TSM Stock Looks Good – Intel Scenario Is Biggest Risk

TSM stock – TSMC – NYSE: TSM – Taiwan Semiconductor Manufacturing Company

TSM stock analysis is part of my research into the chip sector that has high growth potential over the next few years. Here is a video discussing TSM stock for those who prefer watching. Article continues below.

TSM stock price overview

TSM stock has been an amazing compounder over the years and it is actually more than a 100 bagger.

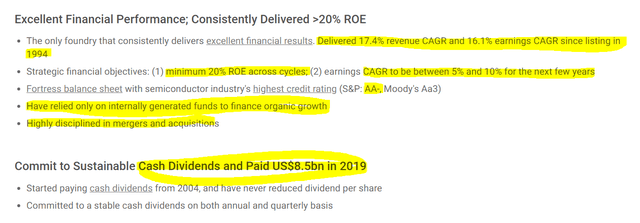

The reason for such an amazing stock performance are the fundamentals shown in the figure below. This is also what one should look for when investing in companies; a good growing market, high returns on equity, a strong balance sheet that makes you survive the cycles, organic growth that is possible thanks to a profitable operation.

However, it is also on the top of the list of MSCI emerging market index which means it has the largest market capitalization and thus could also be an expensive stock.

Let’s look at the business, fundamentals and investing outlook and finish with a TSM stock valuation. The management expects low teens growth over the next few years.

TSM stock analysis – business overview

Taiwan Semiconductor (TSMC) is the world’s largest semiconductor foundry, it manufactures a lot of the chips that are in your phone and computer. Its total foundry market share of 56% and it is about to spend $28 billion in 2021 to keep that position and to dissuade competitors from entering the field (constructing plant in Arizona too for US market). Given the environment we are in, the company must anticipate a huge surge in chipmaking, especially advanced chips. It is not yet known whether TSMC expected to get also a share of INTEL’s chip production as the company said earlier it has been exploring outsourced production but the new CEO recently said how most will still be kept inhouse. Perhaps TSMC will lower its CAPEX in 2021, we will see.

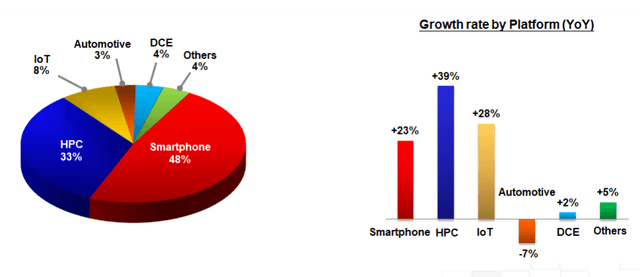

Smartphones are currently contributing to most of the revenue but as other segments like IoT, automotive and other grow, this might change over time and further grow both the top and bottom line for TSMC.

All in all, global market leader in chip manufacturing making the chips for many companies, from Apple to Qualcomm. The sector is a growth one which is always a good tailwind when investing; if you make a mistake, the growth in demand might save your investment while if you nail the right business, you can expect great returns.

TSM stock fundamental analysis

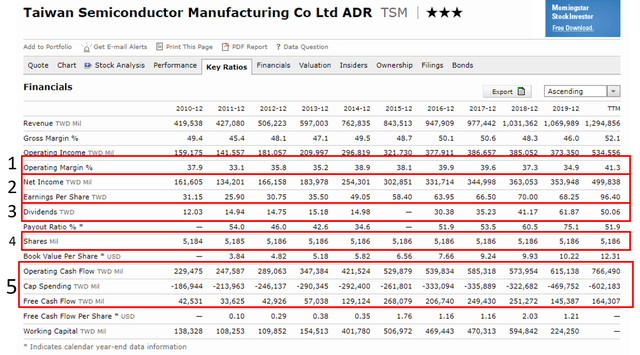

Operating margins (1) have been improving over time but we must always keep in mind the high cyclicality of the sector as in exuberant periods there can easily be overcapacity that lowers margins like it had been the case in 2011 to 2013.

Net income (2) has been growing at a steady pace alongside earnings and dividends (3) and what is very important is that the company achieved it all without issuing any shares (4) like many current growth stocks do.

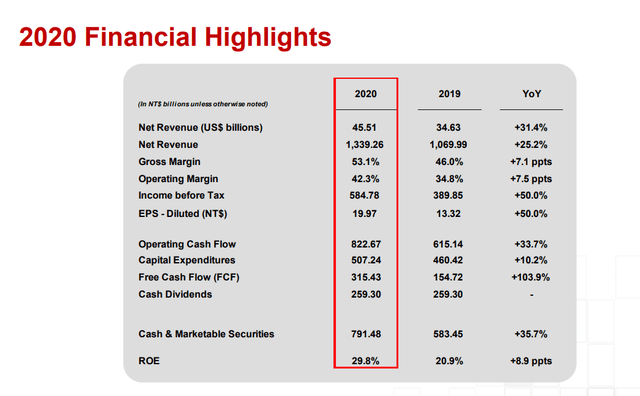

Operating cash flows have tripled and free cash flows quadrupled (5) over the past 10 years and even more in 2020 where free cash flows expanded to $9.25 billion.

Total liabilities are just 32.16% of total assets and long-term liabilities are just 9.83% of total assets which puts TSMC in a very strong financial position.

For reference:

TSMC’s functional currency is TWD

TSM stock intrinsic valuation

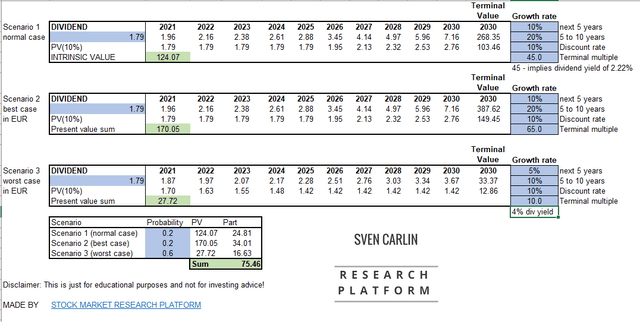

For a valuation I am going to take the dividend that quadrupled over the last decade. I am focusing on the dividend because that is how the company rewards its shareholders as the other 50% of net income is reinvested into growth. As long as they keep reinvesting the equity at an ROE of above 20%, shareholders have nothing to worry.

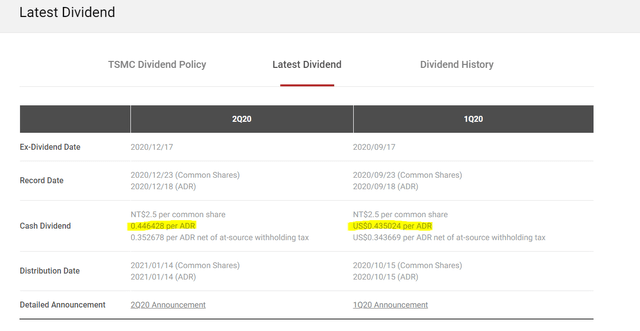

The last quarterly dividend was $0.446428 per ADR which multiplied by 4 is $1.7857 for a dividend yield of 1.367%. TSMC’s dividend policy is to increase or at least keep the dividend stable.

Over the last ten years top line growth was around 11% and the dividend grew at 15%. Given the outlook is not for 11 to 15% revenue growth, I’ll estimate 15% dividend growth over the coming decade, slower now as huge capex is expected, bigger later.

The above calculation tells me that what is currently priced in TSM stock is similar execution to the last 10 years and a stable valuation for 10 years where investors are happy with a 1.5% dividend yield and growth in the best case scenario or 2.22% yield in the normal case scenario assuming the required yield increases to 2.2%. We could say the market is pricing in low required yields for the next decade in this case.

In a worst-case scenario (actually the Intel scenario), where the expected dividend yield in 2030 would be 4%, the present value is a bit less than half of the current stock price with all estimations keeping a stable growth rate which we know is not something natural for the semis industry.

TSM stock investing conclusion

I would say that if you own TSM stock you have to expect a lot of volatility and therefore adjust your exposure in line with the portfolio impact volatility can have. TSMC is priced for perfection thanks to its technological advantages, global scale and extremely strong market position alongside the collaboration with companies like Apple and Qualcomm. However, always keep in mind the cycle in the industry because things change very quickly.

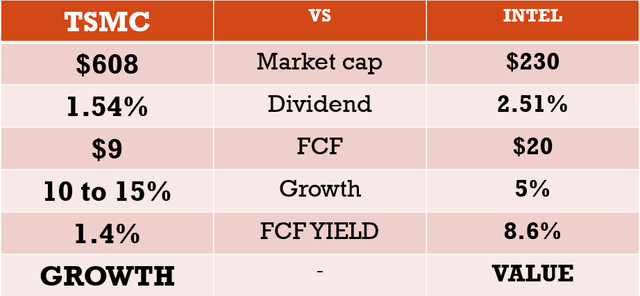

TSM stock vs Intel stock

A good example of how things can change is Intel. Further, my Intel stock analysis shows what can happen to a company if it loses its advantage over the cycles. Compared to TSM, Intel is a cheap stock and perhaps the best description of the risk of investing in TSM now.

Intel’s free cash flows are around $20 billion while TSMC’s are at $9.25 billion where Intel’s market capitalization is at $230 billion where TSMC’s is at $608 billion. I guess the investing depends more on what kind of an investor you are; a value investor looking for a margin of safety and cash flows will likely pick Intel while a growth investor will stick to TSMC.

Comparison with INTC

All in all, TSM stock looks good and fairly priced for a growth stock in the current environment and therefore, the biggest risk is actually its valuation in what is clearly a cyclical and fast changing environment. Manage your exposure accordingly.

TSM stock is a stock that I watch and follow on my stock list that you can check here: Sven Carlin Stock Market Research Platform.