fit for me.

Sven Carlin Valuation Template – Free Dowload

If you wish to receive new analyses into your inbox, subscribe to the newsletter.