Tesla at a Crossroads: Separating Vision from Investment Reality

If you want a deep dive into Tesla stock, watch the full video about the Magnificent 7 Stocks:

The Tesla investment thesis has always been a story of contradictions – a company that simultaneously represents the most exciting possibilities of technological innovation and the most glaring examples of market irrationality. As we examine Tesla’s current position, we find a company at a critical juncture, where its visionary promises are increasingly colliding with financial and operational realities. This comprehensive analysis aims to cut through the hype and examine whether Tesla’s stock represents a compelling investment opportunity or a cautionary tale of overvaluation.

The Financial Picture: Cracks in the Foundation

Tesla’s financial performance in recent quarters has revealed troubling signs that go beyond normal cyclical fluctuations. After years of seemingly unstoppable growth, the company reported its first year-over-year decline in vehicle deliveries in Q1 2024, with an 8.5% drop that shocked many investors. This decline wasn’t merely a blip but reflected deeper challenges: intensifying competition in major markets, saturation in its premium customer base, and the limits of its price-cutting strategy.

The financial statements tell an even more concerning story. Revenue growth has slowed dramatically from its historical 50%+ annual pace to low single digits. More alarmingly, net income has plummeted by 55% year-over-year as the company’s aggressive price reductions – implemented to maintain sales volume – have severely compressed margins. Perhaps most telling is the deterioration in free cash flow, which turned negative to the tune of $2.5 billion in Q1 2024 after being consistently positive in prior years.

A deeper examination of Tesla’s profitability reveals an even more troubling pattern. The company’s financial health has been significantly bolstered by regulatory credits – essentially payments from other automakers needing to offset their emissions. These credits contributed $1.8 billion to Tesla’s bottom line in 2023 alone. When we exclude these essentially artificial earnings, Tesla’s core automotive business has barely broken even over the past decade, raising serious questions about its fundamental economic viability.

The Autonomous Future: Promise Versus Practicality

Tesla’s investment case increasingly rests on its potential to dominate future autonomous vehicle markets, particularly through its much-hyped robotaxi ambitions. While this vision captures imaginations, a sober analysis reveals significant challenges.

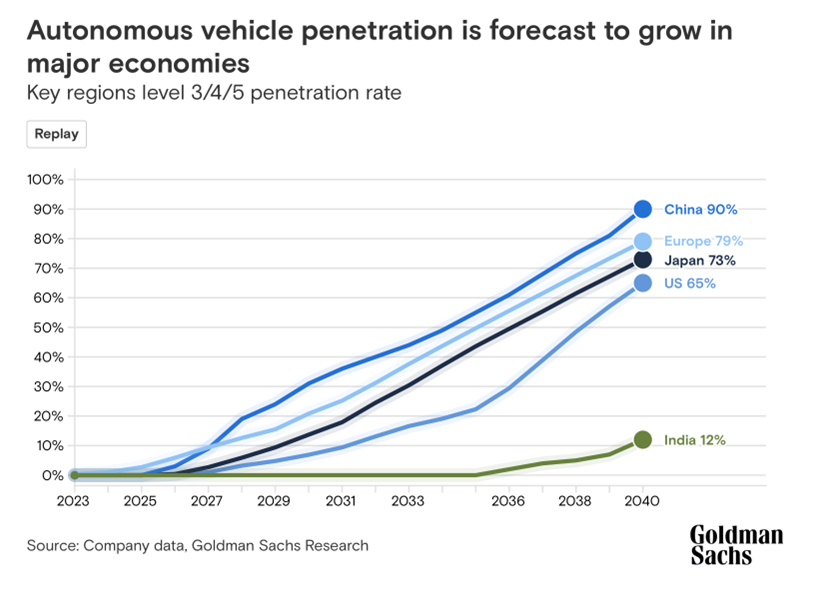

Technologically, Tesla’s Full Self-Driving (FSD) system remains stuck at Level 2 autonomy despite more than a decade of development and countless promises of imminent breakthroughs. This puts Tesla behind competitors like Waymo and Cruise in actual autonomous capability, not to mention several Chinese EV makers who are making rapid progress in real-world testing environments.

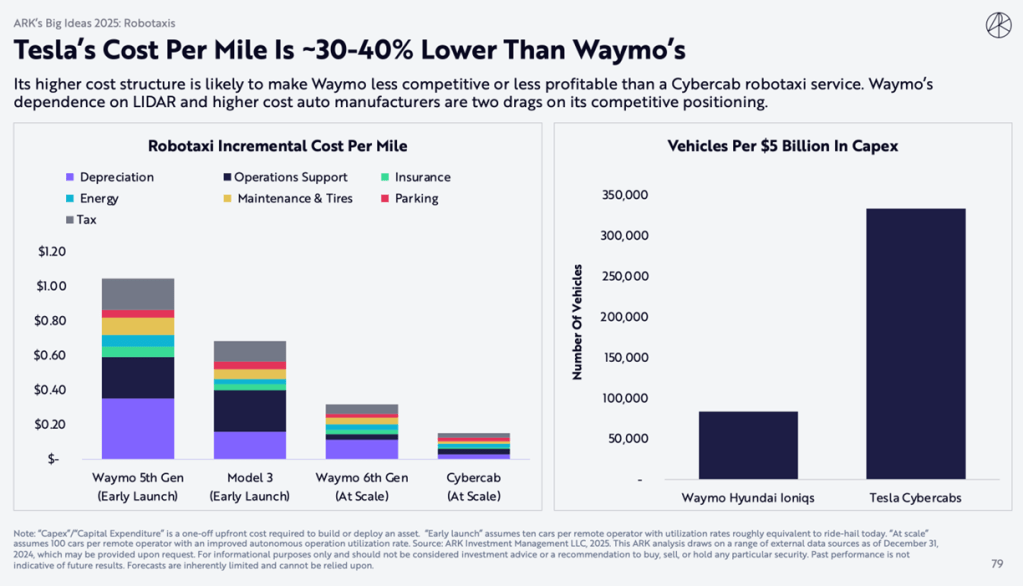

The economic assumptions underlying the robotaxi narrative appear even more questionable. Some bullish analysts, particularly those at ARK Invest, have projected a $10 trillion market for autonomous taxis – a figure representing about 12% of global GDP. More grounded analyses from Goldman Sachs and S&P Global suggest the total addressable market might reach $174 billion by 2040 – still substantial but orders of magnitude smaller than the most optimistic projections.

Even if we accept the more bullish scenarios, Tesla faces intense competition in this space. Chinese manufacturers like BYD and Xpeng are advancing their autonomous technologies at lower cost points, while traditional automakers maintain the capability to repurpose existing vehicle platforms if the autonomous market materializes. Tesla’s first-mover advantage, if it ever existed, is rapidly eroding.

Valuation: The Grand Disconnect

Tesla’s current market valuation presents perhaps the most glaring contradiction in its investment case. The stock trades at approximately 50 times forward earnings, compared to 15 for Toyota and just 5 for Ford. Similarly, its price-to-sales ratio of 6 stands in stark contrast to the 0.5 multiple typical of legacy automakers.

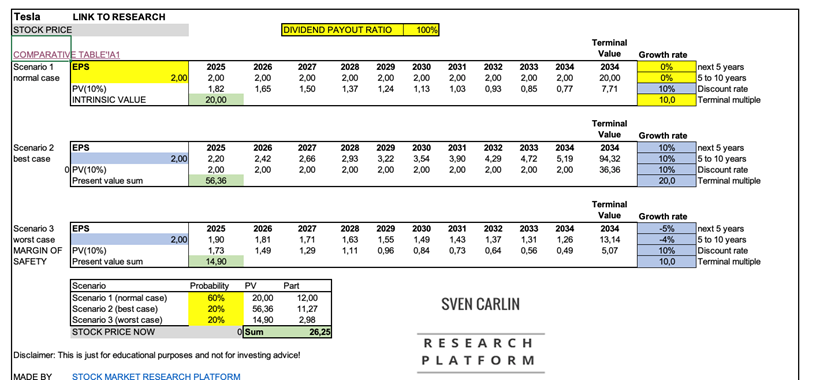

To understand how extreme this valuation is, consider a conservative discounted cash flow analysis. If we assume no growth and the gradual phase-out of regulatory credits – hardly pessimistic assumptions given recent trends – Tesla’s intrinsic value falls below $20 per share, compared to its current price around $175. Even moderately bullish scenarios struggle to justify the current valuation:

In a best-case scenario assuming 15% annual growth and a generous 30x terminal multiple, the stock might be worth $300. More realistic base-case assumptions (5% growth, 15x multiple) suggest $80 per share, while a bear case accounting for declining sales points to $20.

Structural Challenges: Beyond the Hype

Several fundamental challenges threaten Tesla’s business model:

- Margin Compression: The EV price wars, particularly in China and Europe, are destroying profitability across the industry. Tesla’s ability to maintain premium pricing while competing with lower-cost Chinese manufacturers appears increasingly doubtful.

- Execution Risks: The troubled rollout of the Cybertruck – with its production delays and cost overruns – exemplifies Tesla’s growing pains in manufacturing. The apparent delay of the promised $25,000 Model 2 in favor of doubling down on robotaxis raises further questions about strategic focus.

- Leadership Concerns: Elon Musk’s attention is famously divided among multiple ventures (SpaceX, X, xAI, Neuralink). Recent high-profile executive departures, including Drew Baglino and Rohan Patel, suggest potential turmoil in Tesla’s leadership ranks.

Investment Implications: Waiting for Reality to Bite

Given this comprehensive analysis, Tesla stock appears dramatically overvalued by any conventional metric. While the company undoubtedly pioneered the modern EV revolution, it now faces the same competitive pressures and margin challenges that have long plagued the automotive industry.

Conclusion: Vision Without Execution is Hallucination

Tesla’s story serves as a powerful reminder that even the most compelling narratives must eventually face financial reality. While Elon Musk’s vision transformed the automotive industry and made Tesla one of the most valuable companies in the world, the current valuation assumes near-perfect execution of technologies that remain unproven at scale.

As investors, we must distinguish between admiring technological ambition and making prudent capital allocation decisions. Tesla may well achieve its most ambitious goals eventually, but at current prices, investors are paying for success that remains highly uncertain. In the words of Benjamin Graham, “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” For Tesla, the weighing may prove uncomfortable.

The coming years will likely see Tesla’s stock reconcile with its fundamentals – whether through improved operations or price declines. Until then, patient investors would do well to watch from the sidelines, allowing the company’s execution to either validate or disprove its ambitious vision.

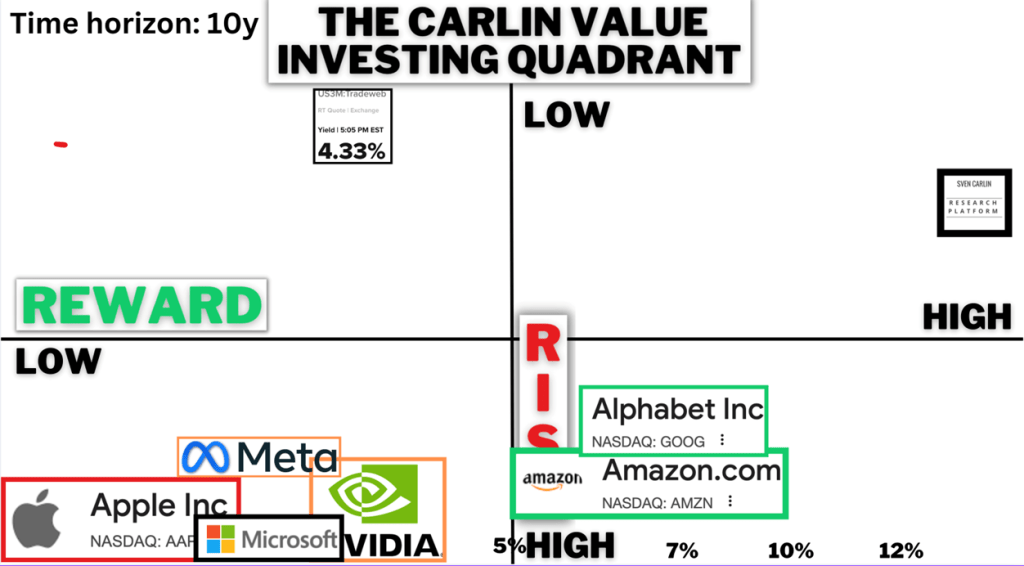

Value Investing Risk & Reward Quadrant (check all the stock analyses)